These are top 10 stocks traded on the Robinhood UK platform in July

Introduction & Market Context

MFA Financial, Inc. (NYSE:MFA) presented its first quarter 2025 company update on May 6, revealing a modest economic return of 1.9% amid continued portfolio growth and a slight decline in book value. The hybrid mortgage REIT, which manages $11.5 billion in total assets, has maintained its strategy of targeting residential mortgage subsectors with less competition from banks and government-sponsored enterprises.

MFA shares were trading at $9.75 at the time of this writing, down 1.67% for the day, reflecting ongoing market volatility in the mortgage REIT sector. The stock is currently trading at a significant discount to its economic book value of $13.84 per share, representing a potential value opportunity for investors.

Quarterly Performance Highlights

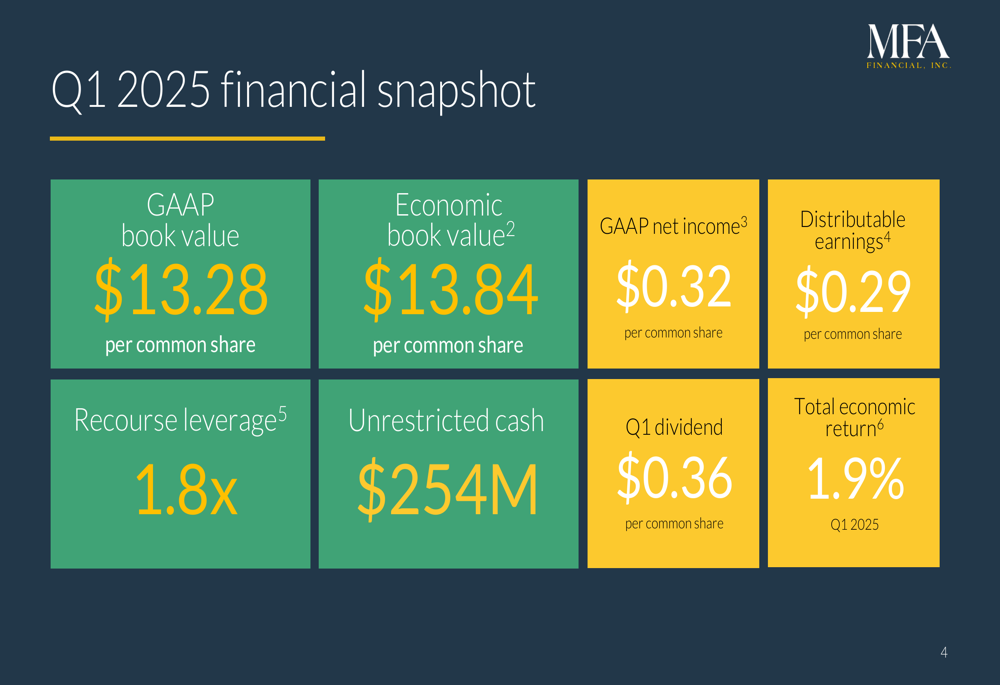

MFA Financial reported GAAP net income of $0.32 per common share for Q1 2025, with distributable earnings of $0.29 per share. The company declared a quarterly dividend of $0.36 per share, representing a 14.4% annualized yield based on the May 2 stock price.

Economic book value declined slightly by 0.6% during the quarter to $13.84 per share, as the benefit of lower interest rates was offset by wider credit spreads. GAAP book value ended the quarter at $13.28 per share.

As shown in the following snapshot of Q1 2025 financial metrics:

The company maintained a conservative leverage profile with recourse leverage at 1.8x and held $254 million in unrestricted cash at quarter-end. This liquidity position provides flexibility for future investment opportunities while serving as a buffer against market volatility.

