Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Introduction & Market Context

Middleby Corporation (NASDAQ:MIDD) presented its first quarter 2025 earnings update on May 7, revealing a strategic pivot toward share repurchases amid mixed financial results. The stock is trading down 4.34% in premarket at $129.51, suggesting investors may be concerned about revenue declines despite improved profitability.

The commercial foodservice equipment manufacturer faces multiple challenges, including tariff pressures and segment-specific headwinds, while simultaneously pursuing a significant corporate restructuring with the planned spin-off of its Food Processing business.

Executive Summary

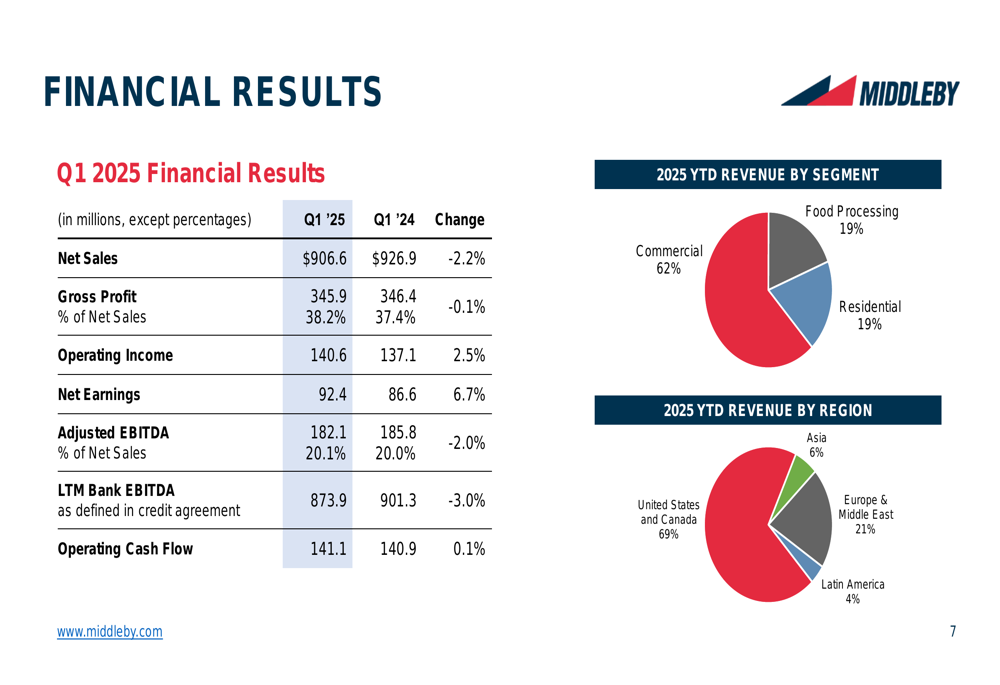

Middleby reported Q1 2025 net sales of $906.6 million, down 2.2% compared to the same period last year, while net earnings increased 6.7% to $92.4 million. The company announced a significant capital allocation shift, prioritizing share repurchases with a target of reducing outstanding shares by 6-8% annually.

The company also confirmed its Food Processing spin-off remains on track for completion by early 2026, creating two distinct publicly traded entities. Additionally, Middleby outlined its strategy to offset an estimated $150-200 million annual tariff impact through operational initiatives and price increases.

As shown in the following financial results overview:

Strategic Initiatives

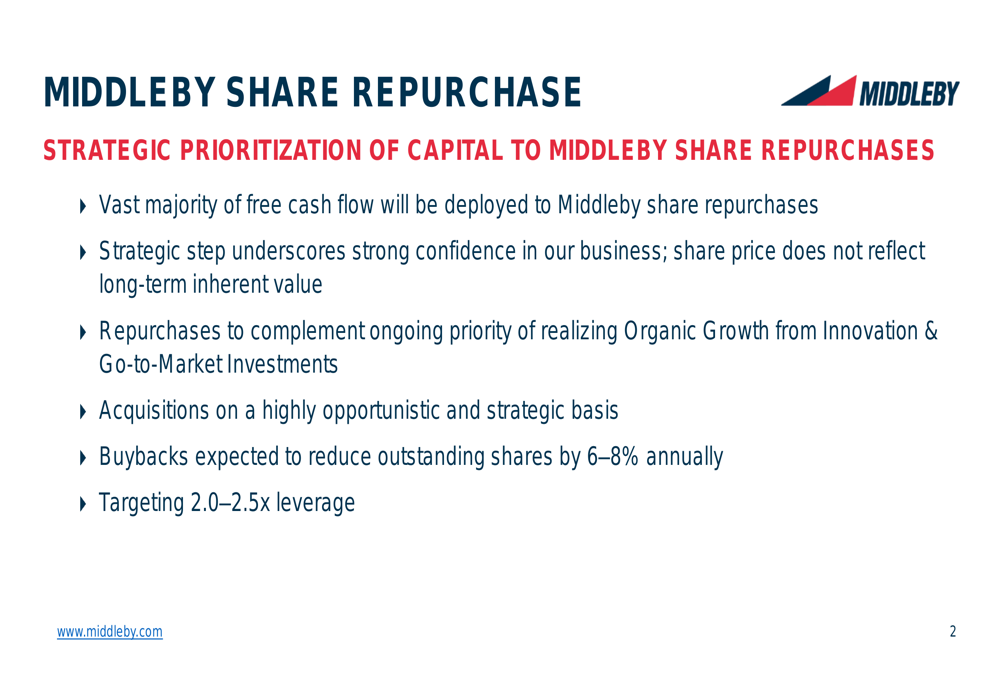

Middleby’s most significant strategic announcement is its share repurchase program, which will deploy the "vast majority" of free cash flow to reduce outstanding shares by 6-8% annually. This move signals management’s confidence that the current share price does not reflect the company’s long-term value.

The repurchase strategy is detailed in the following slide:

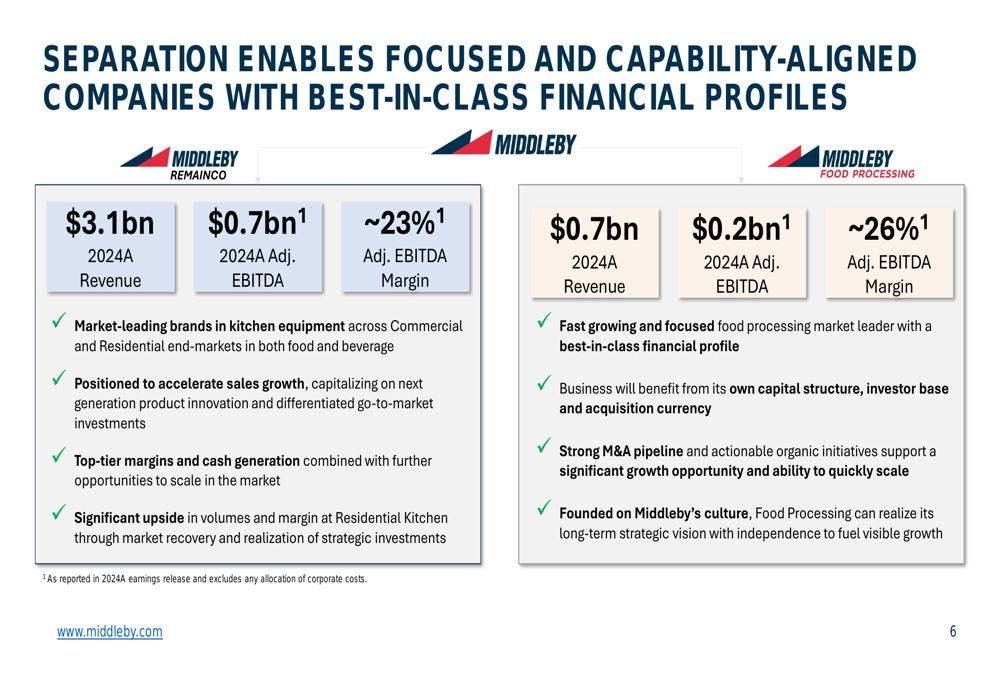

The second major strategic initiative is the planned separation of Middleby’s Food Processing segment, targeted for completion by early 2026. The company has established a separation management office and plans to hold shareholder days for both RemainCo and SpinCo in Q4 2025.

