Fed Governor Adriana Kugler to resign

Introduction & Market Context

Mondelez International (NASDAQ:MDLZ) presented its second quarter 2025 results on July 29, showing accelerated revenue growth compared to Q1, while continuing to navigate significant headwinds from record-high cocoa prices. The global snacking giant demonstrated resilience in its pricing strategy and chocolate segment performance, though profitability remains under pressure.

The company’s presentation revealed a continuation of consumer behavior shifts across regions, with value-seeking becoming more prominent in North America, increased price elasticity in Europe, and a shift toward bulk and discount options in emerging markets. Despite these challenges, Mondelez maintained its full-year outlook, suggesting confidence in its ability to manage through the current environment.

Quarterly Performance Highlights

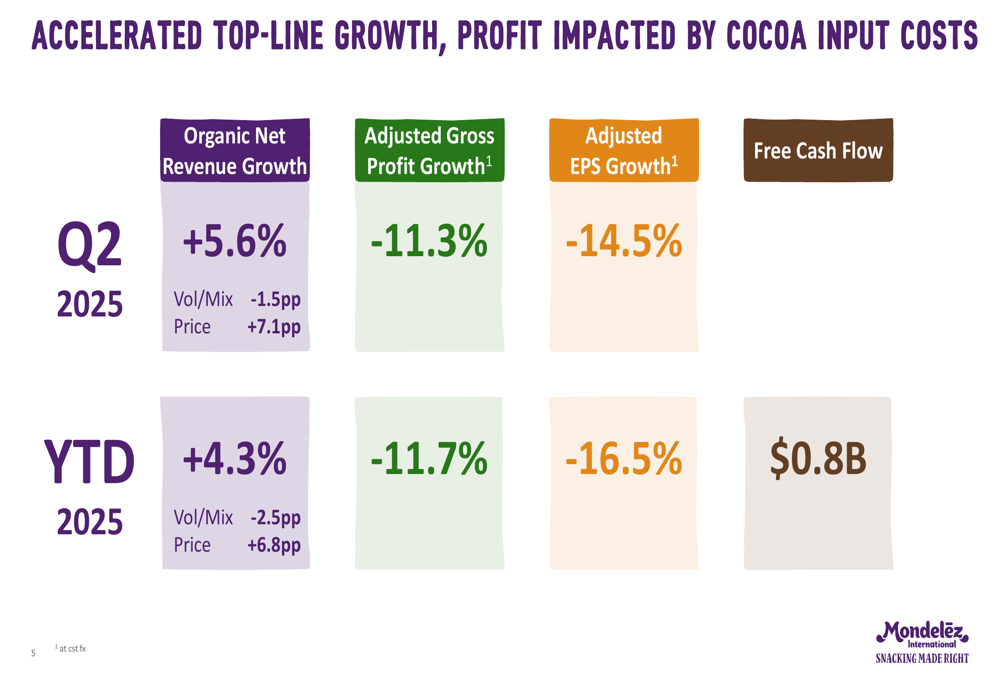

Mondelez reported organic net revenue growth of 5.6% for Q2 2025, a notable acceleration from the 3.1% growth reported in Q1. This growth was primarily driven by strong pricing (+7.1 percentage points), partially offset by volume/mix (-1.5 percentage points). However, adjusted gross profit declined by 11.3% and adjusted EPS fell by 14.5% compared to the prior year, primarily due to elevated cocoa input costs.

As shown in the following financial performance summary:

The company’s year-to-date performance follows a similar pattern, with organic net revenue growth of 4.3% driven by pricing (+6.8 percentage points) and partially offset by volume/mix (-2.5 percentage points). Free cash flow generation remained solid at $0.8 billion year-to-date.

Mondelez continues to return capital to shareholders, with $1.7 billion in share repurchases at an average price of $58.33 and $1.2 billion in dividends, including an announced 6% dividend increase.

