IonQ CRO Alameddine Rima sells $4.6m in shares

Introduction & Market Context

Mercury Systems (NASDAQ:MRCY) presented its fourth quarter and fiscal year 2025 financial results on August 11, 2025, revealing a significant improvement in profitability and operational efficiency. The defense technology provider's stock closed at $52.83, up 1.7% on the day, reflecting positive investor sentiment ahead of the earnings presentation.

The company has staged a remarkable turnaround from its challenging third quarter, when it reported an EPS miss of -$0.33 against forecasts of $0.10. The fourth quarter results demonstrate substantial progress in Mercury's strategic initiatives focused on predictable performance, organic growth, margin expansion, and improved free cash flow.

Quarterly Performance Highlights

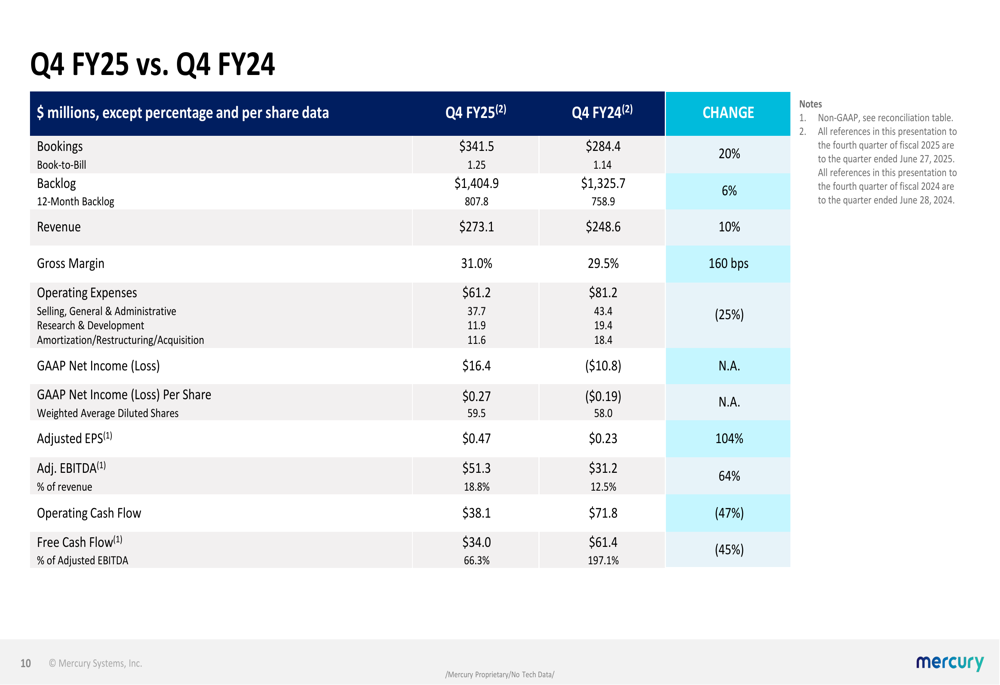

Mercury Systems reported robust fourth quarter results, with revenue reaching $273.1 million, a 9.9% increase year-over-year. More impressively, adjusted EBITDA surged 64% to $51.3 million, representing an 18.8% margin – a sequential improvement of over 700 basis points.

The company achieved record quarterly bookings of $342 million, resulting in a book-to-bill ratio of 1.25, indicating strong future revenue potential. Adjusted earnings per share more than doubled to $0.47, compared to $0.23 in the same quarter last year.

As shown in the following quarterly comparison:

Gross margin improved to 31.0%, up 160 basis points year-over-year, reflecting the company's focus on operational efficiency and higher-margin contracts. Free cash flow generation remained strong at $34 million, representing 66.3% of adjusted EBITDA.