The separation will create two distinct companies with different financial profiles:

- Middleby RemainCo: $3.1 billion in revenue with 23% adjusted EBITDA margin (2024)

- Middleby Food Processing: $0.7 billion in revenue with 26% adjusted EBITDA margin (2024)

As illustrated in this breakdown of the two future companies:

Tariff Impact and Mitigation Strategy

Middleby faces significant tariff challenges, with preliminary cost effects projected at $150-200 million annually. The company noted that China represents approximately 50% of its identified cost exposure, with minimal impact in Q1 2025 but increasing pressure expected in the second half of the year.

Management outlined a comprehensive mitigation strategy, stating that tariff impacts are "expected to be fully offset by year end through operating initiatives and price increases set to take effect Q3 2025." The company also anticipates potential long-term market share gains by leveraging its U.S. and global manufacturing footprint.

The tariff strategy is detailed in the following slide:

Segment Performance Analysis

Middleby’s performance varied significantly across its three business segments:

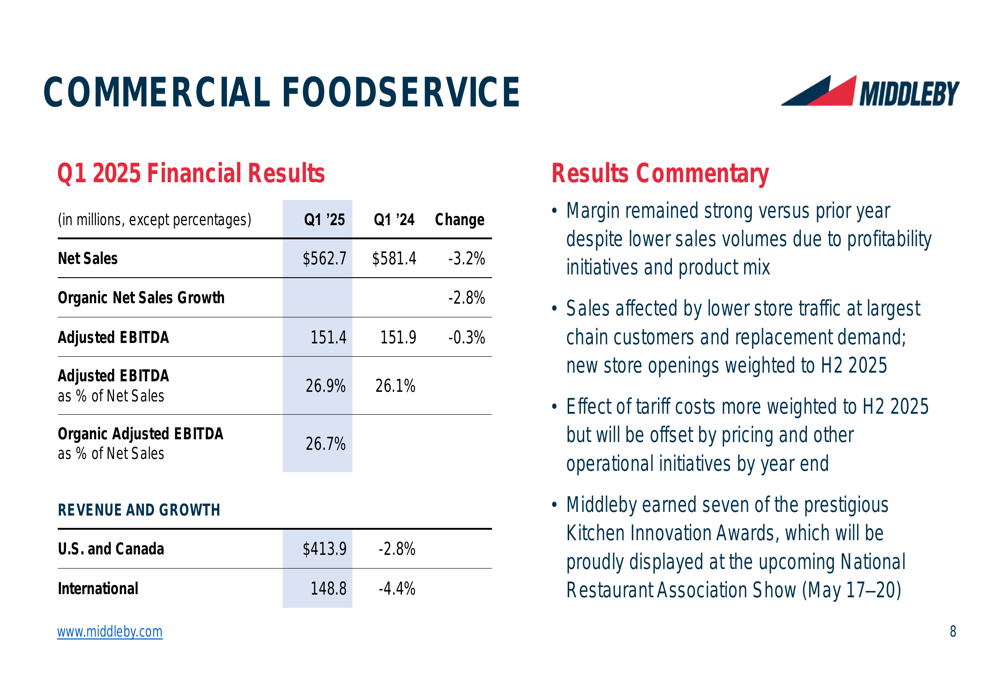

The Commercial Foodservice segment, which represents 62% of total revenue, reported net sales of $562.7 million, down 3.2% year-over-year. Despite the revenue decline, adjusted EBITDA margin improved to 26.9% from 26.1% in the prior year period.