Detailed Financial Analysis

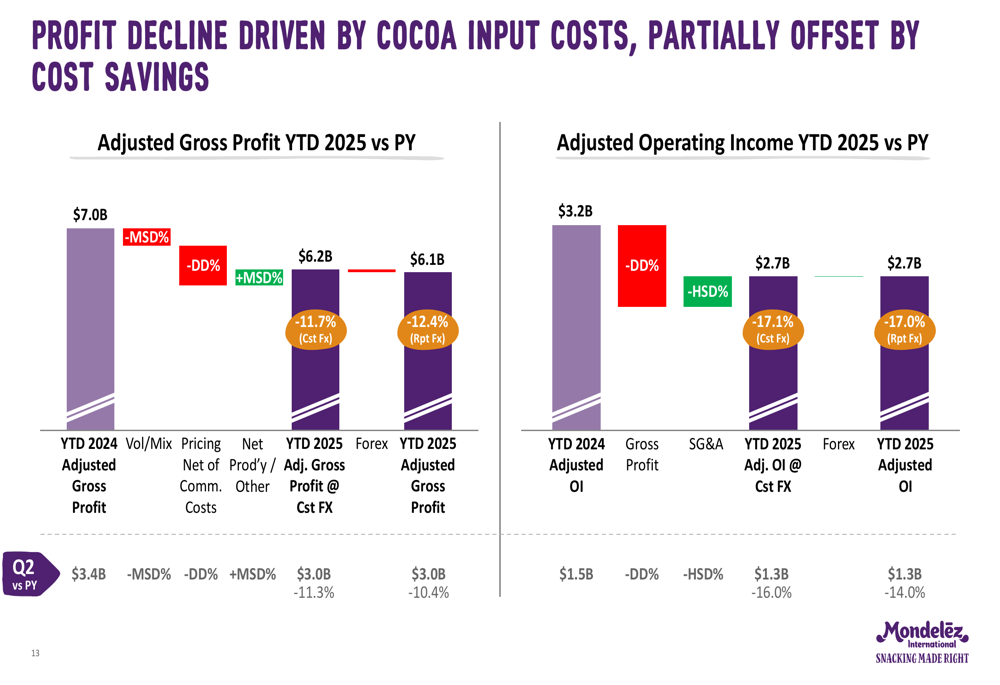

The most significant factor impacting Mondelez’s profitability continues to be the unprecedented rise in cocoa prices. The company’s presentation included a detailed breakdown of how these input costs have affected gross profit and operating income.

The following waterfall chart illustrates the components driving the decline in adjusted gross profit and operating income:

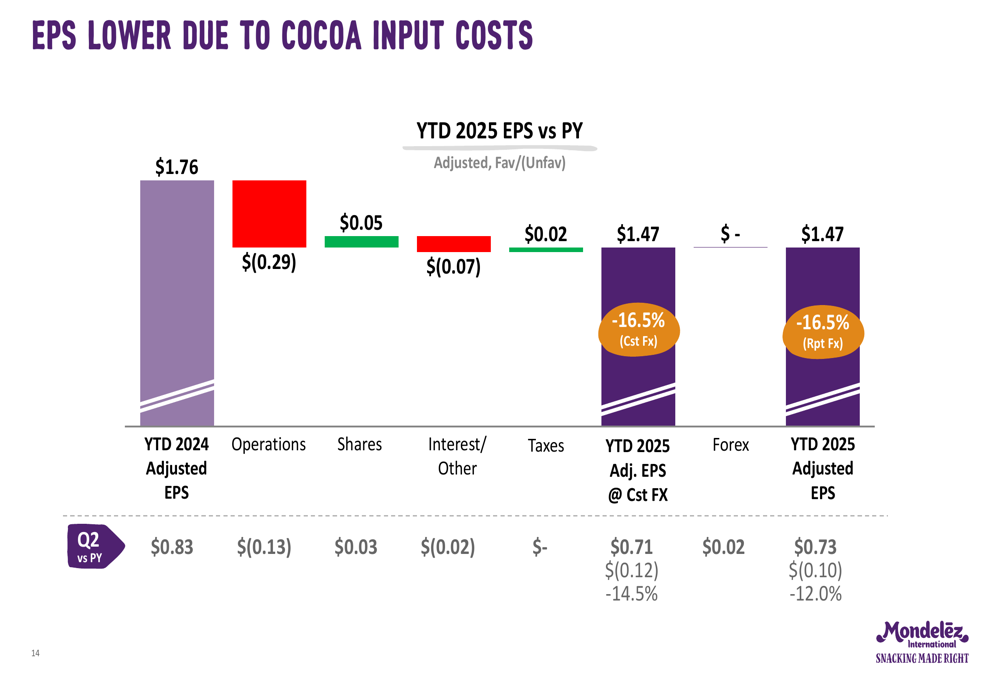

Similarly, the decline in EPS can be attributed primarily to operational challenges related to cocoa costs, as shown in this breakdown:

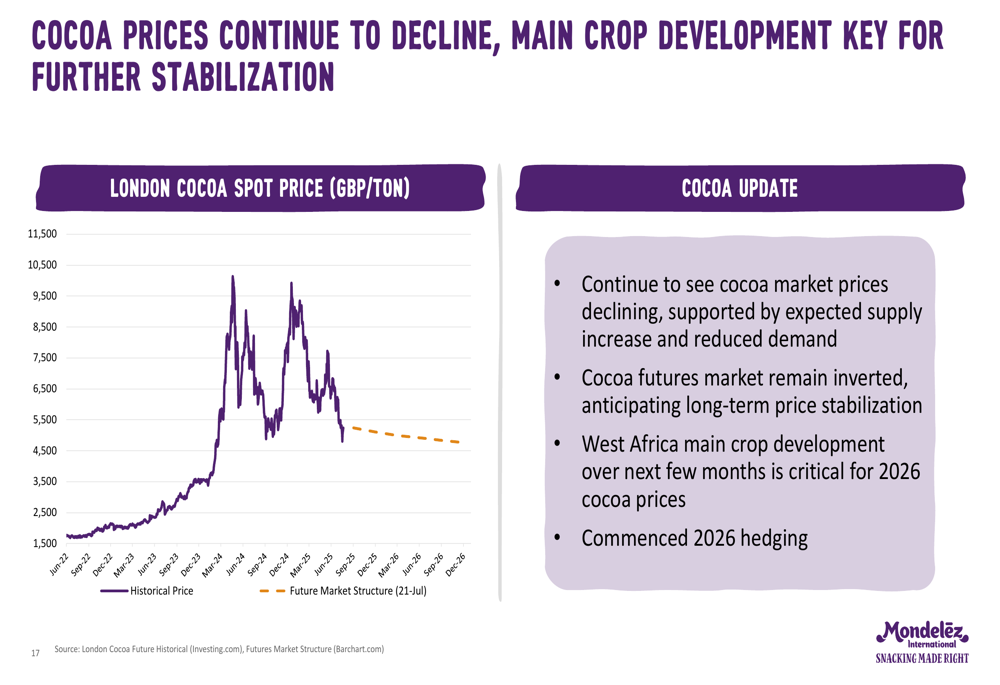

However, there appears to be light at the end of the tunnel regarding cocoa prices. The company’s presentation included a chart showing recent declines in cocoa spot prices, with expectations for further moderation supported by anticipated supply increases and reduced demand:

Regional and Category Performance

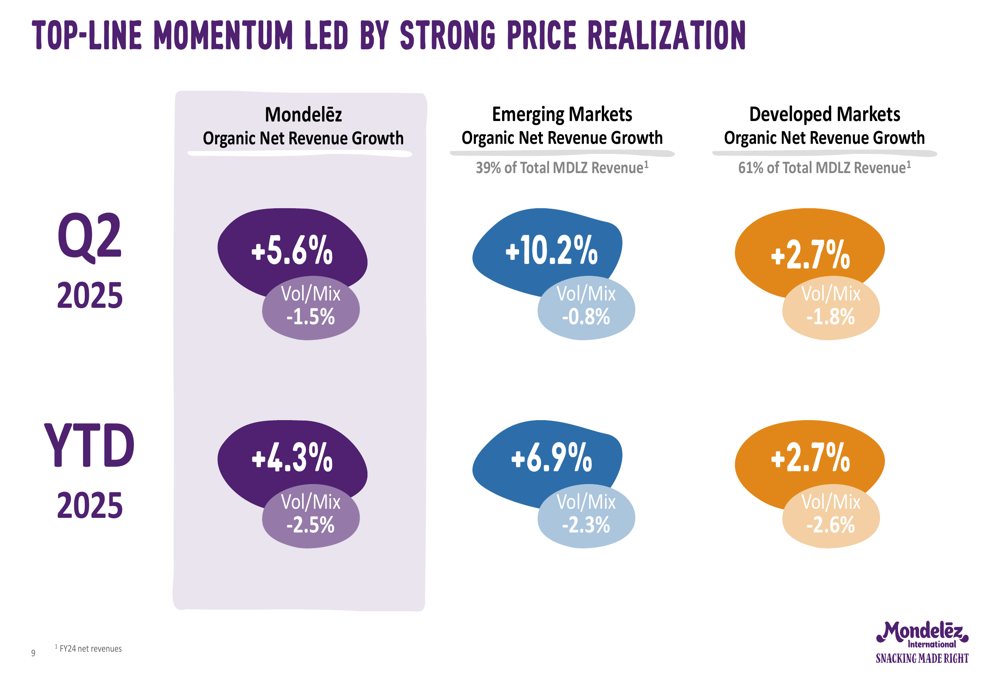

Mondelez’s performance varied significantly across regions and product categories. Emerging markets led growth with a 10.2% increase in Q2, substantially outpacing developed markets at 2.7%. This represents a significant improvement from Q1, particularly in emerging markets which grew at 3.9% in the first quarter.

