Gold soars to record high over $3,900/oz amid yen slump, US rate cut bets

Introduction & Market Context

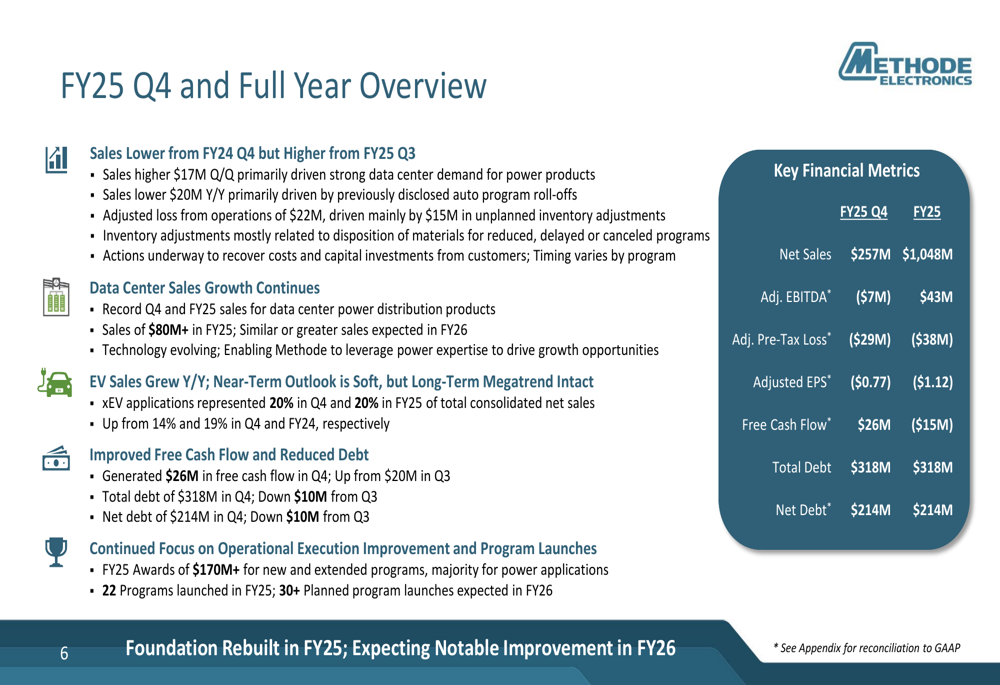

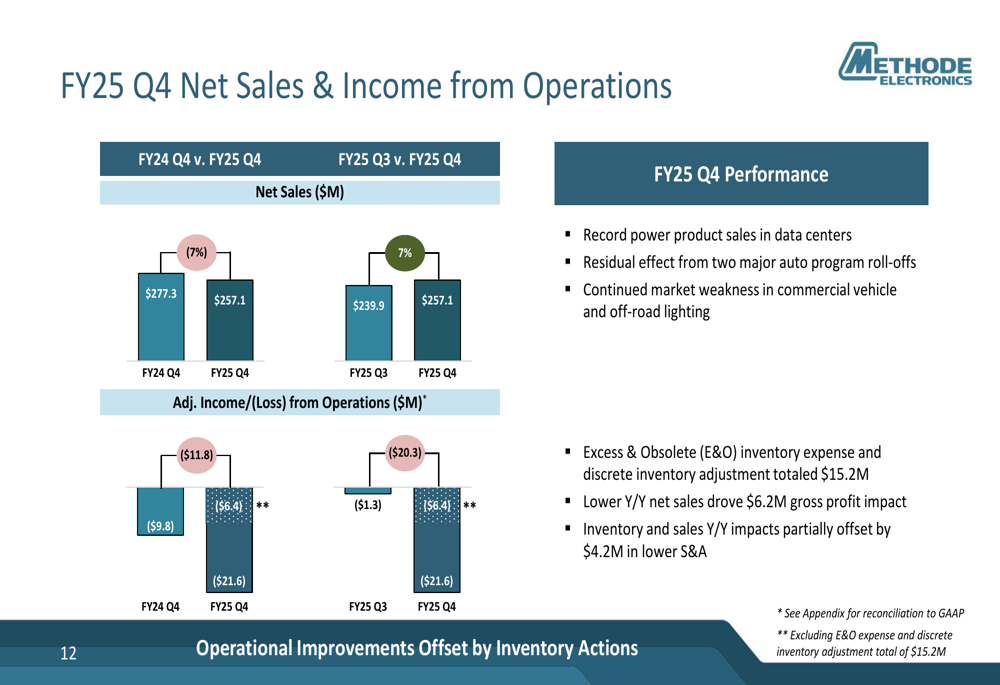

Methode Electronics Inc (NYSE:MEI) presented its fourth quarter and full fiscal year 2025 results on July 10, 2025, revealing continued challenges but also highlighting progress in its transformation strategy and an optimistic outlook for fiscal 2026. The company reported Q4 net sales of $257.1 million, down from $277.3 million in the same period last year but showing improvement from $239.9 million in Q3 FY25.

The automotive and electronics component manufacturer continues to navigate a challenging environment, particularly in the electric vehicle (EV) market, where a slowdown primarily driven by Stellantis (NYSE:STLA) has prompted a reset of EV sales expectations for FY26. Despite these headwinds, Methode’s shares closed at $10.39 on July 9, 2025, near the middle of its 52-week range of $5.08 to $17.45.

Quarterly Performance Highlights

Methode’s fourth quarter results showed mixed performance across key metrics. While sales declined year-over-year, the company achieved significant improvements in free cash flow and saw record performance in its data center power products segment.

As shown in the following comprehensive overview of Q4 and full-year results:

Q4 sales were higher by $17 million compared to Q3, primarily driven by strong data center demand for power products. However, the company reported an adjusted loss from operations of $22 million, largely due to $15.2 million in unplanned inventory adjustments related to reduced, delayed, or canceled programs.

The quarterly net sales and income from operations comparison illustrates both the year-over-year decline and sequential improvement:

Adjusted EBITDA for Q4 FY25 was negative $7.1 million (-2.8% of net sales), a significant decline from both Q4 FY24 ($5.3 million) and Q3 FY25 ($12.3 million). This deterioration was primarily attributed to inventory adjustments, which drove both year-over-year and quarter-over-quarter declines.

