FTSE 100 today: Index flat at open, European markets mixed; pound weakens

Introduction & Market Context

Moody’s Corporation (NYSE:MCO) presented its second quarter 2025 earnings results on July 23, showing continued growth despite a challenging comparison to the prior year. The company’s stock was down 1.23% in premarket trading at $493, following a slight 0.21% decline the previous day, as investors digested the results against the backdrop of recent strong performance that has pushed the stock near its 52-week high of $531.93.

The Q2 results follow a particularly strong first quarter where Moody’s exceeded expectations with an EPS of $3.83 and 8% revenue growth. While Q2 showed some moderation in growth rates, the company demonstrated resilience in its core businesses and sufficient confidence to narrow its full-year guidance range upward.

Quarterly Performance Highlights

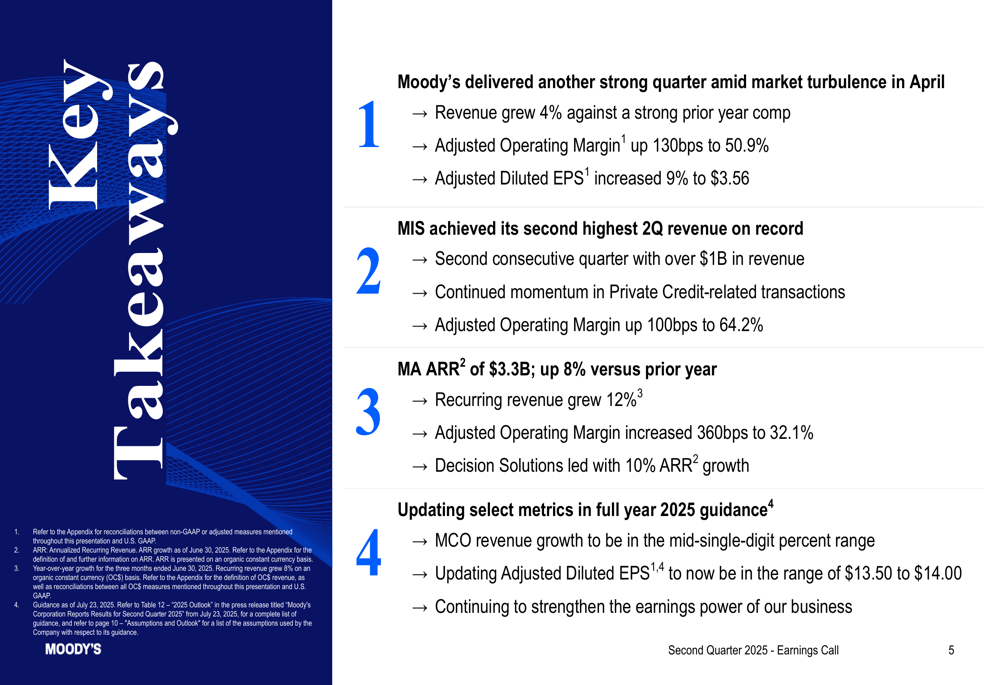

Moody’s delivered 4% revenue growth against a strong prior year comparison, with adjusted operating margin expanding 130 basis points to 50.9% and adjusted diluted EPS increasing 9% to $3.56.

As shown in the following comprehensive summary of quarterly results:

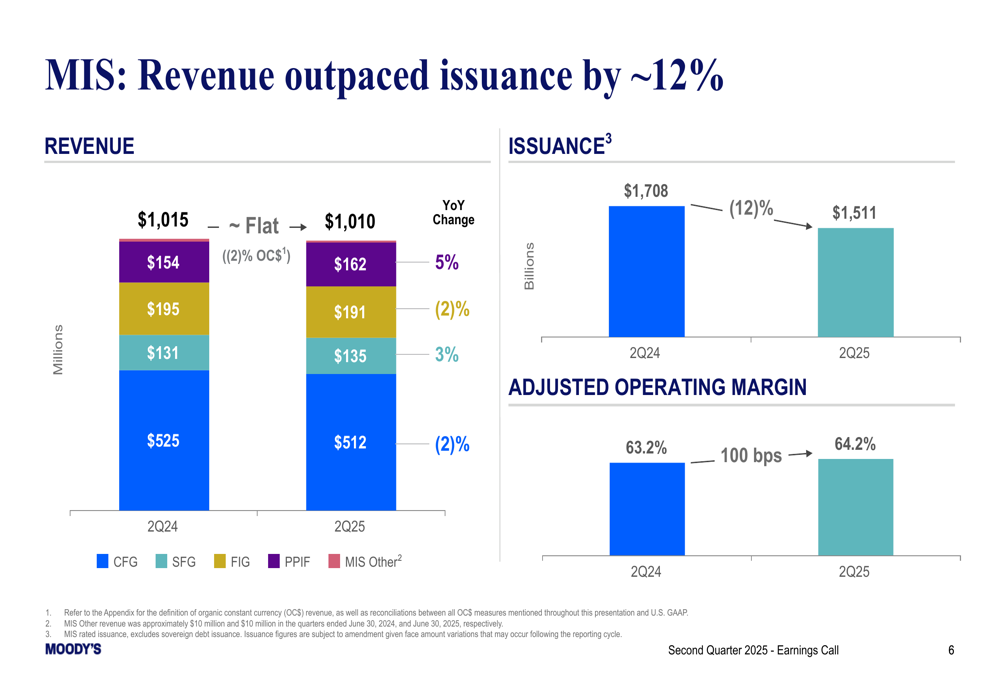

The company’s performance was driven by strength in both major segments. Moody’s Investors Service (MIS) achieved its second highest Q2 revenue on record with over $1 billion, marking the second consecutive quarter exceeding this threshold. Notably, MIS revenue remained resilient despite a 12% decrease in issuance volume, demonstrating the company’s pricing power and value proposition.

The following chart illustrates how MIS revenue outpaced issuance by approximately 12%:

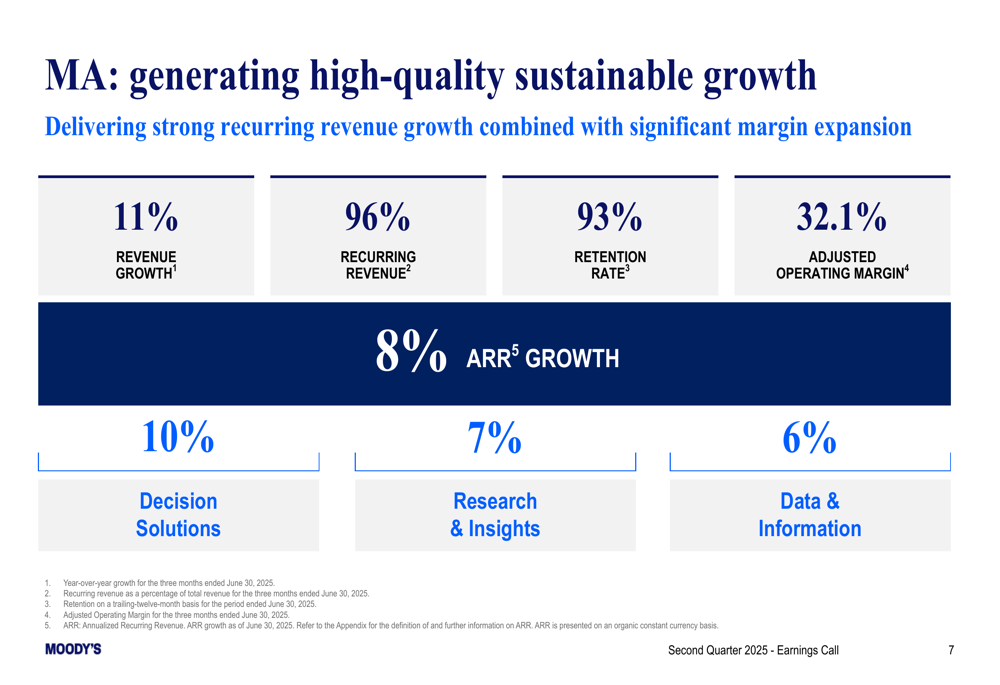

Meanwhile, Moody’s Analytics (MA) continued to demonstrate high-quality sustainable growth with annualized recurring revenue (ARR) of $3.3 billion, up 8% versus the prior year. The segment’s recurring revenue grew 12%, and its adjusted operating margin increased significantly by 360 basis points to 32.1%.

The stability of MA’s business model is highlighted in this performance summary:

Detailed Financial Analysis

Moody’s Analytics has established itself as a cornerstone of the company’s growth strategy, with 96% of its revenue being recurring and a strong retention rate of 93%. This provides significant visibility into future performance and reduces vulnerability to market fluctuations.

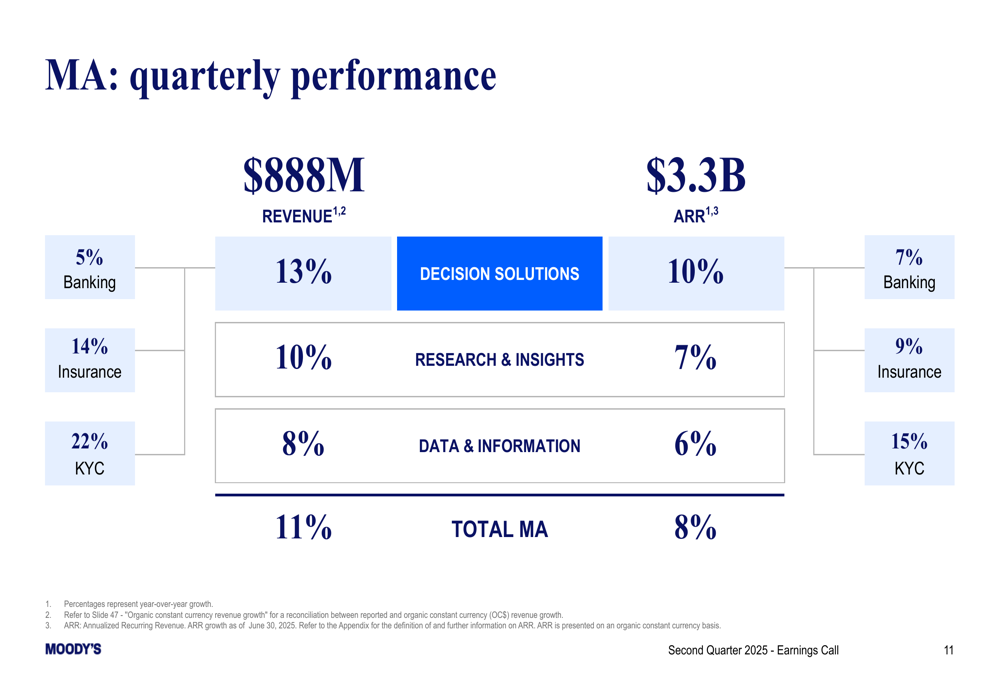

Within MA, Decision Solutions led growth with a 10% increase in ARR, followed by Research & Insights at 7% and Data & Information at 6%. The segment’s quarterly performance breakdown reveals the diverse revenue streams that contribute to its stability:

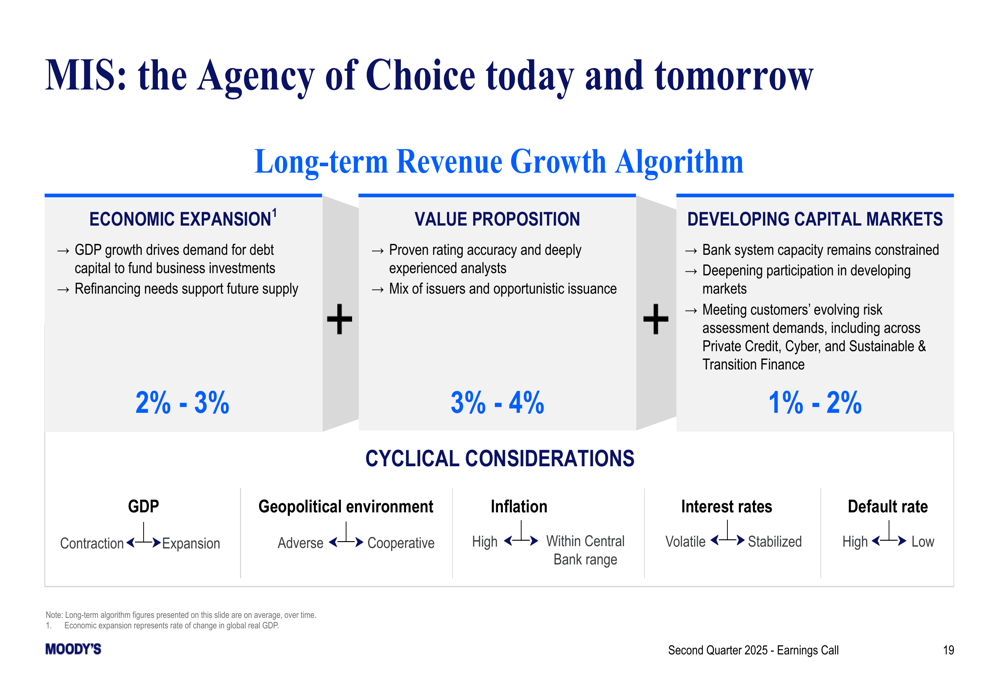

For Moody’s Investors Service, the company has developed a long-term revenue growth algorithm that targets 6-9% growth through economic expansion (2-3%), value proposition (3-4%), and developing capital markets (1-2%). This strategy positions MIS to continue growing even in challenging market environments.

The following chart details this growth algorithm:

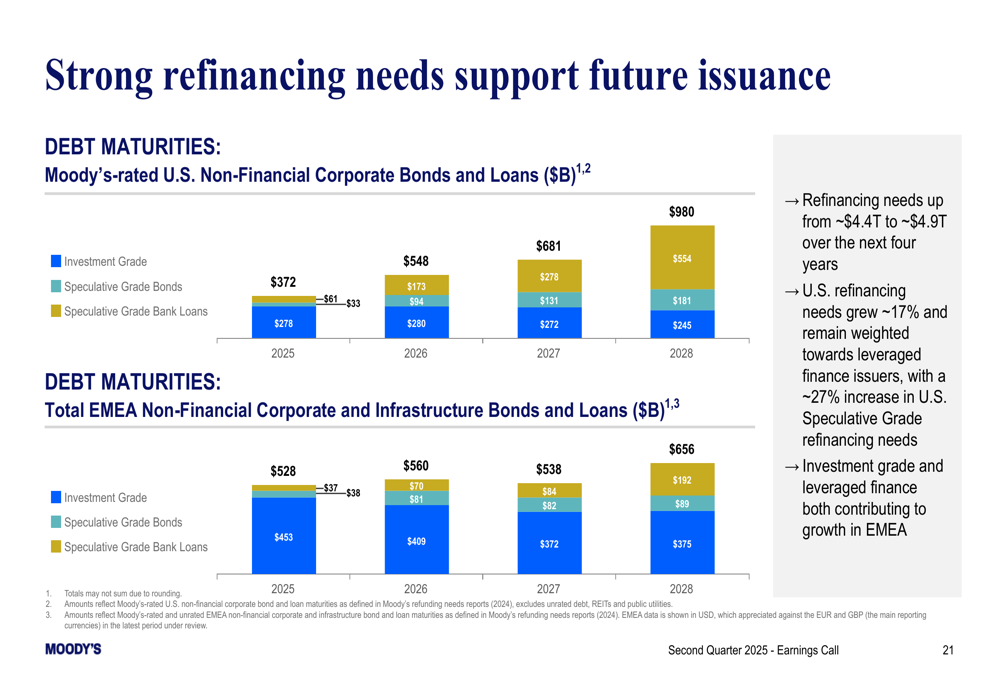

Looking ahead, Moody’s expects strong refinancing needs to support future issuance, with approximately $4.9 trillion of refinancing needs between 2025 and 2028. This provides a solid foundation for future revenue growth in the MIS segment.

As illustrated in this debt maturity schedule:

Strategic Initiatives

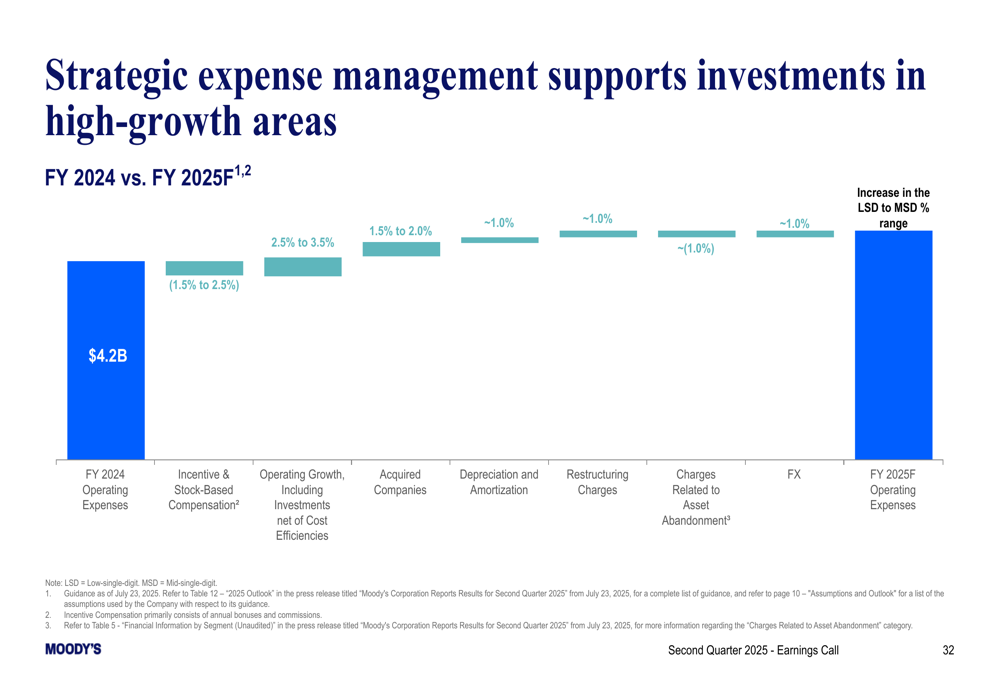

Moody’s is strategically managing expenses to support investments in high-growth areas while maintaining strong margins. The company expects operating expenses to increase in the low-to-mid-single-digit percent range for fiscal year 2025, balancing growth investments with cost efficiencies.