The regional breakdown of organic net revenue growth is illustrated here:

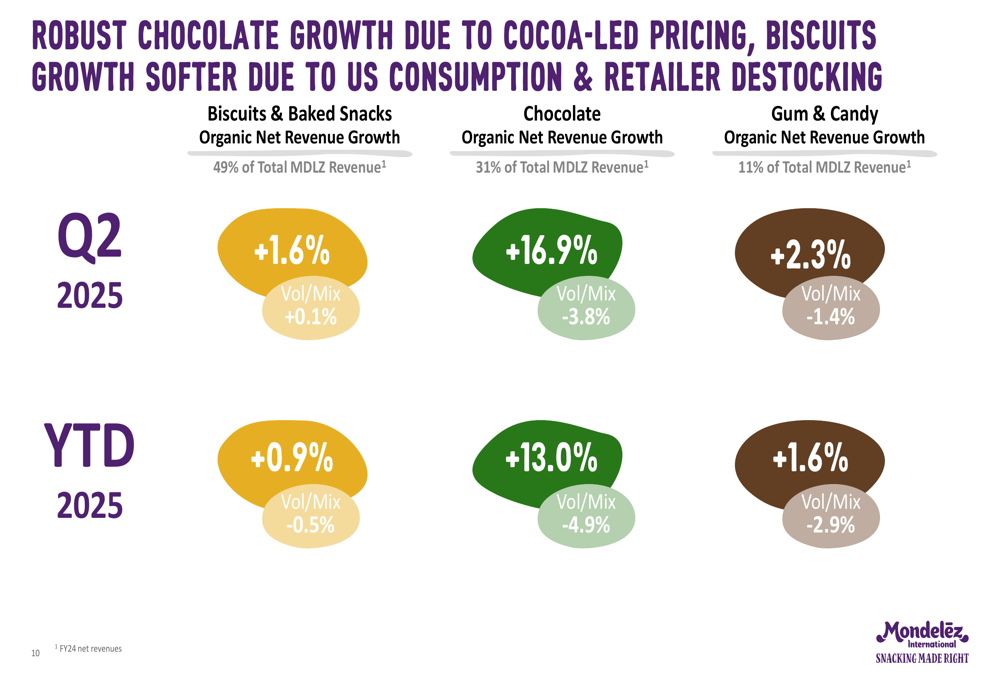

Among product categories, chocolate was the standout performer with 16.9% growth in Q2 and 13.0% year-to-date, significantly accelerating from the 10.1% growth reported in Q1. Biscuits and baked snacks showed more modest growth at 1.6% for Q2 and 0.9% year-to-date, while gum and candy grew 2.3% in Q2 and 1.6% year-to-date.

The following chart shows the category performance:

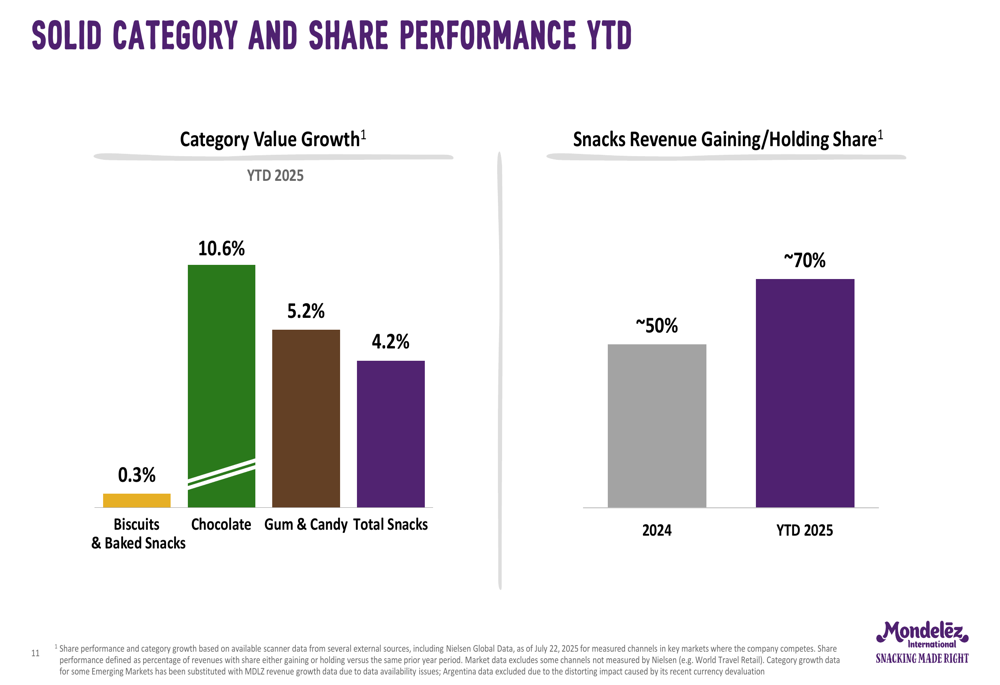

Mondelez has been successful in maintaining or gaining market share across its portfolio, with approximately 70% of its revenue coming from categories where it is gaining or holding share year-to-date 2025, up from about 50% in 2024:

Forward-Looking Statements

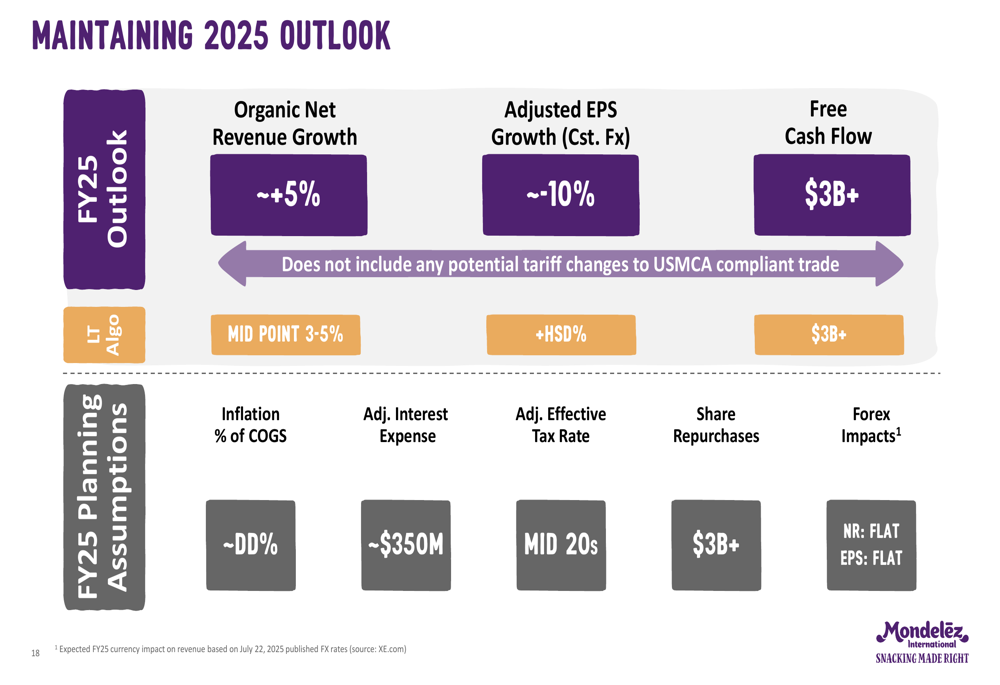

Despite the significant challenges from cocoa input costs, Mondelez maintained its 2025 outlook, projecting organic net revenue growth of approximately 5%, adjusted EPS decline of approximately 10%, and free cash flow of over $3 billion.

The company’s outlook summary is presented here:

Looking ahead to 2026, Mondelez indicated plans to increase investments, primarily in working media, while continuing to execute its long-term strategy. The company remains confident in the long-term growth potential of the snacking category, citing headroom for growth through distribution expansion and penetration into new categories.

Management noted that the current outlook does not include any potential impacts from tariff changes to USMCA-compliant trade, indicating some uncertainty regarding future trade policies that could affect the business.

As cocoa prices continue to moderate from their record highs, Mondelez appears positioned to gradually recover its profit margins while maintaining its top-line momentum through the remainder of 2025 and into 2026.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.