60%+ returns in 2025: Here’s how AI-powered stock investing has changed the game

Introduction & Market Context

Mohawk Industries (NYSE:MHK), the world's largest flooring company, delivered stable financial results in Q2 2025 despite challenging market conditions. The company reported flat year-over-year net sales of $2.8 billion while posting adjusted earnings per share of $2.77, reflecting operational improvements and cost containment initiatives in a difficult housing market environment.

Mohawk's shares responded positively to the results, with the stock rising 4.94% to close at $119.25 following the earnings release. The company continues to navigate a market characterized by cautious consumer confidence, low housing turnover, and high interest rates, while positioning itself for an eventual recovery.

As shown in the following overview of Mohawk's global scale and scope:

Quarterly Performance Highlights

Mohawk's Q2 2025 results demonstrated the company's ability to maintain performance despite market headwinds. The company generated $126 million in free cash flow during the quarter and announced a new $500 million share repurchase program after buying back approximately 393,000 shares for $42 million in the quarter.

The quarterly performance metrics reveal stable operations with adjusted EBITDA of $371 million and adjusted operating income of $223 million:

Segment performance varied across the company's three reporting divisions:

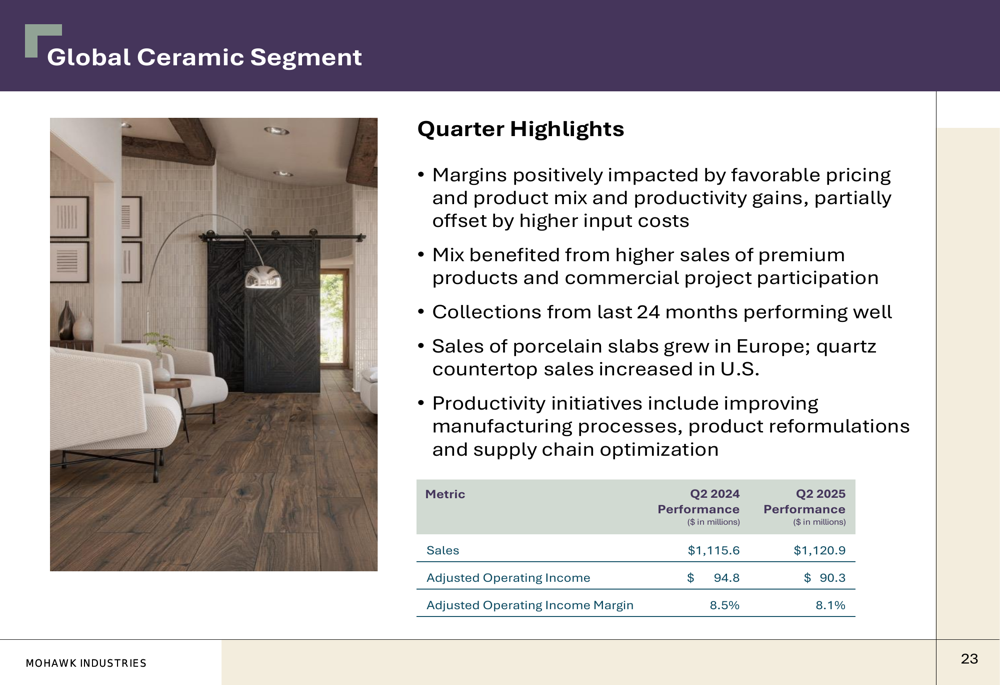

The Global Ceramic segment posted a slight increase in sales to $1.12 billion but experienced a margin decline from 8.5% to 8.1% year-over-year. The segment benefited from favorable pricing and product mix, particularly from higher sales of premium products and commercial projects:

The Flooring Rest of the World segment saw a modest sales increase to $734.4 million, though operating margins declined from 12.6% to 10.4%. This segment was positively impacted by productivity gains while the company balanced sales actions to optimize topline in soft market conditions:

In contrast, the Flooring North America segment experienced a slight sales decline to $946.8 million but improved its operating margin from 7.3% to 8.6%. The segment benefited from strong performance in hard surface categories and improved mix from new product launches:

Strategic Initiatives

Mohawk continues to focus on operational excellence, with restructuring actions expected to deliver approximately $100 million in savings for 2025. The company is streamlining manufacturing processes, simplifying product offerings, and leveraging advanced technology to enhance productivity.

