Sana Biotechnology stock higher after Eric Jackson touts 100-bagger potential

Introduction & Market Context

Montauk Renewables Inc. (NASDAQ:MNTK) presented its first quarter 2025 financial results on May 9, revealing a mixed performance characterized by revenue growth but declining profitability. The renewable energy company continues to navigate challenging market conditions, particularly regarding environmental attribute pricing, while advancing several development projects aimed at future growth.

The company’s stock has shown volatility in recent trading, with a 4.02% gain in its last session closing at $2.33, though premarket trading indicated a 1.29% decline. This follows a significant drop after the company’s Q4 2024 earnings release, when the stock fell nearly 5% after missing both EPS and revenue forecasts.

Quarterly Performance Highlights

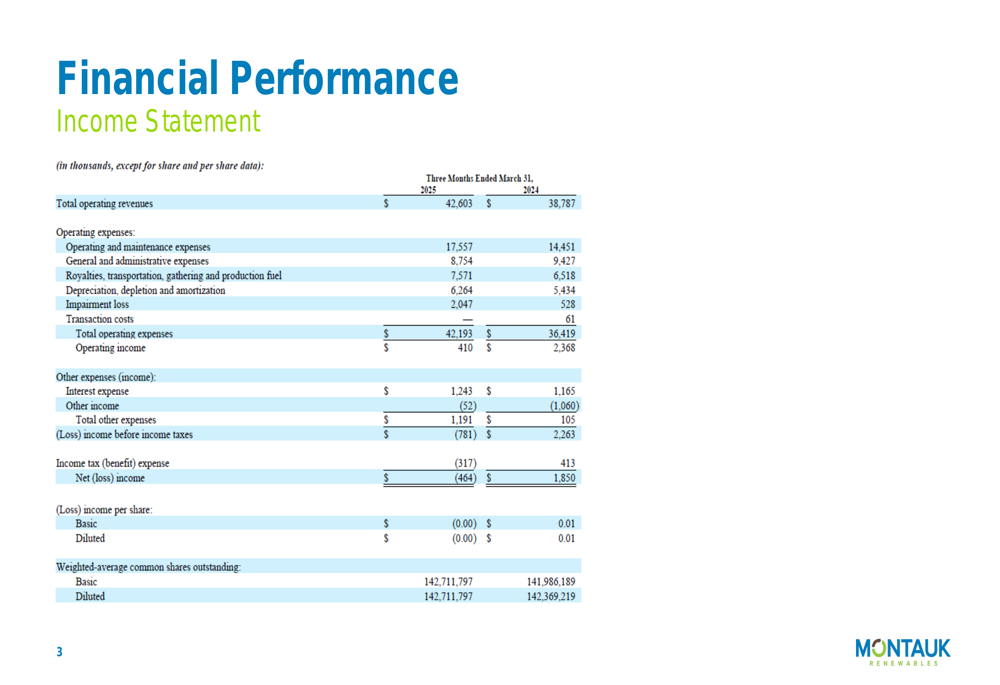

Montauk reported total operating revenues of $42.6 million for Q1 2025, representing a 9.8% increase from $38.8 million in the same period last year. However, this revenue growth was overshadowed by a substantial decline in profitability, with operating income falling 82.7% to $410,000 compared to $2.37 million in Q1 2024.

The company recorded a net loss of $464,000 for the quarter, a significant reversal from the $1.85 million net income reported in the prior-year period. This resulted in a loss per share of less than $0.01, compared to earnings per share of $0.01 in Q1 2024.

As shown in the following income statement summary:

The decline in profitability occurred despite the revenue increase, primarily due to a 15.9% rise in operating expenses, which reached $42.2 million. This increase was driven by higher RNG operating expenses ($21.2 million, up 16.9%) and increased REG operating expenses.

