Trump to impose 100% tariff on China starting November 1

Montrose Environmental Group (NYSE:MEG) shares surged over 30% in premarket trading after the company’s Q2 2025 earnings presentation revealed exceptional financial performance, with triple-digit profit growth and significantly raised full-year guidance.

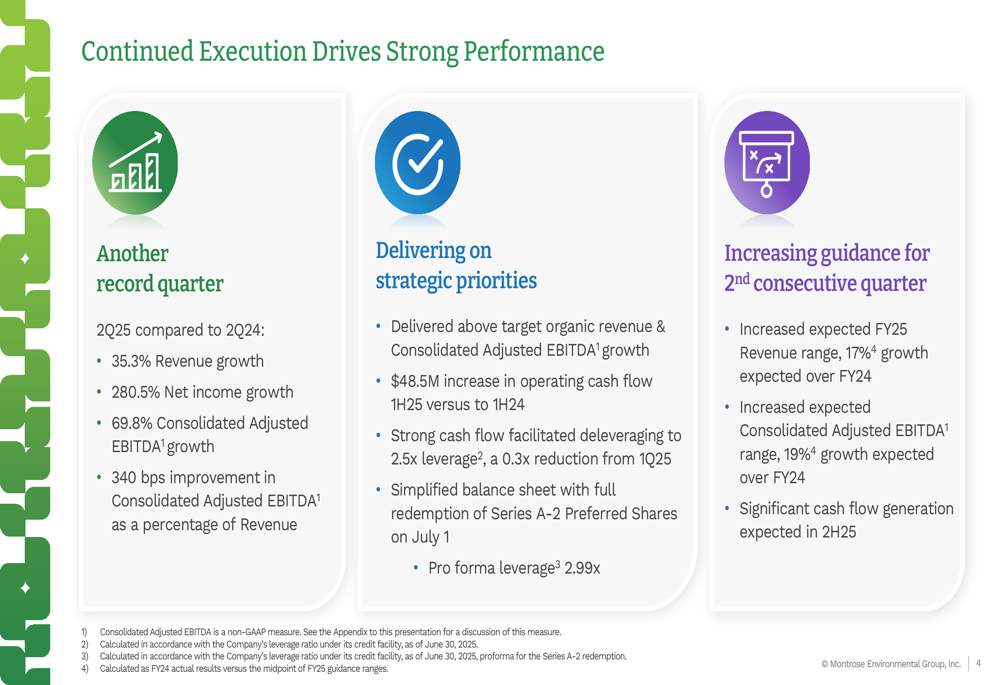

Quarterly Performance Highlights

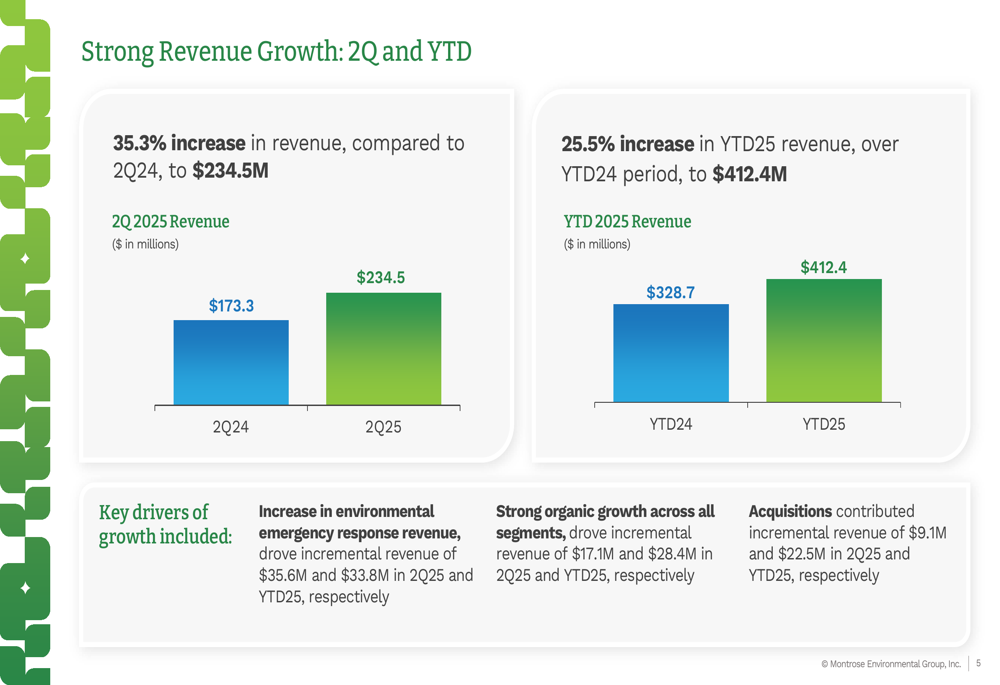

Montrose Environmental delivered what it called "another record quarter" with substantial growth across all key financial metrics. The company reported Q2 2025 revenue of $234.5 million, representing a 35.3% increase compared to the same period last year.

