Intellia presents positive data for hereditary angioedema treatment

Introduction & Market Context

Motiva Infraestrutura de Mobilidade S.A. (BOVESPA:MOTV3) presented its third quarter 2025 earnings results on October 30, showcasing significant profitability improvements despite falling short of revenue expectations. The company’s stock closed at R$15.56, down 0.96% on the day of the presentation, reflecting mixed investor sentiment following the earnings announcement.

The infrastructure operator, which manages toll roads, railways, and airports across Brazil, reported an EPS of $0.3381, exceeding analyst forecasts by 28.7%. However, revenue came in at R$4.91 billion, missing the expected R$5.11 billion by 3.91%, highlighting the company’s focus on profitability over top-line growth.

Quarterly Performance Highlights

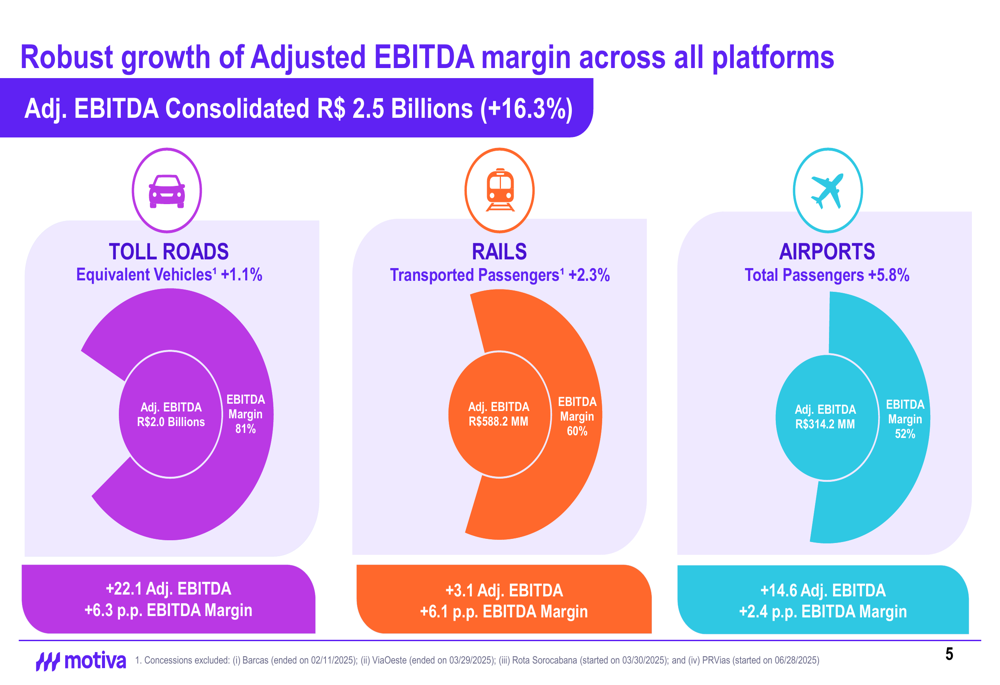

Motiva delivered robust growth in profitability metrics, with adjusted EBITDA increasing by 16.3% compared to the same period last year, while adjusted net income surged by 22% to reach R$683 million. The company also achieved a significant 6.5 percentage point improvement in adjusted EBITDA margin.

As shown in the following chart of Motiva’s main quarterly highlights:

The company’s performance was driven by traffic growth across all transportation modes, with toll roads, railways, and airports experiencing increases of 1.1%, 2.3%, and 5.8% respectively. This growth, combined with operational efficiencies, contributed to expanded EBITDA margins across all business platforms.

The following visualization illustrates the EBITDA margin improvements across Motiva’s business segments:

Toll roads remained the most profitable segment with an impressive 81% EBITDA margin (up 6.3 percentage points year-over-year), followed by rails at 60% (up 6.1 percentage points) and airports at 52% (up 2.4 percentage points). These improvements demonstrate the company’s successful execution of its operational efficiency initiatives.

Detailed Financial Analysis

Motiva’s strategic focus on cost reduction has been a key driver of its improved profitability. The company reduced adjusted cash costs by 11.4% compared to the third quarter of 2024, resulting in an improved Opex ratio (Cash)/Adjusted Net Revenue of 38.3% for the last twelve months, down from 41.5% in 3Q24.

The following chart details the company’s cost reduction journey:

The most significant cost reductions came from third-party services (-24% or R$130 million), personnel costs (-5% or R$31 million), and other operational expenses (-6% or R$21 million). These reductions were partially driven by the termination of the Barcas and ViaOeste operation contracts, as well as reduced pavement maintenance expenses at Motiva Pantanal.

