Can anything shut down the Gold rally?

Introduction & Market Context

MillerKnoll Inc (NASDAQ:MLKN), a global leader in design with a portfolio of 14 premium brands, presented its third quarter fiscal year 2024 results on March 27, 2024. The presentation revealed a company navigating challenging market conditions while successfully implementing cost-saving initiatives and margin improvement strategies.

The company operates in a mixed macroeconomic environment, with some positive indicators for non-residential construction (forecasted 4% growth in 2024) offset by weakness in commercial segments (expected -0.7% decline). This context helps explain some of the revenue challenges faced by MillerKnoll in the most recent quarter.

Quarterly Performance Highlights

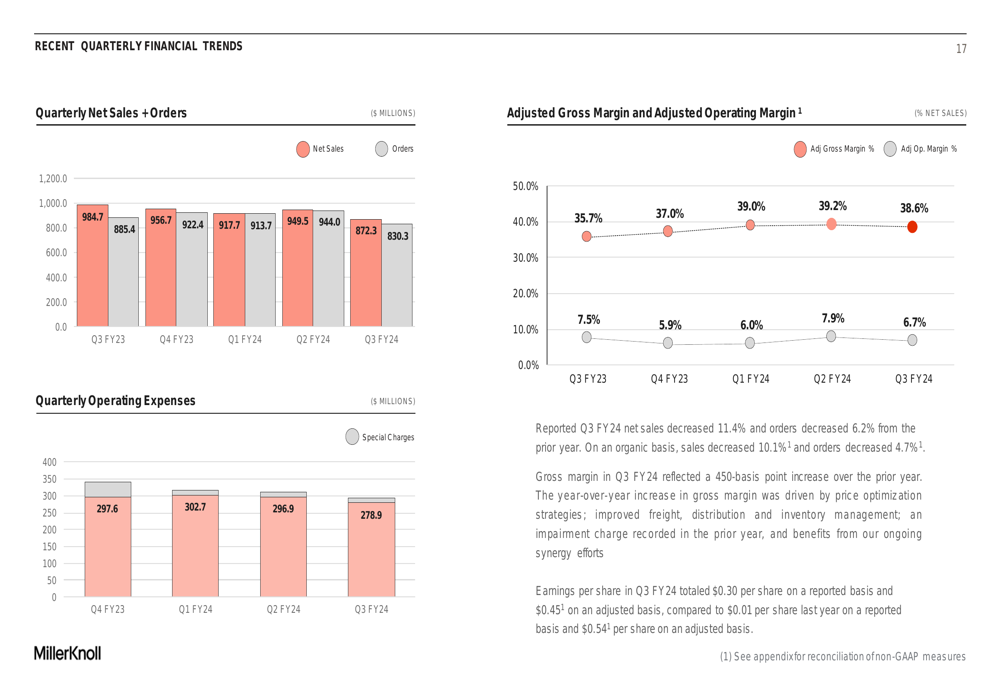

MillerKnoll reported Q3 FY24 net sales of $872.3 million, representing an 11.4% decrease compared to the same period last year. Orders also declined by 6.2% to $830.3 million. On an organic basis, sales decreased by 10.1%.

Despite the revenue challenges, the company showed significant improvement in profitability metrics. Adjusted gross margin increased to 38.6% in Q3 FY24, up 450 basis points from 35.7% in Q3 FY23. Adjusted operating margin reached 6.7%, compared to 7.5% in the prior year period.

As shown in the following chart of quarterly financial trends:

The company reported earnings per share of $0.30 on a GAAP basis and $0.45 on an adjusted basis for Q3 FY24. Cash flow from operations remained positive at $61 million, though down from $76 million in the same quarter last year.