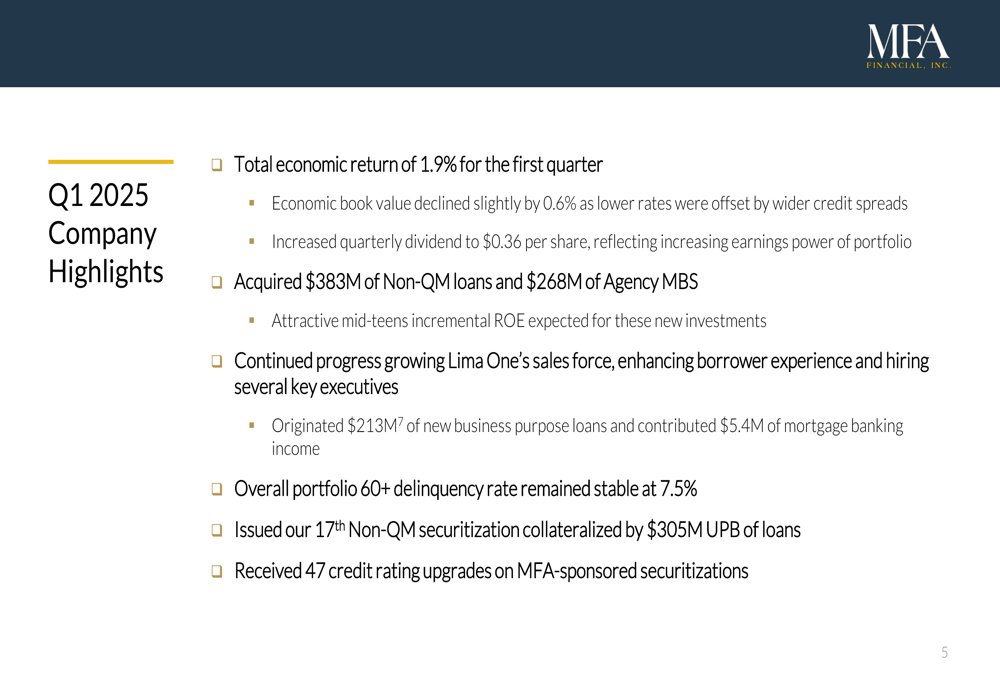

MFA highlighted several key achievements during the quarter, including the acquisition of $383 million of Non-QM loans and $268 million of Agency MBS, the issuance of its 17th Non-QM securitization, and continued expansion of Lima One’s sales force.

The following slide summarizes the company’s Q1 2025 highlights:

Investment Strategy & Portfolio Composition

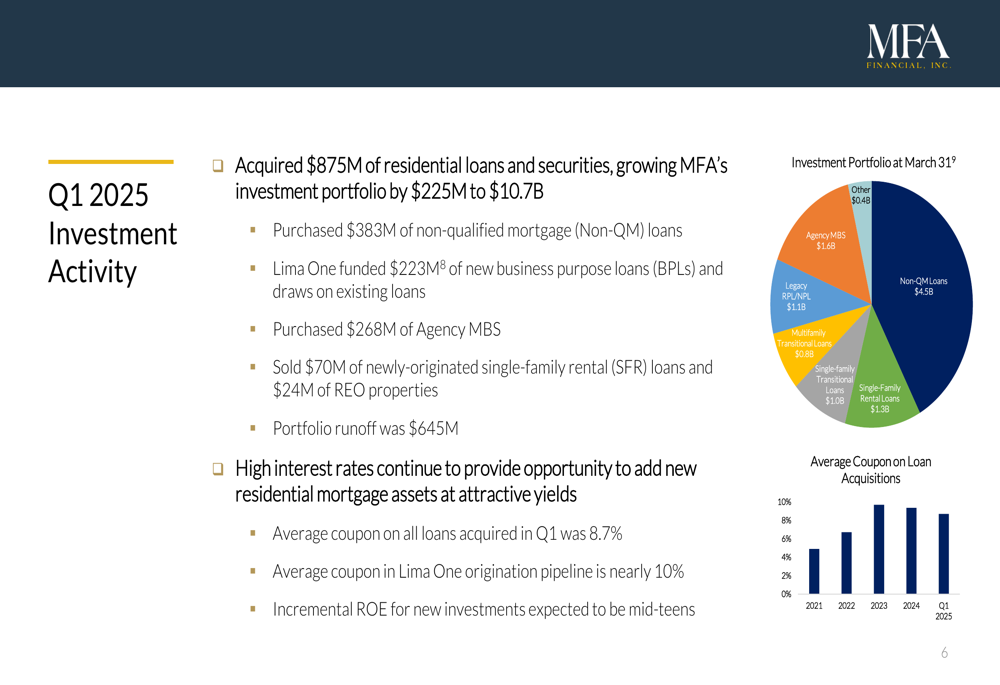

MFA Financial grew its investment portfolio by $225 million to $10.7 billion during the quarter, acquiring $875 million of residential loans and securities. The company continues to benefit from the high interest rate environment, which enables it to add new residential mortgage assets at attractive yields.

The average coupon on loans acquired in Q1 was 8.7%, significantly higher than acquisitions in previous years, which the company expects to generate mid-teens incremental returns on equity. This represents a substantial increase from the average coupon of approximately 2% on loans acquired in 2021.

As illustrated in the following investment activity summary:

The company’s portfolio remains diversified across various residential loan types, with Single-Family Loans representing the largest segment at $4.5 billion, followed by Agency MBS at $1.6 billion, Single-Family Rental Loans at $1.3 billion, and Legacy RPL/NPL at $1.1 billion.

MFA added $268 million of Agency MBS during the quarter, growing this segment to $1.6 billion. Management noted that historically-wide spreads over Treasuries make Agency MBS particularly attractive, with expected levered returns in the mid-teens. These securities also provide a complement to the company’s less liquid, more credit-sensitive assets.

Credit Performance & Risk Management

MFA’s overall portfolio 60+ day delinquency rate remained stable at 7.5% during the quarter. Credit performance varies significantly by loan type, with Non-QM loans and Single-Family Rental loans showing lower delinquency rates of 3.9% and 4.0%, respectively.

The following chart illustrates the company’s portfolio credit metrics:

In terms of interest rate risk management, MFA added $602 million of longer-dated swaps during the quarter, bringing its total swap position to $3.4 billion. These swaps had a weighted average fixed pay rate of 2.66% and variable receive rate of 4.41% at March 31, generating net positive carry of $15 million. The company’s net portfolio duration was estimated at 0.96 as of quarter-end.

MFA continues to emphasize non-mark-to-market (non-MTM) borrowing, with 83% of loan-based financing and 70% of all liabilities structured as non-MTM. This approach helps insulate the company from potential margin calls during periods of market volatility.

