AZTR receives NYSE delisting warning over equity requirement

Introduction & Market Context

Mission Produce Inc (NASDAQ:AVO), a global leader in fresh produce, presented its fiscal third-quarter 2025 results on September 8, showcasing record revenue performance driven by strong volume growth despite avocado price pressures. The company’s stock responded positively, rising 1.9% to $12.87 in after-hours trading following the presentation.

As a vertically integrated avocado producer serving customers in over 25 countries, Mission Produce has leveraged its global sourcing network to navigate seasonal supply variations and deliver consistent results. The company’s diversification strategy across products and regions has proven effective in the competitive fresh produce market.

Quarterly Performance Highlights

Mission Produce reported record third-quarter revenue of $357.7 million, representing a 10% increase year-over-year. This growth was primarily driven by robust avocado sales volume, which increased by 10% to 183.5 million pounds, offsetting a 5% decrease in average selling price to $1.74 per pound.

The company’s adjusted EBITDA reached $32.6 million, up 3% compared to the same period last year, while adjusted earnings per share came in at $0.26, significantly exceeding analyst forecasts of $0.155. Mission also generated strong operating cash flow of $34 million during the quarter.

CEO Steve Barnard highlighted the company’s resilience in his commentary: "Our third-quarter results really demonstrate what we’ve been building here at Mission Produce, specifically the ability to consistently deliver strong performance no matter what the market throws at us."

Detailed Financial Analysis

Mission Produce’s financial performance showed strength across multiple metrics. While the 10% revenue growth was impressive, the company’s gross profit increase of 22% to $45.1 million demonstrates effective cost management despite price pressures in the avocado market.

The company’s adjusted net income reached $18.2 million, up from $16.7 million in the prior year period. This performance reflects Mission’s ability to leverage its vertically integrated model and global sourcing capabilities to maintain profitability even as average selling prices declined.

The International Farming segment was particularly strong, with adjusted EBITDA more than doubling year-over-year due to higher avocado yields and expanded packing and cooling services. This segment’s performance underscores the value of Mission’s diversified approach to production and services.

Strategic Initiatives

Mission’s presentation emphasized its diversification strategy, which extends beyond avocados to include mangos and blueberries, strengthening the company’s year-round offerings beyond peak avocado seasons. This portfolio expansion helps mitigate seasonal fluctuations and provides more consistent revenue streams.

The company’s global sourcing network remains a key competitive advantage. Mission’s ability to source avocados from multiple regions throughout the year ensures reliable supply for customers regardless of seasonal variations or weather-related disruptions in specific growing regions.

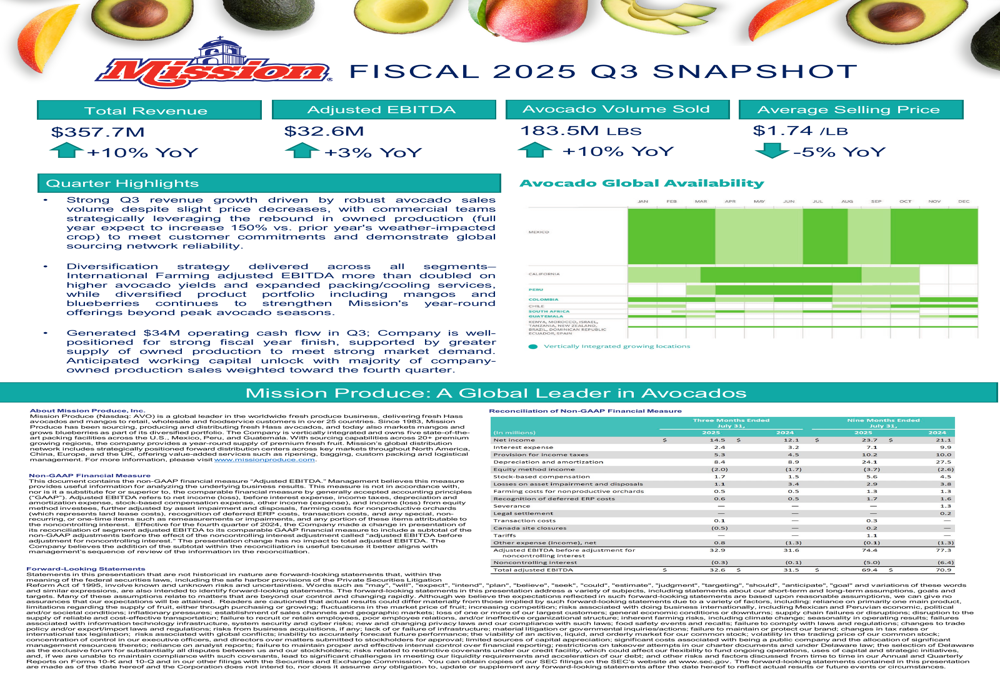

As shown in the following chart of global avocado availability:

The chart illustrates how Mission strategically sources from different regions throughout the year, with Mexico and Guatemala providing year-round supply, while regions like California, Peru, Colombia, and Chile offer seasonal production windows. This diversified sourcing approach enables Mission to maintain consistent supply despite regional growing seasons.

The company’s owned production is rebounding significantly, with full-year production expected to increase 150% compared to the prior year’s weather-impacted crop. This increased production allows Mission to better meet customer commitments and demonstrate the reliability of its global sourcing network.

Forward-Looking Statements

Mission Produce appears well-positioned for a strong finish to fiscal year 2025, supported by greater supply from owned production to meet market demand. The company anticipates a working capital unlock in the fourth quarter, as the majority of company-owned production sales are weighted toward that period.

According to the earnings call, Mission expects continued growth in blueberry volumes in Q4 and Q1, though avocado pricing is projected to decrease by 20-25% in Q4. The company maintains a net debt-to-adjusted EBITDA ratio of approximately 1x, indicating a healthy balance sheet position.

While Mission faces some headwinds, including an estimated $10 million annual tariff impact (less than 1% of total cost of goods sold), the company’s strong financial health score of 2.79 and Altman Z-Score of 3.53 suggest solid financial stability. No significant new acreage expansion is planned for avocados or mangoes in the next 3-5 years, indicating a focus on optimizing existing operations rather than aggressive expansion.

John Pawlowski, President and COO, summarized the company’s positioning: "The level of operational sophistication and international reach here at Mission is remarkable." With its diversified product portfolio, global sourcing network, and vertical integration, Mission Produce appears well-equipped to navigate market challenges while continuing to deliver growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.