Diversified Business Model

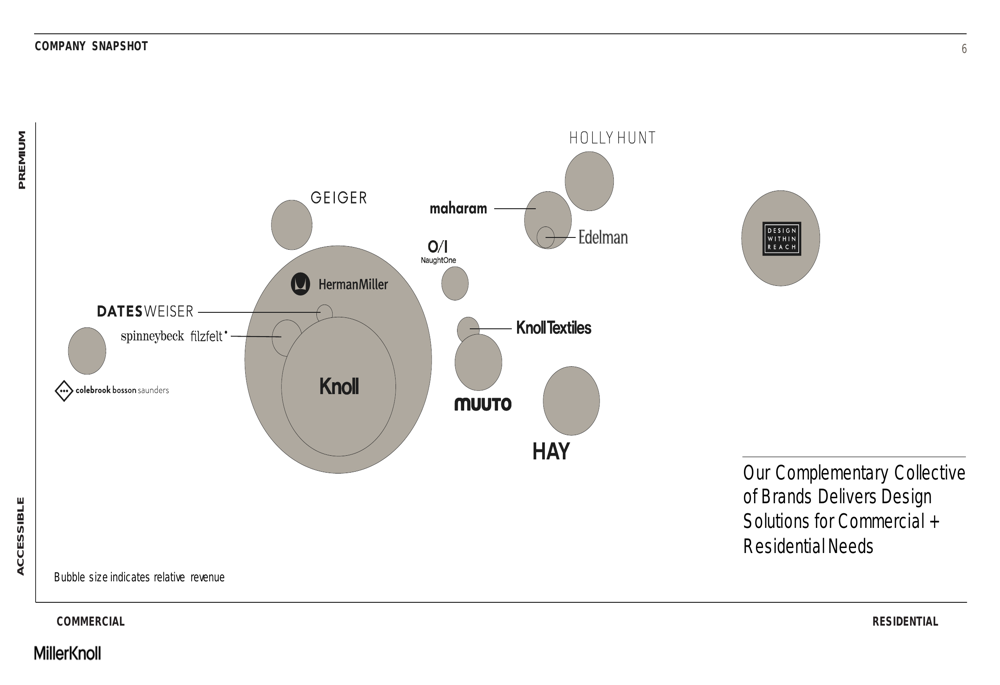

MillerKnoll’s business is built around a diverse portfolio of 14 design brands, including Herman Miller, Knoll, Design Within Reach, and others. The company generated $4.1 billion in revenue in FY23, with a balanced distribution across market segments: 50% from Americas Contract, 25% from International Contract & Specialty, and 25% from Global Retail.

The company’s brand positioning strategy is illustrated in this matrix, showing how its various brands span premium and accessible market segments:

This diversification provides resilience against market fluctuations and allows MillerKnoll to address various customer segments. The company maintains a global presence with over 1,000 dealers in 110 countries, 70+ retail stores, and approximately 11,000 employees worldwide.

Financial Trends and Margin Improvement

While recent quarters have shown revenue pressure, MillerKnoll has made significant progress in improving operational efficiency. The company has been actively reducing operating expenses, which decreased to $278.9 million in Q3 FY24 from higher levels in previous quarters.