Detailed Financial Analysis

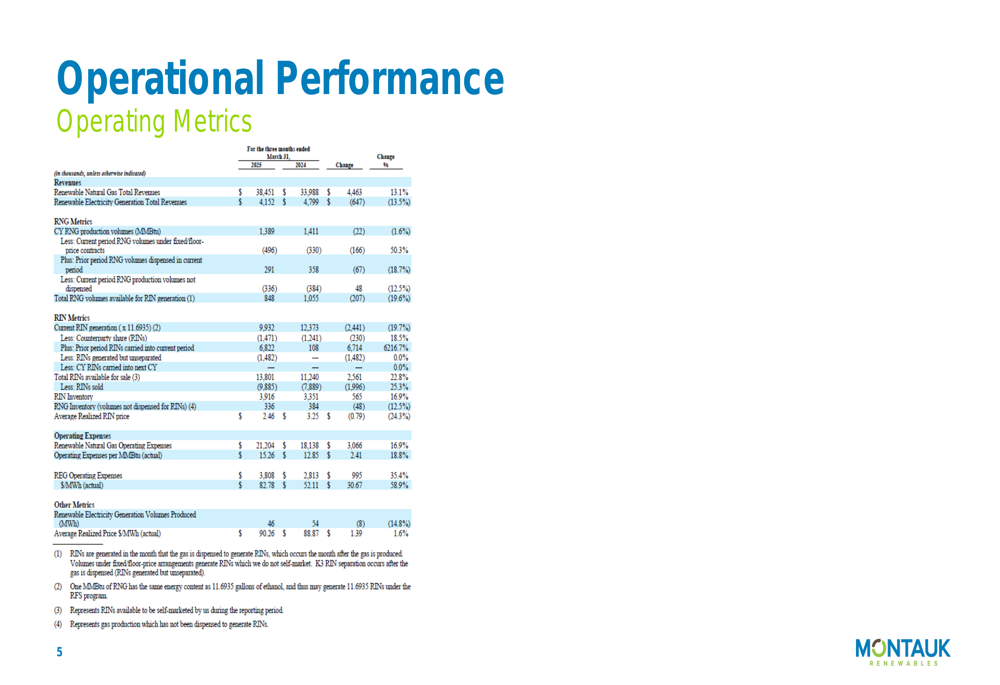

A closer examination of Montauk’s operational metrics reveals the underlying factors affecting performance. The company’s renewable natural gas (RNG) segment, which accounts for approximately 90% of total revenue, saw a 13.1% revenue increase to $38.5 million despite a 1.6% decrease in production volumes.

This revenue growth in the face of lower production was driven by an increase in RIN (Renewable Identification Number) volumes available for sale, which rose 22.8% to 13,801. However, the average realized RIN price declined significantly by 24.3% to $2.46 from $3.25 in the prior year, partially offsetting the volume benefits.

The following operational performance metrics provide a comprehensive view of the company’s results:

Montauk’s renewable electricity generation (REG) segment experienced a 13.5% revenue decline to $4.15 million, primarily due to a 14.8% decrease in production volumes to 46 MWh. This was partially offset by a modest 1.6% increase in the average realized price to $90.26 per MWh.

