Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

Modine Manufacturing Company (NYSE:MOD) reported its first quarter fiscal 2026 results on July 31, 2025, highlighting continued momentum in its Climate Solutions segment while navigating challenges in its Performance Technologies business. The thermal management solutions provider saw its stock trading at $111.95 at market close on July 30, with after-hours movement showing a 1.56% increase to $113.70.

The company’s presentation revealed a tale of two segments: robust growth in data center and HVAC technologies contrasted with ongoing weakness in vehicular markets. This divergence reflects Modine’s strategic pivot toward higher-margin climate control solutions, particularly in the rapidly expanding data center infrastructure space.

Quarterly Performance Highlights

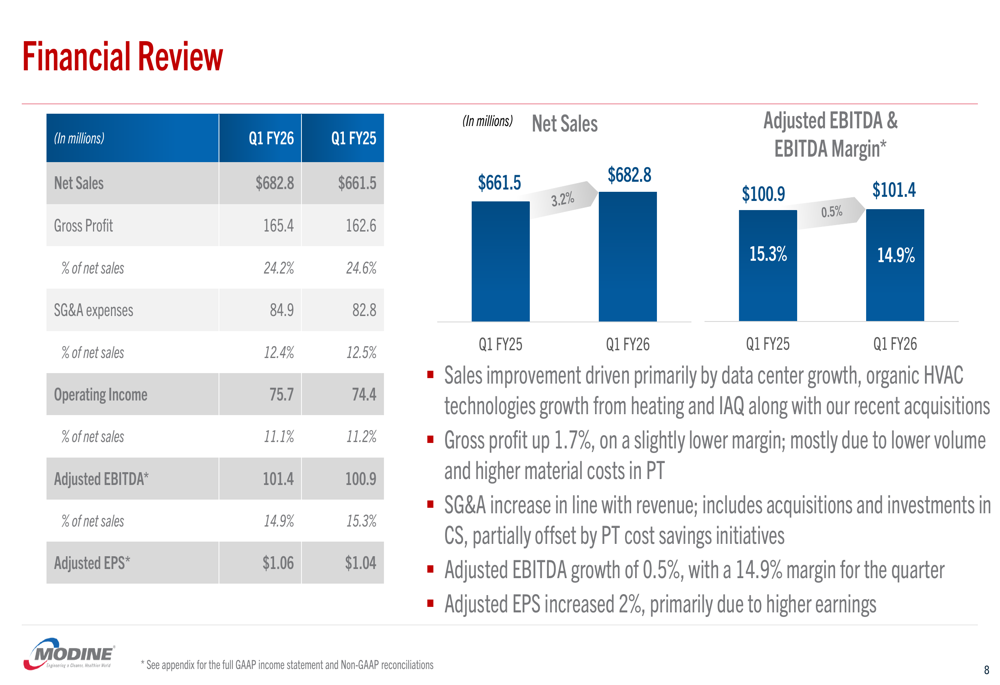

Modine reported Q1 FY26 net sales of $682.8 million, a 3.2% increase from $661.5 million in the same period last year. Adjusted EBITDA rose slightly to $101.4 million from $100.9 million, though the margin contracted to 14.9% from 15.3%. Adjusted earnings per share increased to $1.06 from $1.04 year-over-year.

The company’s performance was primarily driven by strong results in the Climate Solutions segment, which saw significant growth in both revenue and profitability.

