U.S. may expand Nvidia and AMD’s 15% China chips deal to other companies

Introduction & Market Context

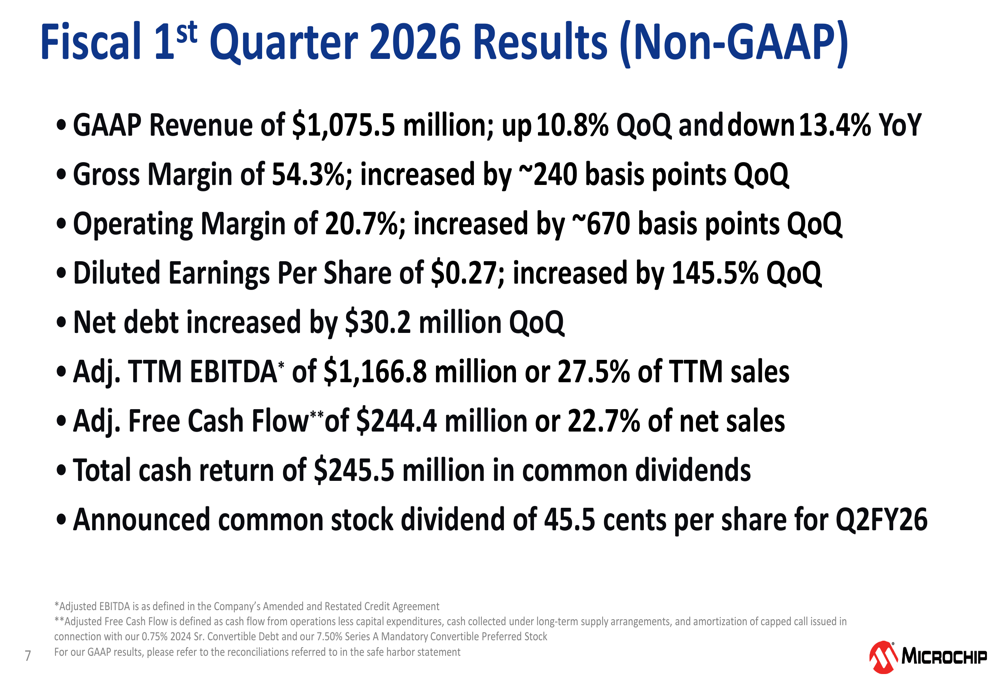

Microchip Technology Inc (NASDAQ:MCHP) reported significant sequential growth in its fiscal first quarter 2026 results, with revenue increasing 10.8% quarter-over-quarter to $1,075.5 million. Despite these improvements, the stock dropped 6.83% in pre-market trading to $61.70, suggesting investors may have expected even stronger results or were concerned about future guidance.

The semiconductor company, which positions itself as "A Leading Provider of Smart, Connected and Secure Embedded Solutions," continues to navigate a recovery phase after experiencing year-over-year declines, with Q1 revenue still down 13.4% compared to the same period last year.

Quarterly Performance Highlights

Microchip’s Q1 FY2026 results showed substantial improvement in profitability metrics compared to the previous quarter. The company reported non-GAAP gross margin of 54.3%, representing an increase of approximately 240 basis points quarter-over-quarter. Operating margin expanded even more dramatically, reaching 20.7% after a 670 basis point improvement from the previous quarter.

Diluted earnings per share saw the most impressive growth, jumping 145.5% quarter-over-quarter to $0.27, significantly exceeding the previous quarter’s guidance range of $0.18-$0.26.

As shown in the following financial results summary:

The company’s adjusted EBITDA for the trailing twelve months stood at $1,166.8 million, representing 27.5% of TTM sales. Adjusted free cash flow for the quarter was $244.4 million, or 22.7% of net sales, demonstrating Microchip’s continued ability to generate substantial cash despite market challenges.

End Market Analysis

Microchip’s revenue mix demonstrates a well-diversified business across product lines, geographies, and end markets. For Q1 FY2026, Mixed Signal MCUs represented nearly half of the company’s revenue at 49.5%, followed by Analog at 29.4%, and Other products at 21.1%. Geographically, Asia continues to be the largest market at 50.4%, with Americas at 28.6% and Europe at 21.0%.

