First Brands Group debt targeted by Apollo Global Management - report

Introduction & Market Context

The Mosaic Company (NYSE:MOS) reported its first quarter 2025 results on May 6, 2025, showing significant improvement in net income despite challenges in production costs. The stock responded positively, rising 4.6% in after-hours trading to $31.85, following the earnings release.

The fertilizer giant’s results reflect a rebound from the disappointing fourth quarter of 2024, when the company missed both revenue and earnings expectations. This quarter’s performance demonstrates Mosaic’s ability to navigate market uncertainties while capitalizing on stronger global demand, particularly in Brazil and other international markets.

Quarterly Performance Highlights

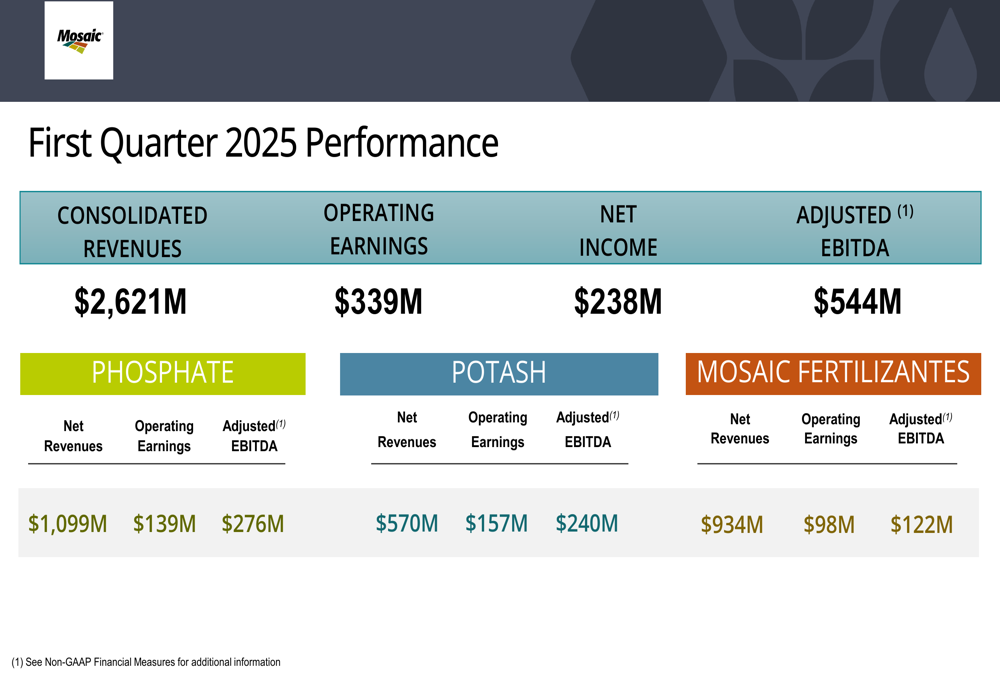

Mosaic reported consolidated net earnings of $238 million for Q1 2025, a substantial increase from $45 million in Q1 2024. However, adjusted EBITDA slightly decreased to $544 million from $576 million in the same period last year, while adjusted diluted earnings per share fell to $0.49 from $0.65.

As shown in the following financial performance summary, the company’s three main segments delivered mixed results compared to the previous year:

The Potash segment saw adjusted EBITDA decrease to $240 million from $281 million in Q1 2024, while Phosphate’s adjusted EBITDA remained relatively stable at $276 million compared to $277 million. The standout performer was Mosaic Fertilizantes, which increased its adjusted EBITDA to $122 million from $83 million, representing a 47% year-over-year improvement.

