How are energy investors positioned?

Introduction & Market Context

Banca Monte dei Paschi di Siena (BMPS), Italy’s oldest bank, reported strong first-quarter results on May 9, 2025, showcasing resilient performance despite the challenging interest rate environment. The bank, which positions itself as "A Clear and Simple Commercial Bank, Revolving Around Customers," demonstrated solid growth across key metrics while maintaining strict cost discipline and improving asset quality.

Executive Summary

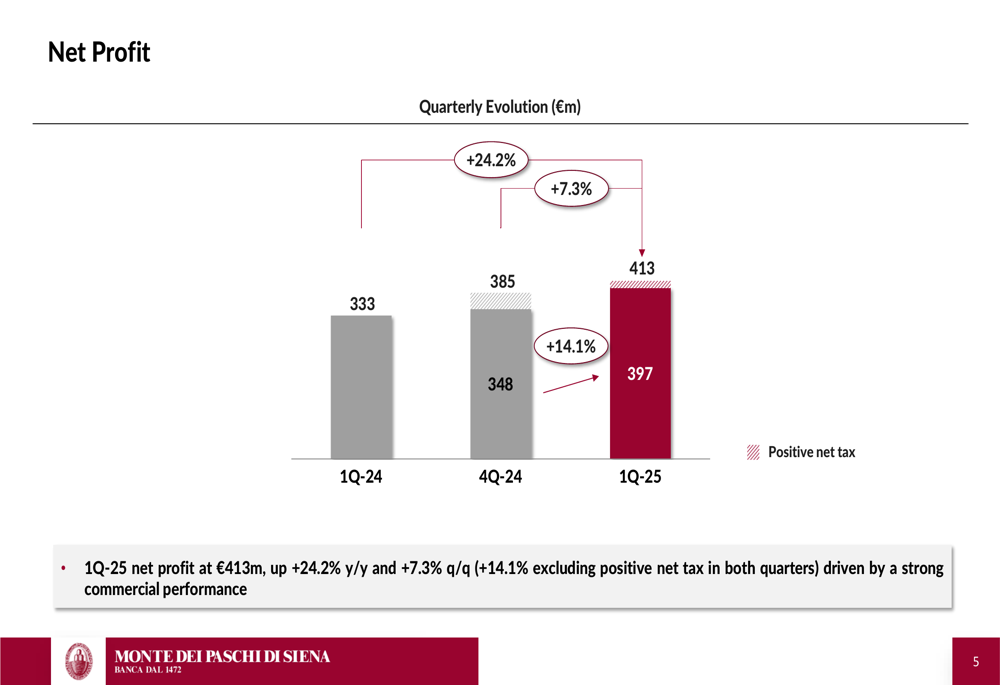

Monte dei Paschi reported a net profit of €413 million for Q1 2025, representing a substantial 24.2% increase year-over-year and a 7.3% rise quarter-over-quarter. When excluding positive net tax effects in both quarters, the profit growth was even more impressive at 14.1% quarter-over-quarter.

As shown in the following chart of quarterly net profit evolution, the bank has maintained consistent profit growth momentum:

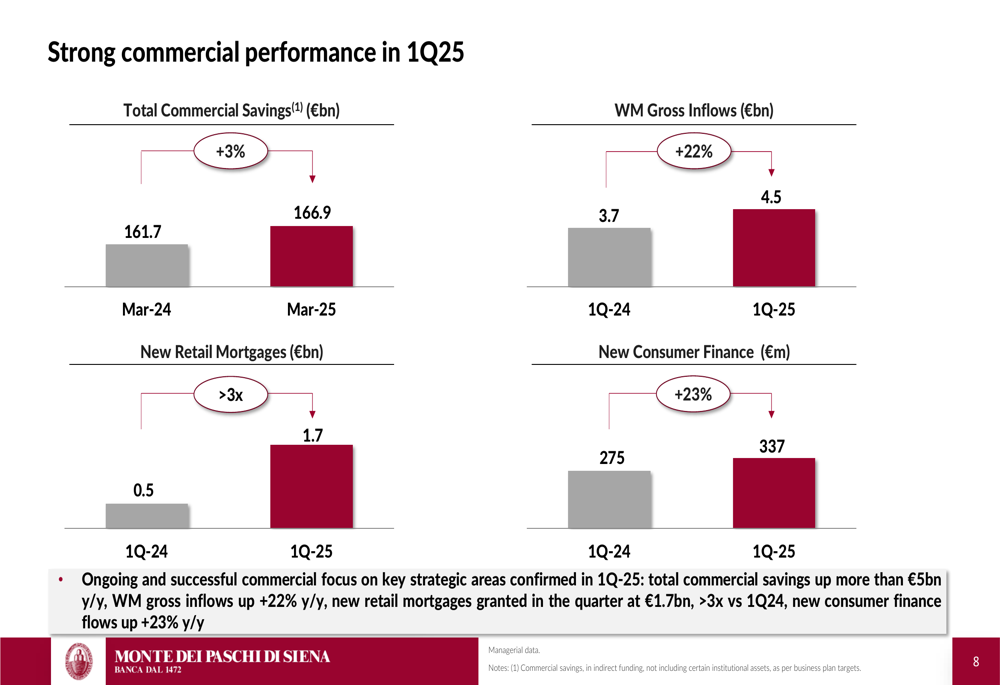

The bank’s performance was driven by strong commercial activity, with total commercial savings increasing by more than €5 billion year-over-year, wealth management gross inflows rising 22% year-over-year, and new retail mortgages granted in the quarter reaching €1.7 billion—more than triple the amount from Q1 2024.

This commercial momentum is clearly illustrated in the following performance metrics:

Quarterly Performance Highlights

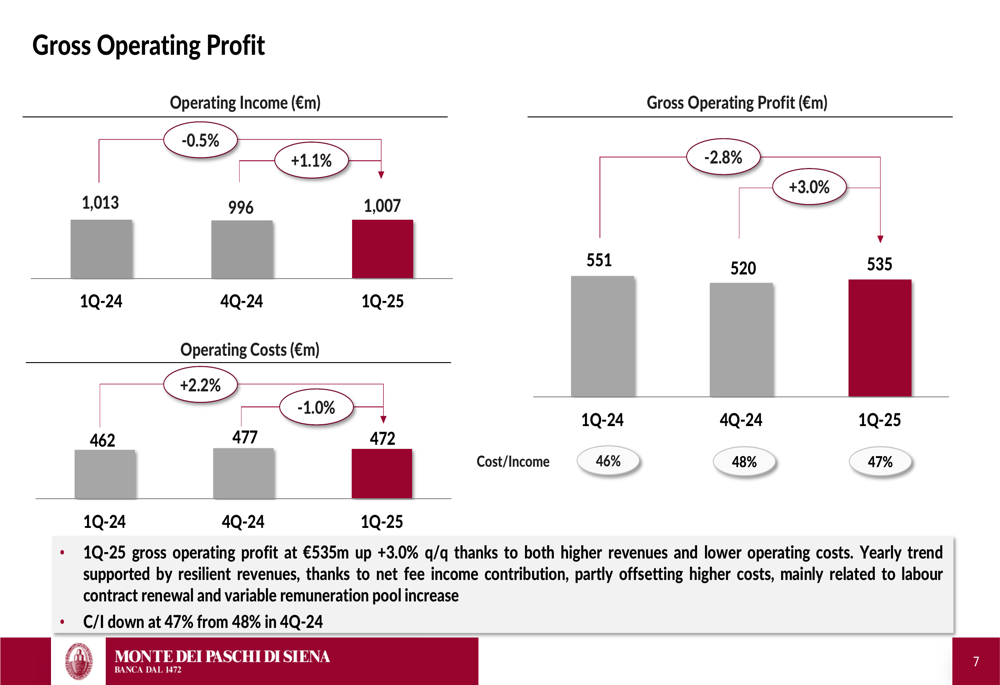

Monte dei Paschi’s gross operating profit reached €535 million in Q1 2025, up 3.0% quarter-over-quarter, benefiting from both higher revenues and lower operating costs. The cost-to-income ratio improved to 47% from 48% in the previous quarter.

