Still betting on Nvidia? Our AI picked this stock instead; it’s up 96%+ THIS MONTH

Introduction & Market Context

Motorola Solutions (NYSE:MSI) reported solid first-quarter results for 2025, with growth across all technology segments and record operating cash flow. The company presented its Q1 2025 earnings on May 1, 2025, showcasing continued momentum in its core business areas while expanding its AI capabilities for public safety applications.

The company’s performance was particularly strong in North America, which offset some weakness in international markets. Motorola Solutions also highlighted its recent acquisitions and new product launches that strengthen its position in the public safety technology ecosystem.

Quarterly Performance Highlights

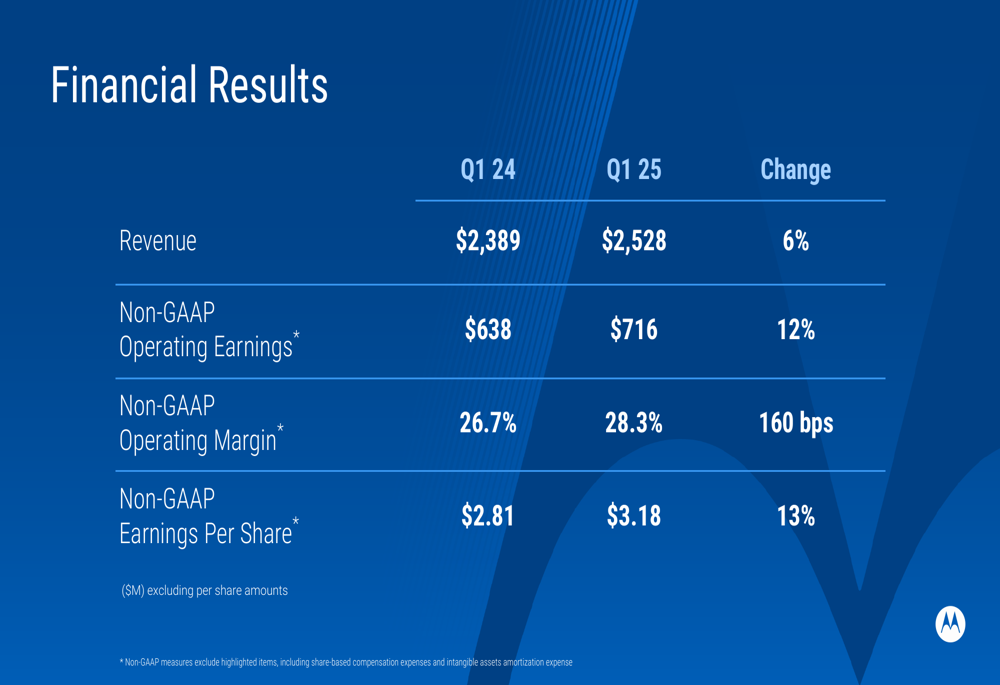

Motorola Solutions reported Q1 2025 sales of $2.5 billion, representing a 6% year-over-year increase. The company saw growth across all its technology segments, with Land Mobile Radio (LMR) up 4%, Video up 11%, and Command Center up 10%.

As shown in the following financial results comparison:

Non-GAAP earnings per share reached $3.18, up 13% compared to the prior year, while GAAP EPS was $2.53. The company’s non-GAAP operating margin expanded to 28.3%, an increase of 160 basis points year-over-year, demonstrating improved operational efficiency.