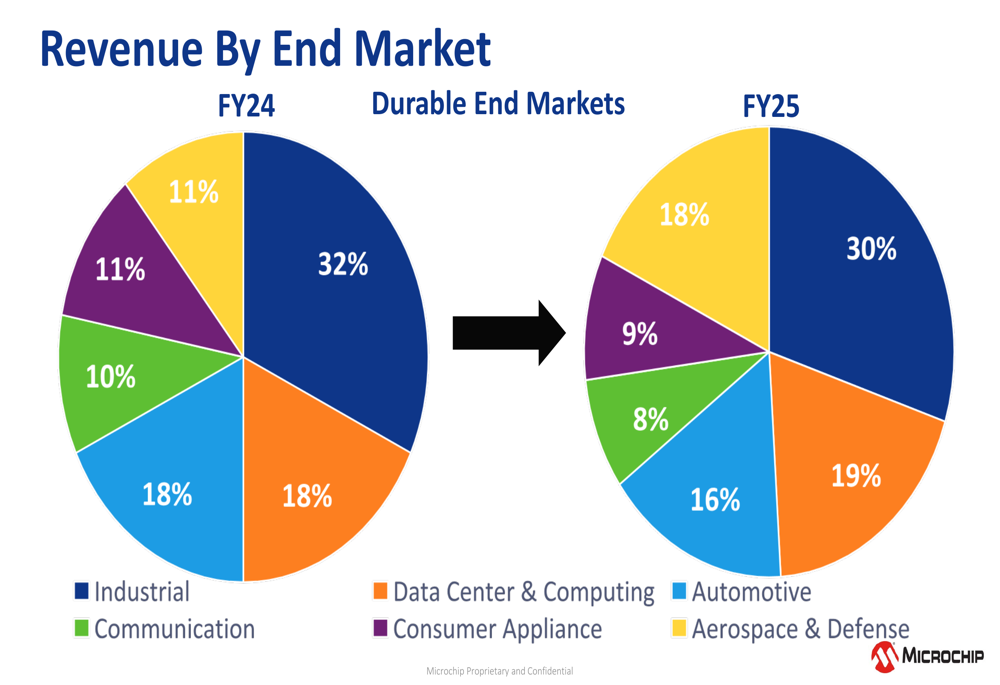

The company’s revenue distribution by end market reveals significant shifts in focus between fiscal years 2024 and 2025, as illustrated in the following chart:

The most notable change is in the automotive segment, which grew from 11% of revenue in FY24 to 18% in FY25, reflecting Microchip’s strategic emphasis on this high-growth area. Meanwhile, the industrial segment, while still the largest contributor, decreased slightly from 32% to 30%. Data Center & Computing increased from 18% to 19%, while Consumer Appliance and Aerospace & Defense both saw modest declines.

Strategic Initiatives

Microchip continues to focus on providing total system solutions across diverse markets, with particular emphasis on megatrends including IoT, edge computing, data centers, AI/ML, E-mobility, sustainability, and networking/connectivity. The company’s product portfolio spans microcontrollers, microprocessors, analog components, and connectivity solutions.

