Powell speech takes center stage in Tuesday’s economic events

Introduction & Market Context

Millrose Properties Inc (NYSE:MRP) reported strong second quarter 2025 results on July 31, with net income rising to $112.8 million and significant expansion of its third-party business beyond its Lennar (NYSE:LEN) relationship. The company’s stock rose 2.82% in premarket trading to $31.40, approaching its 52-week high of $31.56.

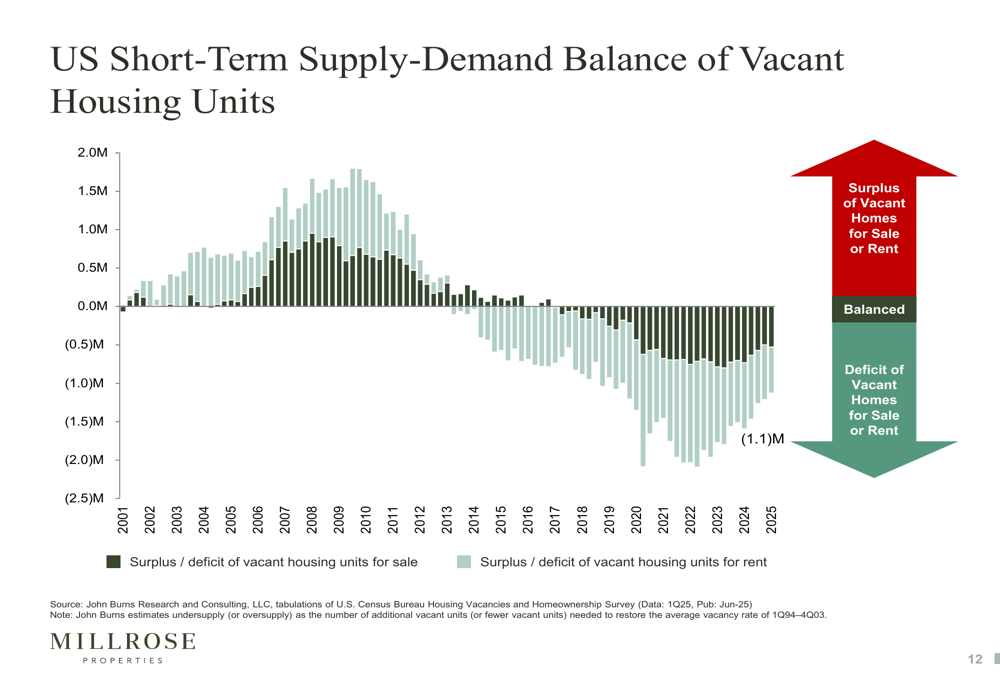

The real estate investment trust continues to benefit from structural tailwinds in the housing market, including a significant deficit of available housing units and historically high homebuilder margins, despite cyclical headwinds.

As shown in the following chart illustrating the housing supply deficit, there is currently a shortage of approximately 1.1 million vacant housing units in the U.S. market:

Quarterly Performance Highlights

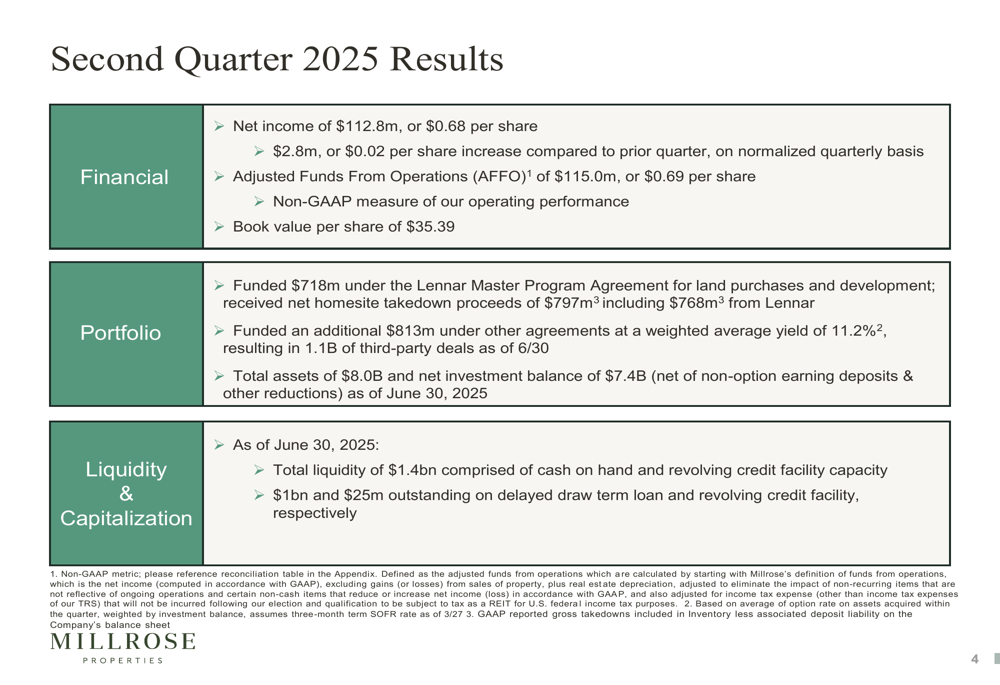

Millrose Properties delivered net income of $112.8 million ($0.68 per share) for Q2 2025, representing a $2.8 million or $0.02 per share increase compared to the previous quarter. This marks significant growth from the $64.8 million ($0.39 per share) reported in Q1 2025.

The company’s Adjusted Funds From Operations (AFFO) reached $115.0 million or $0.69 per share, supporting a quarterly dividend of $114.5 million ($0.69 per share), up from $0.38 in the previous quarter. This maintains Millrose’s commitment to distributing 100% of earnings to shareholders.

The following slide summarizes the key financial results for the second quarter:

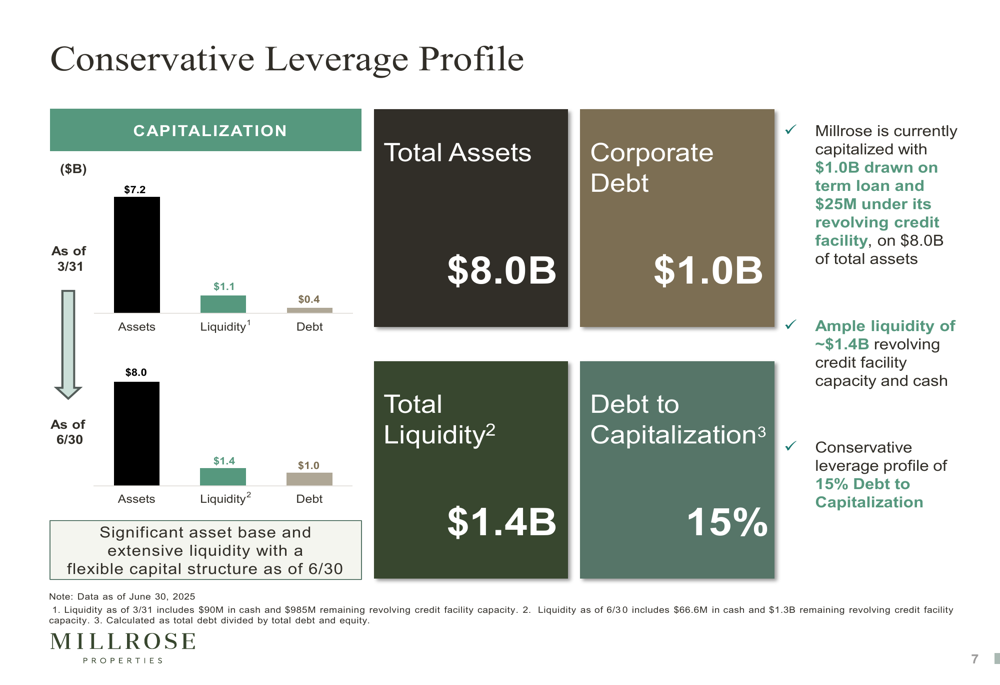

Total (EPA:TTEF) assets grew to $8.0 billion as of June 30, 2025, up from $7.2 billion at the end of Q1. The company’s net investment balance reached $7.4 billion, while maintaining a strong liquidity position of $1.4 billion, comprised of cash on hand and revolving credit facility capacity.