Lima One Performance

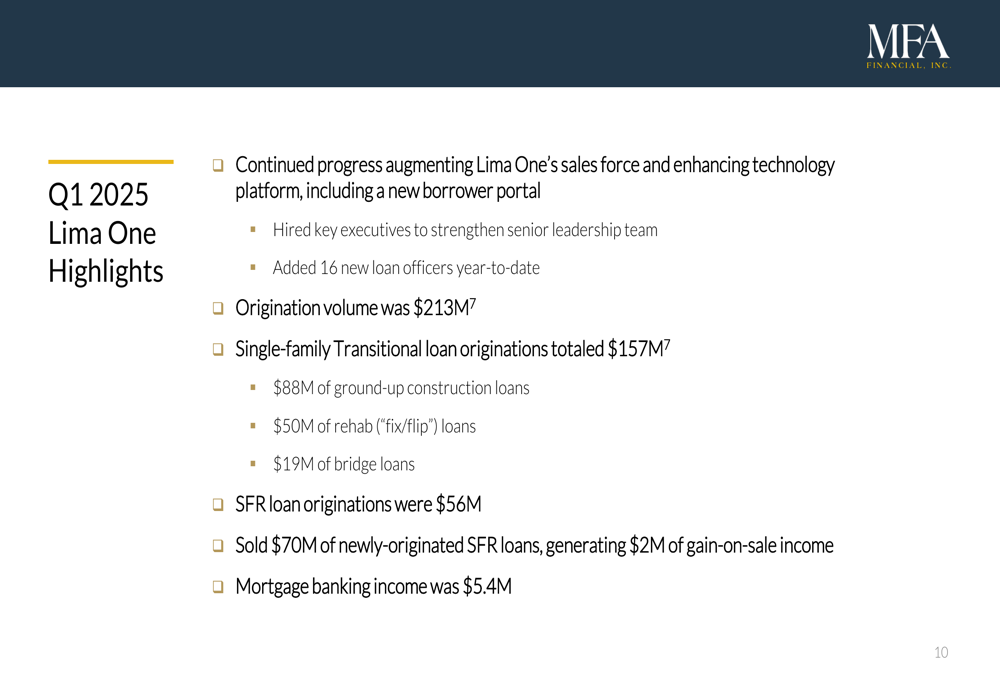

Lima One, MFA’s wholly-owned business purpose loan originator, contributed $5.4 million of mortgage banking income during the quarter. The platform originated $213 million of new business purpose loans, including $157 million of Single-Family Transitional loans and $56 million of SFR loans.

The company continues to strengthen Lima One’s capabilities, hiring key executives and adding 16 new loan officers year-to-date. MFA also sold $70 million of newly-originated SFR loans, generating $2 million of gain-on-sale income.

The following slide details Lima One’s Q1 2025 performance:

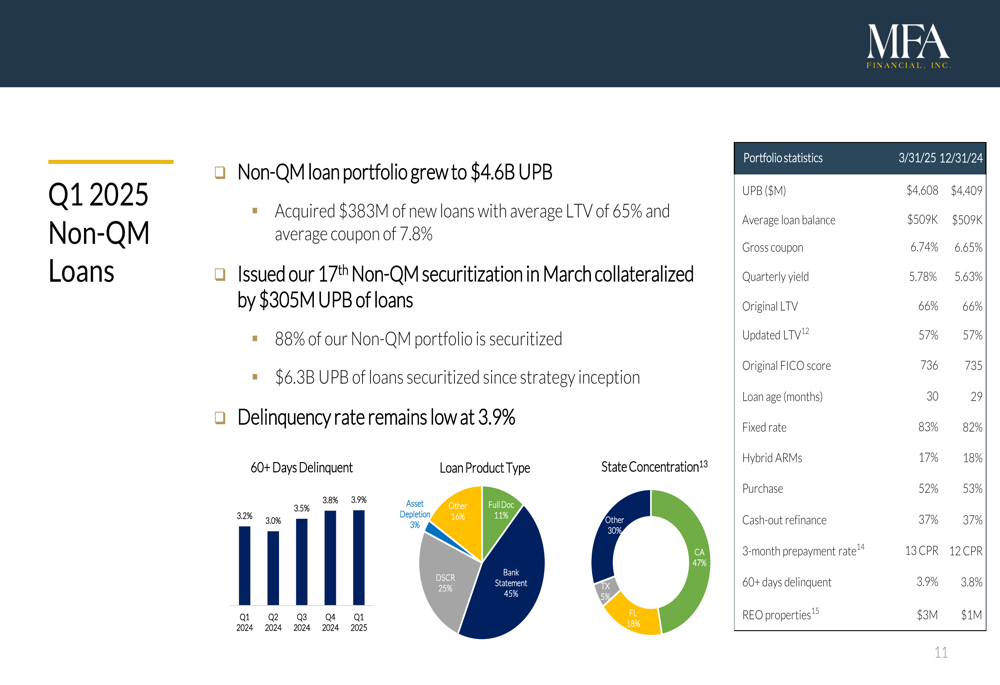

Non-QM Loan Portfolio

MFA’s Non-QM loan portfolio grew to $4.6 billion UPB during the quarter, with $383 million of new loans acquired at an average LTV of 65% and average coupon of 7.8%. The company issued its 17th Non-QM securitization in March, collateralized by $305 million UPB of loans.

