TPI Composites files for Chapter 11 bankruptcy, plans delisting from Nasdaq

Introduction & Market Context

Metallus Inc (NYSE:MTUS) presented its Q1 2025 investor update on May 9, 2025, highlighting sequential improvement in financial performance after a challenging fourth quarter. The specialty metals manufacturer, which rebranded from its previous identity in February 2024, is executing a multi-year transformation strategy while navigating volatile market conditions.

The company’s stock closed at $12.89 on May 8, up 1.55% for the day, but was trading down 3.44% in after-hours at $12.64. This follows a significant drop after Q4 2024 results missed analyst expectations, when shares fell nearly 9% to $14.29.

Q1 2025 Financial Highlights

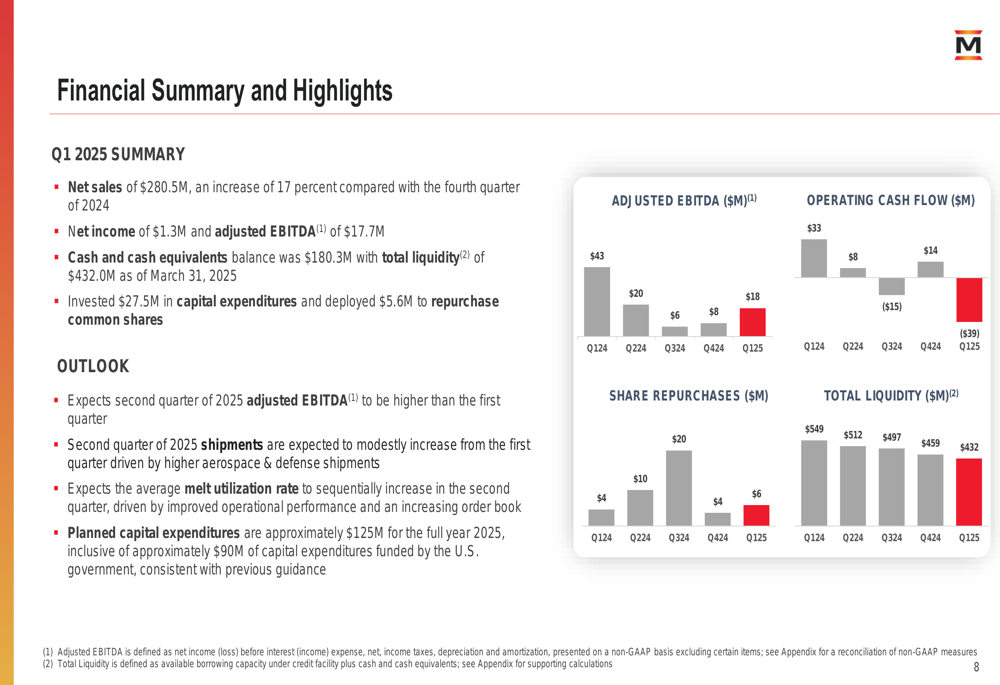

Metallus reported Q1 2025 net sales of $280.5 million, a 17% increase compared to the fourth quarter of 2024. The company returned to profitability with net income of $1.3 million, a significant improvement from the $21.4 million GAAP net loss reported in Q4 2024.

Adjusted EBITDA for the quarter reached $17.7 million, more than doubling the $8.3 million reported in the previous quarter. The company maintained a strong liquidity position with $180.3 million in cash and cash equivalents and total liquidity of $432.0 million as of March 31, 2025.

As shown in the following financial summary chart:

Management expressed optimism about continued improvement, with CFO Chris Westbrooks stating during the Q4 earnings call, "We anticipate first-quarter adjusted EBITDA to be higher than the fourth quarter," a projection that materialized. The company now expects second quarter 2025 adjusted EBITDA to further increase, with modest sequential growth in shipments and melt utilization rates.