Detailed Financial Analysis

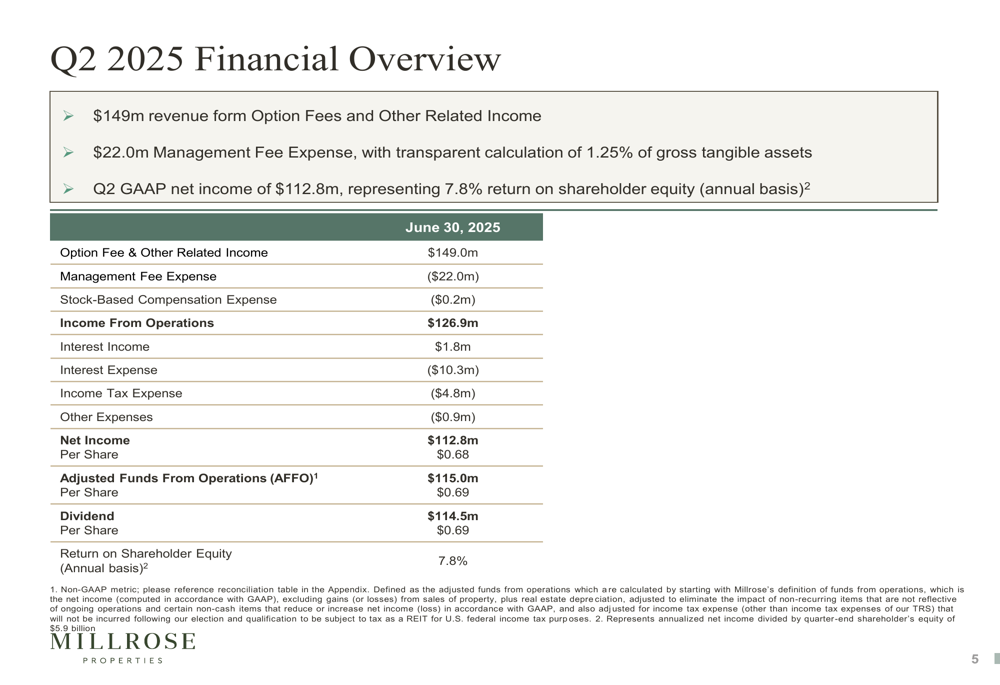

Millrose Properties generated $149 million in revenue from option fees and other related income during Q2 2025. The company achieved a 7.8% return on shareholder equity (annualized basis), representing a 20 basis point increase from the previous quarter.

The detailed financial breakdown is illustrated in the following income statement:

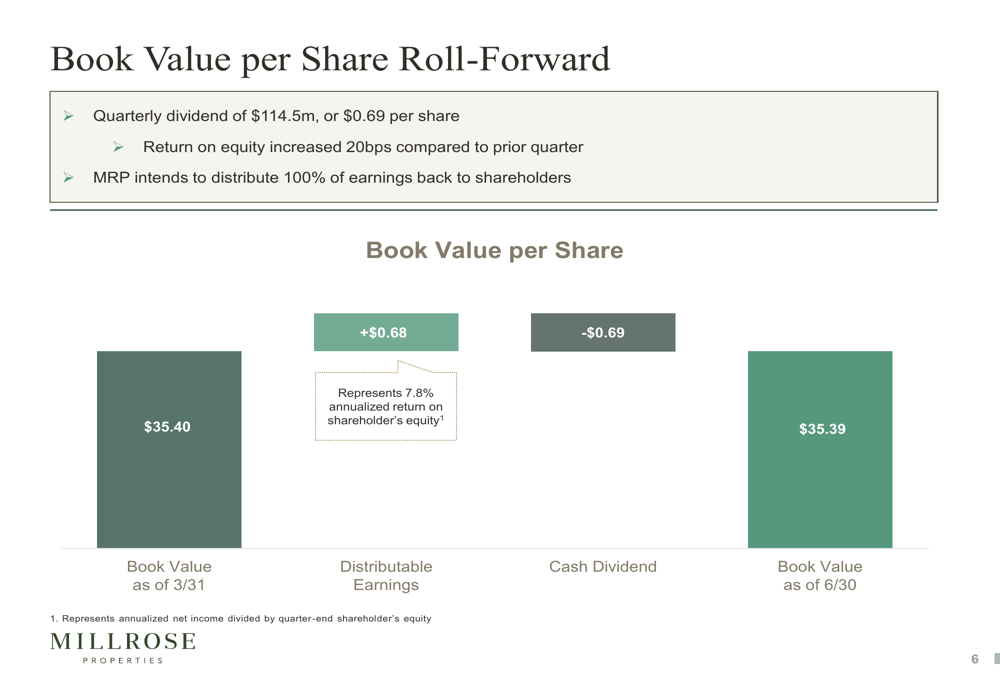

The company’s book value per share remained relatively stable at $35.39 as of June 30, compared to $35.40 at the end of March. This stability reflects Millrose’s balanced approach of returning earnings to shareholders through dividends while maintaining its equity base.

As shown in the following book value roll-forward:

Millrose maintained a conservative leverage profile with debt to capitalization of 15%, though this represents an increase from the 5% reported in Q1 2025. The company drew $1.0 billion on its term loan and $25 million under its revolving credit facility, against $8.0 billion of total assets.

The following chart illustrates the company’s capital structure:

Strategic Initiatives

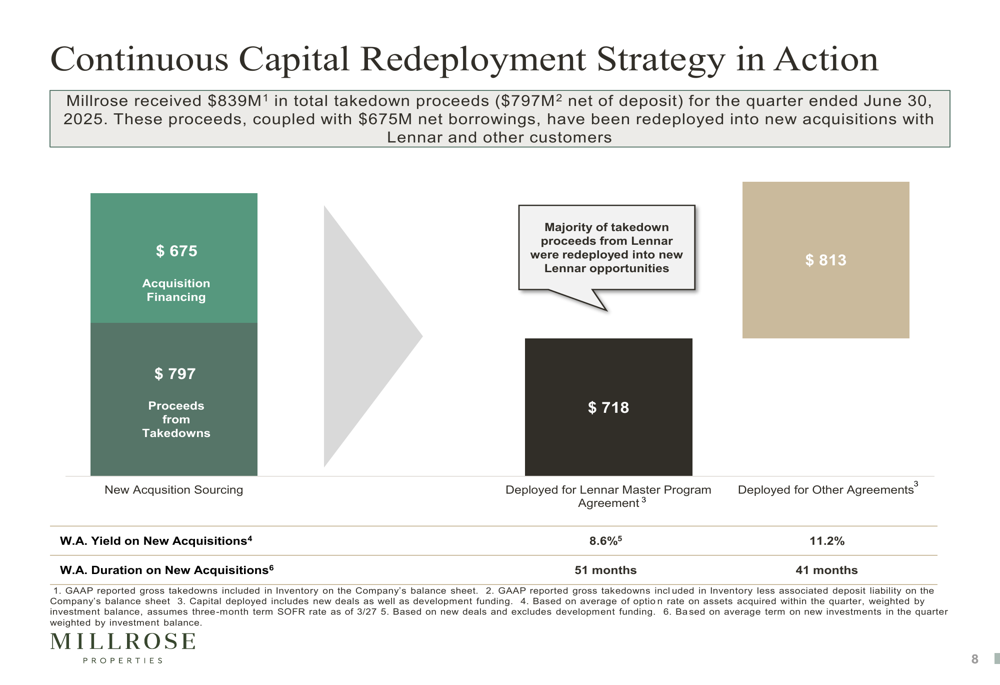

A key development in Millrose’s strategy is the significant expansion of business beyond its Lennar Master Program Agreement. While the company funded $718 million under the Lennar agreement during Q2, it deployed $813 million under other agreements at a weighted average yield of 11.2%, considerably higher than the 8.5% yield on Lennar investments.