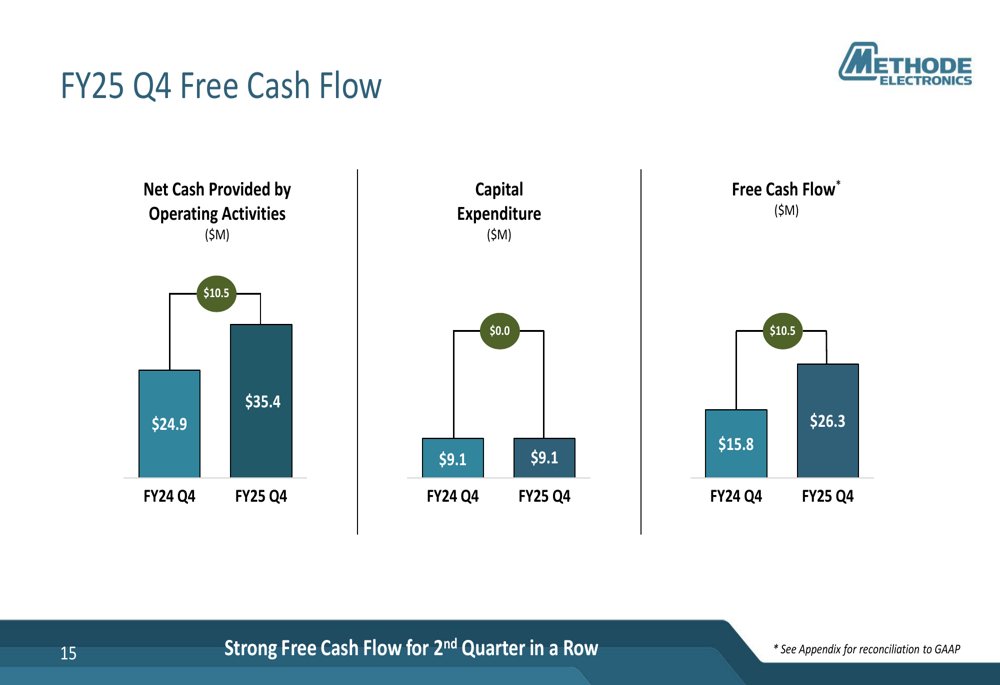

Free Cash Flow & Balance Sheet Strength

Despite profitability challenges, Methode demonstrated strong cash flow generation in Q4. The company reported free cash flow of $26.3 million, a significant improvement from $15.8 million in Q4 FY24.

The following chart illustrates this positive free cash flow trend:

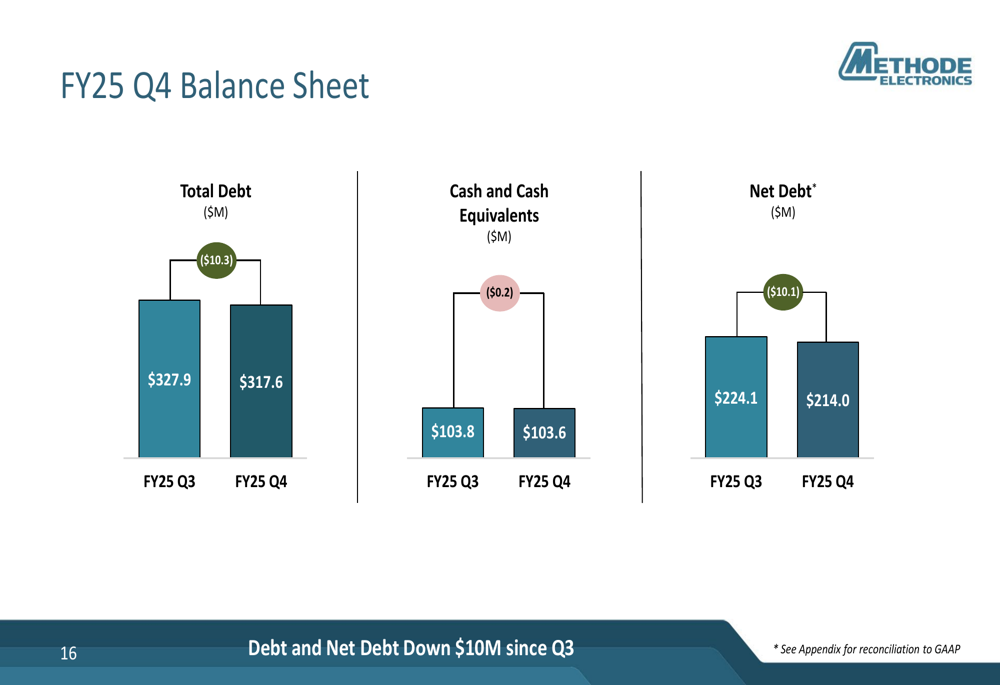

The company also made progress in strengthening its balance sheet, reducing both debt and net debt by $10 million since Q3 FY25. As of the end of FY25, Methode reported total debt of $317.6 million and cash and cash equivalents of $103.6 million, resulting in net debt of $214 million.