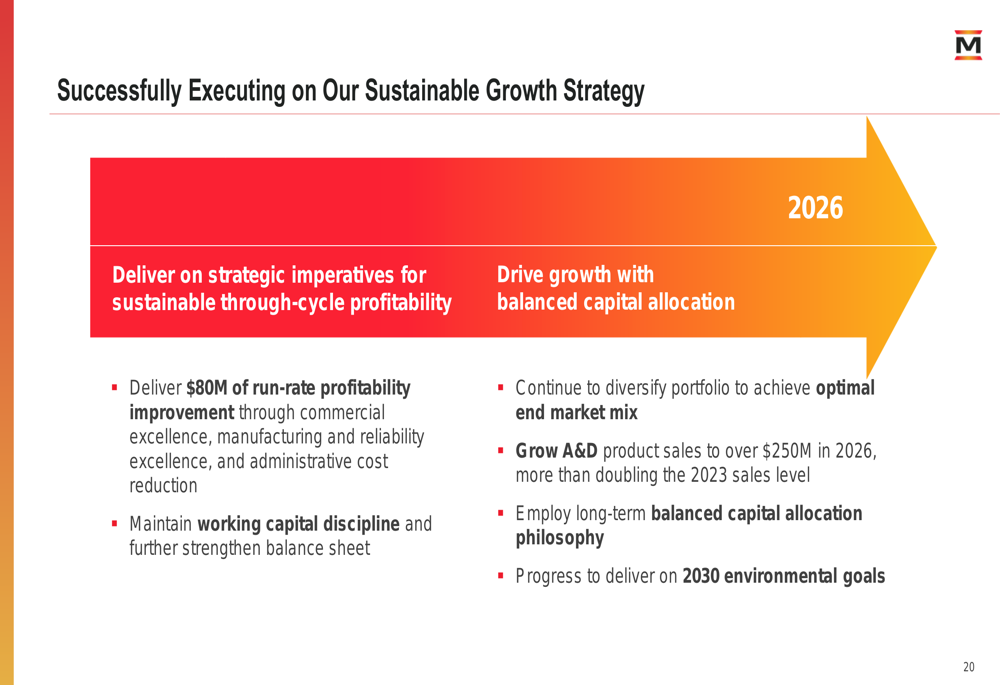

Strategic Growth Initiatives

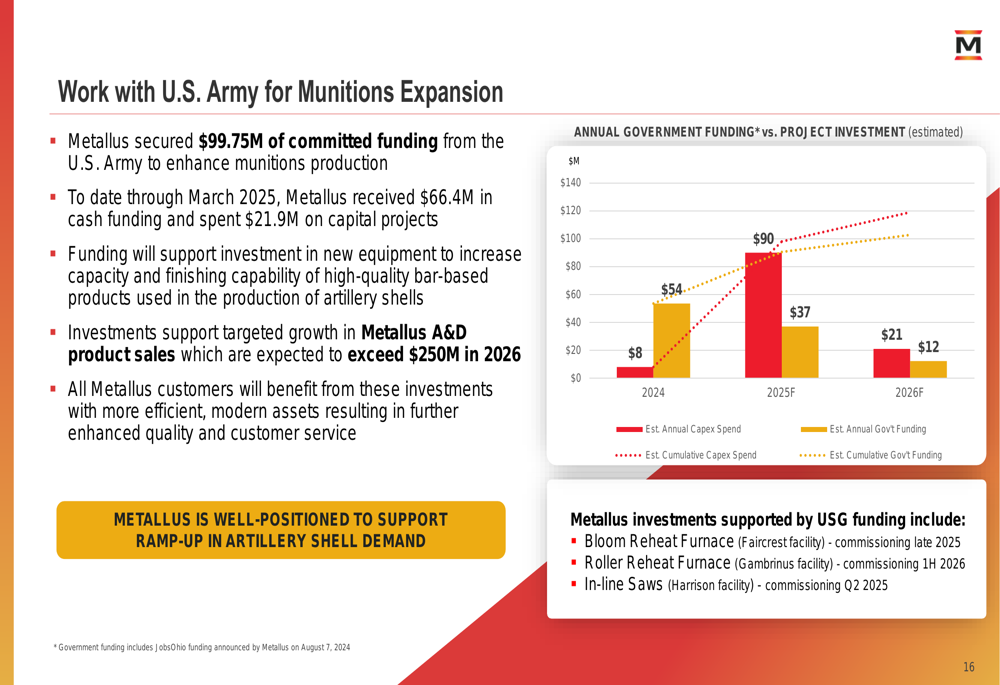

Metallus is pursuing several strategic initiatives to drive growth, with particular emphasis on the aerospace and defense sector. The company has secured $99.75 million in committed funding from the U.S. Army to support munitions expansion, with $66.4 million received through March 2025 and $21.9 million already invested in capital projects.

The following chart details the company’s work with the U.S. Army:

These investments align with Metallus’ goal to grow aerospace and defense product sales to over $250 million by 2026, building on the 17% growth in this segment reported for 2024. The company’s long-standing relationship with the Department of Defense positions it well to capitalize on increased defense spending.