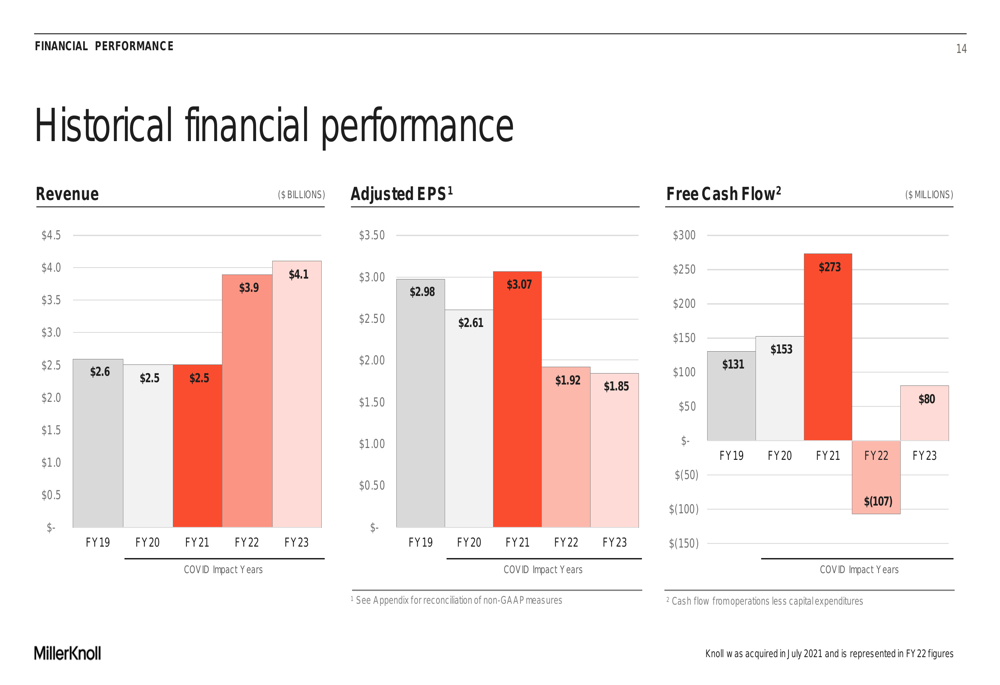

The historical financial performance shows the impact of the Knoll acquisition in July 2021, which significantly expanded the company’s revenue base but initially pressured margins and free cash flow:

A key component of MillerKnoll’s strategy is realizing $160 million in annual cost synergies from the Knoll acquisition within three years of closing. These synergies come from creating centers of excellence, consolidating production, and leveraging manufacturing scale.

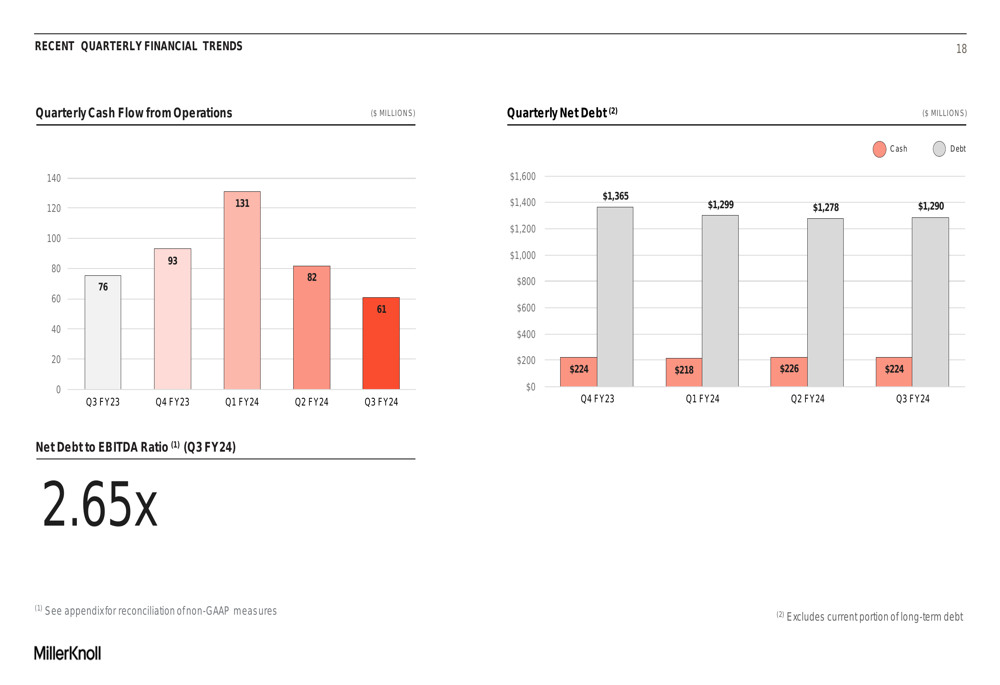

The company’s quarterly cash flow and debt management trends demonstrate a focus on financial discipline:

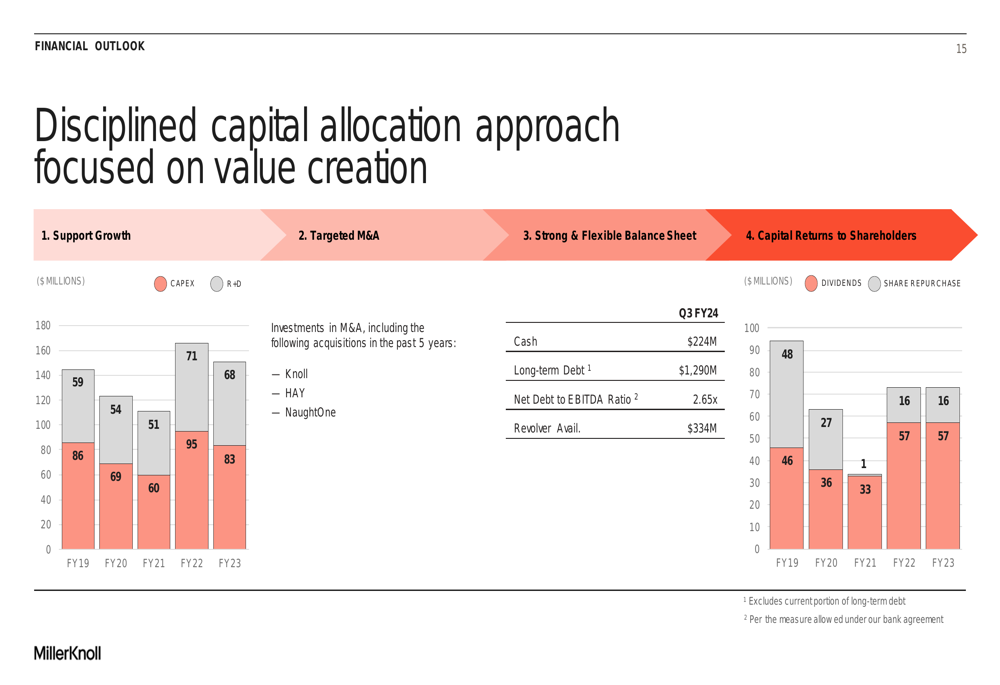

Capital Allocation Strategy

MillerKnoll maintains a disciplined approach to capital allocation, balancing investments in growth, debt reduction, and returns to shareholders. As of Q3 FY24, the company reported $224 million in cash and $1,290 million in long-term debt, resulting in a net debt to EBITDA ratio of 2.65x.

The capital allocation framework prioritizes supporting organic growth through capital expenditures and R&D, maintaining a strong and flexible balance sheet, pursuing targeted M&A opportunities, and returning capital to shareholders through dividends and share repurchases.

The company’s capital allocation approach is summarized in this slide:

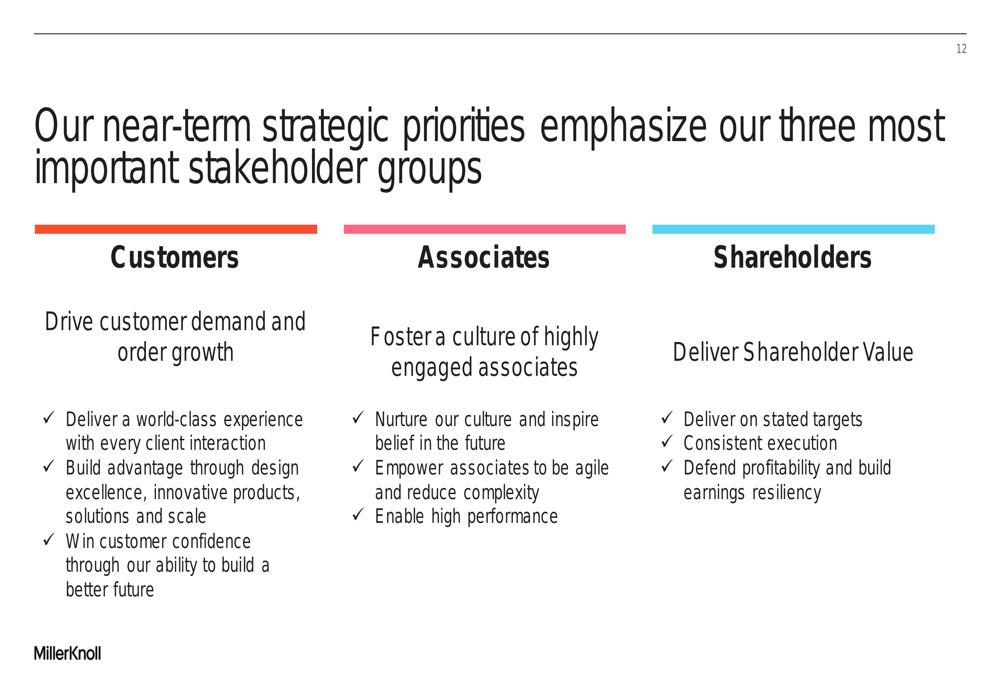

Forward Guidance and Strategic Priorities

For Q4 FY24, MillerKnoll provided guidance for revenue between $880 million and $920 million, with adjusted earnings per share expected to range from $0.49 to $0.57. This guidance suggests sequential improvement in profitability despite continued revenue challenges.

It’s worth noting that based on the more recent earnings article provided, the company actually exceeded this guidance, delivering Q4 revenue of $961.8 million and adjusted EPS of $0.60, demonstrating execution above expectations.

The company’s strategic priorities focus on three key stakeholder groups:

These priorities emphasize customer demand growth, operational excellence, and shareholder value creation through consistent execution and profitability improvement. The company’s near-term focus appears to be on defending profitability and building earnings resilience while navigating a challenging demand environment.

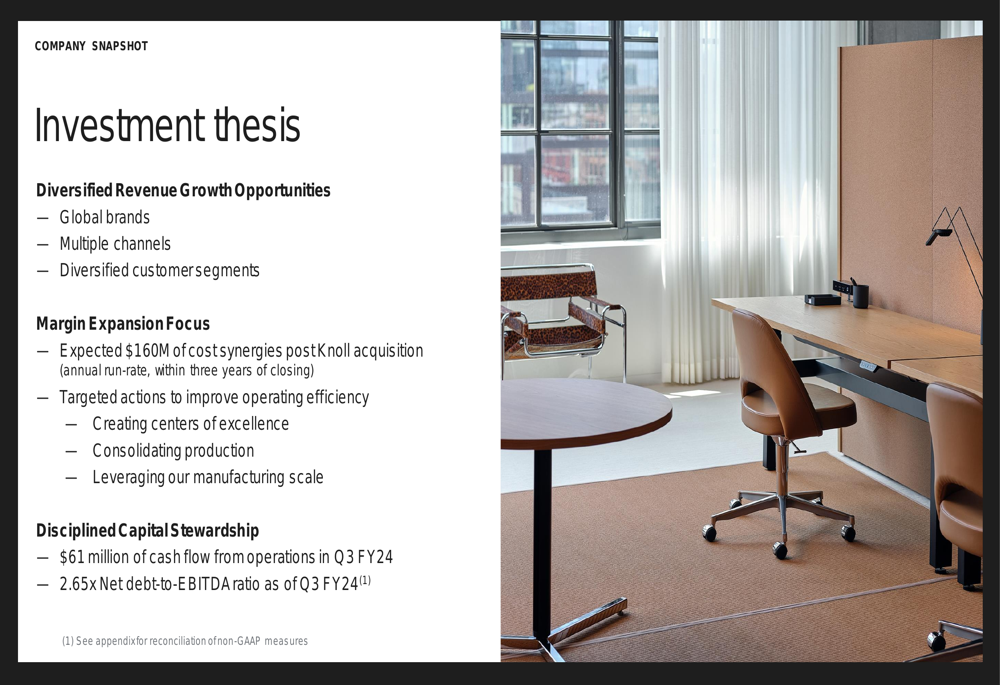

Investment Thesis

MillerKnoll presents its investment case based on three pillars: diversified revenue growth opportunities, margin expansion focus, and disciplined capital stewardship.

The company’s diversified portfolio across global brands, multiple channels, and various customer segments provides multiple avenues for growth. The margin expansion strategy centers on realizing synergies from the Knoll acquisition and improving operational efficiency. Finally, the disciplined approach to capital management aims to balance growth investments with debt reduction and shareholder returns.

This investment thesis is captured in the following slide:

As MillerKnoll continues to execute its strategy, investors will be watching for signs of revenue stabilization and further margin improvement. The recent outperformance in Q4 FY24 suggests the company is making progress on its strategic initiatives despite market headwinds.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.