Full-Year Performance

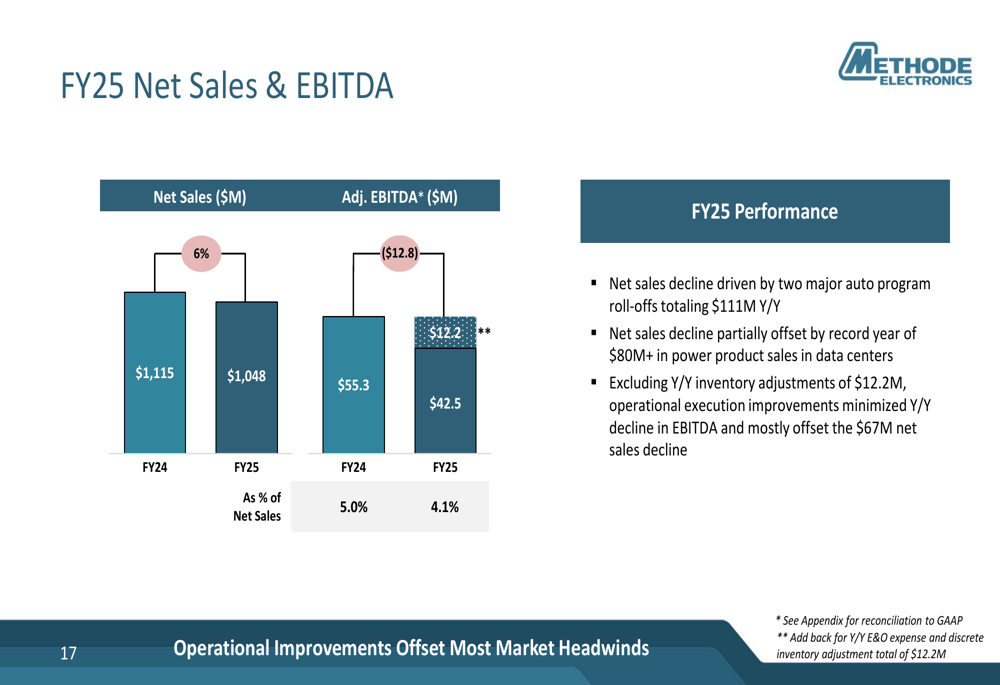

For the full fiscal year 2025, Methode reported net sales of $1,048 million, down from $1,115 million in FY24. Adjusted EBITDA also declined to $42.5 million (4.1% of net sales) from $55.3 million (5.0%) in the previous year.

The following chart provides a clear overview of the full-year performance:

The sales decline was primarily driven by two major automotive program roll-offs totaling $111 million year-over-year. However, this was partially offset by record sales of over $80 million in power products for data centers. The company highlighted that operational execution improvements helped minimize the impact of the sales decline on EBITDA.