The following chart breaks down the components of the gross operating profit:

Despite the challenging interest rate environment, the bank’s net operating profit increased to €448 million, up 0.8% year-over-year and 9.4% quarter-over-quarter. This growth was primarily driven by increased fee contributions, effective cost management, and reduced cost of risk.

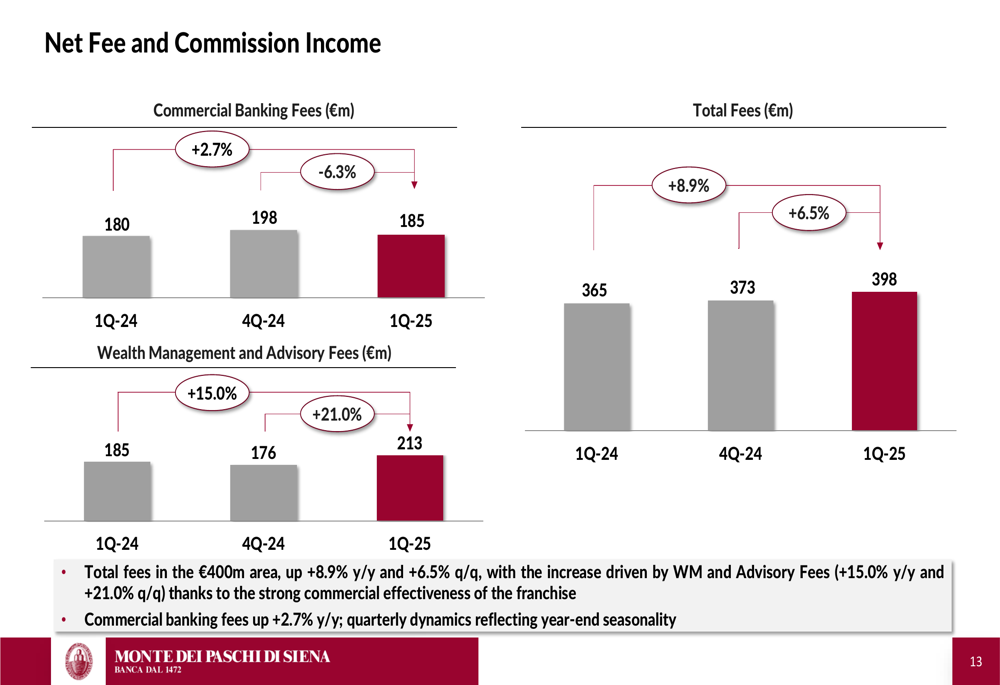

Net fee and commission income reached nearly €400 million, growing 8.9% year-over-year and 6.5% quarter-over-quarter. This increase was largely driven by wealth management and advisory fees, which surged 15.0% year-over-year and 21.0% quarter-over-quarter, highlighting the strong commercial effectiveness of the bank’s franchise.

The following chart illustrates the growth in fee income:

Detailed Financial Analysis

Net interest income declined to €543 million, down 7.5% year-over-year and 7.7% quarter-over-quarter, reflecting the impact of declining interest rates. The lending rate decreased to 3.75% from 4.46% a year earlier, while the funding rate fell to 0.87% from 1.16%, resulting in a compressed spread of 2.89% compared to 3.30% in Q1 2024.

Operating costs were well-controlled at €472 million, down 1.0% quarter-over-quarter despite a 2.2% year-over-year increase. The yearly increase was primarily due to the effects of labor contract renewal, partially offset by lower non-HR costs, which decreased 4.2% year-over-year and 9.0% quarter-over-quarter.