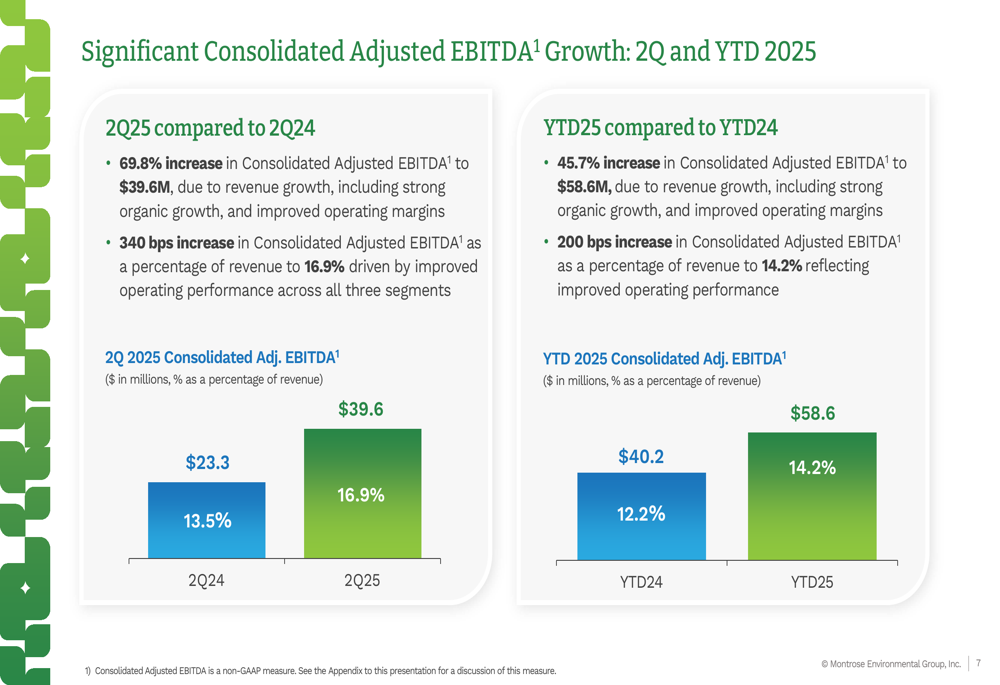

Most notably, Montrose achieved a dramatic 280.5% increase in net income, alongside a 69.8% jump in consolidated adjusted EBITDA to $39.6 million. The company also improved its consolidated adjusted EBITDA margin by 340 basis points to 16.9% of revenue.

As shown in the following performance summary:

"We’re delivering on our strategic priorities with above-target organic revenue and consolidated adjusted EBITDA growth," the company stated in its presentation, highlighting a $48.5 million increase in operating cash flow for the first half of 2025 compared to the same period in 2024.

Detailed Financial Analysis

The company’s revenue growth was driven by multiple factors, including a significant increase in environmental emergency response revenue, which contributed an incremental $35.6 million in Q2 2025. Strong organic growth across all segments added $17.1 million, while acquisitions contributed an additional $9.1 million.

The revenue breakdown is illustrated in the following chart:

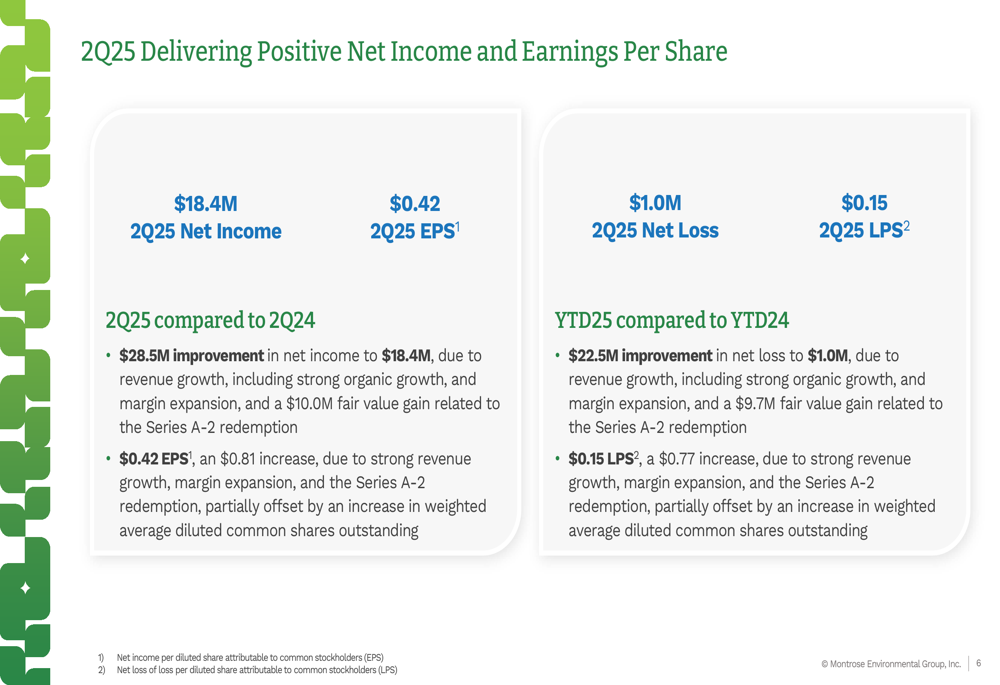

Montrose reported Q2 2025 net income of $18.4 million, translating to earnings per share of $0.42. This represents a substantial improvement from previous periods and demonstrates the company’s progress toward sustainable profitability.

The company’s consolidated adjusted EBITDA showed remarkable growth, both in absolute terms and as a percentage of revenue:

By segment, the Assessment, Permitting & Response division saw the most dramatic growth, with revenue increasing to $103.9 million in Q2 2025 from $53.4 million in Q2 2024, driven largely by environmental emergency response services. The segment’s adjusted EBITDA margin improved to 26.5% from 23.6%.

The Measurement & Analysis segment also performed strongly, with revenue growing to $62.8 million from $54.8 million, while its adjusted EBITDA margin expanded significantly to 29.1% from 22.5%.

Strategic Initiatives

Montrose reported being six months ahead of its strategic financial plan, having redeemed its Series A-2 preferred stock early and achieving a leverage ratio of 2.5x, representing a 0.3x reduction from Q1 2025.

The company has temporarily de-emphasized acquisitions to focus on organic growth, which it expects to maintain at or above its 7-9% target range. In May 2025, Montrose announced its inaugural stock repurchase program of up to $40 million, reflecting confidence in its financial position and future prospects.

