Fubotv earnings beat by $0.10, revenue topped estimates

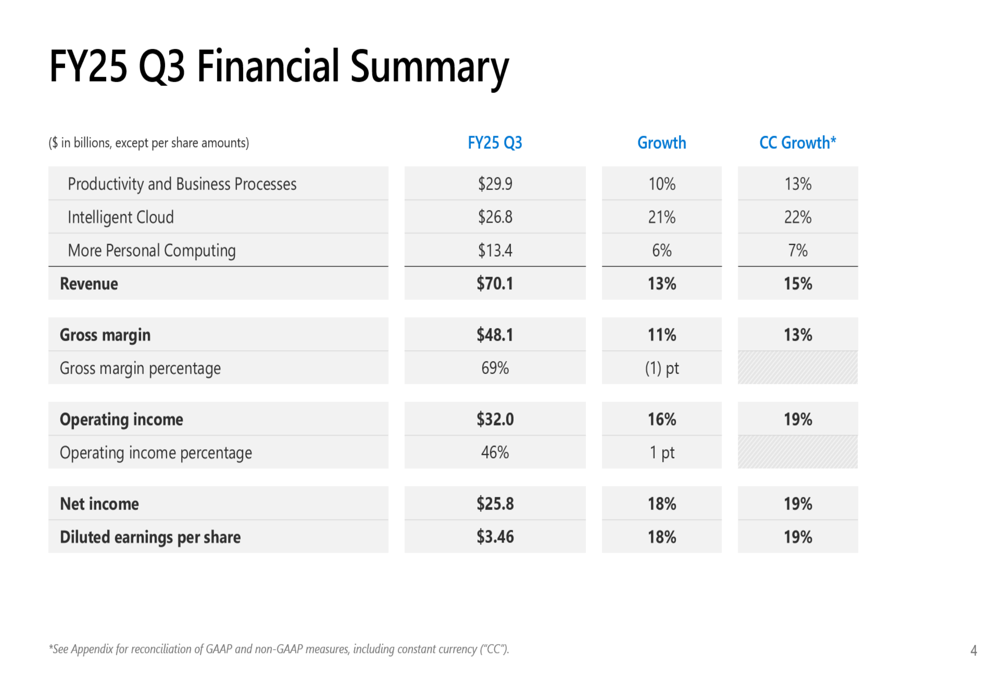

Microsoft Corporation (NASDAQ:MSFT) reported strong fiscal third quarter 2025 results on April 30, 2025, with revenue growing 13% year-over-year to $70.1 billion, exceeding analyst expectations. The tech giant’s performance was driven by continued momentum in cloud services and accelerating adoption of AI offerings.

Quarterly Performance Highlights

Microsoft delivered impressive financial results across all key metrics. Revenue reached $70.1 billion, representing 13% growth (15% in constant currency). Operating income increased 16% to $32 billion, while net income grew 18% to $25.8 billion. Diluted earnings per share rose 18% to $3.46, continuing the company’s trend of exceeding Wall Street expectations.

As shown in the following comprehensive financial summary:

The company returned $9.7 billion to shareholders during the quarter, with $6.2 billion in dividends and $3.5 billion in share repurchases. Microsoft’s effective tax rate for the quarter was 18%.

In after-hours trading, Microsoft shares rose 5.62% to $417.49, reflecting positive investor reaction to the strong results and outlook.