Operational Progress

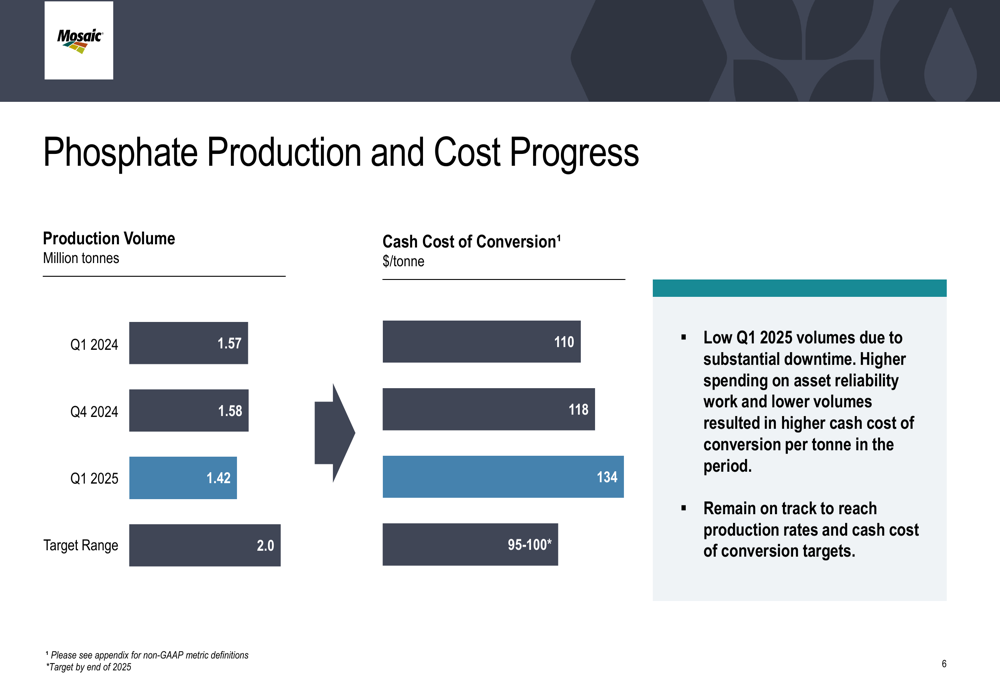

Mosaic highlighted several operational achievements in the quarter, though production volumes and costs remain areas for improvement. The company noted that March was a high phosphate production month, suggesting operations improved as the quarter progressed.

The following chart illustrates phosphate production volumes and cash costs:

Phosphate production volume in Q1 2025 was 1.42 million tonnes, below both the previous year’s 1.57 million tonnes and the target range of 2.0 million tonnes. Cash cost of conversion increased to $134 per tonne from $110 per tonne in Q1 2024, primarily due to lower volumes and higher spending on asset reliability work. Despite these challenges, management expressed confidence in reaching production and cost targets.

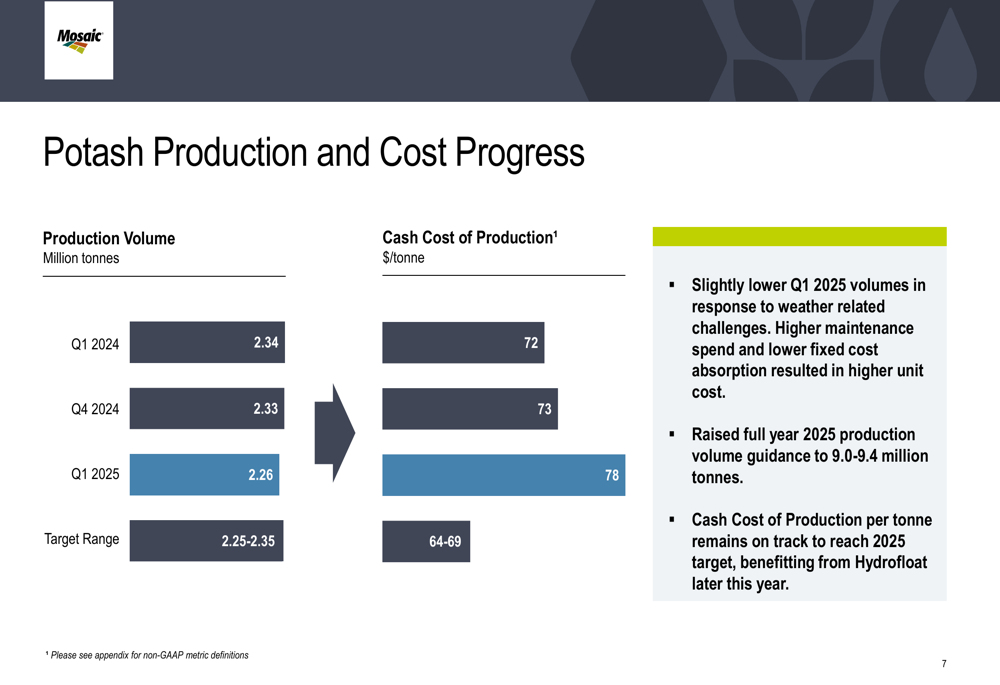

Potash operations showed more stability, as illustrated in this production and cost chart:

Potash production volume in Q1 2025 was 2.26 million tonnes, slightly lower than 2.34 million tonnes in Q1 2024 but within the target range of 2.25-2.35 million tonnes. Cash cost of production increased to $78 per tonne from $72 per tonne in the prior year, partly due to weather-related challenges. Notably, Mosaic raised its full-year 2025 potash production guidance to 9.0-9.4 million tonnes, reflecting strong demand and pricing.