Full-Year Financial Results

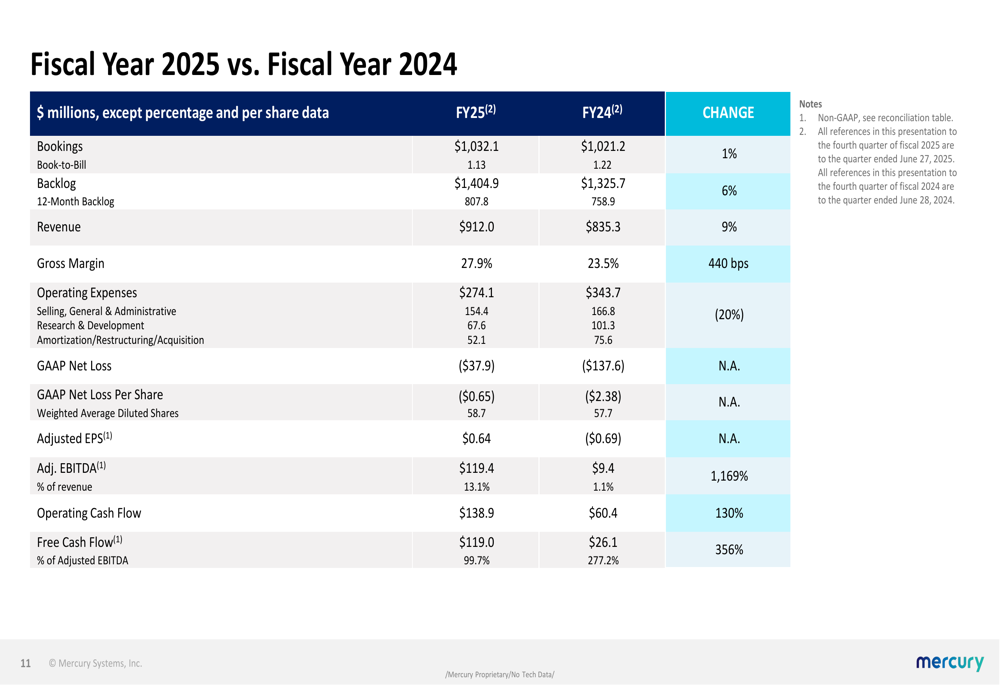

For the full fiscal year 2025, Mercury Systems delivered $912 million in revenue, a 9.2% increase over fiscal 2024. The company's adjusted EBITDA saw a dramatic improvement, soaring 1,169% to $119.4 million, with a margin of 13.1%.

The annual financial comparison highlights this remarkable transformation:

Free cash flow for the year reached $119 million, a 356% increase from the previous year, representing nearly 100% of adjusted EBITDA. This exceptional cash conversion allowed Mercury to reduce its net debt to $282 million, the lowest level since the first quarter of fiscal 2022.

The company ended the fourth quarter with $309 million in cash on hand, providing substantial financial flexibility for future investments and potential acquisitions.

Strategic Initiatives and Margin Expansion

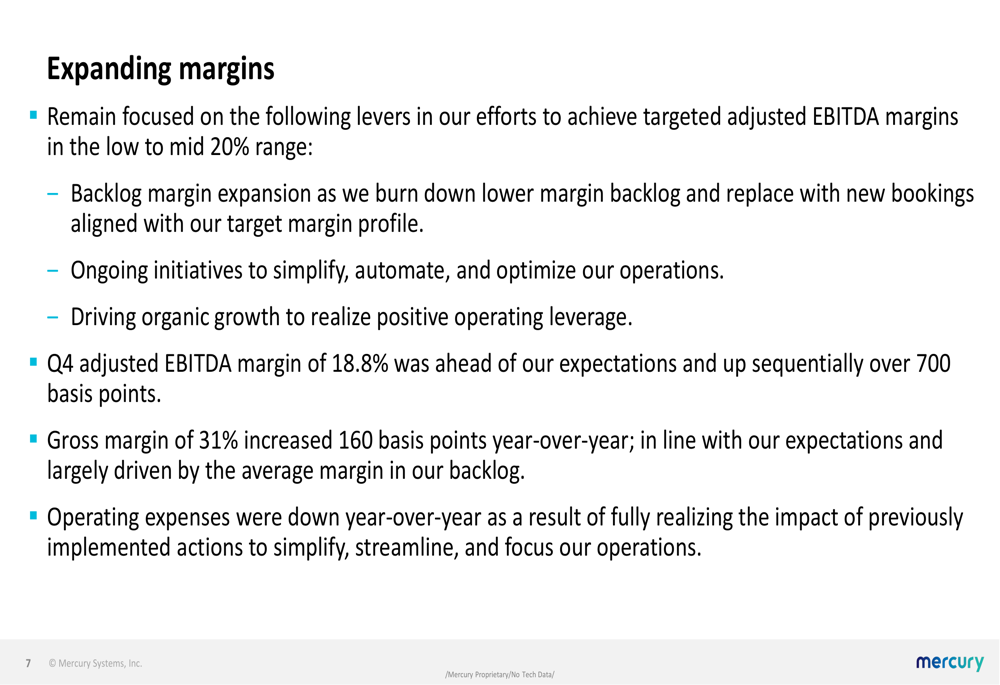

Mercury's management highlighted several key strategic initiatives driving their improved performance. The company has focused on simplifying, automating, and optimizing operations while expanding backlog margins by replacing lower-margin projects with new bookings aligned with target margin profiles.