The delinquency rate for Non-QM loans remains low at 3.9%, reflecting the relatively strong credit quality of this portfolio segment. Approximately 88% of the Non-QM portfolio is securitized, providing stable, non-mark-to-market financing.

The following slide provides a detailed overview of the Non-QM loan portfolio:

Forward-Looking Statements

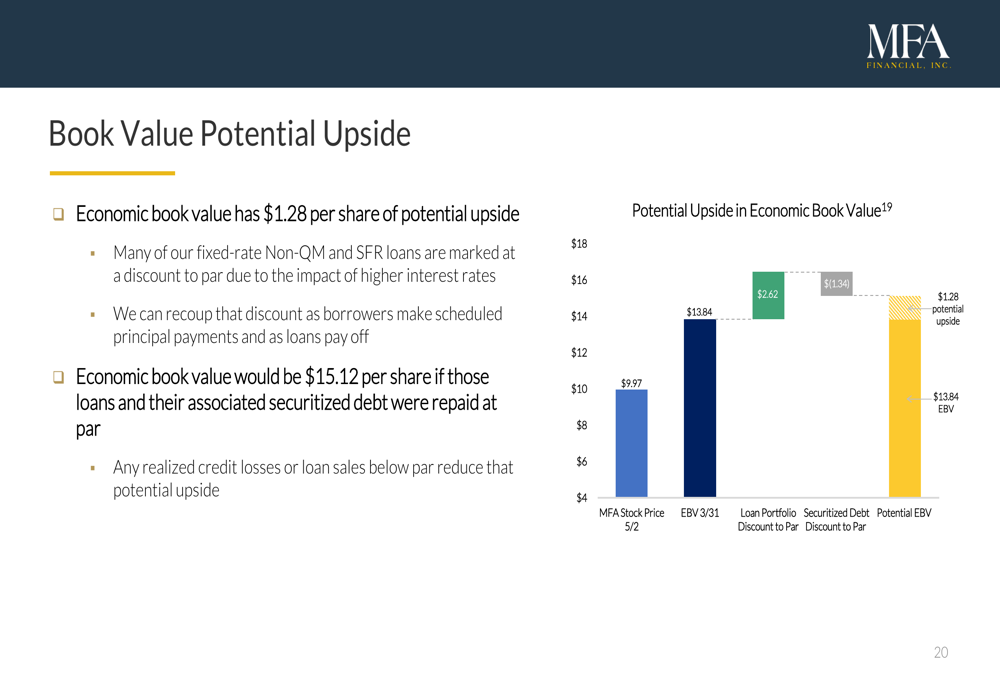

MFA Financial sees potential upside in its economic book value, noting that many of its fixed-rate Non-QM and SFR loans are marked at a discount to par due to higher interest rates. Management estimates this represents $1.28 per share of potential upside that could be recouped as borrowers make scheduled principal payments and as loans pay off.

The company’s economic book value would be $15.12 per share if those loans and their associated securitized debt were repaid at par, though management acknowledges that any realized credit losses or loan sales below par would reduce that potential upside.

As illustrated in the following book value potential upside chart:

Based on the Q1 results, MFA appears to be making progress toward its previously stated goal of achieving a 10% economic return for 2025, though the 1.9% return in Q1 suggests the company will need to accelerate performance in subsequent quarters to meet this target.

The company’s strategy of focusing on high-yielding residential mortgage assets, combined with its diversified portfolio and conservative leverage, positions it to potentially benefit from an eventual decline in interest rates while generating attractive current income for shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.