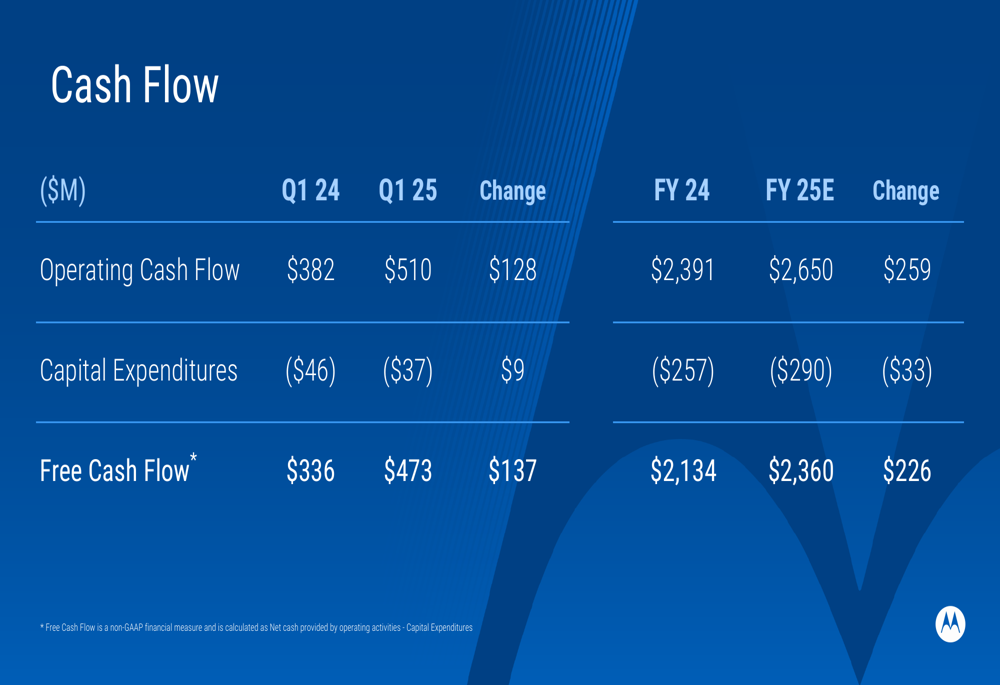

Motorola Solutions generated record first-quarter operating cash flow of $510 million, a significant increase of $128 million compared to Q1 2024. This strong cash generation supported the company’s capital allocation strategy, which included $325 million in share repurchases and $182 million in dividend payments during the quarter.

The company’s free cash flow performance is illustrated in the following chart:

Segment Performance Analysis

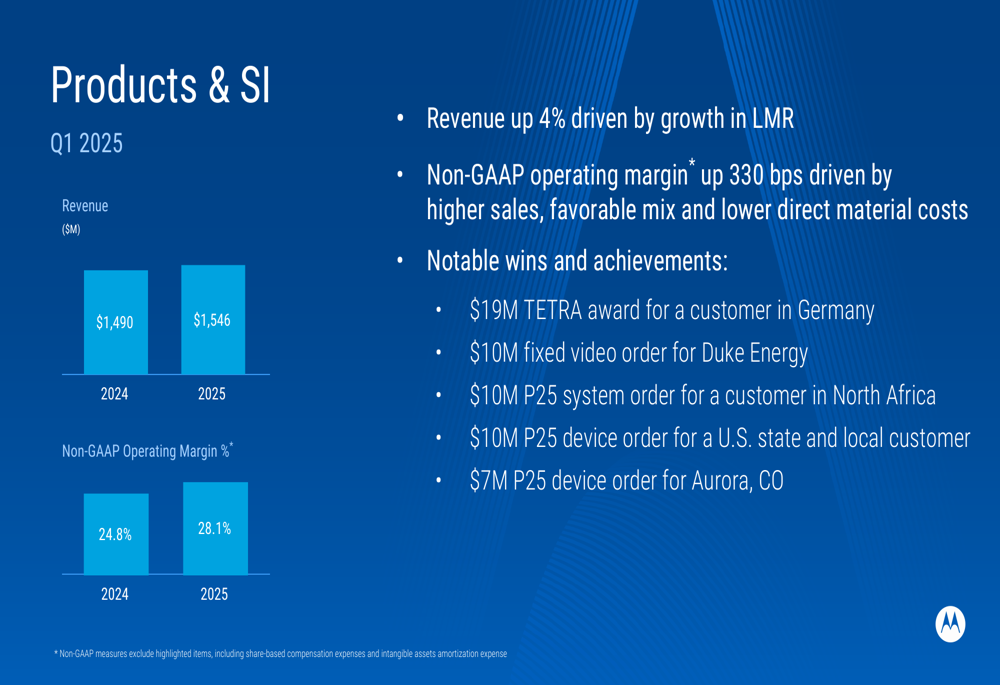

The Products and Systems Integration segment, which includes the company’s hardware offerings, saw revenue increase by 4% to $1.55 billion, driven primarily by growth in LMR products. More impressively, the segment’s non-GAAP operating margin expanded by 330 basis points to 28.1%, benefiting from higher sales, favorable product mix, and lower direct material costs.