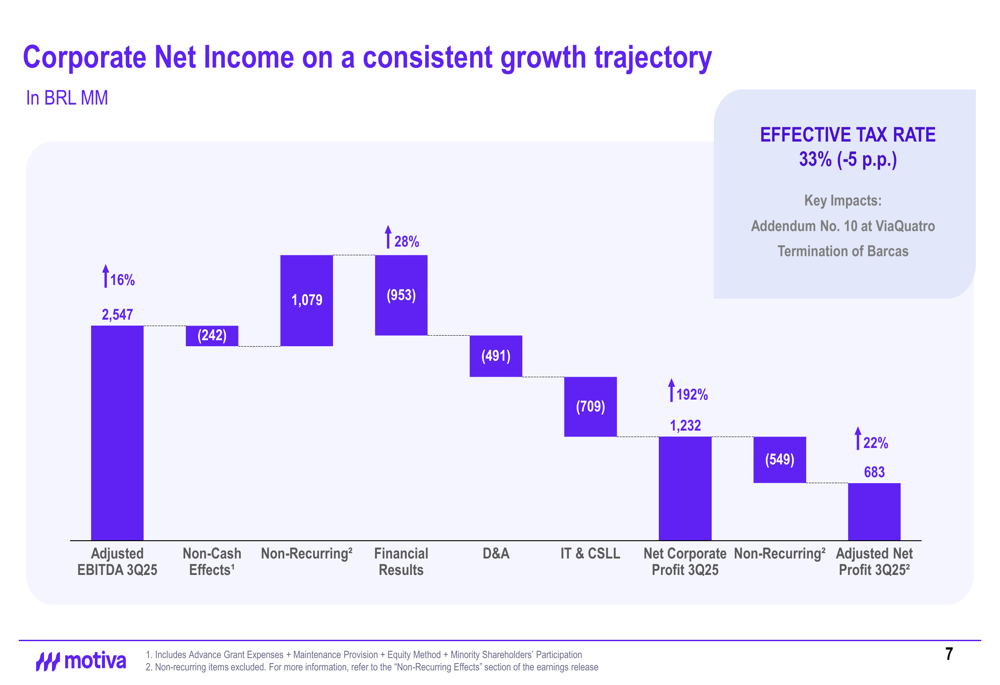

The company’s net income growth trajectory is illustrated in the following waterfall chart:

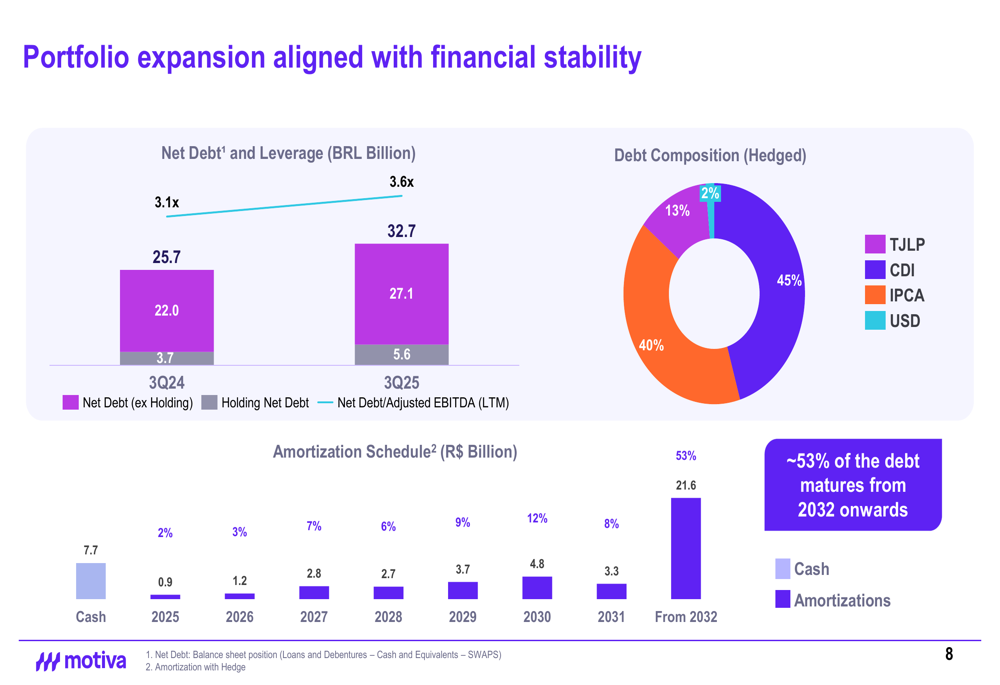

While Motiva has successfully improved its profitability, its leverage has increased compared to the previous year. The Net Debt/Adjusted EBITDA ratio rose to 3.6x in 3Q25 from 3.1x in 3Q24, reflecting the company’s continued investments in portfolio expansion.