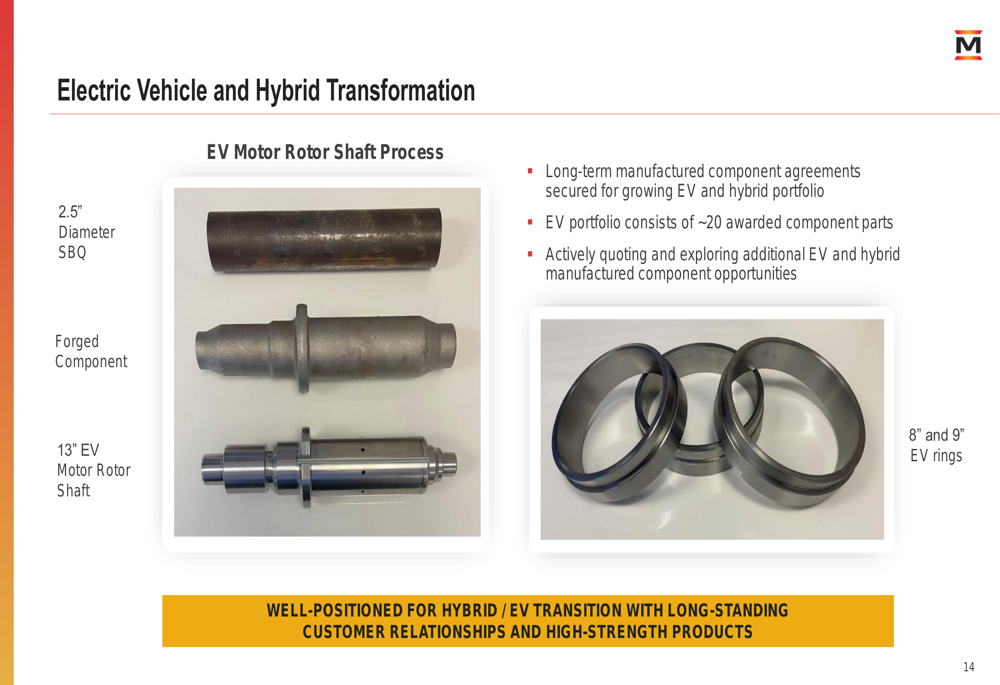

In the automotive sector, Metallus is expanding its presence in electric and hybrid vehicle components, having secured long-term agreements for approximately 20 awarded component parts. The company is actively pursuing additional opportunities in this growing market segment.

As illustrated in the following slide on EV transformation:

End Market Diversification

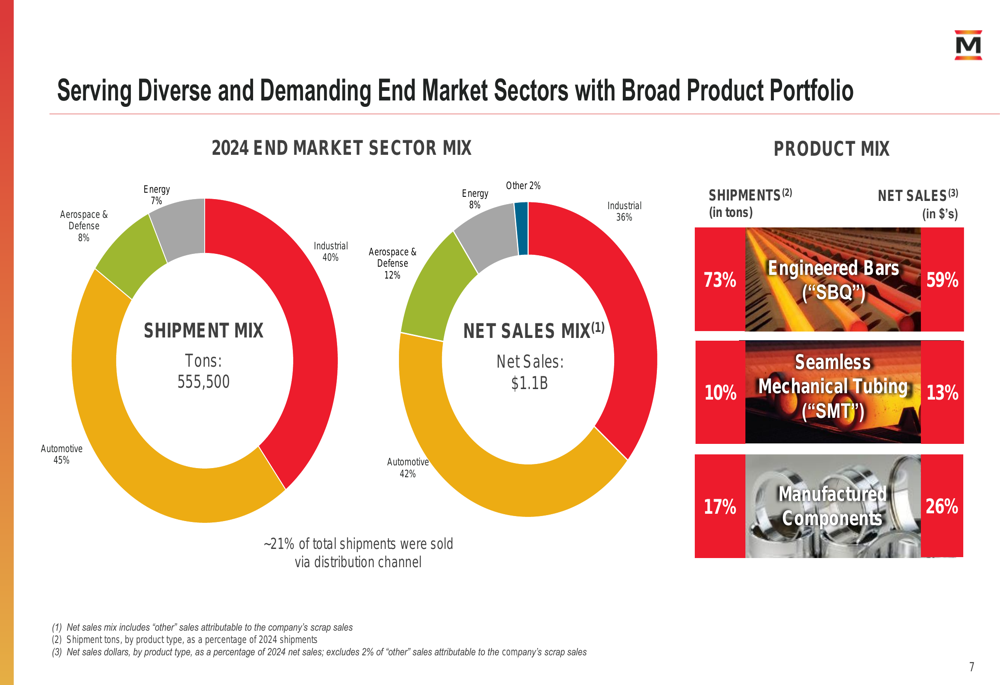

Metallus serves a diverse range of end markets, providing some insulation from sector-specific downturns. In 2024, automotive represented 42% of net sales, followed by industrial at 36%, aerospace and defense at 12%, and energy at 8%.

The company’s product mix consists of engineered bars (73% of shipments, 59% of net sales), seamless mechanical tubing (10% of shipments, 13% of net sales), and manufactured components (17% of shipments, 26% of net sales).