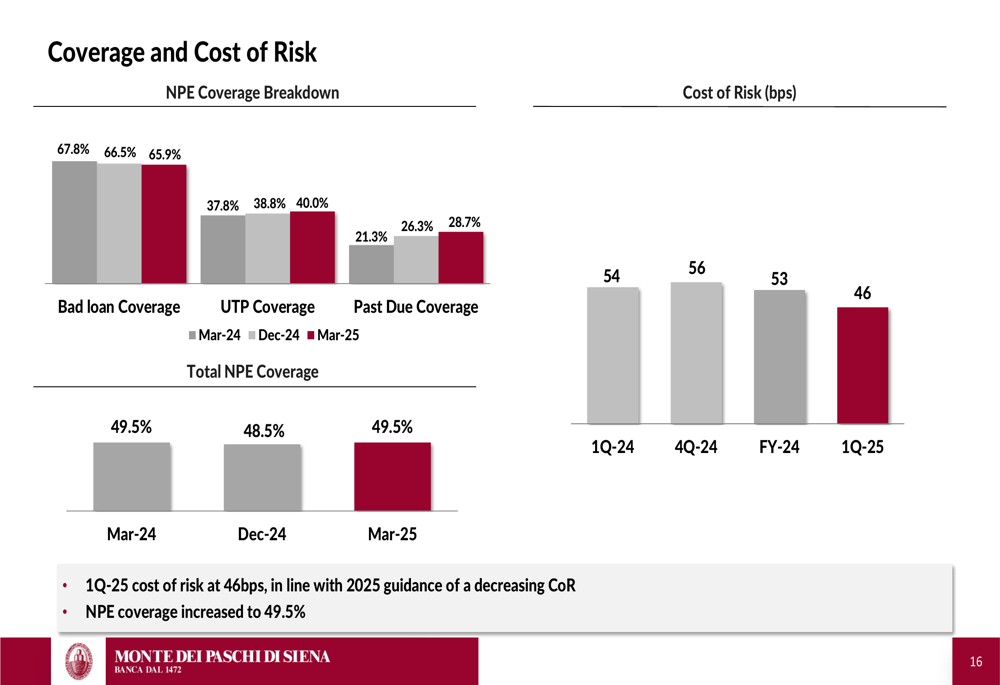

Asset quality continued to improve, with the gross NPE (non-performing exposure) ratio decreasing to 4.4% and the net NPE ratio falling to 2.3%. The NPE coverage ratio stood at a solid 49.5%, while the cost of risk declined to 46 basis points, in line with the bank’s 2025 guidance of a decreasing cost of risk.

The following chart provides a detailed breakdown of the bank’s NPE coverage and cost of risk:

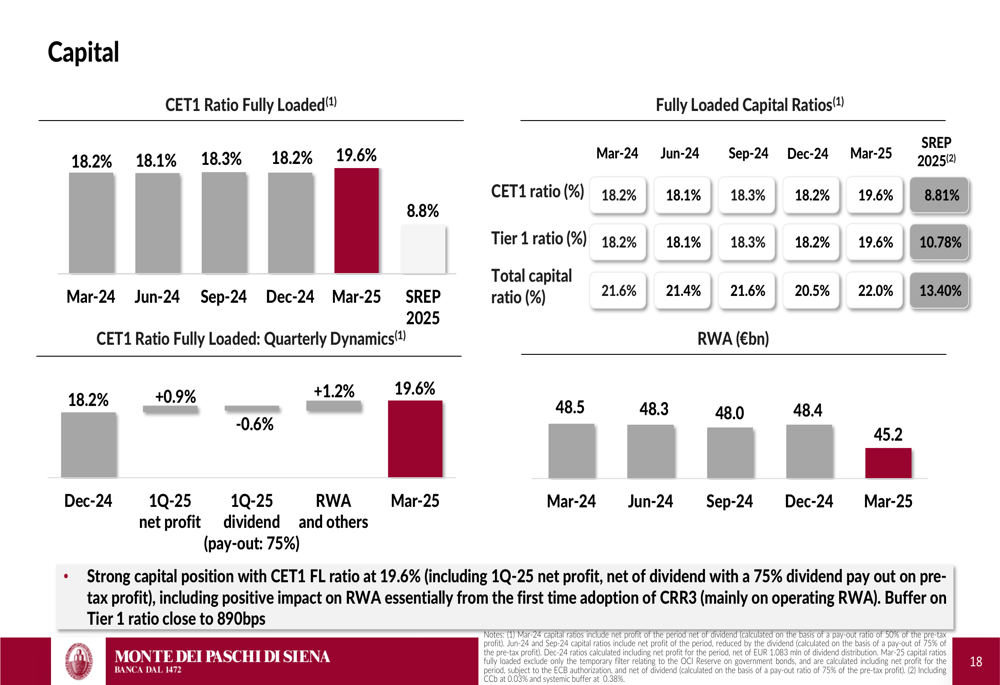

Monte dei Paschi maintained a strong capital position, with a CET1 fully loaded ratio of 19.6%, up from 18.2% a year earlier. This increase includes the positive impact on risk-weighted assets from the first-time adoption of CRR3 (Capital Requirements Regulation). The bank’s buffer on Tier 1 ratio is close to 890 basis points, positioning it at the top of the Italian banking sector in terms of capital strength.