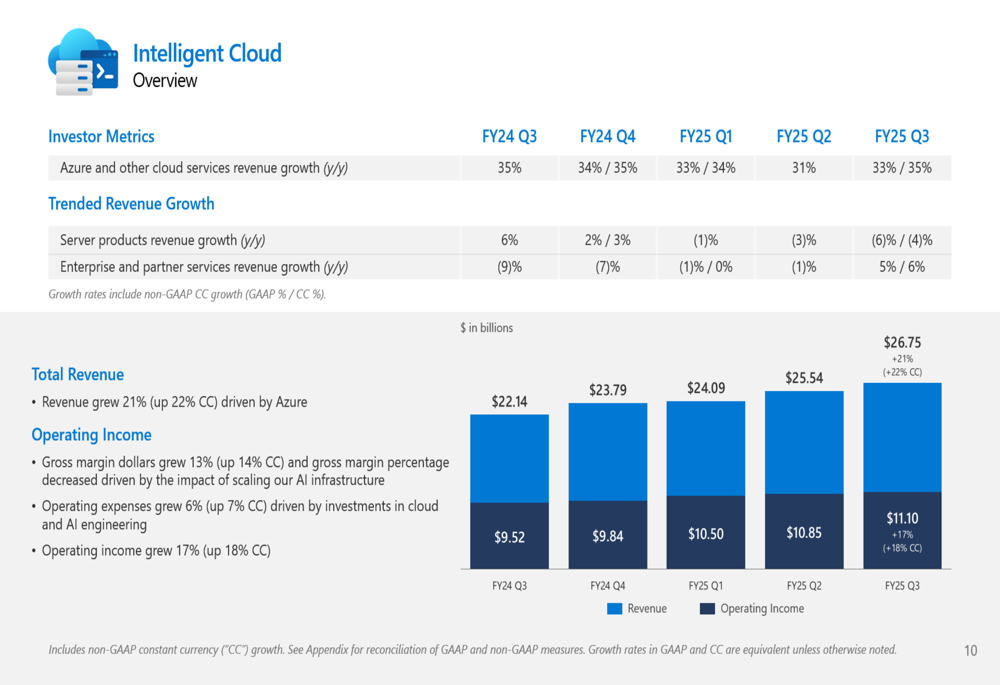

Cloud Performance and AI Momentum

Microsoft’s Intelligent Cloud segment was the standout performer, with revenue growing 21% (22% in constant currency) to $26.8 billion. Azure and other cloud services revenue increased 33% (35% in constant currency), with AI services contributing 16 percentage points to this growth.

The following chart illustrates the consistent growth trajectory of the Intelligent Cloud segment:

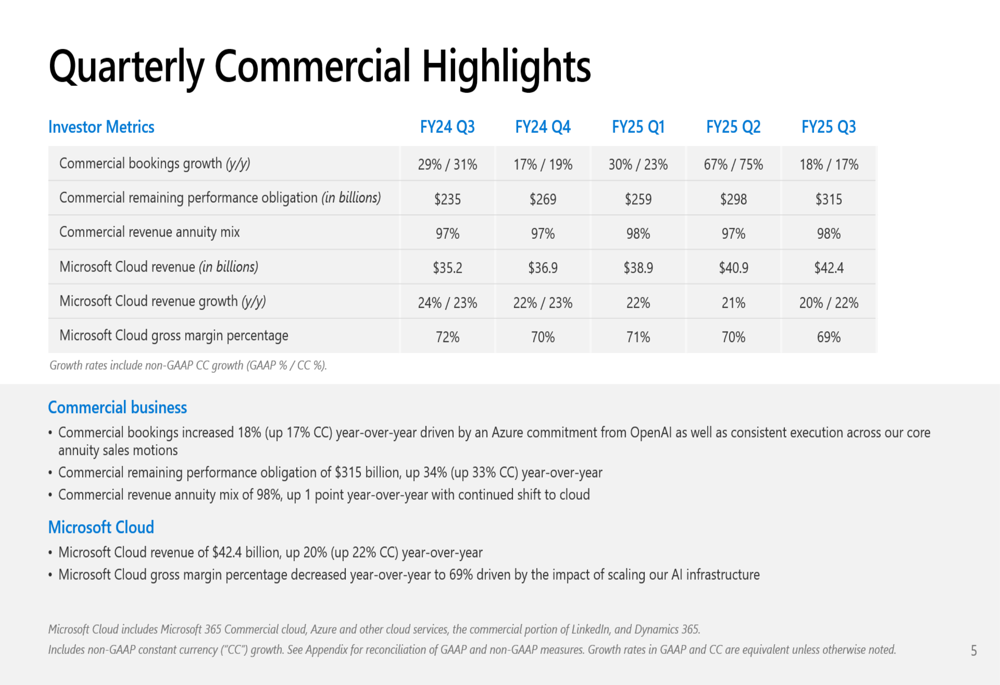

"Microsoft Cloud revenue reached $42.4 billion, up 20% year-over-year, or 22% in constant currency," the company noted in its presentation. Commercial bookings increased 18% (17% in constant currency), driven by an Azure commitment from OpenAI and strong execution across core annuity sales channels.

The company’s commercial remaining performance obligation—a key indicator of future revenue—grew to $315 billion, up 34% year-over-year, demonstrating strong momentum in Microsoft’s enterprise business.

However, Microsoft’s significant investments in AI infrastructure are impacting margins. The Microsoft Cloud gross margin percentage decreased year-over-year to 69%, which the company attributed to "the impact of scaling our AI infrastructure." Capital expenditures reached $21.4 billion during the quarter to support growing demand for cloud and AI offerings.