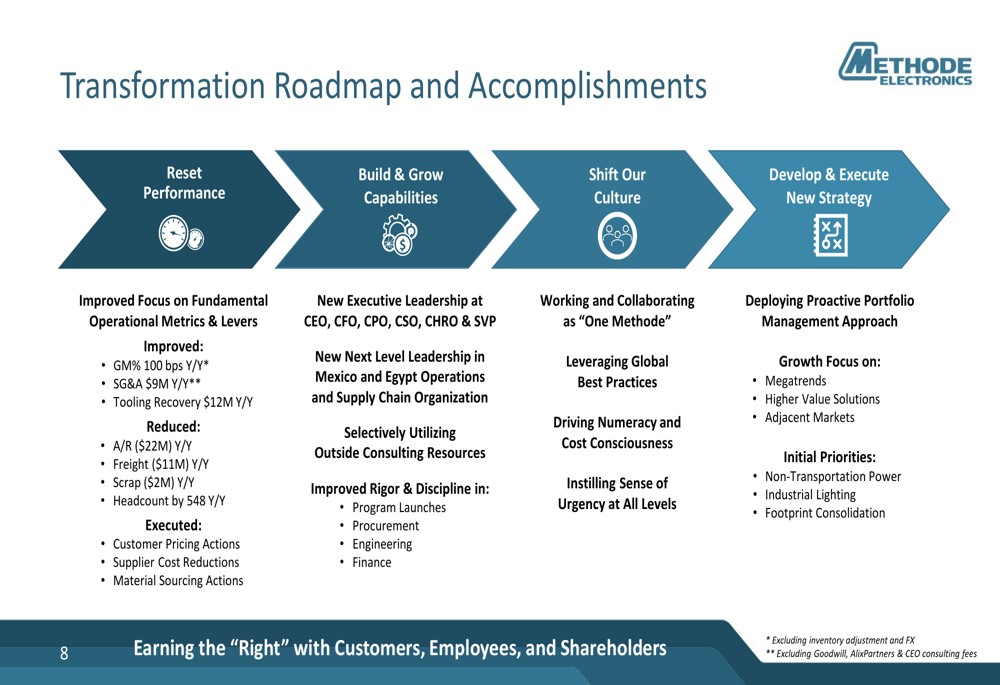

Transformation Strategy

A significant portion of the presentation focused on Methode’s ongoing transformation efforts. The company outlined a comprehensive roadmap divided into four key areas: Reset Performance, Build & Grow Capabilities, Shift Culture, and Develop & Execute New Strategy.

The transformation roadmap and accomplishments detailed in the presentation show progress across multiple fronts:

Notable achievements include improving gross margin by 100 basis points year-over-year, reducing SG&A by $9 million, increasing tooling recovery by $12 million, and reducing accounts receivable by $22 million. The company has also brought in new executive leadership across multiple positions and is working to shift its culture toward "One Methode" with improved collaboration and cost consciousness.