Key wins in this segment included a $19 million TETRA award for a customer in Germany, a $10 million fixed video order for Duke Energy (NYSE:DUK), and several P25 system and device orders for various customers.

The segment’s performance is summarized in the following chart:

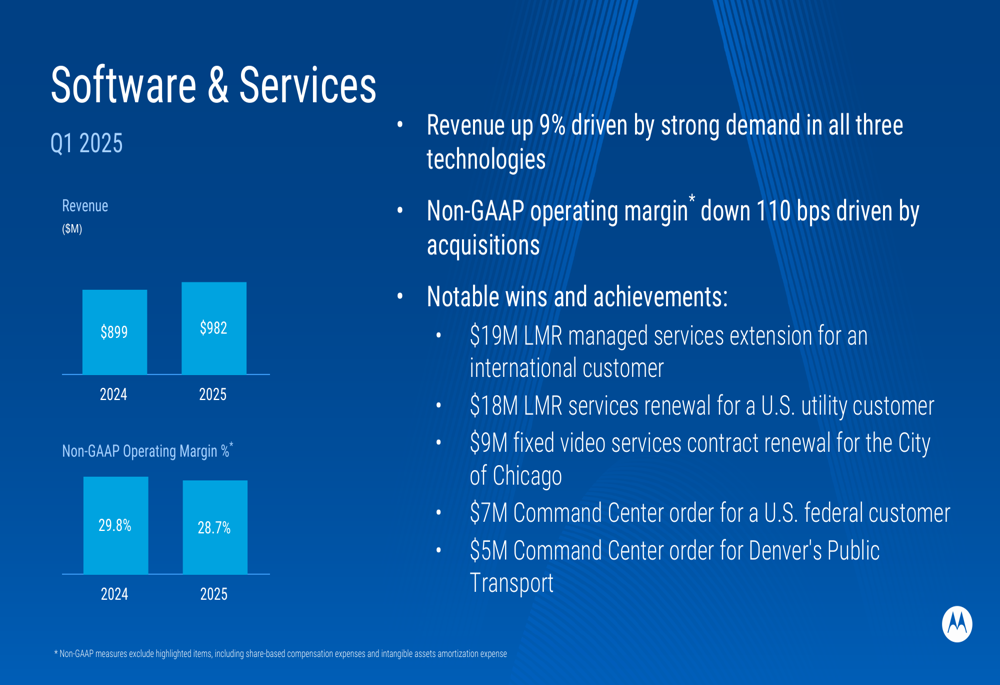

The Software (ETR:SOWGn) and Services segment continued its strong performance with revenue up 9% to $982 million, reflecting robust demand across all three technology areas. However, the segment’s non-GAAP operating margin decreased by 110 basis points to 28.7%, which the company attributed to recent acquisitions.

Notable achievements in this segment included a $19 million LMR managed services extension for an international customer, an $18 million LMR services renewal for a U.S. utility customer, and several Command Center orders for government and transportation clients.

The Software and Services segment performance is illustrated here:

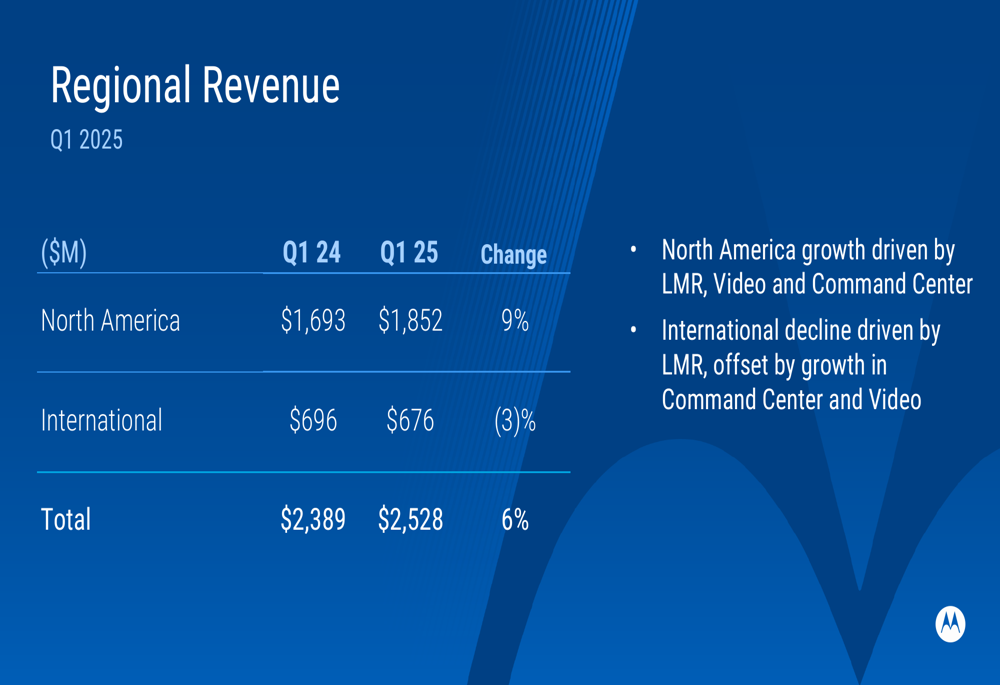

Regional Performance

Motorola Solutions’ performance varied significantly by region in Q1 2025. North America revenue reached $1.85 billion, up 9% year-over-year, driven by growth across LMR, Video, and Command Center technologies. This strong performance in the company’s largest market helped offset challenges in international regions.

International revenue declined by 3% to $676 million, with weakness in LMR partially offset by growth in Command Center and Video solutions. This regional disparity highlights the company’s dependence on its home market for growth in the current environment.

The regional revenue breakdown is shown in the following chart:

Product Innovation and Strategic Initiatives

During the quarter, Motorola Solutions completed two acquisitions for a combined $414 million: RapidDeploy and Theatro. These acquisitions align with the company’s strategy to enhance its software capabilities and expand its offerings for public safety and enterprise customers.

The company also launched two significant new products: SVX, a converged secure P25 speaker mic and body-worn camera, and Assist, an AI solution for public safety. The SVX product represents Motorola’s approach to integrating critical communications equipment with evidence capture capabilities in a single device.

The SVX with Assist product is showcased in the following image:

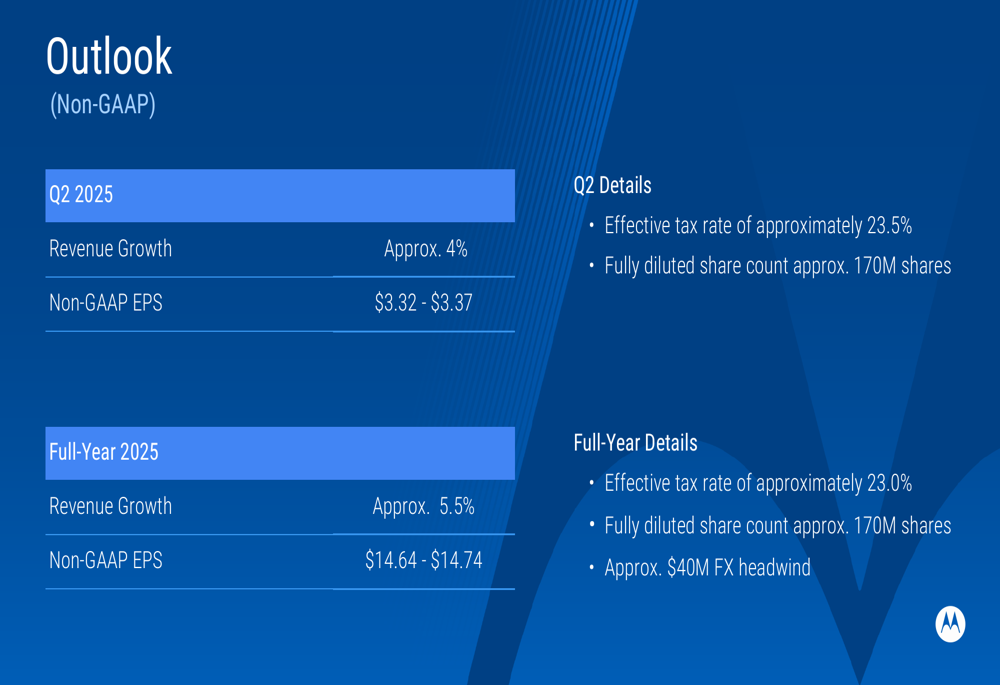

Forward Guidance

Looking ahead, Motorola Solutions provided guidance for both Q2 2025 and the full year. For the second quarter, the company expects revenue growth of approximately 4% and non-GAAP EPS between $3.32 and $3.37.