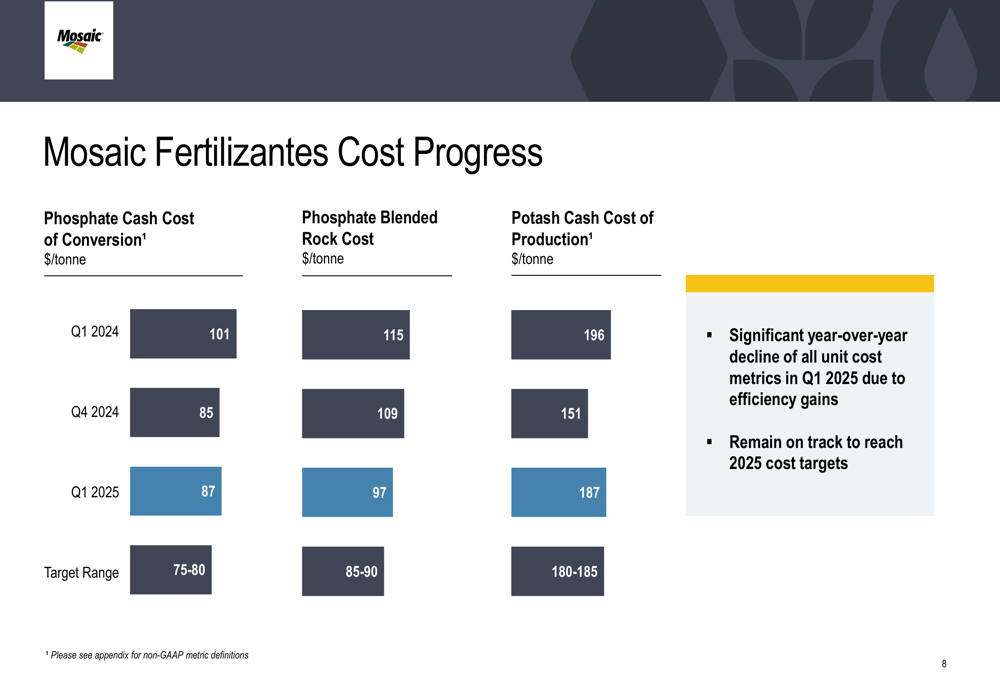

Mosaic Fertilizantes demonstrated significant cost improvements:

The segment achieved substantial year-over-year cost reductions, with phosphate cash cost of conversion decreasing to $87 per tonne from $101 per tonne in Q1 2024. The company remains on track to meet its 2025 cost targets across all segments.

