Oklo stock tumbles as Financial Times scrutinizes valuation

Introduction & Market Context

Merit Medical Systems, Inc. (NASDAQ:MMSI) reported its second quarter 2025 financial results on July 30, showcasing strong revenue growth and record non-GAAP operating margins. The medical device manufacturer, which specializes in cardiac and endoscopy products, continues to execute on its growth strategy through both organic expansion and strategic acquisitions.

Despite the positive financial performance, Merit’s stock experienced a premarket decline of 1.61%, trading at $78.15 following the earnings announcement. This movement contrasts with the broader market trends and may reflect investor caution despite the company’s operational achievements.

Quarterly Performance Highlights

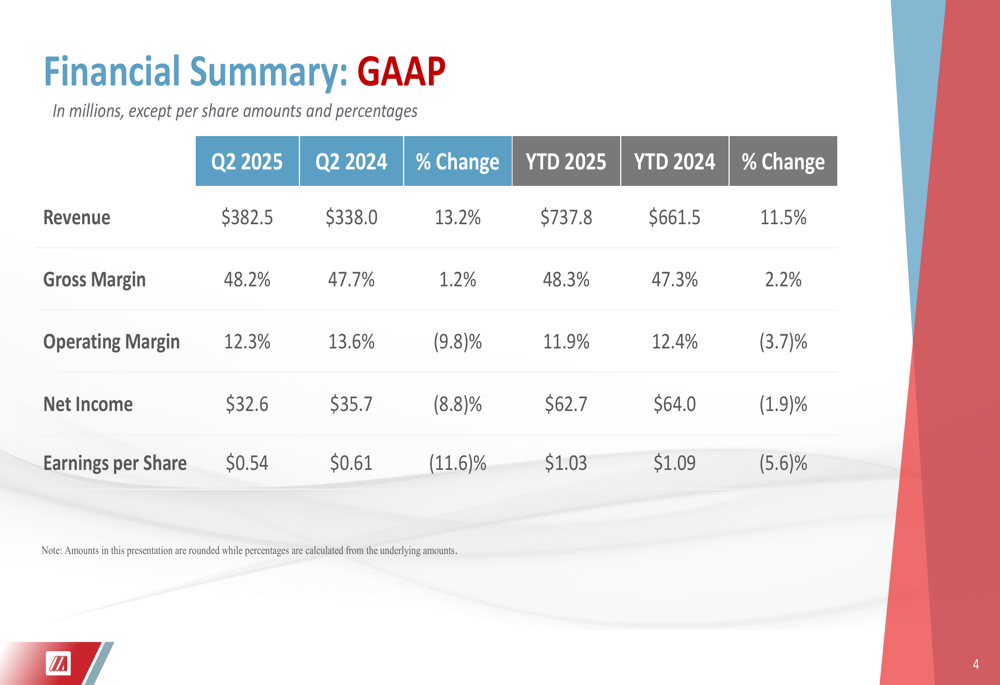

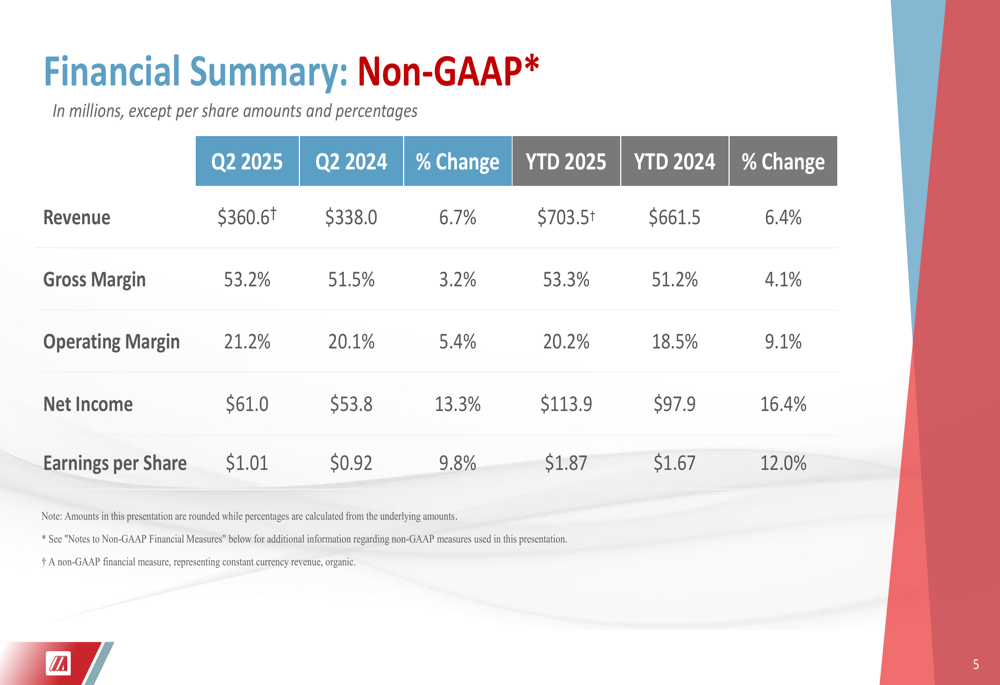

Merit Medical delivered robust financial results for Q2 2025, with total revenue reaching $382.5 million, representing a 13.2% increase compared to the same period last year. On a non-GAAP basis, which accounts for currency fluctuations and organic growth, revenue grew 6.7% to $360.6 million.

The company achieved its highest non-GAAP operating margin in company history at 21.2%, an improvement of 5.4% compared to Q2 2024. This margin expansion demonstrates Merit’s ability to drive operational efficiencies while growing its top line.

As shown in the following financial summary:

On a GAAP basis, Merit’s gross margin improved to 48.2%, up 1.2% year-over-year. However, GAAP operating margin declined by 9.8% to 12.3%, and earnings per share decreased by 11.6% to $0.54. These declines were primarily due to acquisition-related expenses and other one-time costs.

The non-GAAP results paint a more positive picture of Merit’s underlying business performance, with significant improvements across all key metrics:

Merit generated strong cash flow during the quarter, with operating cash flow of $83.3 million compared to $68.5 million in Q2 2024, representing a 21.6% increase. Capital expenditures increased to $13.8 million from $10.6 million in the prior year period, reflecting ongoing investments in manufacturing capacity and infrastructure.

Regional Revenue Analysis

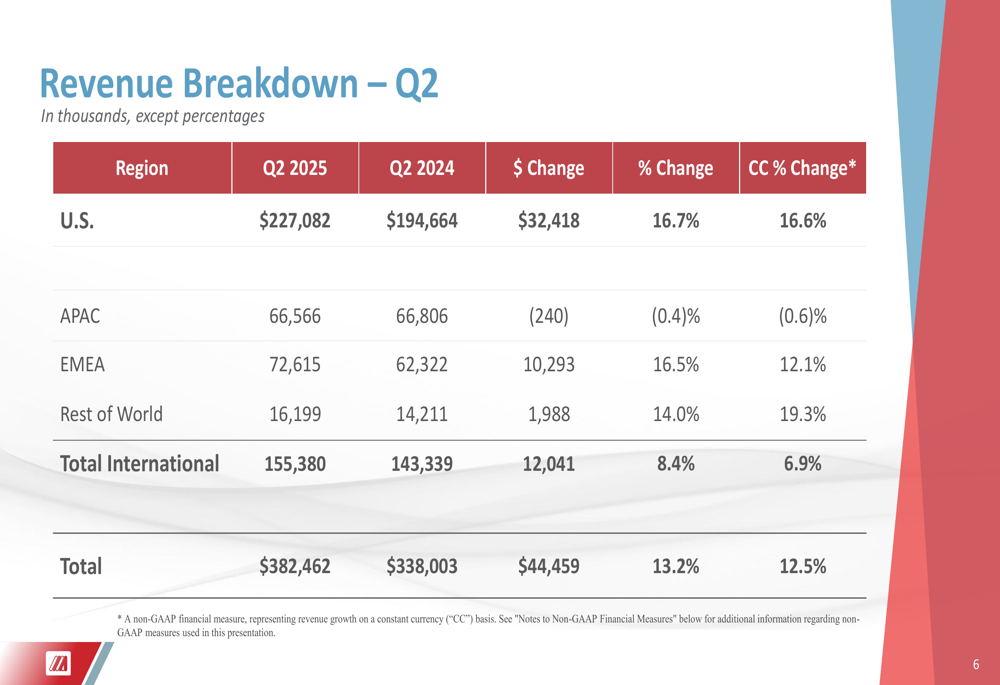

Merit’s revenue growth was driven primarily by strong performance in the U.S. market, which grew 16.7% year-over-year to $227.1 million. The EMEA region also delivered impressive results, with revenue increasing 16.5% to $72.6 million. The Rest of World segment grew by 14.0%.

The APAC region was the only area showing a slight decline, with revenue decreasing by 0.4% to $66.6 million. According to the earnings call transcript, this softness was particularly evident in the Chinese market.

The following breakdown illustrates Merit’s regional performance for Q2 2025:

Year-to-date, Merit’s total revenue reached $737.8 million, an 11.5% increase over the first half of 2024. The U.S. market continued to lead growth with a 15.7% increase, while international markets collectively grew by 5.8%.