Segment Analysis

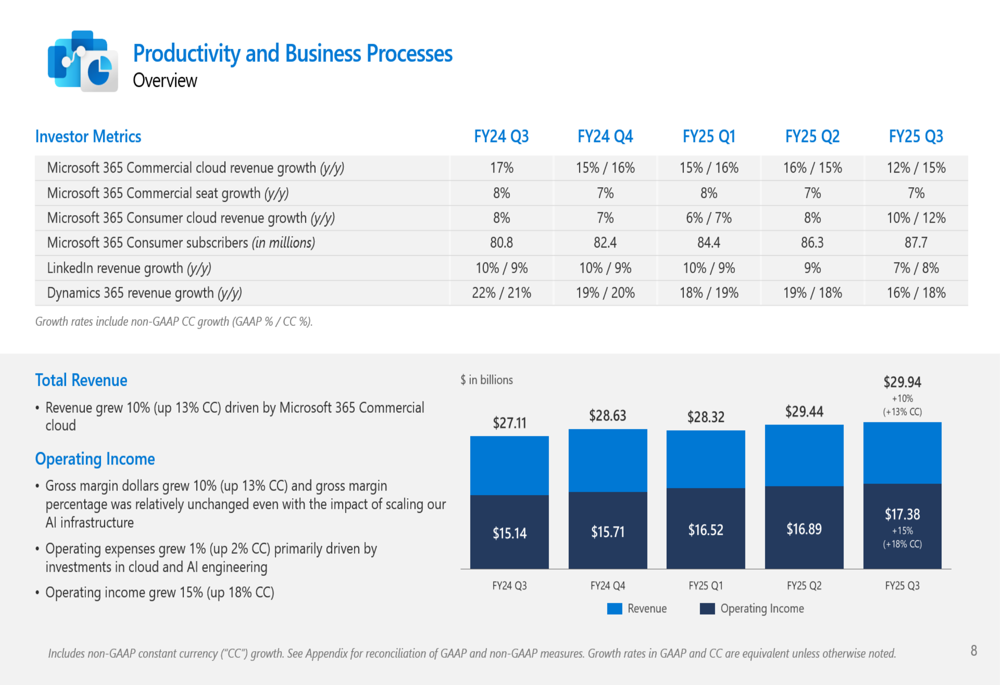

Productivity and Business Processes

The Productivity and Business Processes segment, which includes Office, LinkedIn, and Dynamics, grew 10% (13% in constant currency) to $29.9 billion. Microsoft 365 Commercial products and cloud services revenue increased 11% (14% in constant currency), while LinkedIn revenue grew 7% (8% in constant currency).

Microsoft 365 Consumer subscribers continued to grow, reaching 87.7 million, a 9% increase year-over-year. The segment’s operating income rose 15% (18% in constant currency) to $17.4 billion.

The following chart shows the segment’s consistent revenue and operating income growth:

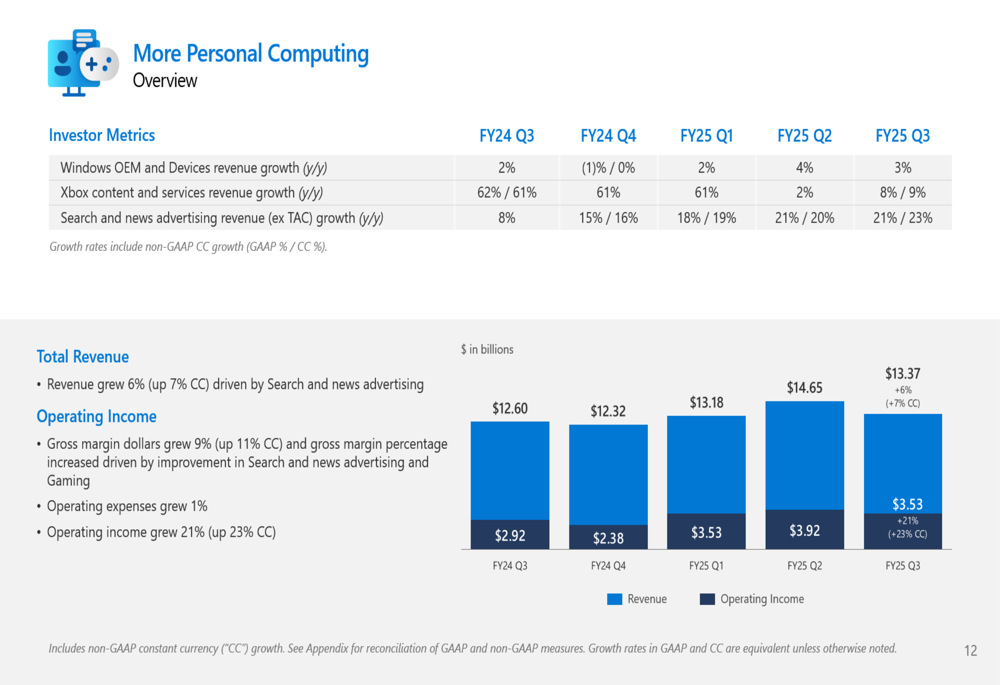

More Personal Computing

The More Personal Computing segment, which includes Windows, devices, gaming, and search, grew 6% (7% in constant currency) to $13.4 billion. Search and news advertising revenue excluding traffic acquisition costs showed particularly strong growth at 21% (23% in constant currency).

Gaming revenue increased 5% (6% in constant currency), with Xbox content and services revenue growing 8% (9% in constant currency), while Xbox hardware revenue declined 6% (5% in constant currency).

Financial Outlook and Cash Flow

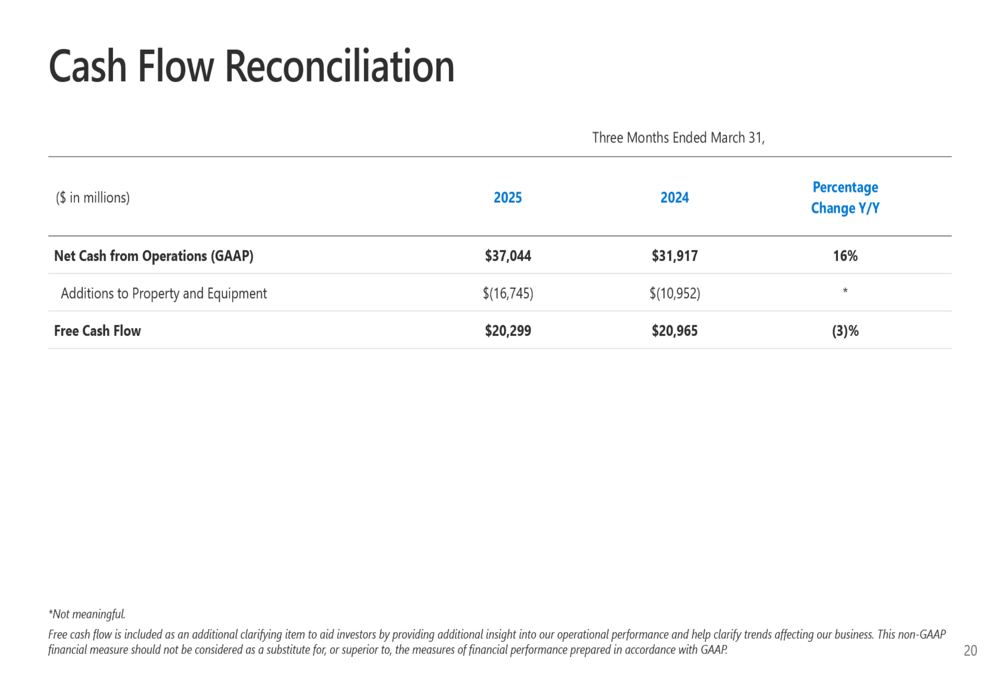

Despite strong operational performance, Microsoft’s free cash flow decreased 3% year-over-year to $20.3 billion, reflecting higher capital expenditures to support cloud and AI offerings. Cash flow from operations was robust at $37 billion, up 16% year-over-year, driven by strong cloud billings and collections.

The following cash flow reconciliation highlights this dynamic:

Microsoft’s financial results demonstrate the company’s continued ability to deliver growth across its business segments while making significant investments in future technologies, particularly AI. The acceleration in Azure growth from 31% in the previous quarter to 33% in Q3, along with the substantial contribution from AI services, indicates that Microsoft’s AI strategy is gaining traction in the market.

The company’s substantial capital expenditures reflect its commitment to building the infrastructure necessary to maintain its competitive position in the rapidly evolving AI landscape. While these investments are temporarily impacting free cash flow, they position Microsoft for sustained long-term growth as AI adoption continues to accelerate across industries.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.