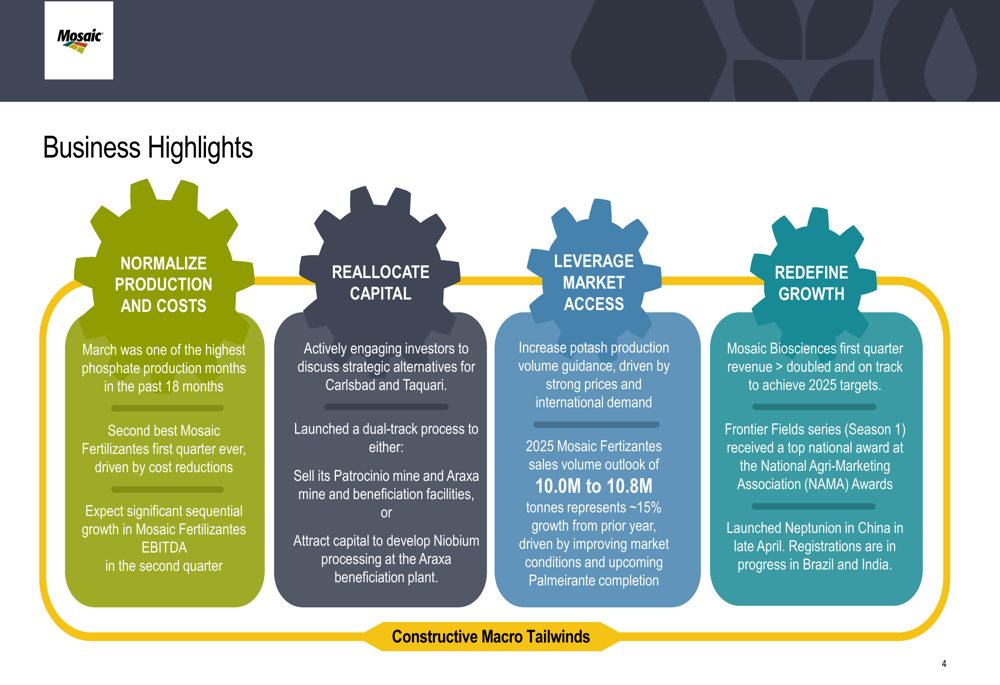

Strategic Initiatives

Mosaic outlined several strategic initiatives aimed at improving operational efficiency and reallocating capital to higher-return opportunities. The company is engaging investors on strategic alternatives for its Carlsbad and Taquari operations, while also launching a dual-track process to either sell the Patrocinio and Araxa mine/beneficiation facilities or attract capital to develop Niobium processing.

The following business highlights showcase the company’s strategic focus areas:

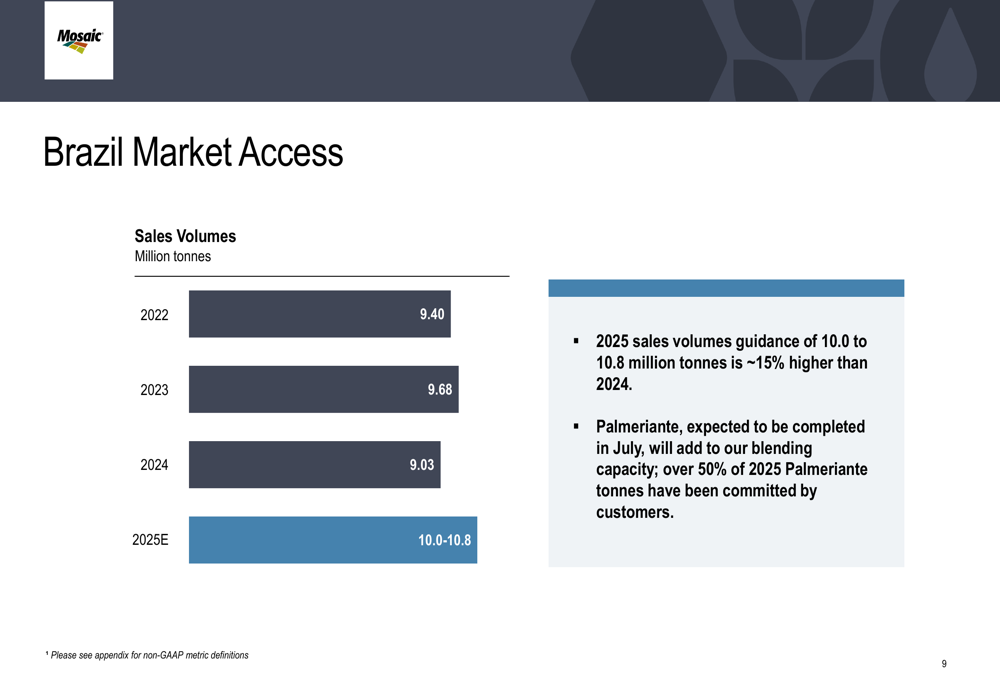

A key element of Mosaic’s strategy is leveraging its strong market access in Brazil, where the company expects significant growth in 2025:

Mosaic projects 2025 sales volumes in Brazil to reach 10.0-10.8 million tonnes, representing approximately 15% growth compared to 2024. This expansion underscores Brazil’s importance as a strategic market for Mosaic, especially as U.S. grower returns remain challenging.

Market Dynamics

The presentation highlighted contrasting market conditions across regions, with U.S. farmer returns facing pressure while international markets show more favorable dynamics. This global perspective is crucial for understanding Mosaic’s strategic positioning.

