Walmart halts H-1B visa offers amid Trump’s $100,000 fee increase - Bloomberg

Molson Coors Brewing Co (NYSE:TAP) shares fell nearly 6% in premarket trading after the company’s first-quarter presentation revealed significant declines across key metrics and a downward revision to its full-year guidance. The brewer reported results on May 8, 2025, highlighting challenges from macroeconomic headwinds and the impact of exiting major contract brewing agreements.

Quarterly Performance Highlights

The beer giant reported a 10.4% year-over-year decline in net sales revenue to $2.3 billion for Q1 2025, while underlying income before income taxes plummeted 49.5% to $131 million. Underlying earnings per share fell 47.4% to $0.50, significantly below the previous quarter’s performance when the company had beaten analyst expectations.

As shown in the following consolidated results table:

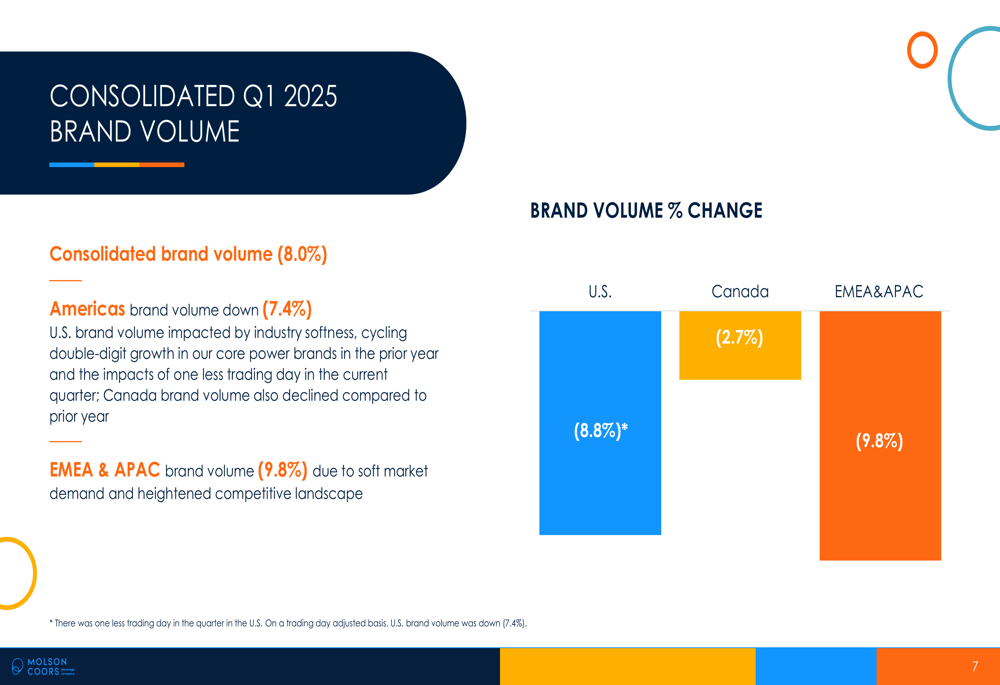

Financial volume decreased 14.3% year-over-year to 15.4 million hectoliters, while brand volume declined 8.0% to 15.5 million hectoliters. The company attributed these declines to several factors, including macroeconomic pressures, cycling significant inventory builds from the prior year, and the discontinuation of large contract brewing agreements with Pabst and Labatt.

Detailed Financial Analysis

The Americas region, which represents the bulk of Molson Coors’ business, saw net sales revenue decrease by 11.5% to $1.88 billion, with underlying income before income taxes falling 36.8% to $203 million. U.S. financial volumes were particularly hard hit, declining 15.6%.

The following chart illustrates the regional brand volume performance:

In the EMEA & APAC region, net sales revenue decreased 4.9% to $427 million, while the segment reported an underlying loss before income taxes of $19 million, representing a 22.5% worsening from the prior year. The company cited soft market demand and heightened competition across all markets in this region.

Cost pressures also impacted profitability, with underlying cost of goods sold per hectoliter increasing 6.1% in constant currency, driven by volume deleverage (420 basis point impact) and mix impacts (220 basis point impact).

Strategic Initiatives

Despite the challenging quarter, Molson Coors emphasized its continued focus on premiumization and portfolio expansion. The company highlighted that its U.S. core power brand collective volume share increased 1.9 points compared to 2023, with Coors Banquet emerging as the fastest-growing volume brand among the top 15 U.S. beer brands.