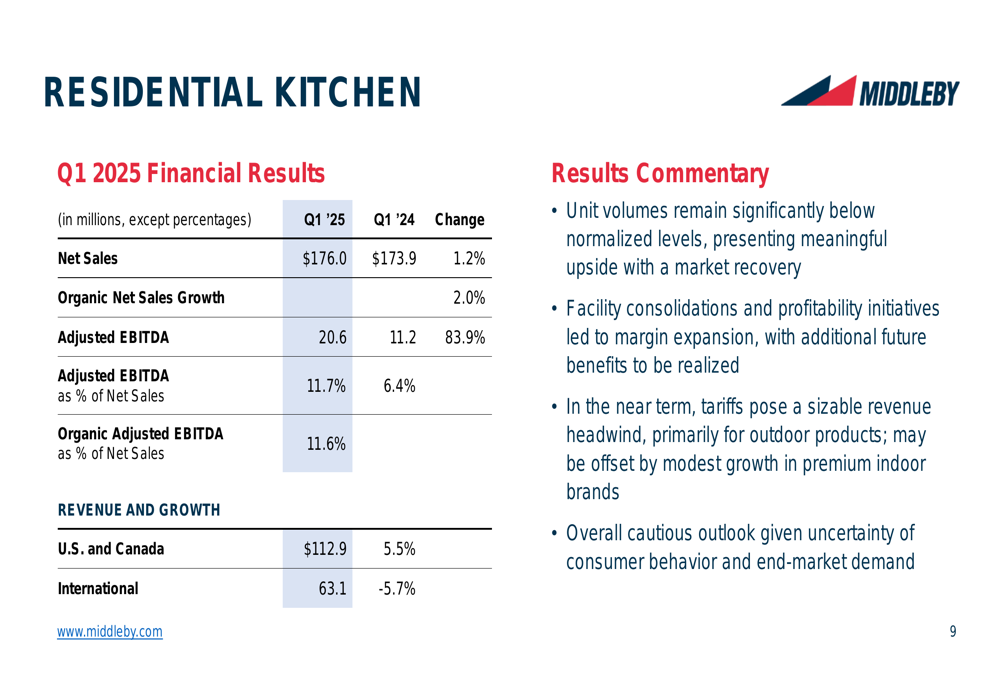

The Residential Kitchen segment showed encouraging signs of recovery with net sales of $176.0 million, up 1.2% year-over-year. More impressively, adjusted EBITDA surged 83.9% to $20.6 million, with margins expanding from 6.4% to 11.7%. This improvement reflects the benefits of facility consolidations and operational efficiencies.