The following chart illustrates this diversification:

This diversification strategy appears to be yielding results, with the aerospace and defense segment providing growth momentum despite challenges in other sectors. The company serves approximately 350 diverse customers, with the majority of relationships spanning more than 20 years.

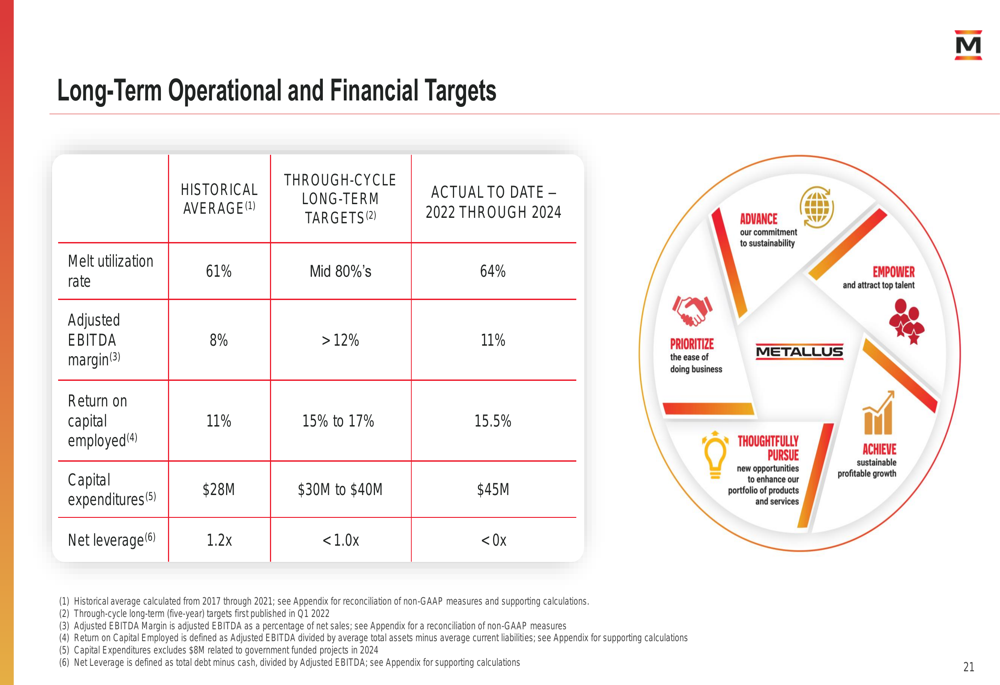

Long-Term Targets & Transformation

Metallus has outlined ambitious long-term operational and financial targets as part of its transformation strategy. The company aims to achieve a melt utilization rate in the mid-80s (compared to a historical average of 61%), an adjusted EBITDA margin exceeding 12% (versus historical 8%), and return on capital employed of 15-17% (versus historical 11%).

As shown in the following targets chart:

To achieve these targets, Metallus is focusing on three key profit drivers: commercial excellence ($30 million), manufacturing and reliability excellence ($30 million), and administrative process simplification ($20 million), for a total of $80 million in run-rate profitability improvements.

The company’s transformation strategy includes:

Capital Allocation & Environmental Goals

Metallus invested $27.5 million in capital expenditures during Q1 2025 and plans approximately $125 million for the full year. The company also deployed $5.6 million to repurchase common shares during the quarter, demonstrating its balanced approach to capital allocation.

The company has established 2030 environmental goals compared to a 2018 baseline, including a 40% absolute reduction in combined Scope 1 and Scope 2 GHG emissions, 30% absolute reduction in total energy consumption, 35% absolute reduction in fresh water withdrawn, and 10% reduction in waste-to-landfill intensity.

Metallus highlights that its use of electric arc furnace (EAF) technology, which produces steel from 100% recycled scrap metal, enables lower greenhouse gas emissions compared to the industry average.

Forward Outlook & Challenges

While Metallus projects improved performance in Q2 2025, the company faces several challenges, including continued weak market demand, high capital expenditures that may strain cash flow, potential impacts from new steel tariffs, and pricing mix challenges that could influence profit margins.

During the Q4 earnings call, CEO Mike Williams emphasized the importance of ongoing investments for long-term growth, stating, "We believe these efforts are key for our long-term growth."

The company’s investment highlights include:

Despite the optimistic outlook presented in the investor slides, Metallus will need to demonstrate consistent execution of its transformation strategy to regain investor confidence following the disappointing Q4 2024 results. The stock’s current trading level, near its 52-week low of $10.78, suggests investors remain cautious about the company’s near-term prospects despite the sequential improvement in Q1 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.