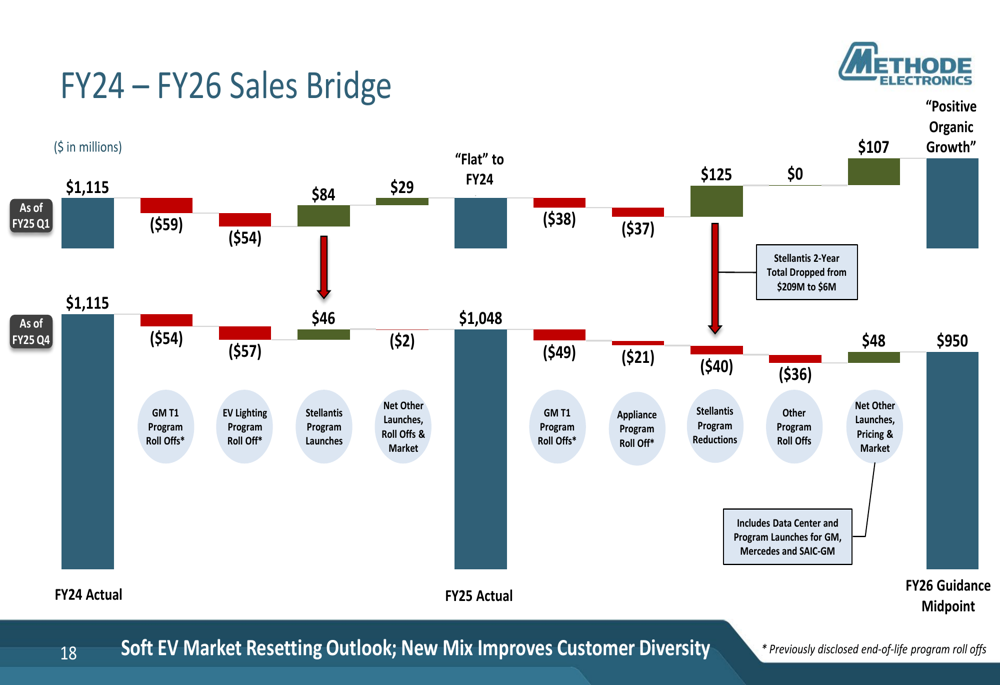

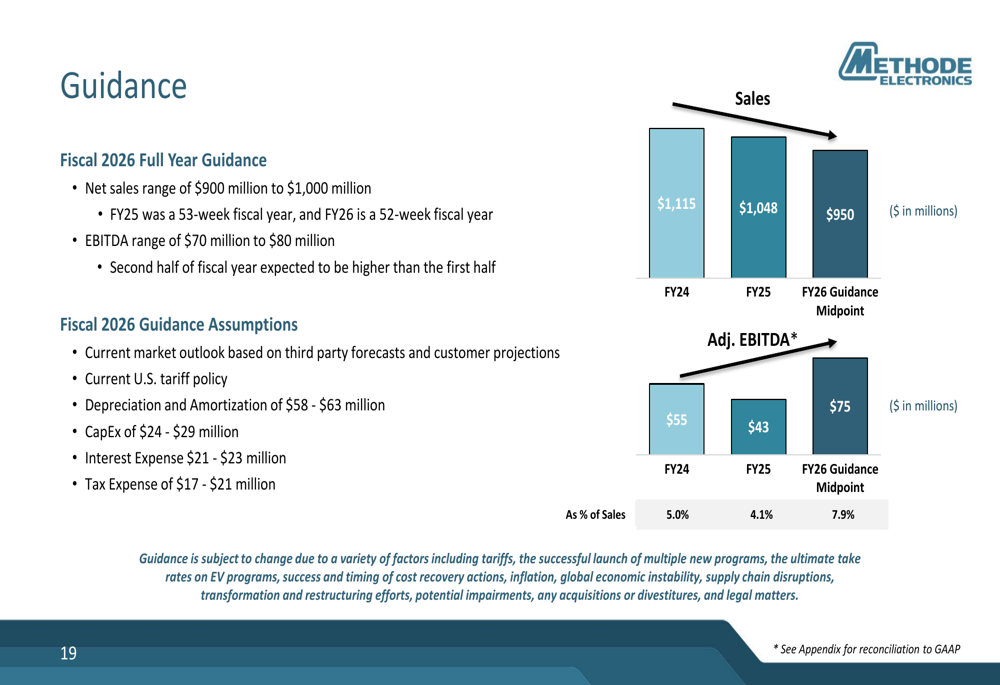

FY26 Outlook & Guidance

Looking ahead to fiscal 2026, Methode provided guidance that shows confidence in its transformation efforts despite expected sales challenges. The company projects net sales in the range of $900 million to $1 billion, representing a decline from FY25, but expects EBITDA to increase significantly to between $70 million and $80 million.

The sales bridge from FY24 to FY26 illustrates the factors affecting the company’s revenue trajectory:

The guidance slide further details the company’s expectations for FY26:

Management emphasized that the FY26 guidance represents a more than 100% increase in EBITDA despite approximately $100 million lower sales, highlighting the expected benefits of the company’s transformation initiatives. The company also noted that the second half of fiscal 2026 is expected to be stronger than the first half.

Market Challenges & Opportunities

Methode faces several challenges, including a reset of EV sales expectations due to market slowdown, particularly related to Stellantis programs. This aligns with the company’s Q3 earnings report, which mentioned delays in Stellantis EV program launches that contributed to a 27.39% stock drop following that announcement.

The company is also navigating potential U.S. tariff impacts, with approximately 25% of its annual global sales exposed to these tariffs. Methode has formed a cross-functional team to manage its response and is targeting 100% tariff impact mitigation through strategies such as customer pass-through and more fully utilizing its global footprint.

Despite these challenges, Methode highlighted significant opportunities, particularly in data centers where it achieved record sales in FY25 and expects similar or greater sales in FY26. The company also continues to focus on vehicle electrification and industrial & commercial vehicle lighting as key growth areas aligned with market megatrends.

Conclusion

Methode Electronics’ Q4 and FY25 results reflect a company in transition, facing market challenges while implementing a comprehensive transformation strategy. While profitability was significantly impacted by inventory adjustments in Q4, the company demonstrated improved cash flow generation and progress in its operational initiatives.

The optimistic FY26 guidance, particularly regarding EBITDA improvement despite lower sales, suggests management’s confidence in the effectiveness of its transformation efforts. However, the company will need to successfully navigate continued market uncertainties, particularly in the EV sector, to achieve these targets.

Investors will likely be watching closely to see if Methode can deliver on its promised EBITDA improvements while managing the reset in sales expectations for the coming fiscal year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.