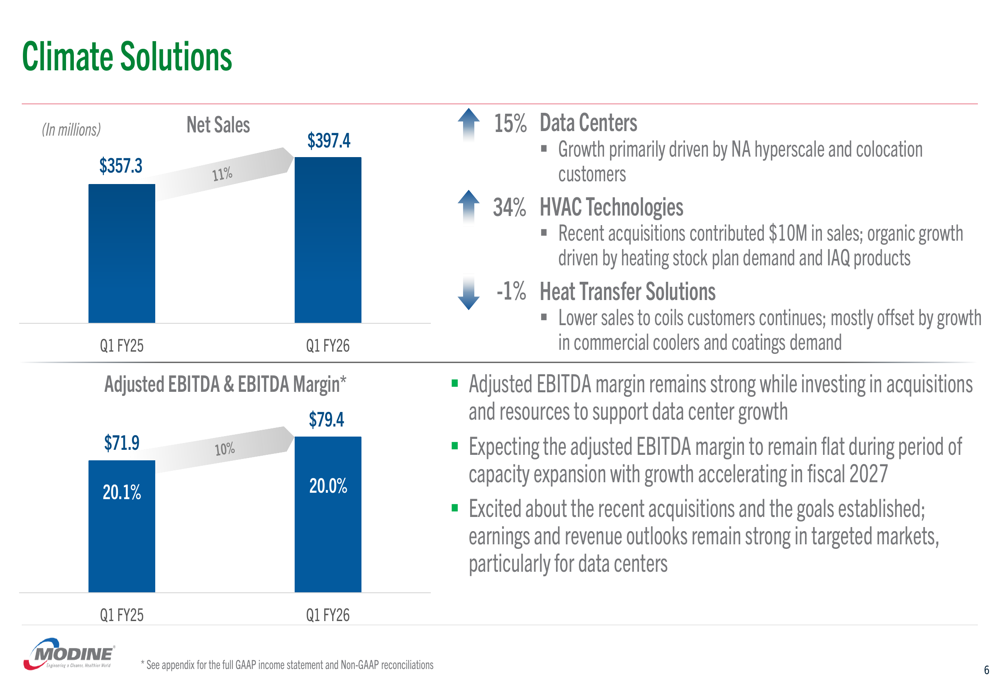

As shown in the following financial performance chart for Climate Solutions:

Climate Solutions delivered impressive results with net sales increasing 11% to $397.4 million and adjusted EBITDA rising 10% to $79.4 million. The segment maintained a robust 20.0% EBITDA margin, nearly unchanged from 20.1% in the prior year. Data Centers led the growth with a 15% increase, while HVAC Technologies surged 34%, partially offset by a 1% decline in Heat Transfer Solutions.

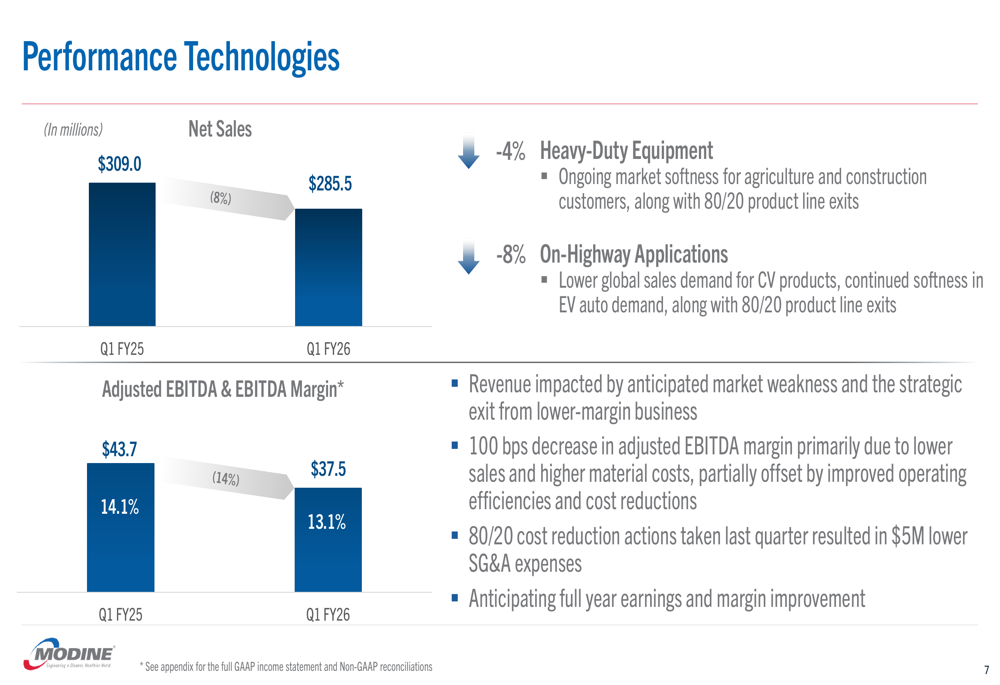

In contrast, the Performance Technologies segment faced headwinds as illustrated in this chart:

Performance Technologies experienced an 8% decline in net sales to $285.5 million, with adjusted EBITDA falling 14% to $37.5 million. The segment’s EBITDA margin contracted to 13.1% from 14.1%. Heavy-Duty Equipment sales decreased by 4% while On-Highway Applications fell by 8%, reflecting broader market weakness in vehicular sectors.

Strategic Initiatives

Modine’s presentation emphasized its strategic focus on expanding data center capabilities, which has become a key growth driver for the company. Management highlighted a $100 million capacity expansion initiative in North America to capitalize on increasing demand for data center cooling solutions.

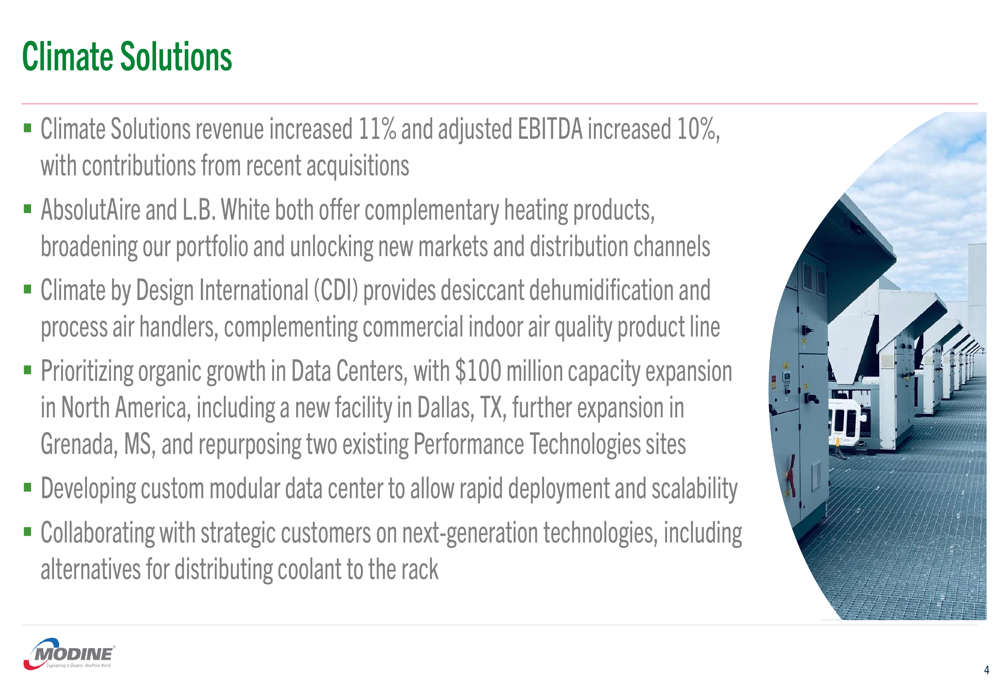

The Climate Solutions segment is benefiting from recent strategic acquisitions that have broadened Modine’s product portfolio. These include AbsolutAire and L.B. White, which offer complementary heating products, and Climate by Design International (CDI), which provides desiccant dehumidification and process air handlers.

As illustrated in the Climate Solutions overview:

The company is developing custom modular data centers designed for rapid deployment and scalability, positioning Modine to capture additional market share in this high-growth sector. Management also noted ongoing collaboration with strategic customers on next-generation technologies, reinforcing the company’s commitment to innovation.

Despite challenges in the Performance Technologies segment, Modine is implementing strategic adjustments, including evaluating the transition of two manufacturing sites to expand data center capacity. The company has maintained tight cost controls, achieving $5 million in lower SG&A expenses through its 80/20 cost reduction initiatives.