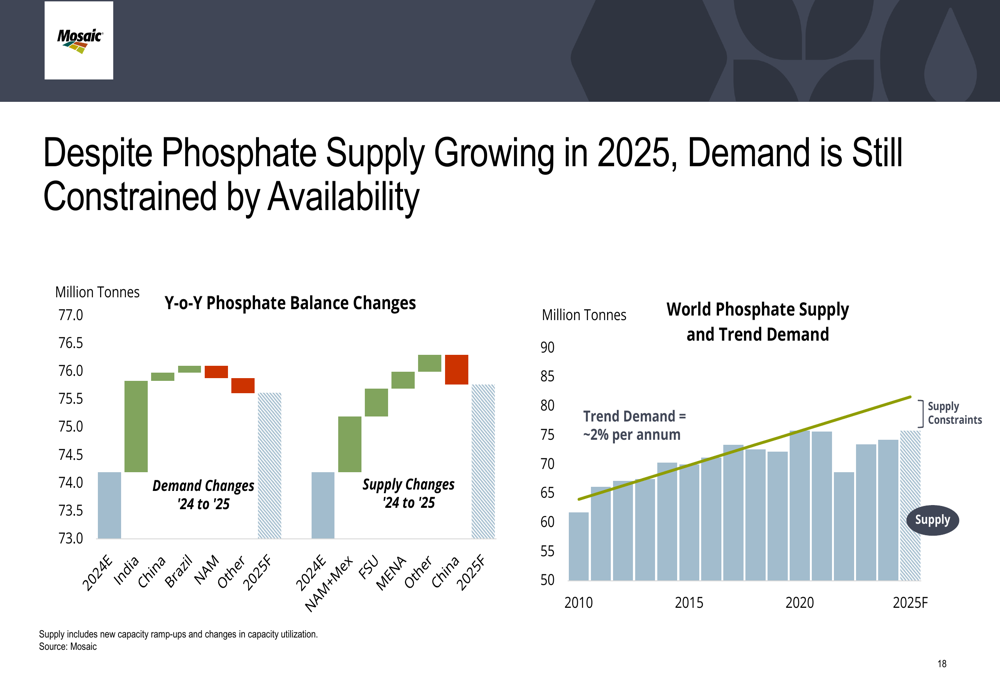

The phosphate market outlook remains constructive despite growing supply:

Despite phosphate supply growth in 2025, demand continues to be constrained by availability, supporting a balanced market. The chart illustrates how world phosphate supply remains below trend demand, with supply constraints expected to continue.

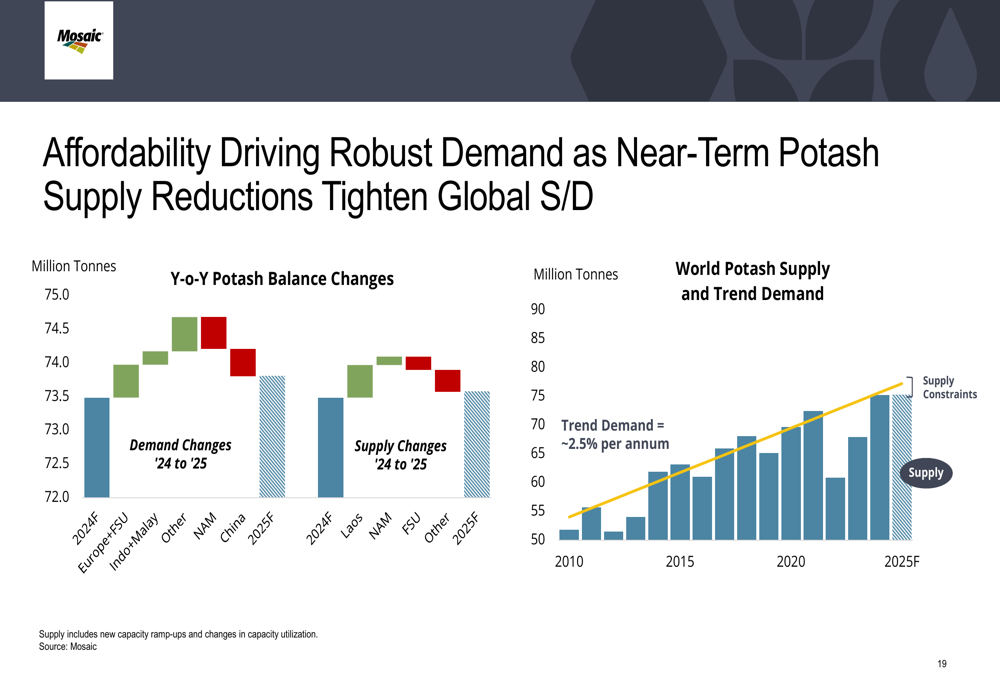

Similarly, the potash market shows favorable dynamics:

Affordability is driving robust potash demand, while near-term supply reductions are tightening the global supply/demand balance. These market conditions support Mosaic’s decision to increase its potash production guidance for 2025.

Forward Guidance

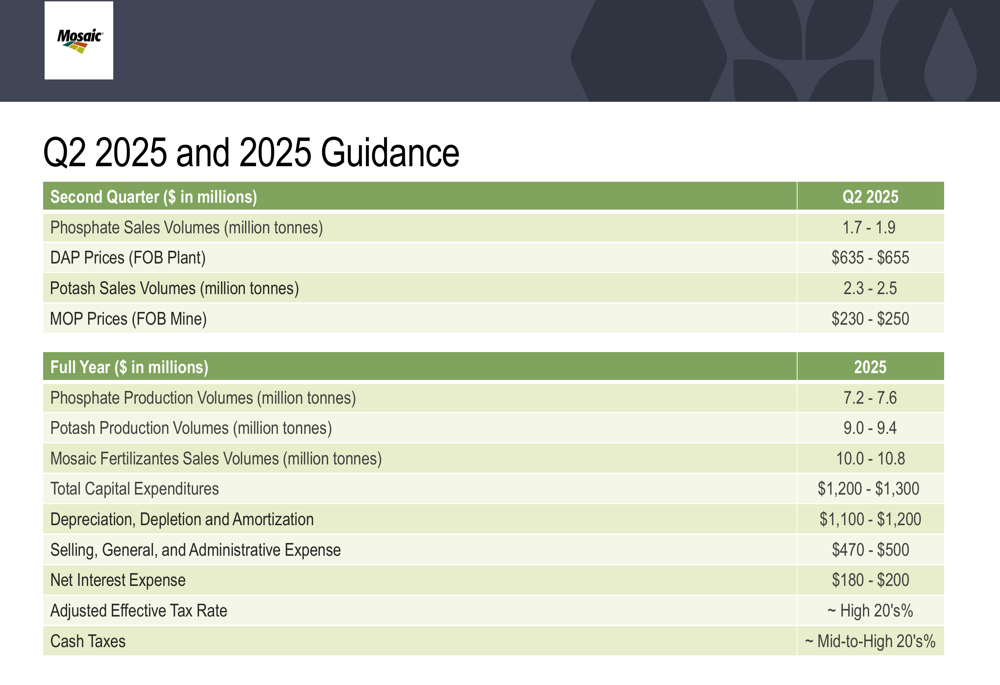

Mosaic provided detailed guidance for both Q2 2025 and the full year, reflecting management’s confidence in continued operational improvements and favorable market conditions:

For Q2 2025, the company expects phosphate sales volumes of 1.7-1.9 million tonnes with DAP prices of $635-$655 per tonne, and potash sales volumes of 2.3-2.5 million tonnes with MOP prices of $230-$250 per tonne.

Full-year guidance includes phosphate production of 7.2-7.6 million tonnes, increased potash production of 9.0-9.4 million tonnes, and Mosaic Fertilizantes sales of 10.0-10.8 million tonnes. Capital expenditures are projected at $1,200-$1,300 million, with an adjusted effective tax rate in the high 20% range.

Conclusion

Mosaic’s Q1 2025 results demonstrate a significant improvement in net income and a strategic pivot toward global markets, particularly Brazil, to offset challenges in North America. While operational metrics show mixed results, with production volumes and costs still working toward targets, the company’s increased guidance for potash production and Mosaic Fertilizantes sales volumes reflects management’s confidence in the business outlook.

The positive after-hours stock reaction suggests investors are encouraged by the company’s progress and forward guidance, marking a notable turnaround from the disappointing Q4 2024 results. As Mosaic continues to implement its strategic initiatives and capitalize on favorable global market dynamics, investors will be watching closely to see if operational improvements translate into sustained financial performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.