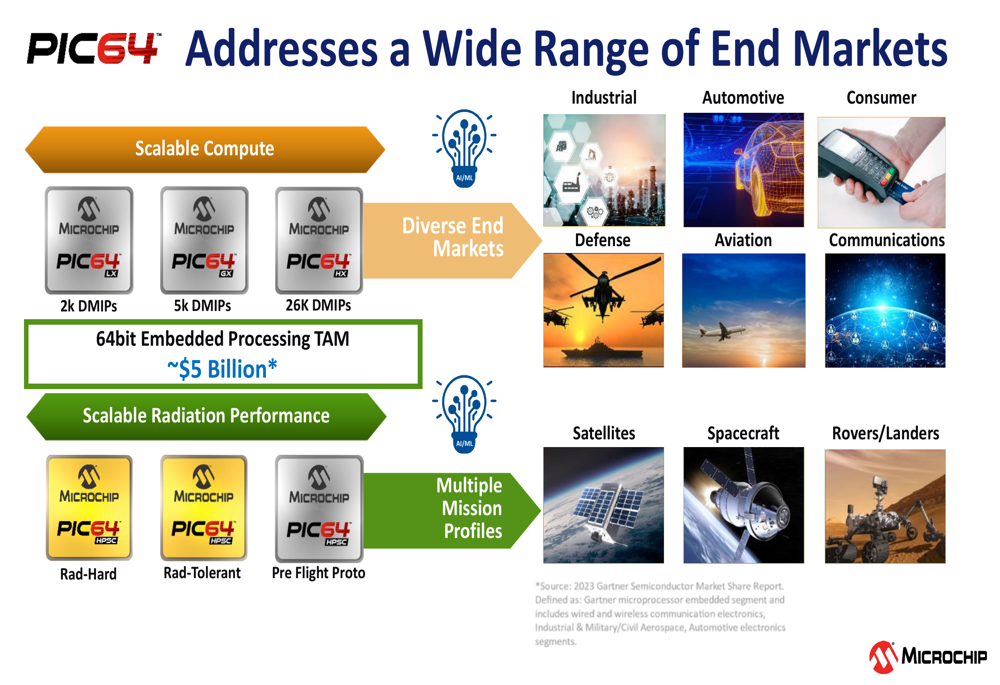

The company highlighted its PIC64 family, which addresses approximately $5 billion in market opportunity across multiple sectors including industrial, automotive, communications, defense, and space applications:

Another strategic focus area is the company’s 10BASE-T1S technology, which provides scalable interfaces for various applications in industrial automation, automotive systems, and defense electronics.

Microchip also emphasized its strong position in the aerospace and defense market, with over 71,000 high-reliability products, more than 60 years of space innovation heritage, and over 1,000 A&D customers worldwide.

Forward-Looking Statements

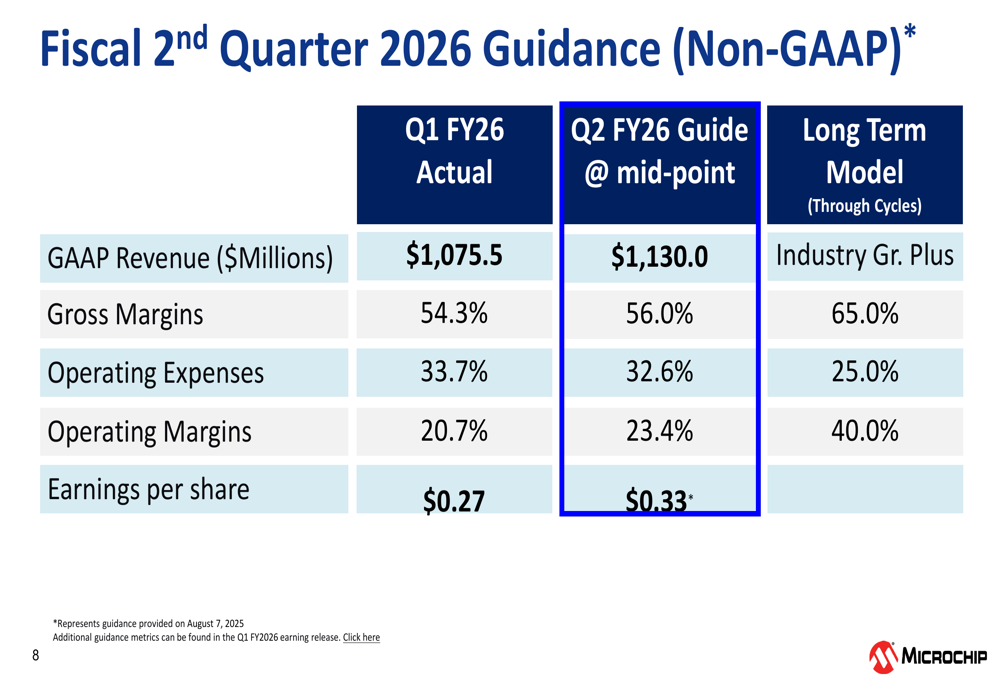

For the second quarter of fiscal 2026, Microchip provided optimistic guidance, projecting continued improvement across all key financial metrics:

The company expects revenue to increase to $1,130.0 million, representing approximately 5.1% sequential growth. Gross margins are projected to expand to 56.0%, while operating margins are expected to reach 23.4%. These improvements should drive earnings per share to $0.33, a 22.2% increase from Q1.