The company’s continuous capital redeployment strategy is illustrated below:

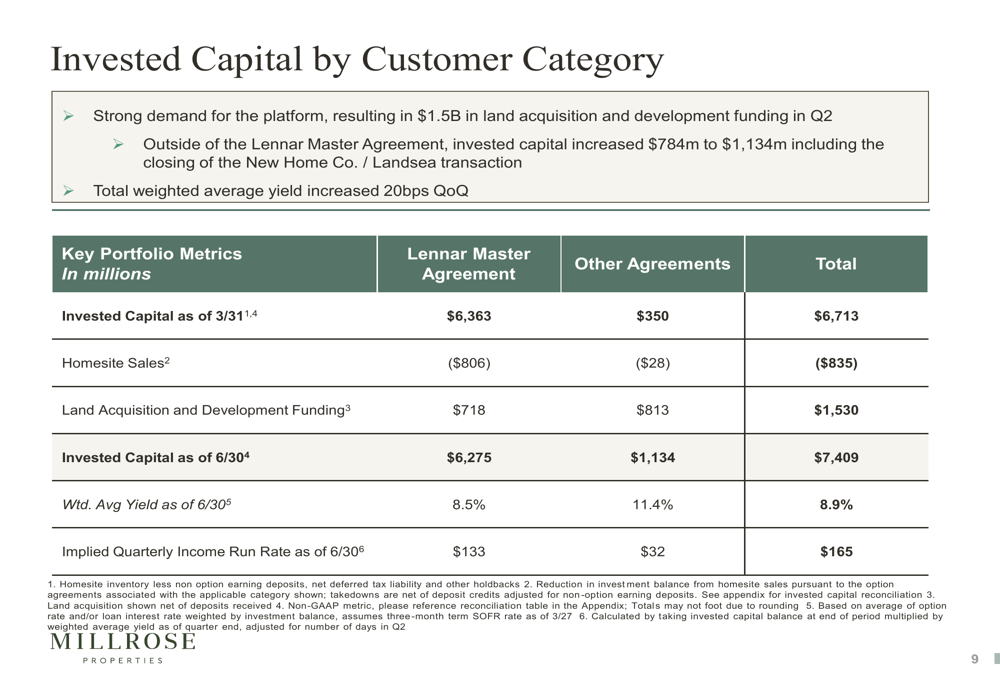

This expansion has resulted in non-Lennar invested capital increasing by $784 million to $1.13 billion during the quarter. The total weighted average yield across all investments increased by 20 basis points quarter-over-quarter to 8.9%.

As shown in the following breakdown of invested capital by customer category:

After the quarter end, Millrose announced a significant partnership with Taylor Morrison (NYSE:TMHC)’s "Yardly" build-to-rent platform. On July 23, 2025, Taylor Morrison and Kennedy Lewis (JO:LEWJ) Investment Management announced a $3 billion Financing Facility Agreement for Built-to-Rent Communities, with Millrose securing a right-of-first-refusal for funding during the 2.5-year term of the exclusivity agreement.