The following chart breaks down the company’s strategic expense management approach:

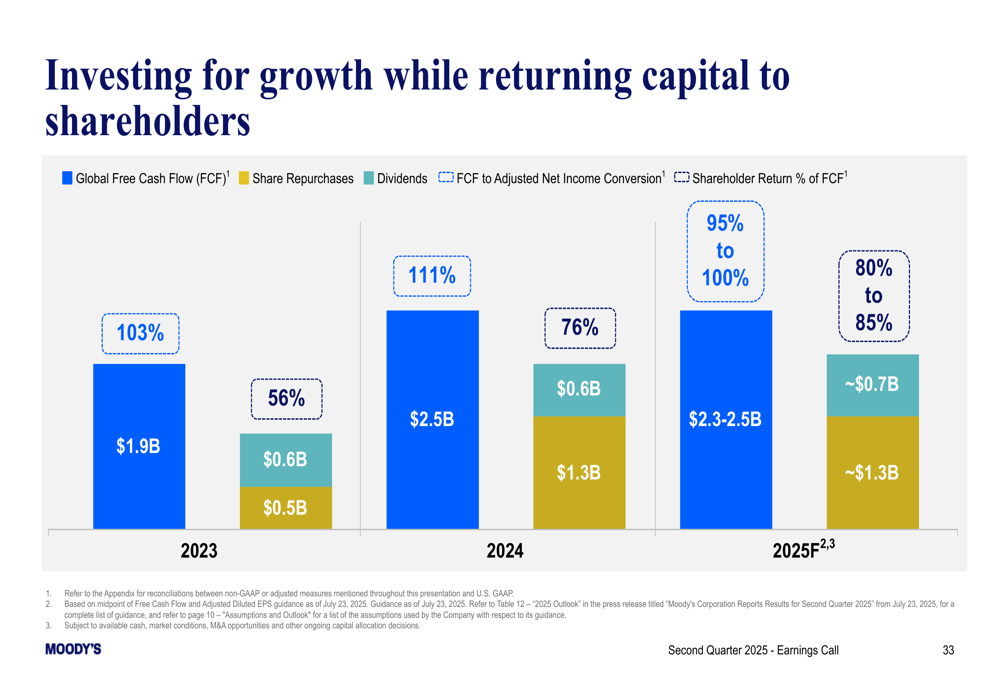

Capital allocation remains disciplined, with the company continuing to invest for growth while returning significant capital to shareholders. For 2025, Moody’s expects to generate free cash flow of $2.3-2.5 billion, with plans to repurchase at least $1.3 billion in shares and continue its dividend program.

The company’s approach to balancing growth investments with shareholder returns is illustrated here:

Forward-Looking Statements

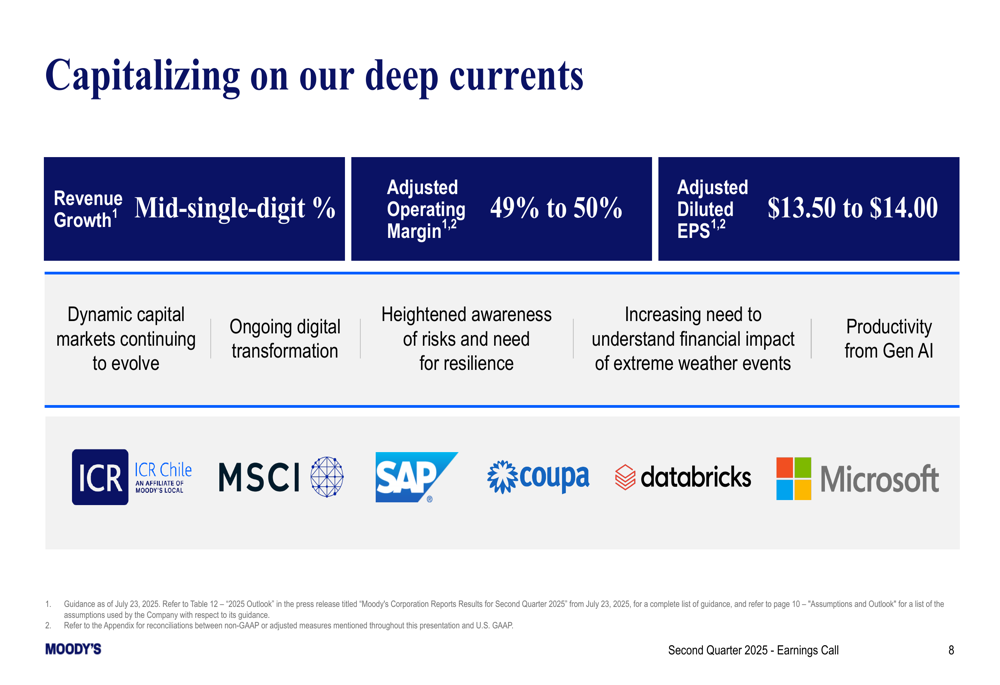

Based on its Q2 performance, Moody’s has updated select metrics in its full-year 2025 guidance. The company now expects revenue growth to be in the mid-single-digit percent range, with adjusted diluted EPS narrowed to $13.50-$14.00 from the previous range of $13.25-$14.00. This adjustment reflects increased confidence in the company’s earnings power despite macroeconomic headwinds.

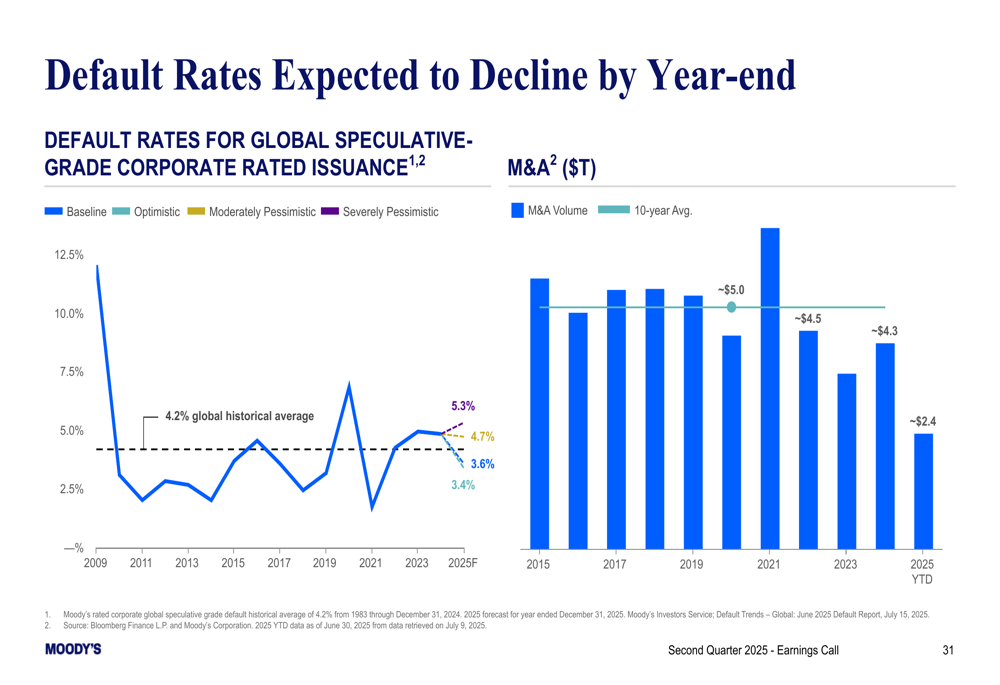

Moody’s expects global default rates to decline by year-end, providing a more favorable environment for its credit rating business. However, the company acknowledges several headwinds, including inflationary concerns, elevated funding costs, subdued M&A activity, and geopolitical uncertainties.

The following chart shows the expected trajectory of default rates:

The company’s strategic positioning focuses on capitalizing on several "deep currents" in the market, including evolving capital markets, ongoing digital transformation, heightened risk awareness, increasing need to understand climate impacts, and productivity gains from generative AI.

As shown in this strategic overview:

In conclusion, Moody’s Q2 2025 results demonstrate the resilience of its business model and its ability to generate consistent growth and expanding margins even in challenging market conditions. The narrowing of full-year EPS guidance toward the upper end of the previous range signals management’s confidence in the company’s execution and strategic positioning for the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.