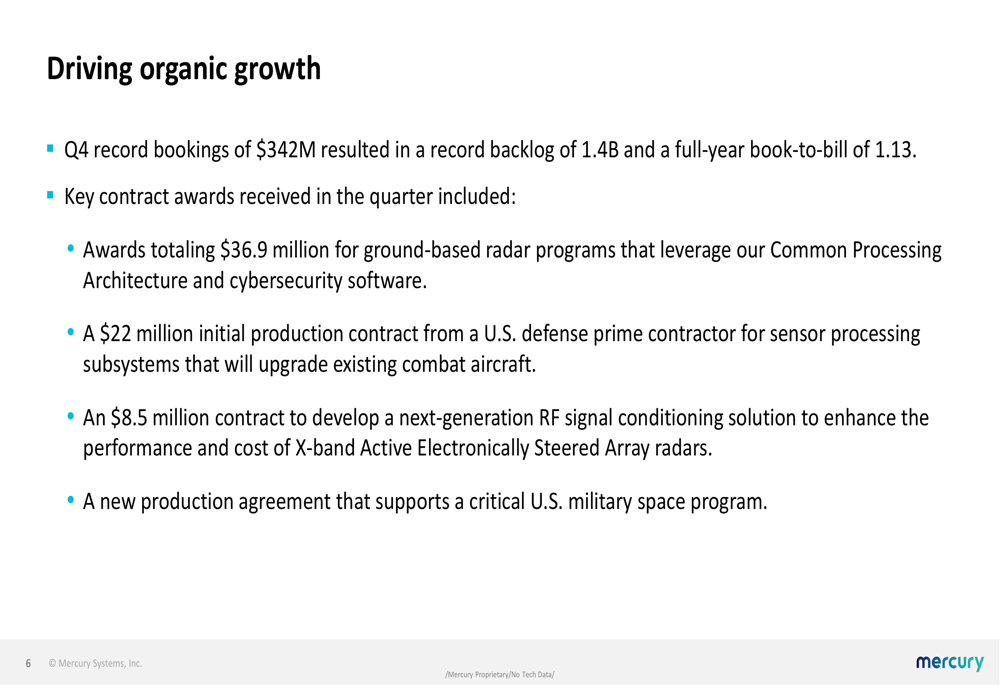

As illustrated in the company's organic growth strategy:

Significant contract wins during the quarter included $36.9 million for ground-based radar programs, $22 million for sensor processing subsystems, and $8.5 million for RF signal conditioning solutions. These awards contributed to Mercury's record backlog of $1.4 billion and full-year book-to-bill ratio of 1.13.

The company's margin expansion strategy has shown tangible results:

Management attributed the margin improvements to reduced operating expenses and positive operating leverage from organic growth. The company remains focused on achieving adjusted EBITDA margins in the low to mid-20% range over time.