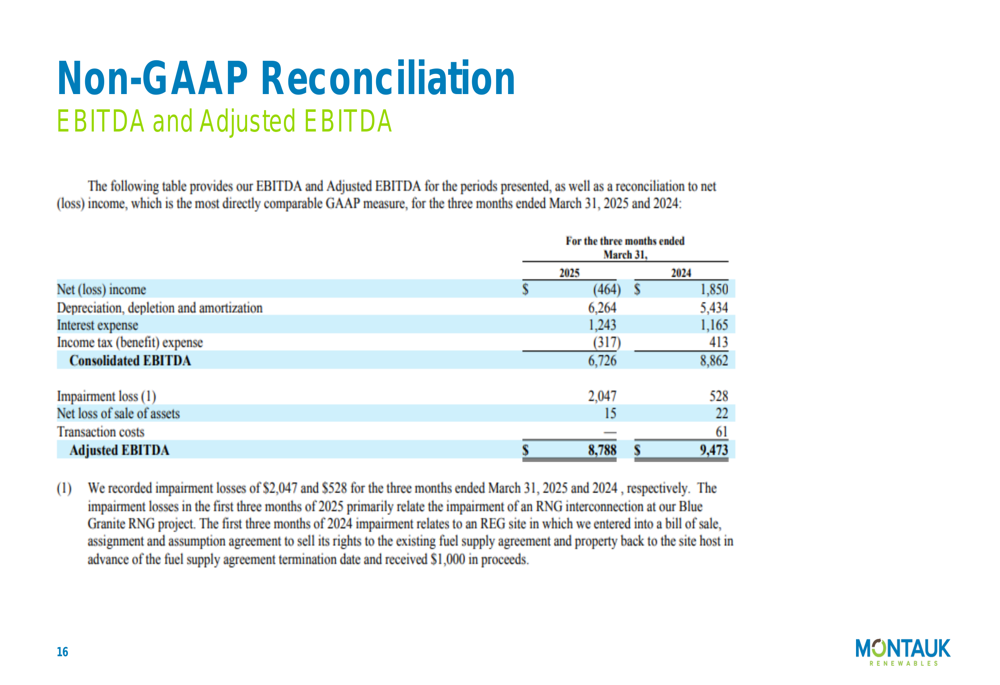

The company’s adjusted EBITDA, a key non-GAAP metric, decreased by 7.2% to $8.79 million compared to $9.47 million in Q1 2024. This decline was less severe than the drop in operating income, largely due to the impact of a $2.05 million impairment loss related to the Blue Granite RNG facility.

The reconciliation of net income to adjusted EBITDA is shown below:

Strategic Initiatives & Development Pipeline

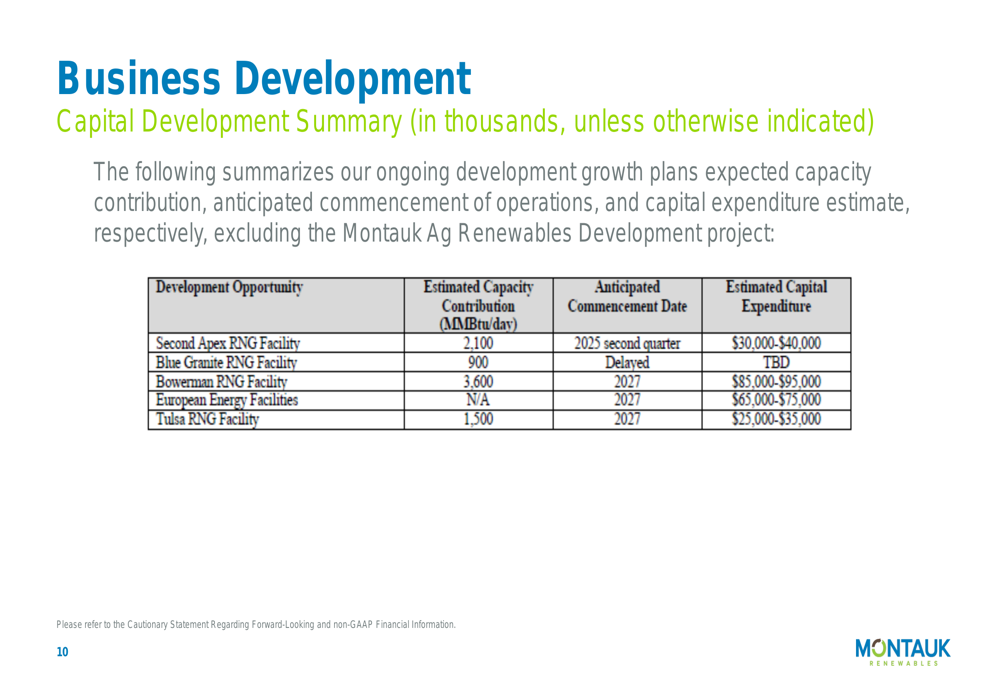

Montauk continues to advance several development projects aimed at expanding its production capacity and diversifying its revenue streams. The company’s second Apex RNG facility is expected to be commissioned in the second quarter of 2025, with an estimated capacity of 2,100 MMBtu per day and capital expenditure of $30-40 million.

However, the company faces challenges with its Blue Granite RNG facility, as the utility has provided notice that it will no longer accept RNG into its distribution system, despite previously providing a letter of intent. This has resulted in an impairment of RNG equipment related to design capital expenditures.

The company’s capital development summary outlines several ongoing and planned projects:

Montauk is also pursuing alternative fuel source development initiatives, including a biogenic carbon dioxide beneficial use project and waste-stream biogas recovery. The company has signed a 15-year contract with European Energy North America to deliver 140 tons of CO2 from its Texas facilities, with commissioning expected in 2027.

Additionally, the company is collaborating with Emvolon to transform waste stream biogas into carbon-negative fuel, with a proof-of-concept installation at its Atascocita facility in Houston designed to produce green methanol at commercial scale.