For the full year 2025, Motorola Solutions forecasts revenue growth of approximately 5.5% and non-GAAP EPS between $14.64 and $14.74. The company noted an anticipated $40 million foreign exchange headwind for the year.

The detailed outlook is presented in the following slide:

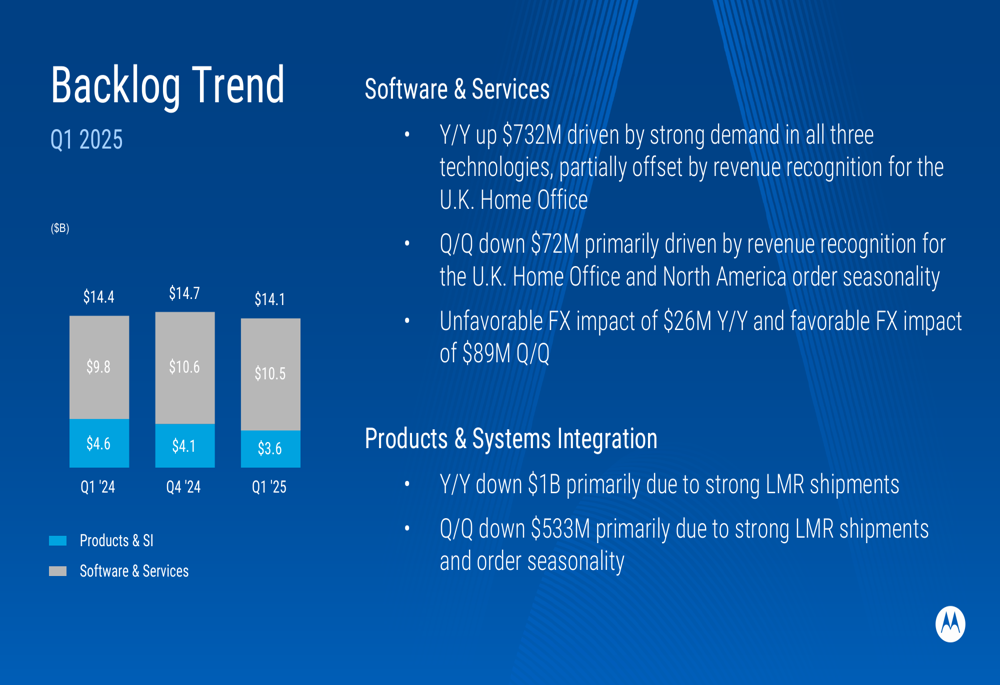

Backlog and Future Opportunities

Motorola Solutions reported a total backlog of $14.1 billion at the end of Q1 2025, down from $14.4 billion a year earlier. The Software & Services backlog increased by $732 million year-over-year, driven by strong demand across all technologies, but was partially offset by revenue recognition for the U.K. Home Office contract.

The Products & Systems Integration backlog decreased by $1 billion year-over-year, which the company attributed primarily to strong LMR shipments. This reduction in backlog, while potentially concerning at first glance, reflects the company’s ability to fulfill orders efficiently rather than a decline in demand.

The backlog trend is illustrated in the following chart:

Conclusion

Motorola Solutions delivered a solid first quarter for 2025, with growth across all technology segments and significant margin expansion in its Products and Systems Integration business. The company’s strong performance in North America offset weakness in international markets, resulting in overall revenue growth of 6%.

With record operating cash flow, continued product innovation, and strategic acquisitions, Motorola Solutions appears well-positioned to maintain its leadership in public safety technology. The company’s guidance suggests continued growth, albeit at a slightly moderated pace compared to Q1, with full-year revenue expected to increase by approximately 5.5%.

Investors will likely focus on the company’s ability to maintain margin expansion while integrating recent acquisitions and navigating challenges in international markets. The emphasis on AI-powered solutions and integrated products like the SVX demonstrates Motorola’s commitment to innovation in its core public safety market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.