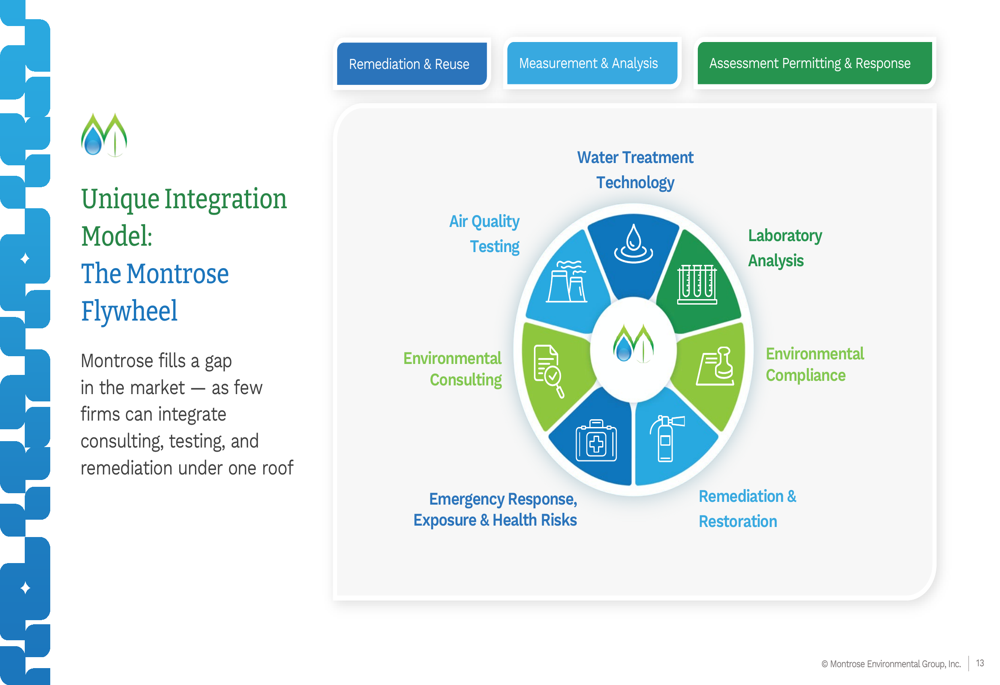

A key competitive advantage highlighted in the presentation is Montrose’s integrated business model, which the company refers to as "The Montrose Flywheel":

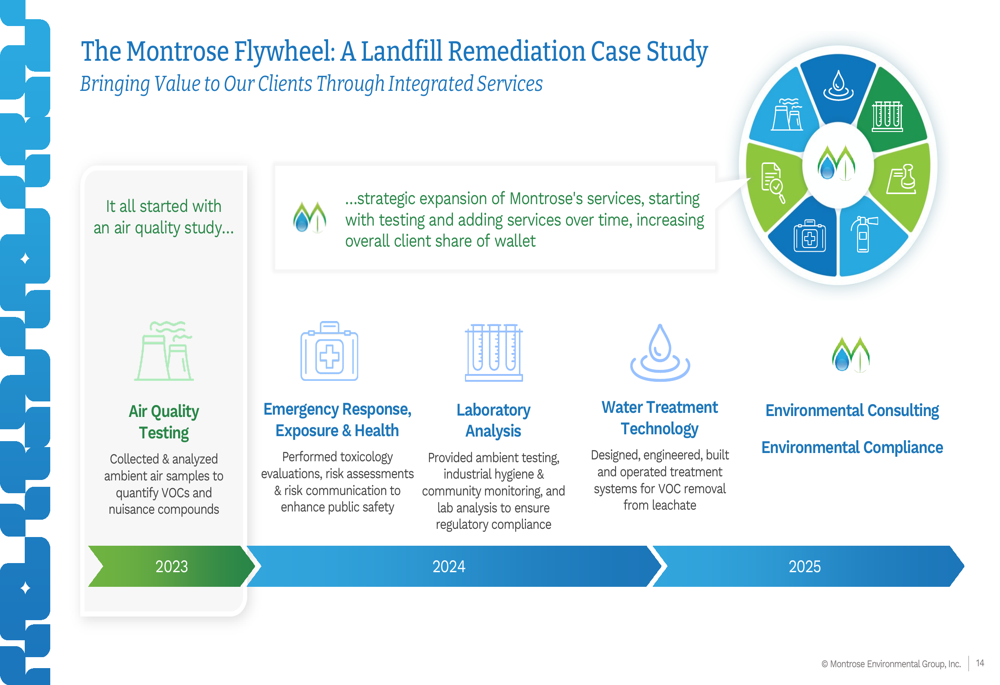

This integration allows Montrose to expand relationships with clients over time, as illustrated in a landfill remediation case study:

Forward-Looking Statements

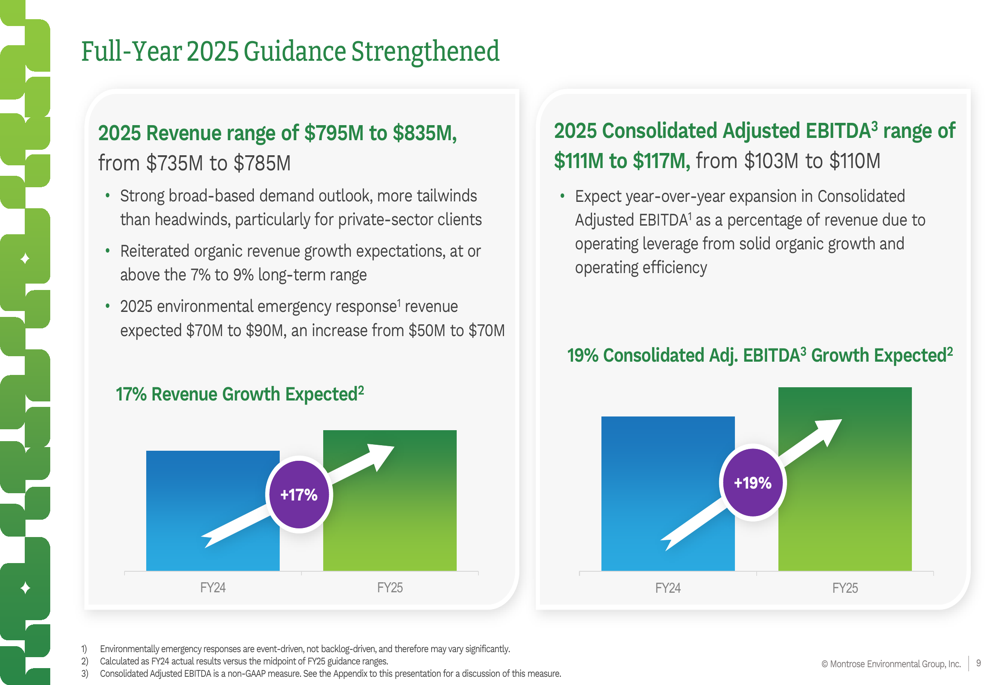

Based on its strong performance, Montrose has raised its full-year 2025 guidance for the second consecutive quarter. The company now expects revenue between $795 million and $835 million, up from the previous range of $735 million to $785 million, representing approximately 17% growth over fiscal year 2024.

Similarly, consolidated adjusted EBITDA guidance has been increased to a range of $111 million to $117 million, up from $103 million to $110 million, implying 19% growth over the previous year.

The company also raised its expectations for environmental emergency response revenue to between $70 million and $90 million for 2025, an increase from the previous guidance of $50 million to $70 million.

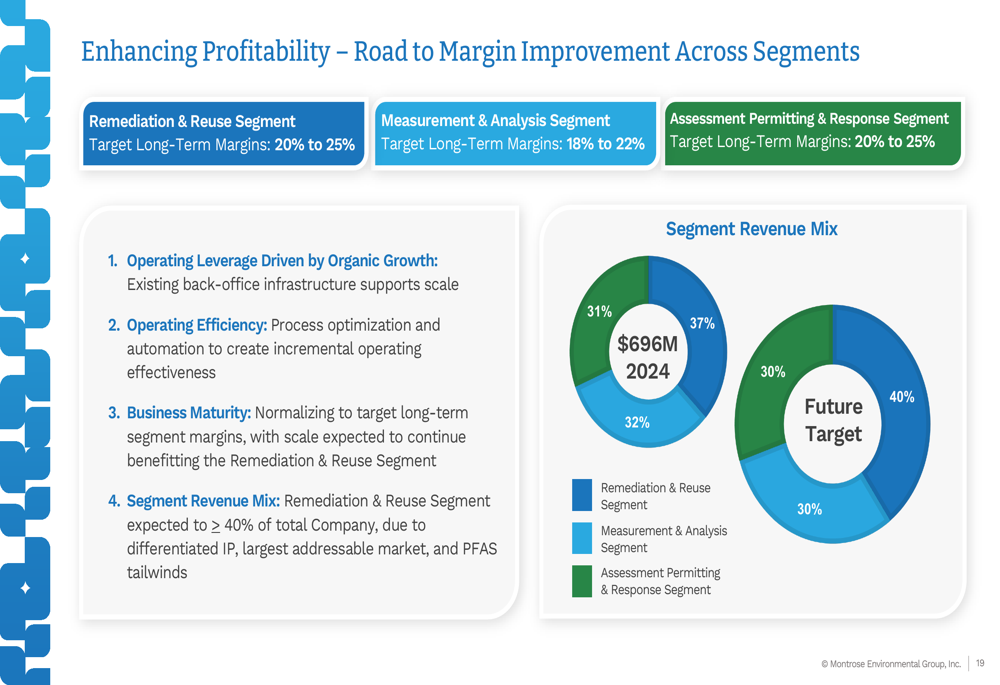

Looking further ahead, Montrose outlined its path to margin improvement, which includes leveraging organic growth, improving operating efficiency, and shifting its revenue mix toward higher-margin segments:

"We expect the Remediation & Reuse segment to grow to more than 40% of total company revenue in the future, up from 31% in 2024," the company noted, highlighting this as a key driver for future margin expansion.

The strong quarterly results and raised guidance appear to validate Montrose’s business strategy and position in the environmental services market. With shares up over 30% in premarket trading to $29.40, investors are clearly responding positively to the company’s exceptional performance and improved outlook for the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.