60%+ returns in 2025: Here’s how AI-powered stock investing has changed the game

MP Materials Corp (NYSE:MP) presented its third-quarter 2025 results on November 6, highlighting record production of neodymium-praseodymium (NdPr) oxide despite ongoing revenue challenges as the company transitions its business model. The rare earth materials producer's stock closed down 5.43% at $54.93 during regular trading hours before recovering 2.28% in aftermarket trading.

Introduction & Market Context

MP Materials is positioning itself as a vertically integrated supplier in the critical rare earth materials space, with operations spanning from mining to magnet production. The company's strategic importance has grown amid increasing geopolitical tensions and concerns about China's dominance in the rare earth supply chain, which CEO Jim Litinsky characterized as "a new kind of Cold War" fought with supply chains rather than weapons.

The company's Q3 results reflect a transitional period as MP Materials shifts from selling concentrate to higher-value separated products and magnetic materials, resulting in near-term revenue pressure but potential for stronger future margins and strategic positioning.

Quarterly Performance Highlights

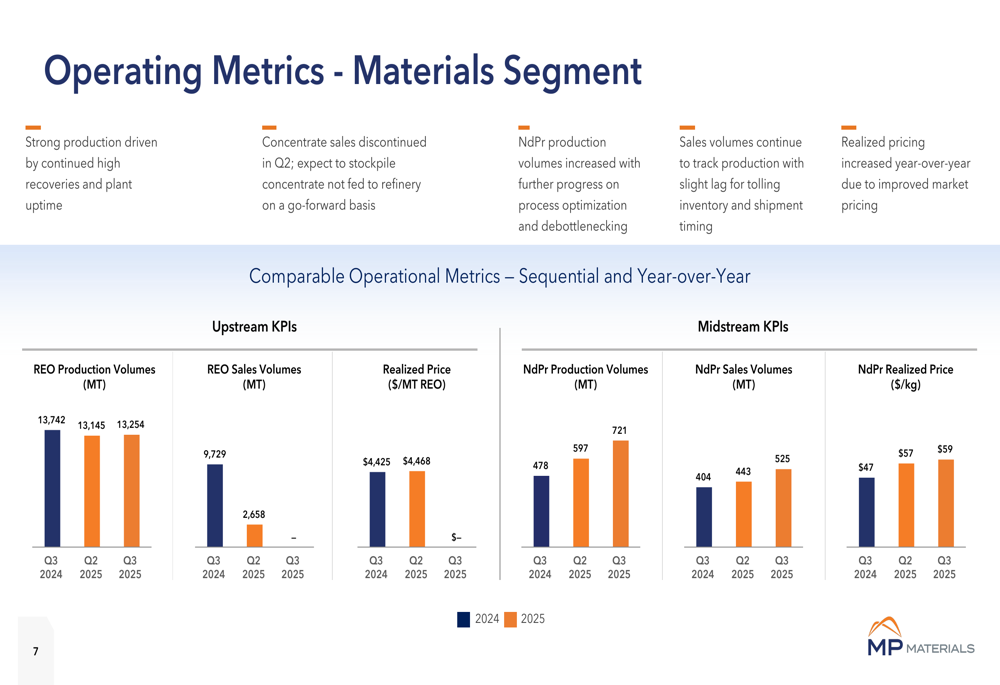

MP Materials achieved record NdPr oxide production of 721 metric tons in Q3 2025, representing a 21% sequential increase from Q2 and a 51% year-over-year improvement. This production milestone comes alongside the company's second-highest quarterly production of rare earth oxide (REO).

As shown in the following operational metrics chart, the company has steadily increased its NdPr production while completely phasing out concentrate sales:

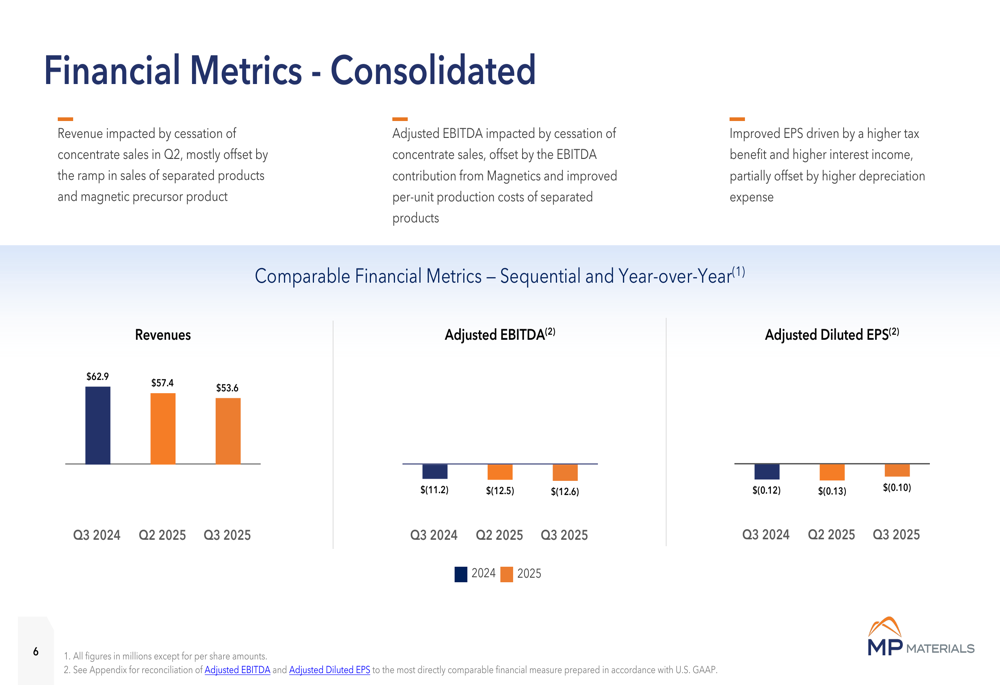

The company reported revenue of $53.6 million for Q3 2025, down from $62.9 million in Q3 2024 but relatively stable compared to $57.4 million in Q2 2025. This revenue decline was primarily attributed to the cessation of concentrate sales, which was partially offset by increased sales of separated products and magnetic precursor materials.