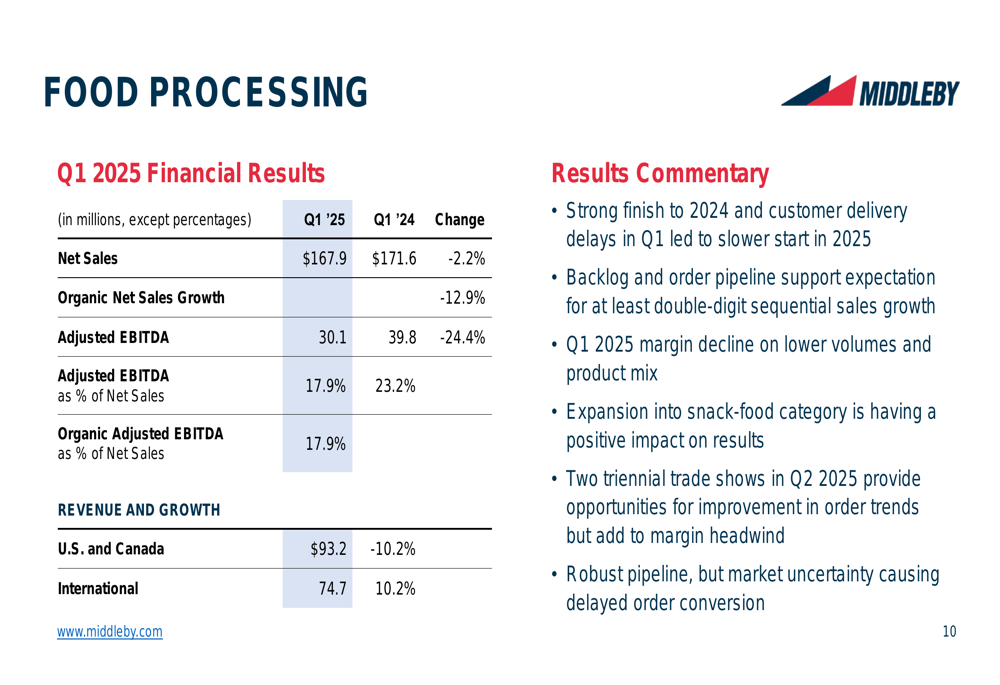

The Food Processing segment, which is slated for spin-off, reported disappointing results with net sales of $167.9 million, down 2.2% year-over-year. Organic sales declined 12.9%, and adjusted EBITDA fell 24.4% to $30.1 million, with margins contracting from 23.2% to 17.9%. Management attributed the decline to customer delivery delays and timing of large projects.

Financial Position and Outlook

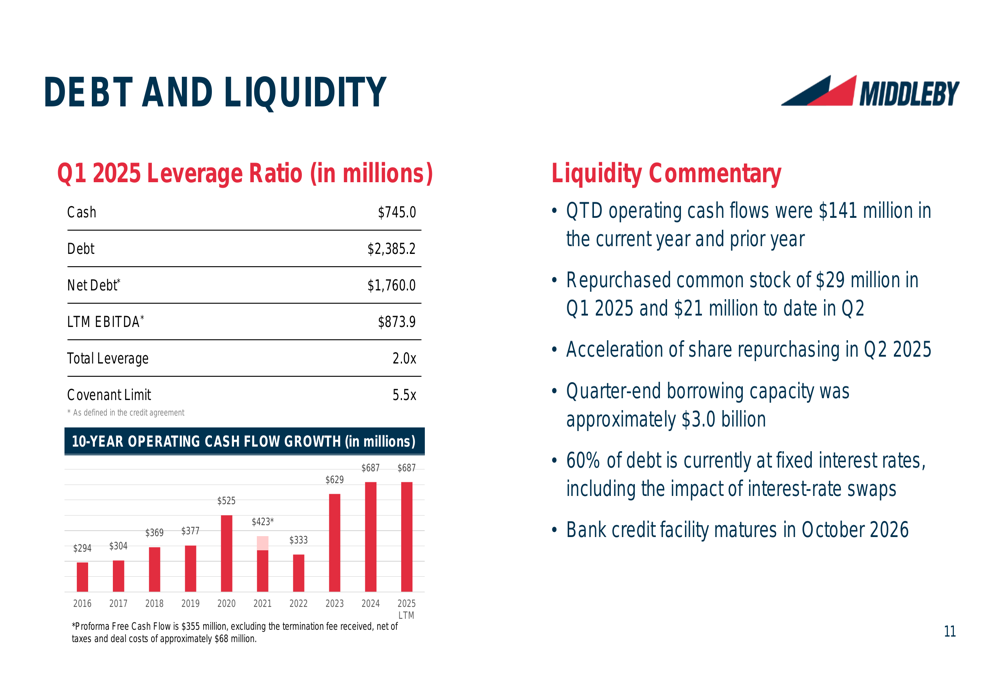

Middleby maintains a solid financial position with $745 million in cash and a total leverage ratio of 2.0x, well below its covenant limit of 5.5x. The company generated $141.1 million in operating cash flow during Q1 2025, consistent with the prior year.

The company repurchased $29 million of common stock in Q1 2025 and an additional $21 million in early Q2, with plans to accelerate share repurchases. Middleby has substantial liquidity with approximately $3.0 billion in borrowing capacity as of quarter-end.

As shown in the debt and liquidity overview:

Looking ahead, Middleby faces several challenges, including tariff pressures and segment-specific headwinds, particularly in Food Processing. However, management remains confident in its strategic direction, emphasizing the long-term benefits of the Food Processing spin-off and the value creation potential of its share repurchase program.

The significant premarket stock decline suggests investors may be concerned about revenue trends and margin pressures in the Food Processing segment, despite the company’s strategic initiatives and improved overall profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.