The company’s acceleration plan centers around premiumization, as illustrated in this strategic framework:

A key strategic development is the new partnership with Fever-Tree, which Molson Coors described as "immediately accretive" and adding meaningful scale to its non-alcoholic operations. This aligns with the company’s broader strategy of expanding beyond traditional beer categories.

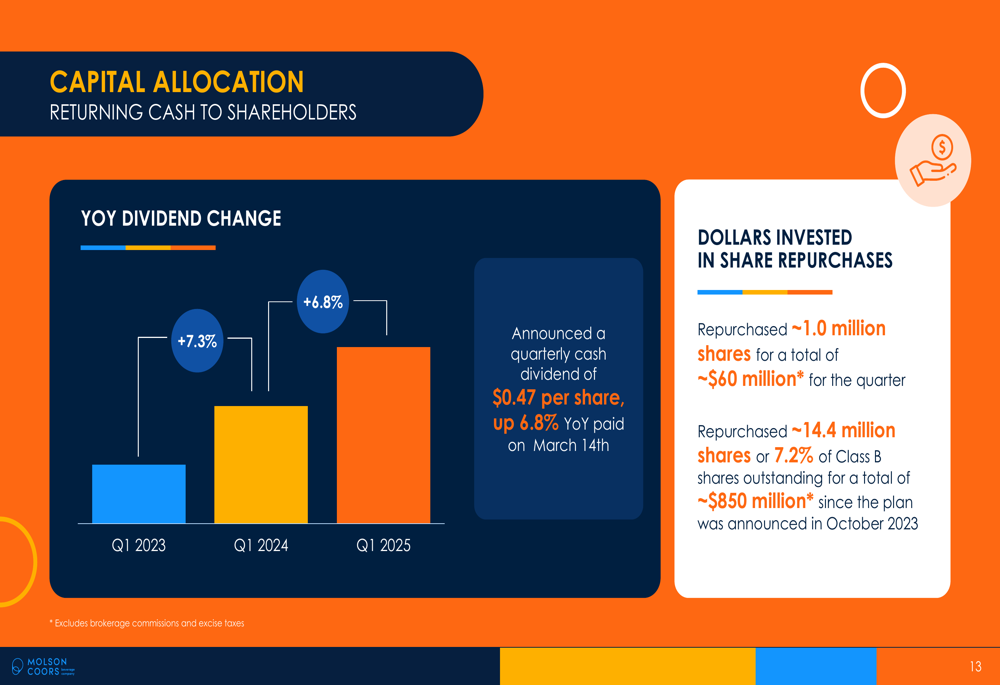

The company also continues to return cash to shareholders, increasing its quarterly dividend by 6.8% to $0.47 per share and repurchasing approximately 1 million shares for $60 million during the quarter. Since announcing its repurchase plan in October 2023, Molson Coors has bought back approximately 14.4 million shares (7.2% of Class B shares outstanding) for a total of $850 million.

The following chart shows the company’s dividend growth trend:

Forward-Looking Statements

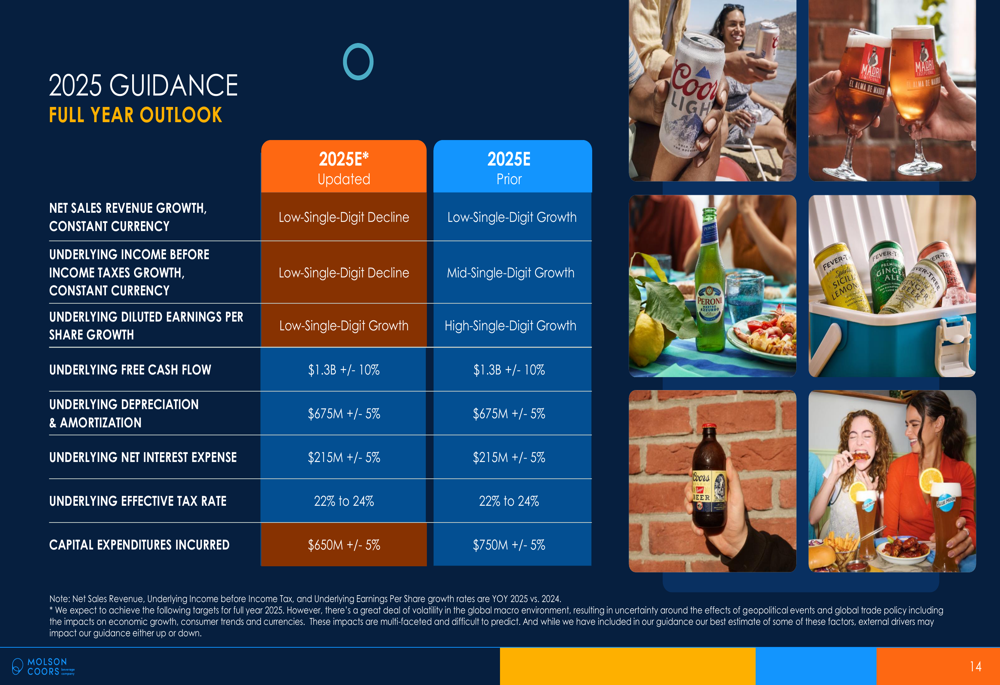

In a significant shift from its previous outlook, Molson Coors revised its full-year 2025 guidance downward across multiple metrics:

The company now expects a low-single-digit decline in net sales revenue (in constant currency), compared to its previous guidance of low-single-digit growth. Similarly, underlying income before income taxes is now projected to decline at a low-single-digit rate, versus the previously forecasted mid-single-digit growth.

Underlying diluted earnings per share growth expectations were lowered from high-single-digit to low-single-digit growth. The company also reduced its capital expenditure guidance to $650 million (±5%) from $750 million (±5%) previously.

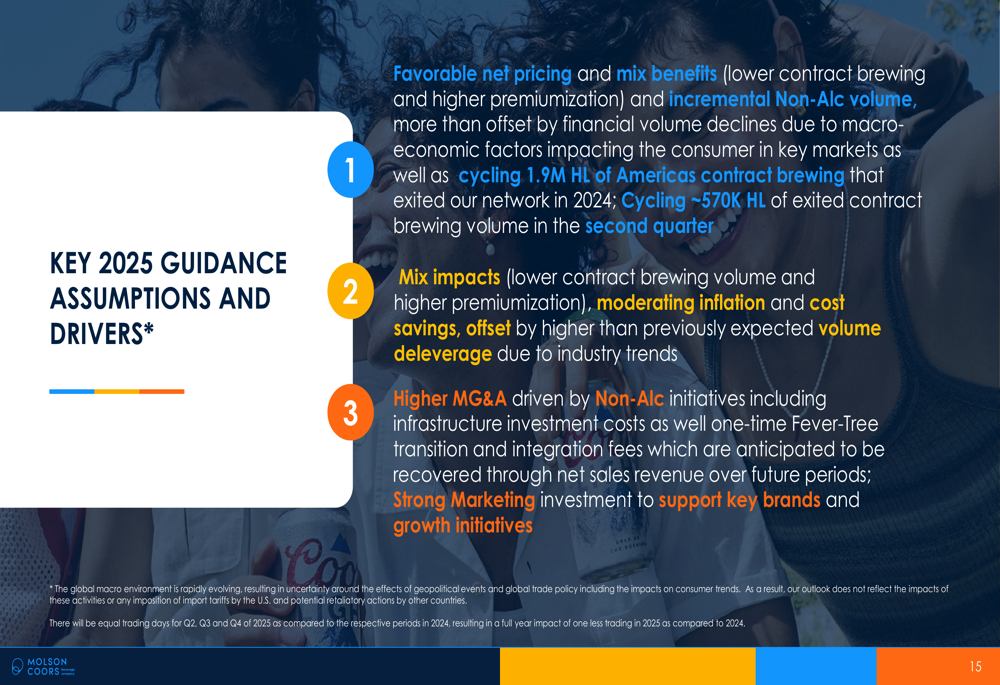

Key assumptions behind the revised guidance include:

This downward revision represents a stark contrast to the optimism following the company’s Q4 2024 results, when Molson Coors had reported better-than-expected earnings and projected growth across key metrics for 2025.

Despite the challenging start to the fiscal year, Molson Coors maintains that it is taking appropriate actions to mitigate short-term macroeconomic challenges while supporting its medium and long-term growth objectives through continued investment in its brands and strategic initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.