Strategic Initiatives and Acquisition

A key strategic development highlighted during the earnings presentation was Merit’s acquisition of BioLife Delaware LLC for $120 million. This acquisition expands Merit’s product portfolio in the hemostatic device market, which is estimated to be worth approximately $350 million globally.

The company also emphasized the upcoming U.S. launch of its Rhapsody CIE product, which is expected to contribute $2-4 million in revenue. During the earnings call, CEO Fred Lampropoulos expressed confidence in this new offering, stating, "We believe the Rhapsody CIE is a completely new treatment option for patients."

Merit also announced a significant leadership transition, with Martha Aronson set to become the new CEO effective October 3, 2025, succeeding Fred Lampropoulos.

Updated Financial Guidance

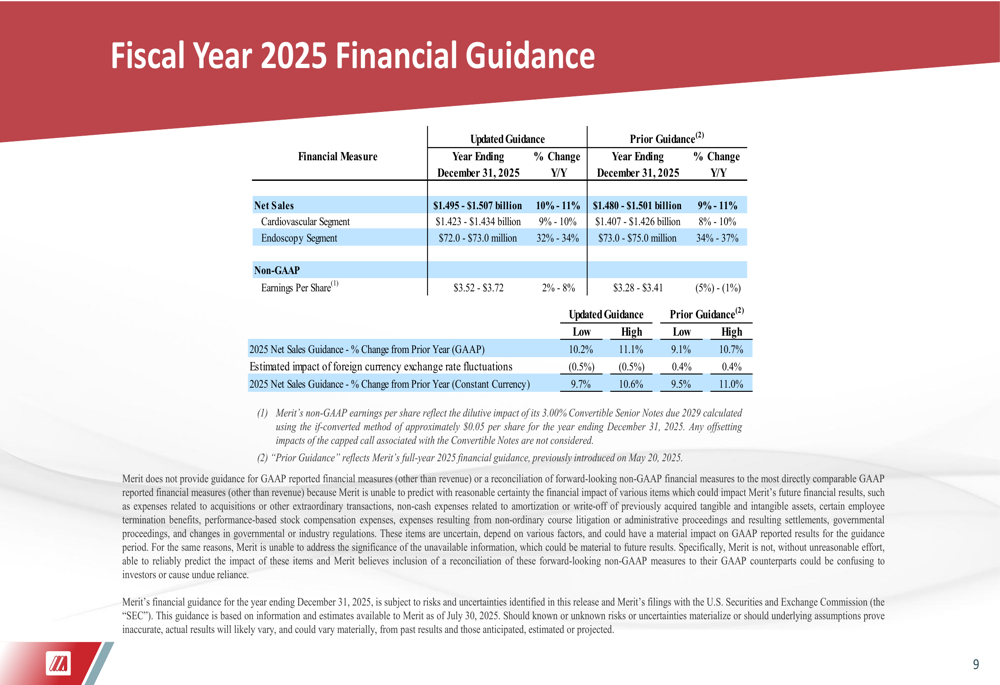

Based on strong first-half performance and confidence in its growth initiatives, Merit Medical raised its full-year 2025 guidance. The company now expects total revenue between $1.495 billion and $1.507 billion, representing year-over-year growth of 10-11%, up from its previous guidance of 9-11% growth.

The updated guidance includes higher expectations for the Cardiovascular segment but slightly lower projections for the Endoscopy segment. Most notably, Merit significantly raised its non-GAAP earnings per share guidance from $3.28-$3.41 to $3.52-$3.72, representing potential growth of 2-8% compared to the previous guidance of -5% to -1%.

The detailed guidance update is illustrated in the following slide:

Market Reaction and Analyst Perspectives

Despite Merit’s strong financial performance and raised guidance, the market reaction was somewhat muted, with the stock declining 1.61% in premarket trading to $78.15. This places the stock near its 52-week low of $78.12, significantly below its high of $111.45.

The disconnect between operational performance and stock price movement may reflect broader market concerns about the medical device sector, potential challenges in the Chinese market, or investor caution regarding the upcoming CEO transition.

According to the earnings call transcript, analysts expressed particular interest in the Rhapsody CIE reimbursement strategy and the expected synergies from the BioLife acquisition. The company also addressed questions about tariff impacts, noting that Merit is redirecting shipments to mitigate these effects.

Merit’s CFO Rahul Parra emphasized the company’s pricing strategy during the call, stating, "We’re gonna hold our premium pricing," suggesting confidence in the value proposition of Merit’s products despite competitive pressures.

While Merit faces challenges including tariff impacts, softness in the Chinese market, and ongoing global supply chain disruptions, the company’s record margins and raised guidance indicate management’s confidence in navigating these headwinds while continuing to execute on its growth strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.