Forward-Looking Statements

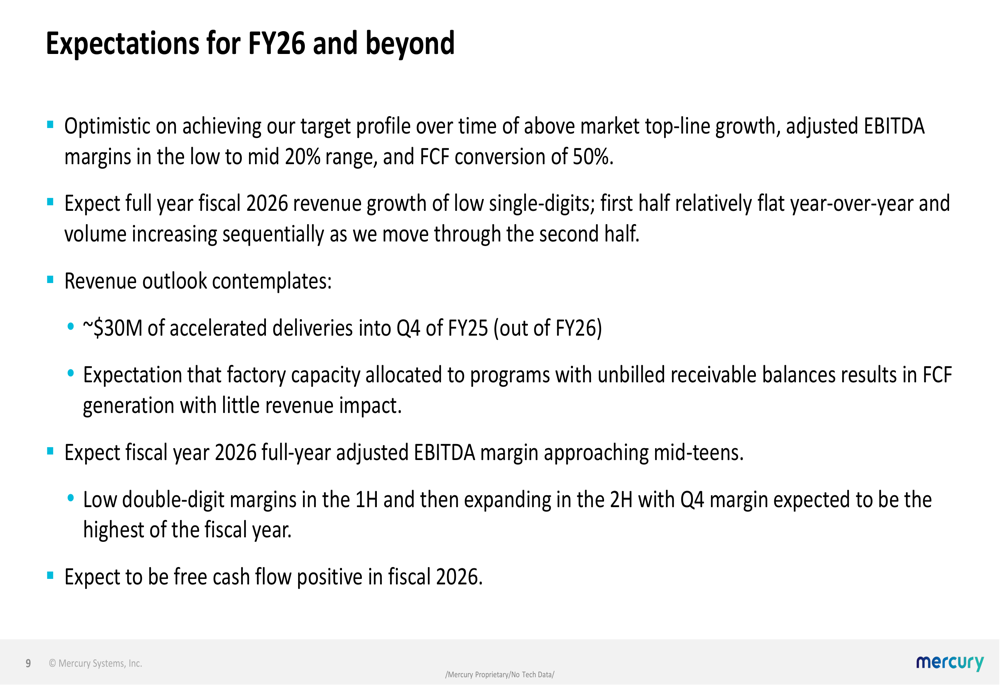

Looking ahead to fiscal 2026, Mercury Systems provided a cautiously optimistic outlook, expecting low single-digit revenue growth with a relatively flat first half followed by sequential increases in the second half.

The company's detailed expectations for fiscal 2026 include:

Management noted that approximately $30 million of deliveries planned for fiscal 2026 were accelerated into the fourth quarter of fiscal 2025. Despite this pull-forward, the company expects adjusted EBITDA margins to approach mid-teens for fiscal 2026, with the fourth quarter projected to deliver the highest margins of the year.

Mercury's long-term financial targets remain unchanged: above-market top-line growth, adjusted EBITDA margins in the low to mid-20% range, and free cash flow conversion of 50%.

Cash Flow and Balance Sheet

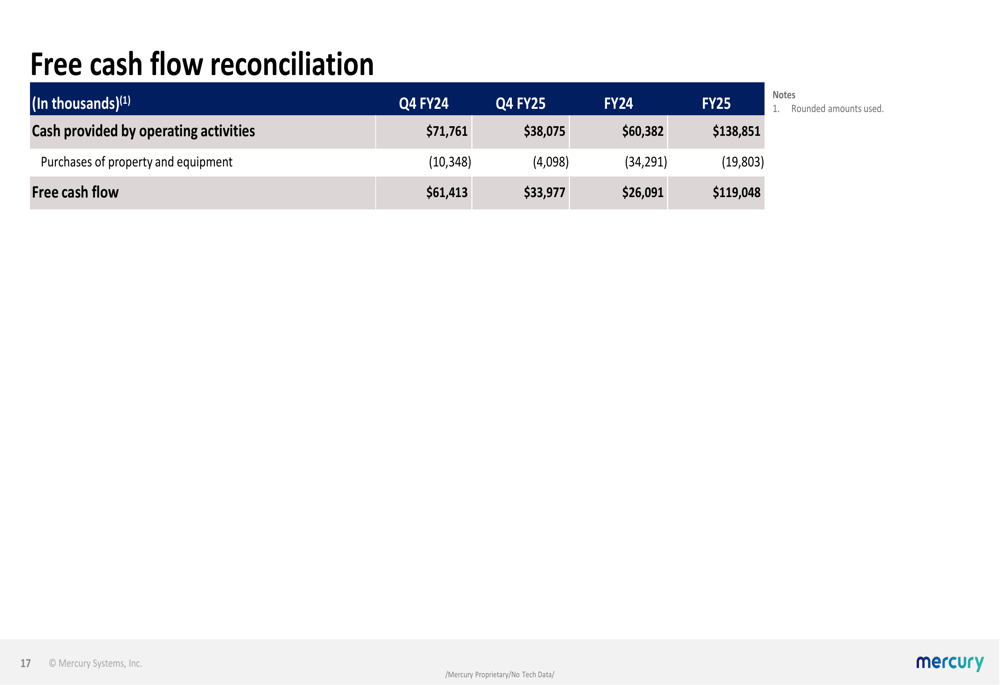

Mercury's improved operational efficiency has translated into stronger cash flow generation. The company has made significant progress in reducing working capital, which is down $211 million from peak levels in the first quarter of fiscal 2024.

The free cash flow reconciliation demonstrates this improvement:

This enhanced cash generation has strengthened Mercury's balance sheet and reduced its financial leverage, providing greater flexibility to pursue strategic opportunities while maintaining financial discipline.

Mercury Systems' fourth quarter presentation reveals a company that has successfully executed its turnaround strategy, delivering substantial improvements in profitability, cash flow, and operational efficiency. While challenges remain in achieving consistent growth and further margin expansion, the foundation appears to be in place for continued financial improvement in fiscal 2026 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.