The following chart provides a comprehensive overview of Motiva’s debt profile:

The company maintains a relatively comfortable debt maturity profile, with approximately 53% of its debt maturing from 2032 onwards and only 2% due in 2025. The debt is primarily denominated in local currency, with 45% linked to the CDI rate and 40% to the IPCA inflation index.

Strategic Initiatives

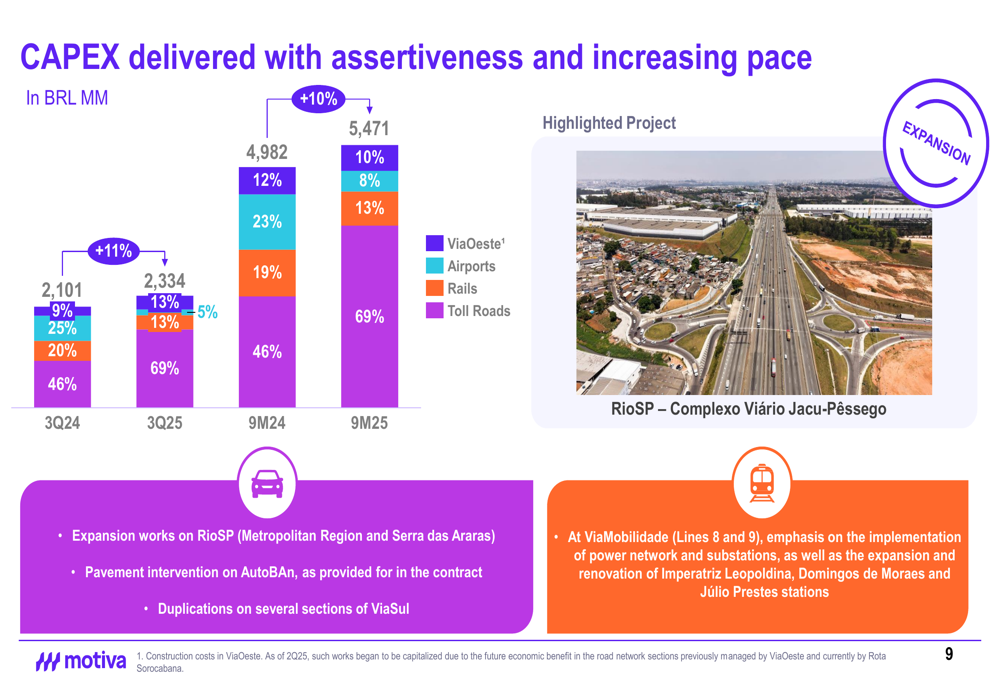

Motiva continues to execute its capital expenditure program, with CAPEX increasing by 11.1% to R$2.3 billion compared to 3Q24. The 9-month CAPEX total reached R$5.47 billion, representing a 10% increase over the same period last year.

The following chart illustrates Motiva’s CAPEX allocation across business segments:

The rails segment saw a significant increase in investment, accounting for 69% of 3Q25 CAPEX compared to 20% in 3Q24. This shift reflects the company’s strategic focus on expanding and modernizing its rail infrastructure, particularly at ViaMobilidade (Lines 8 and 9), where investments are being made in power networks, substations, and station renovations.

Motiva also secured important contractual amendments, including a 20-year extension with ViaQuatro and a 73-day extension with SPVias. Additionally, the company signed a modernization contract for Motiva Pantanal, further strengthening its long-term operational outlook.

Forward-Looking Statements

Looking ahead, Motiva aims to maintain its operational efficiency ratio below 38%, potentially achieving this target by the end of 2025. The company is also preparing for a potential airport platform transaction by year-end and plans to develop an international partnership platform for its airport business in 2026.

During the earnings call, CEO Miguel Setos emphasized the company’s selective approach to asset acquisition, stating, "We are being very selective. We’re looking at assets that have synergies and that are very strategic for our business." Meanwhile, CFO Valdo Perez highlighted the benefits of industry competition in maintaining performance pressure.

Despite the positive profitability trends, investors should note the increasing leverage ratio and revenue shortfall, which could pose challenges if they persist. Additionally, the competitive infrastructure investment landscape may pressure margins, and macroeconomic factors could impact credit market conditions.

With its diversified portfolio across toll roads, railways, and airports, combined with a strong focus on operational efficiency and strategic contract extensions, Motiva appears well-positioned to navigate these challenges while continuing to deliver improved profitability for shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.