Financial Position

Modine’s overall financial results for Q1 FY26 showed modest growth despite the mixed segment performance:

The company reported free cash flow of $0.2 million for the quarter, significantly lower than the $13.7 million generated in Q1 FY25. This reduction was attributed to inventory build-up to support future data center deliveries. Capital expenditures totaled $28 million, reflecting investments in capacity expansion.

Net debt increased to $403 million as of June 30, 2025, up from $279.2 million at the end of March 2025, primarily due to recent acquisitions. Despite this increase, Modine maintained a conservative leverage ratio of 1.0x, indicating a strong balance sheet position. The company also highlighted its recently upsized and extended credit facilities, which provide additional financial flexibility to support both organic growth and acquisition initiatives.

Forward-Looking Statements

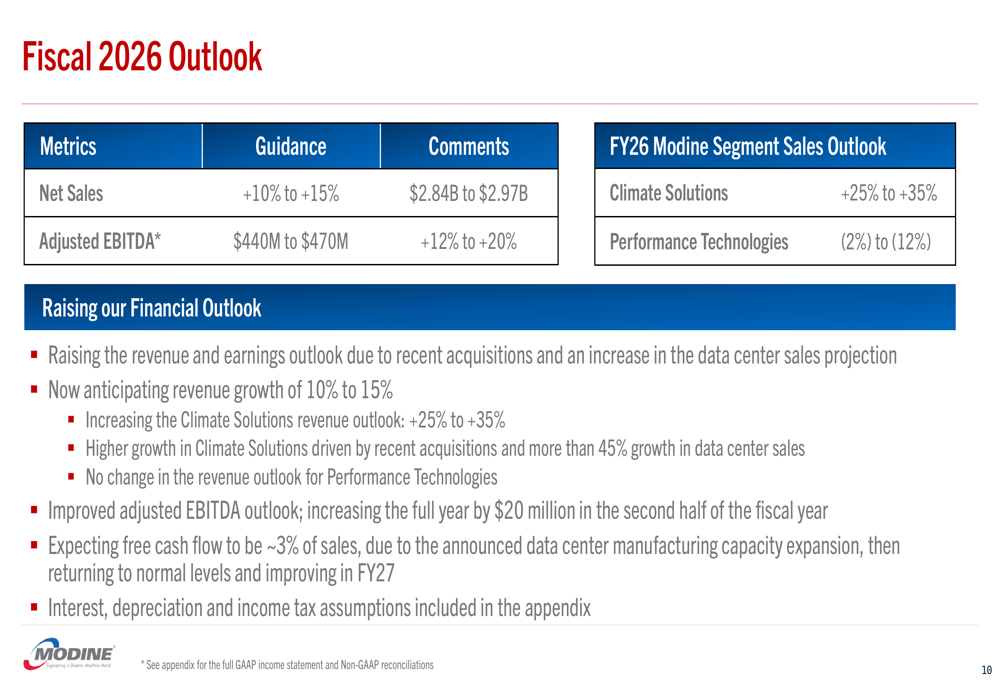

Looking ahead, Modine provided an optimistic outlook for fiscal 2026:

The company raised its full-year guidance, now projecting net sales growth of 10% to 15% ($2.84 billion to $2.97 billion) and adjusted EBITDA of $440 million to $470 million (12% to 20% increase). This improved outlook reflects stronger-than-expected performance in the data center market and contributions from recent acquisitions.

By segment, Modine expects Climate Solutions sales to grow 25% to 35%, while Performance Technologies sales are projected to decline 2% to 12%, reflecting continued market weakness in vehicular sectors.

Management anticipates free cash flow to be approximately 3% of sales for the fiscal year, temporarily impacted by data center manufacturing capacity expansion. The company expects free cash flow to return to normal levels and improve in fiscal 2027 as these investments begin to generate returns.

The presentation suggests Modine is successfully executing its strategic transformation toward higher-margin climate control solutions, particularly in the data center space, while managing through cyclical weakness in traditional vehicular markets. With a strong balance sheet and focused investment strategy, the company appears well-positioned to deliver on its growth objectives despite mixed market conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.