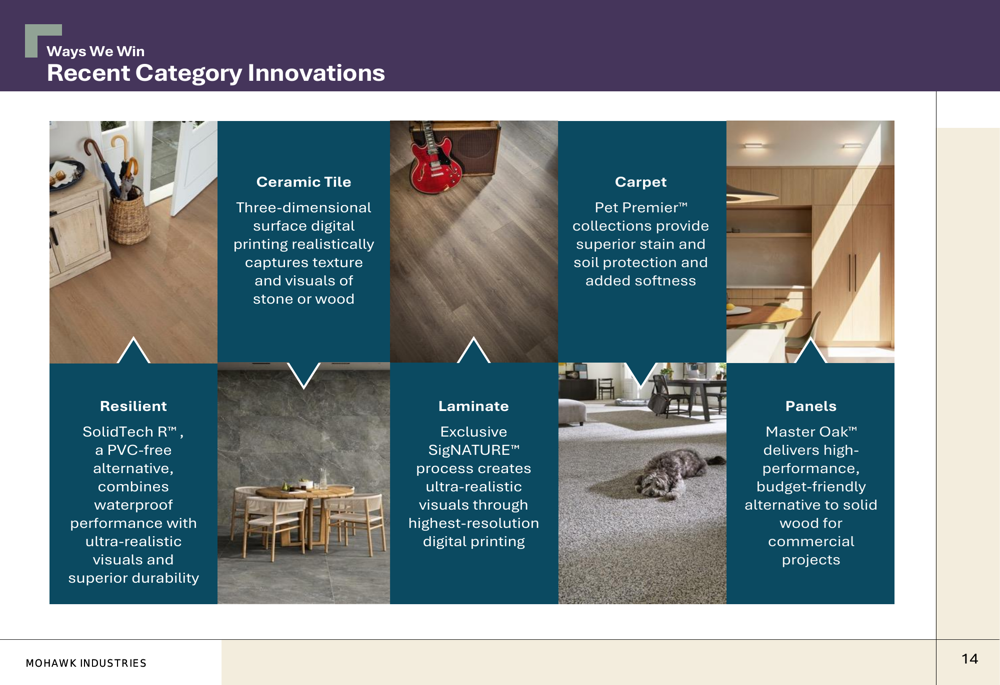

Product innovation remains a key differentiator for Mohawk, with recent category innovations including SolidTech R™ as a PVC-free resilient alternative, advanced ceramic tile with three-dimensional surface digital printing, and specialized carpet collections:

The company has maintained a disciplined approach to capital allocation, focusing on maintaining a strong balance sheet while reinvesting in the business, pursuing strategic acquisitions, and returning capital to shareholders:

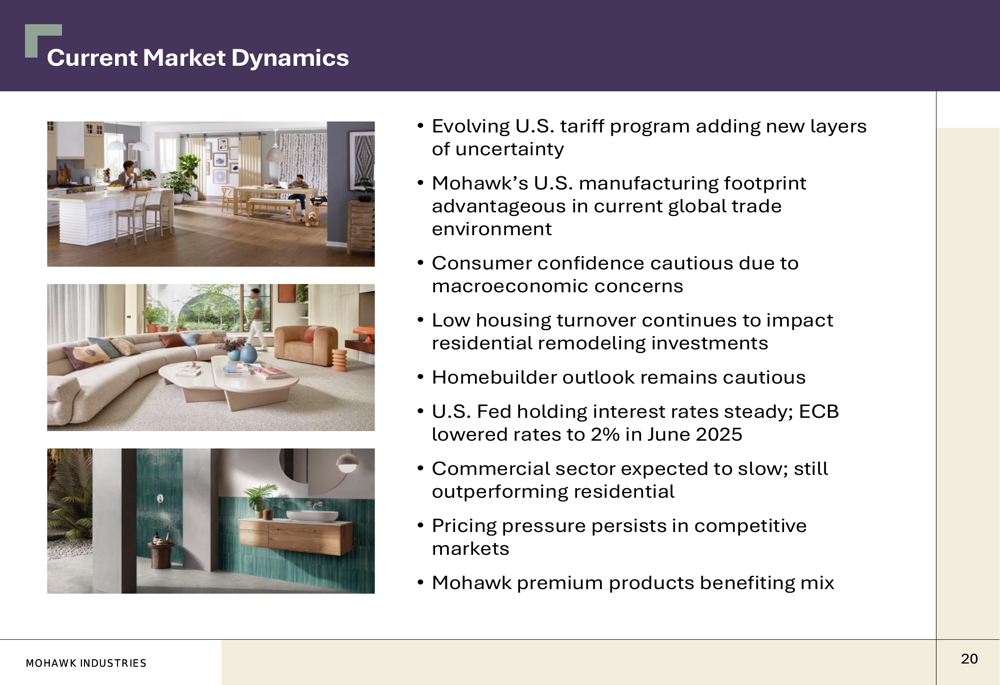

Market Dynamics and Outlook

Mohawk faces several market challenges, including evolving U.S. tariff programs, cautious consumer confidence, and low housing turnover. However, the company's domestic U.S. manufacturing footprint provides advantages in the current trade environment, while the commercial sector continues to outperform residential markets.

The company provided Q3 2025 guidance with expected adjusted EPS ranging from $2.56 to $2.66, reflecting continued market pressures but also the benefits of operational improvements.

Long-term industry trends suggest resilience, with historical data showing strong recovery following economic downturns. As illustrated in the following chart, the flooring industry has demonstrated a pattern of robust growth after previous recessions:

Financial Position

Mohawk maintains a strong financial position with a net debt to adjusted EBITDA ratio of 1.1x as of the end of 2024, down from 1.5x in 2023. This conservative leverage provides flexibility to navigate current market challenges while positioning the company to capitalize on future opportunities.

The company has generated substantial free cash flow, with $716 million in 2023 and $680 million in 2024. This has enabled Mohawk to return significant capital to shareholders, having repurchased approximately 15% of outstanding shares for $1.6 billion since 2020.

Mohawk's global geographic reach provides diversification benefits, with 55% of sales coming from the U.S., 29% from Europe, 7% from Latin America, and 9% from other regions:

Forward-Looking Statements

Looking ahead, Mohawk expects market conditions to remain soft in the near term, with pricing pressure remaining elevated and higher input costs peaking in Q3. The company has reduced its 2025 capital expenditure projection to approximately $500 million to align with current market conditions.

Despite these challenges, management remains optimistic about the long-term outlook, citing significant future demand from the housing deficit and the expectation that industry volumes will eventually return to historical levels. The company believes its reduced cost structures and operational improvements position it well to benefit when the market recovers.

CEO Jeffrey Lorberbaum expressed confidence in the company's positioning, stating in the earnings call, "We are well positioned for the recovery that will occur," and noting that "historically, down cycles in our industry are followed by several years of sales growth from pent-up demand."

As Mohawk navigates the current market environment, its focus on operational excellence, product innovation, and financial discipline provides a foundation for sustainable performance and positions the company to capitalize on market recovery when it occurs.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.