Competitive Industry Position

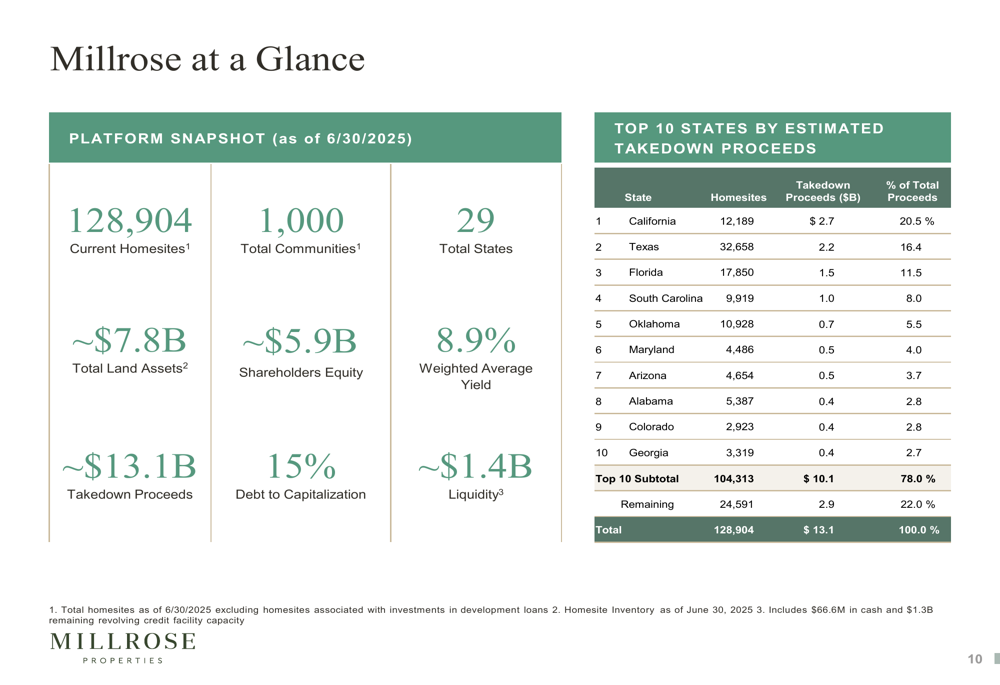

Millrose Properties continues to benefit from favorable industry dynamics. The company’s platform now encompasses 128,904 homesites across 1,000 communities in 29 states, with total land assets of approximately $7.8 billion.

The following snapshot provides an overview of Millrose’s scale and geographic diversification:

The company’s business model aligns with the growing trend of public homebuilders increasing their market share while reducing direct land ownership. This shift has created opportunities for land banking services like those provided by Millrose.

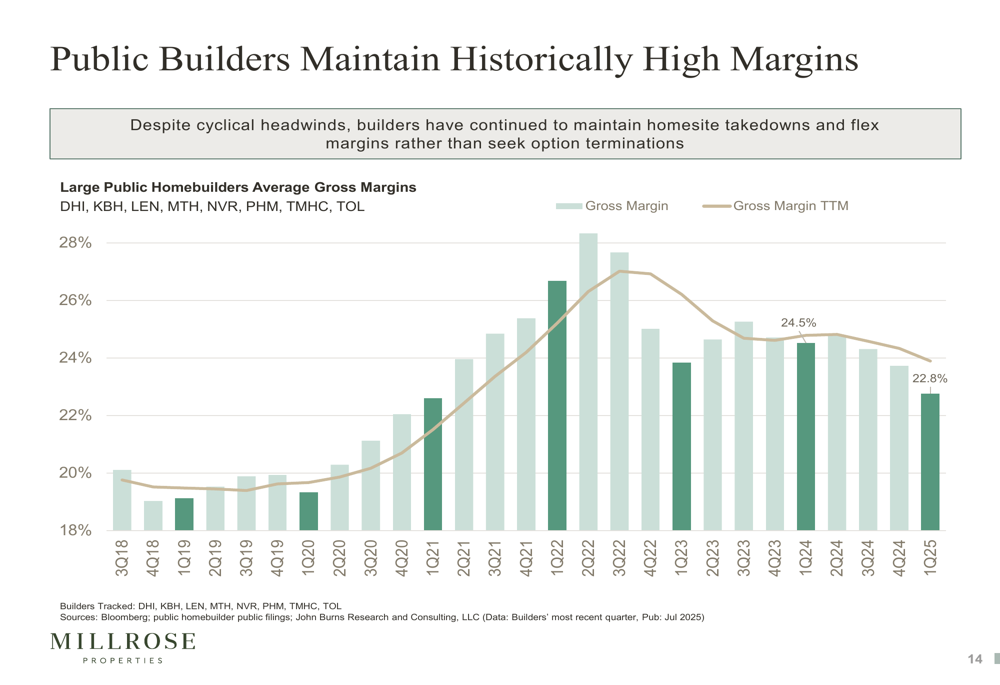

Public builders have maintained historically high margins despite market challenges, with gross margins at 22.8% in Q1 2025, as illustrated below:

Forward-Looking Statements

Millrose Properties appears well-positioned to continue its growth trajectory, with significant liquidity to fund new investments. The company has already deployed an additional approximately $200 million outside of the Lennar Master Program Agreement as of July 31st, including initial closings under the Taylor Morrison Yardly facility.

The expansion into the build-to-rent sector through the Taylor Morrison partnership represents a strategic diversification that could provide additional growth opportunities beyond traditional homebuilding.

With housing inventory remaining historically low and homebuilder leverage at record lows, the structural tailwinds supporting Millrose’s business model appear intact despite potential interest rate and economic uncertainties.

The company’s conservative financial approach, with 15% debt to capitalization, provides flexibility to navigate potential market volatility while continuing to fund growth opportunities and maintain its dividend policy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.