The consolidated financial metrics reveal the current challenges and transition state:

Detailed Financial Analysis

MP Materials' financial performance reflects its strategic pivot toward higher-value products. The company reported an adjusted EBITDA of $(12.6) million in Q3 2025, compared to $(11.2) million in Q3 2024. Despite the slight deterioration, adjusted diluted EPS improved to $(0.10) from $(0.12) year-over-year, beating analyst expectations of $(0.17).

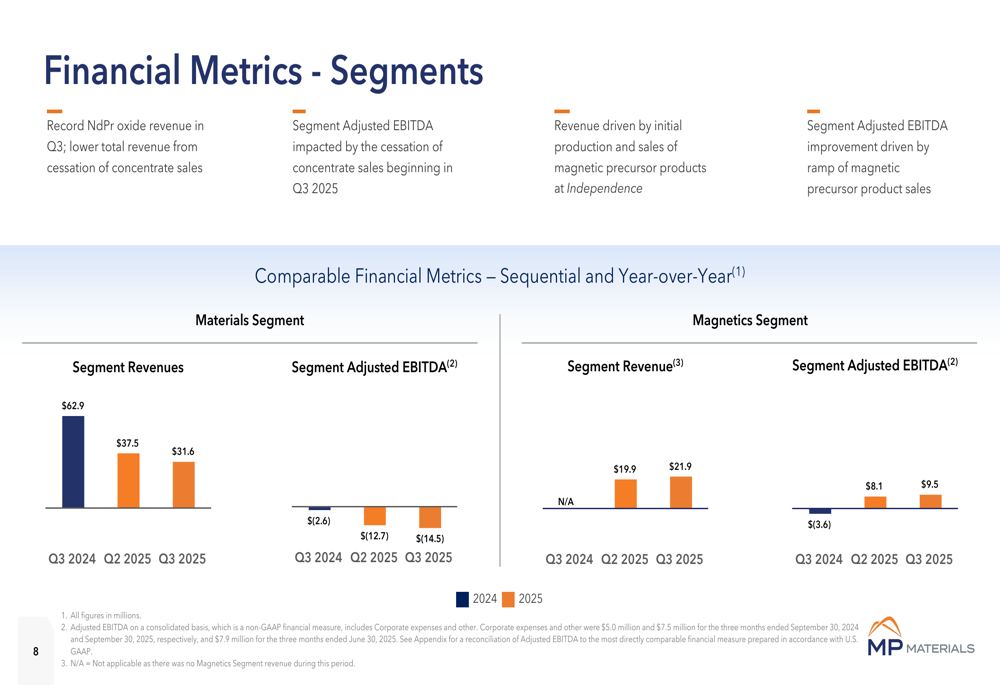

The segment breakdown provides additional insight into the company's transition:

The Materials segment, which includes mining and processing operations, generated $31.6 million in revenue with an adjusted EBITDA of $(14.5) million. Meanwhile, the Magnetics segment contributed $21.9 million in revenue with a positive adjusted EBITDA of $9.5 million, demonstrating the potential profitability of downstream operations.

NdPr sales volumes increased to 525 metric tons (from 404 metric tons in Q3 2024), with realized prices rising to $59/kg from $47/kg year-over-year, reflecting improved market conditions for separated rare earth products.

Strategic Initiatives

MP Materials highlighted several strategic developments during the quarter that position the company for future growth. The Department of Defense purchase price agreement commenced on October 1, 2025, providing price protection and revenue stability. Additionally, the company received an initial $40 million prepayment from Apple, strengthening its financial position and validating its strategic direction.

The company is advancing its vertical integration strategy, as illustrated in this supply chain overview:

MP Materials is also developing heavy rare earth separation capabilities, with initial capacity of 200+ metric tons per annum for dysprosium and terbium separations expected to be commissioned in mid-2026. This expansion into heavy rare earths will complement the company's existing light rare earth operations.

The following image shows the heavy rare earth separation equipment being installed:

The company continues to progress on its Independence facility commissioning, with initial commercial magnet production on track for year-end 2025. This vertical integration is expected to capture more value from the rare earth supply chain and reduce dependence on Chinese processing.

Forward-Looking Statements

MP Materials presented an optimistic outlook for future EBITDA potential, suggesting that the current financial challenges are temporary as the company completes its strategic transformation:

The company projects potential annual EBITDA exceeding $650 million, driven by the Independence facility, minimum pricing agreements, and potential upside from NdPr price increases, upstream expansion, and magnetics growth.

Management expressed confidence about returning to profitability in Q4 2025, with magnet revenue expected to commence in the second half of 2026. The company is targeting 10,000 metric tons of annual magnet production capacity.

CEO Jim Litinsky emphasized long-term demand prospects during the earnings call, stating, "We do not lose any sleep over what demand is going to look like in 10 years... I think it is going to be amazing for us."

Despite current challenges, MP Materials' strategic positioning in the rare earth supply chain, coupled with its progress in vertical integration and key partnerships, suggests potential for improved financial performance as the company completes its transition from a concentrate producer to a fully integrated rare earth magnetics supplier.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.