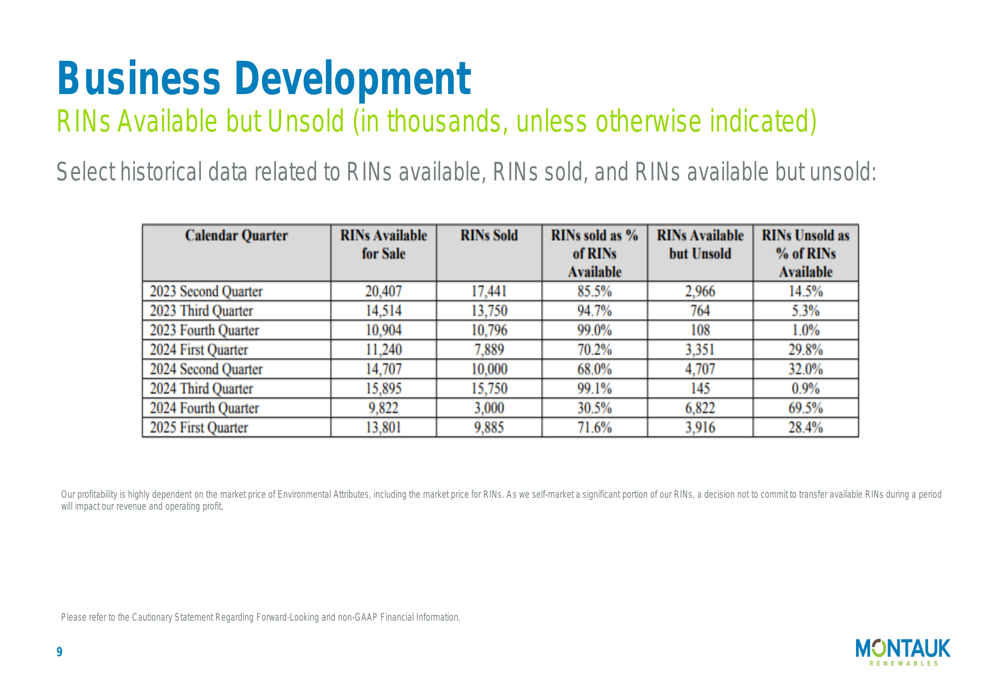

RIN Market Dynamics

A critical factor affecting Montauk’s financial performance is the market for Renewable Identification Numbers (RINs), which are tradable credits used for compliance with the EPA’s Renewable Fuel Standard program. The company’s profitability is highly dependent on the market price of these environmental attributes.

New EPA BRRR (Biogas Regulatory Relief Rule) rules requiring RIN separation have deferred RIN generation by approximately one month, affecting the timing of revenue recognition. As of Q1 2025, approximately 1,482 RINs were generated but unseparated related to 2025 RNG production, with 3,916 RINs in inventory.

The following table shows the historical trend of RINs available for sale, sold, and unsold:

In Q1 2025, Montauk sold 71.6% of available RINs, leaving 28.4% unsold. This is slightly better than Q1 2024, when the company sold 70.2% of available RINs, but remains below the sell-through rates achieved in most quarters of 2023.

Forward-Looking Statements

Looking ahead, Montauk continues to focus on expanding its production capacity through several development projects. The second Apex RNG facility is expected to be completed in Q2 2025, while the Tulsa REG conversion to RNG and Rumpke relocation projects are advancing with long-lead capital expenditures expected to begin in Q2 2025.

The company faces ongoing challenges with RIN pricing and regulatory changes, which may continue to impact profitability in the near term. However, its diversification efforts into alternative fuel sources and expansion of production capacity aim to strengthen its market position over the longer term.

Cash flow from operations decreased to $9.14 million in Q1 2025 from $14.29 million in Q1 2024, while investing activities used $11.63 million, down from $22.79 million in the prior year. This reflects the company’s continued investment in growth projects, albeit at a somewhat reduced pace compared to the previous year.

With cash and cash equivalents of $40.49 million at the end of Q1 2025 (down from $63.73 million a year earlier), Montauk maintains financial flexibility to pursue its development pipeline, though careful capital allocation will be crucial given the challenging market environment and recent profitability pressures.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.