Microchip’s long-term model remains ambitious, targeting gross margins of 65.0%, operating expenses of 25.0%, and operating margins of 40.0%, suggesting significant potential for further profitability expansion beyond the current recovery phase.

Capital Allocation Strategy

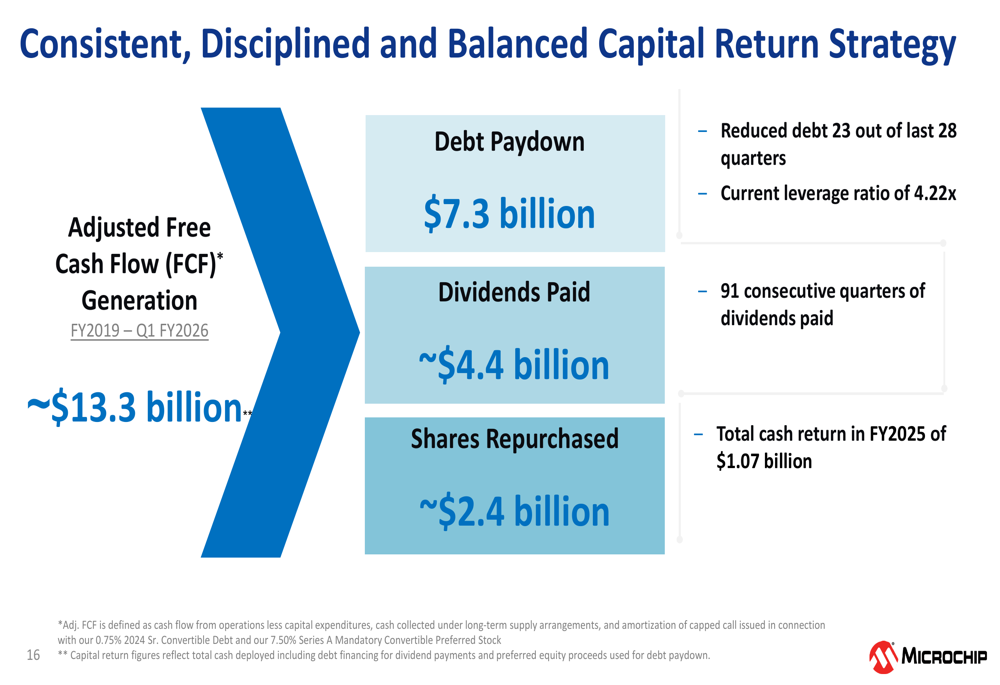

Microchip continues to maintain a disciplined and balanced approach to capital allocation, focusing on debt reduction, dividend payments, and share repurchases:

Since fiscal 2019, the company has paid down $7.3 billion in debt, reduced leverage in 23 out of the last 28 quarters, and maintained a current leverage ratio of 4.22x. During the same period, Microchip has returned approximately $4.4 billion to shareholders through dividends and repurchased approximately $2.4 billion in shares.

The company announced a quarterly dividend of 45.5 cents per share for Q2 FY26, marking its 91st consecutive quarter of dividend payments. This consistent capital return strategy underscores management’s commitment to balancing growth investments with shareholder returns.

Conclusion

Microchip’s Q1 FY2026 results demonstrate significant sequential improvement in revenue, margins, and earnings per share, suggesting the company continues to recover from previous market challenges. The strategic shift toward higher-growth segments like automotive and data center computing, combined with disciplined capital allocation, positions the company for potential long-term growth.

However, the negative pre-market stock reaction indicates investors may have concerns about the pace of recovery or future guidance. As Microchip continues to execute its strategic initiatives and capitalize on emerging opportunities in AI, IoT, and automotive electronics, investors will be watching closely to see if the company can sustain its momentum and achieve its ambitious long-term financial targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.