The following chart illustrates the bank’s strong capital position:

Liquidity metrics remained robust, with the Liquidity Coverage Ratio (LCR) at 156% and the Net Stable Funding Ratio (NSFR) at 130%. The bank’s unencumbered counterbalancing capacity stood at €32 billion, while its reliance on ECB funding decreased to 6% of total liabilities, down from 9% in Q1 2024.

Strategic Initiatives & Outlook

Monte dei Paschi provided an update on the Mediobanca (OTC:MDIBY) Exchange Offer, noting that the process is on track with key milestones, including capital increase approval. The bank described the offer as an "unparalleled financial proposition" with benefits including pre-tax synergies and double-digit accretion. Supervisory and antitrust authorizations are expected in June/July 2025, followed by the approval of the Exchange Offer Document and the commencement of the Exchange Offer period.

Looking ahead, Monte dei Paschi expects its 2025 profit before tax to be higher year-over-year, with further room for growth in 2026. The bank’s strong commercial momentum, improving asset quality, and solid capital position provide a foundation for continued growth despite the challenging interest rate environment.

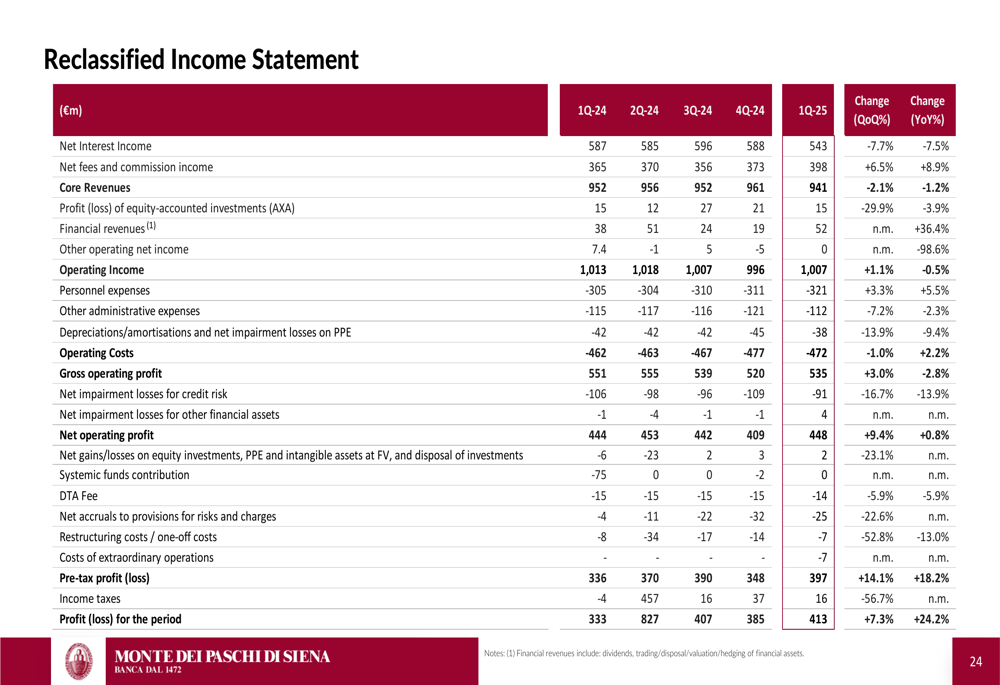

The comprehensive income statement below provides additional details on the bank’s financial performance:

Monte dei Paschi’s Q1 2025 results demonstrate the bank’s ability to navigate a declining interest rate environment through diversified revenue streams, strong commercial activity, and disciplined cost management. With its solid capital position and improving asset quality, the bank appears well-positioned to deliver on its growth expectations for 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.