Street Calls of the Week

Introduction & Market Context

MRC Global Inc (NYSE:MRC) released its second quarter 2025 earnings presentation on August 6, 2025, revealing a 12% sequential revenue increase and announcing a significant strategic combination with DNOW. The company’s shares responded positively in premarket trading, rising 5.15% to $15.10, suggesting investors are encouraged by the improved performance following a disappointing first quarter.

The presentation comes after MRC Global missed expectations in Q1 2025, when the company reported earnings per share of $0.14 against a forecast of $0.22, causing an 8% stock drop. The Q2 results indicate a substantial recovery with sequential improvements across all business segments.

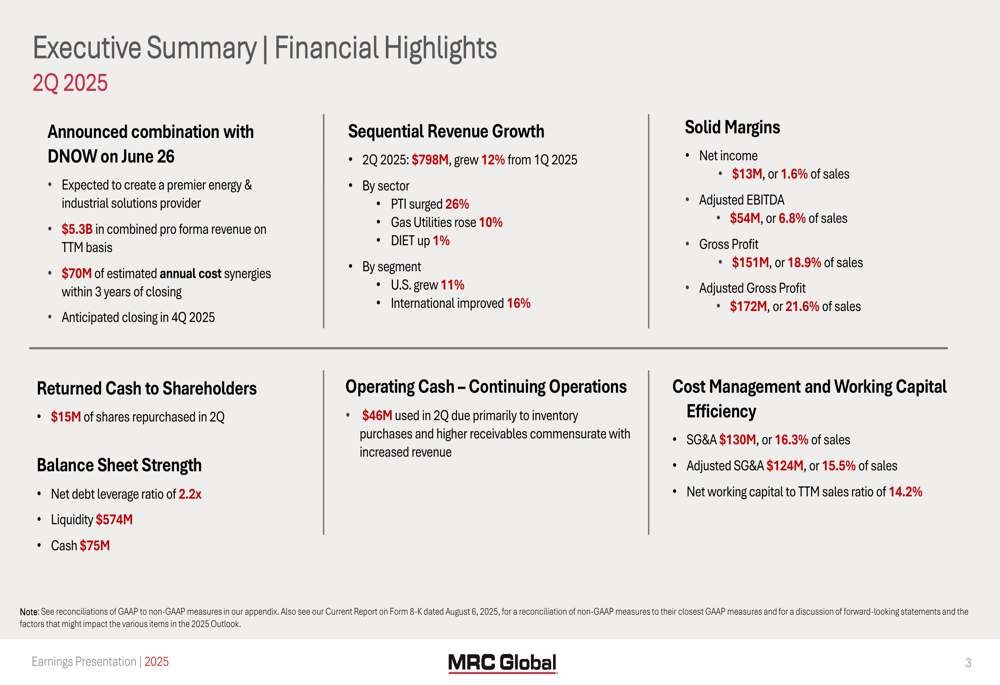

Executive Summary

MRC Global reported Q2 2025 revenue of $798 million, representing a 12% increase from the $712 million reported in Q1. Net income reached $13 million (1.6% of sales), while adjusted EBITDA was $54 million (6.8% of sales), showing significant improvement from the 5.1% adjusted EBITDA margin in the previous quarter.

The most notable strategic development was the announced combination with DNOW on June 26, which is expected to create a premier energy and industrial solutions provider with $5.3 billion in combined pro forma revenue on a trailing twelve-month basis. The company anticipates approximately $70 million in annual cost synergies within three years of closing, which is expected in Q4 2025.

As shown in the following financial highlights summary:

Quarterly Performance Highlights

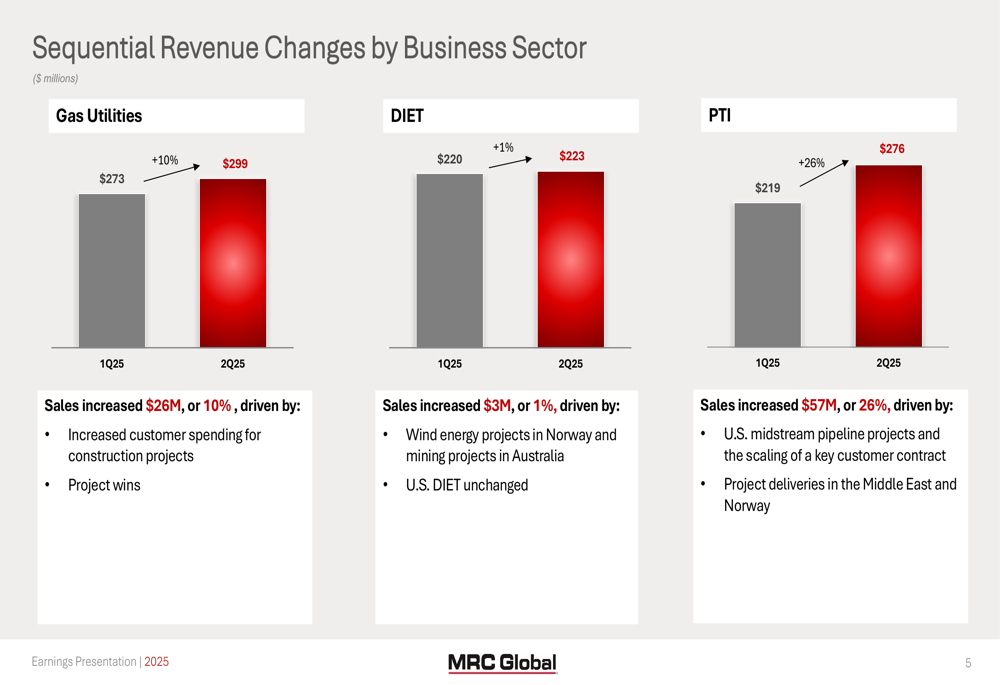

All three of MRC Global’s business segments showed sequential growth in Q2 2025, with the Pipeline, Transmission & Infrastructure (PTI) sector leading the way with a 26% increase to $276 million. This growth was primarily driven by U.S. midstream pipeline projects, the scaling of a key customer contract, and project deliveries in the Middle East and Norway.

The Gas Utilities sector, which represents the largest portion of MRC’s business at 37% of total revenue, grew 10% sequentially to $299 million, fueled by increased customer spending for construction projects and new project wins. The Downstream, Industrial, Energy Transition (DIET) sector showed modest growth of 1%, reaching $223 million, supported by wind energy projects in Norway and mining projects in Australia.

The following chart illustrates the sequential revenue changes by business sector:

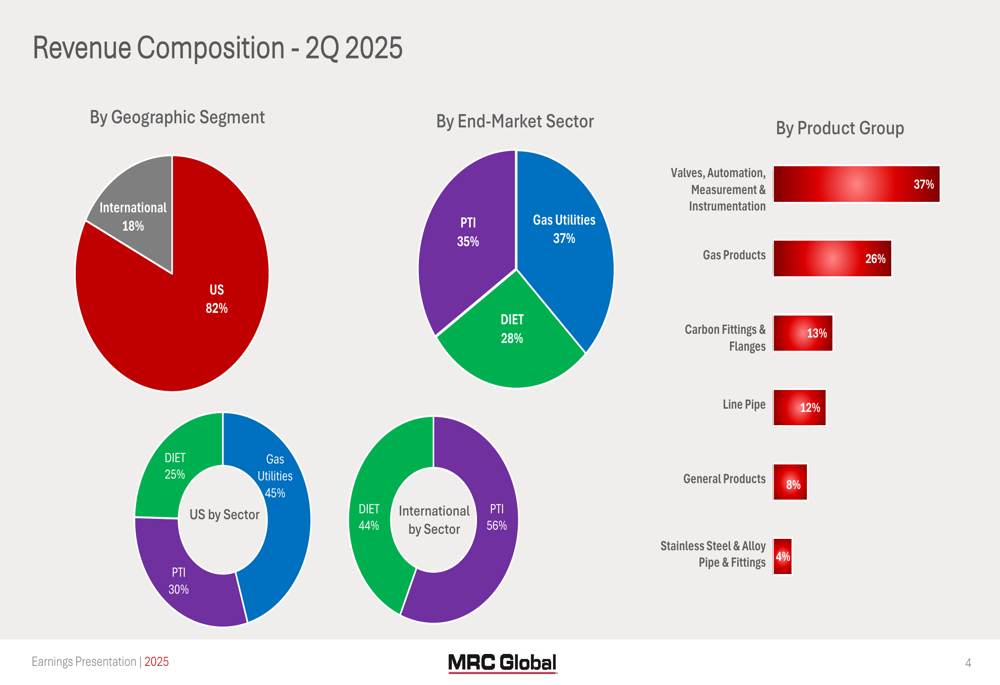

From a geographic perspective, U.S. operations, which account for 82% of total revenue, grew 11% sequentially, while International operations, representing 18% of revenue, increased by 16%. The company’s revenue composition by product group continues to be led by Valves, Automation, Measurement & Instrumentation at 37% of revenue, followed by Gas Products at 26%.

The revenue breakdown by various segments is shown in the following chart:

Detailed Financial Analysis

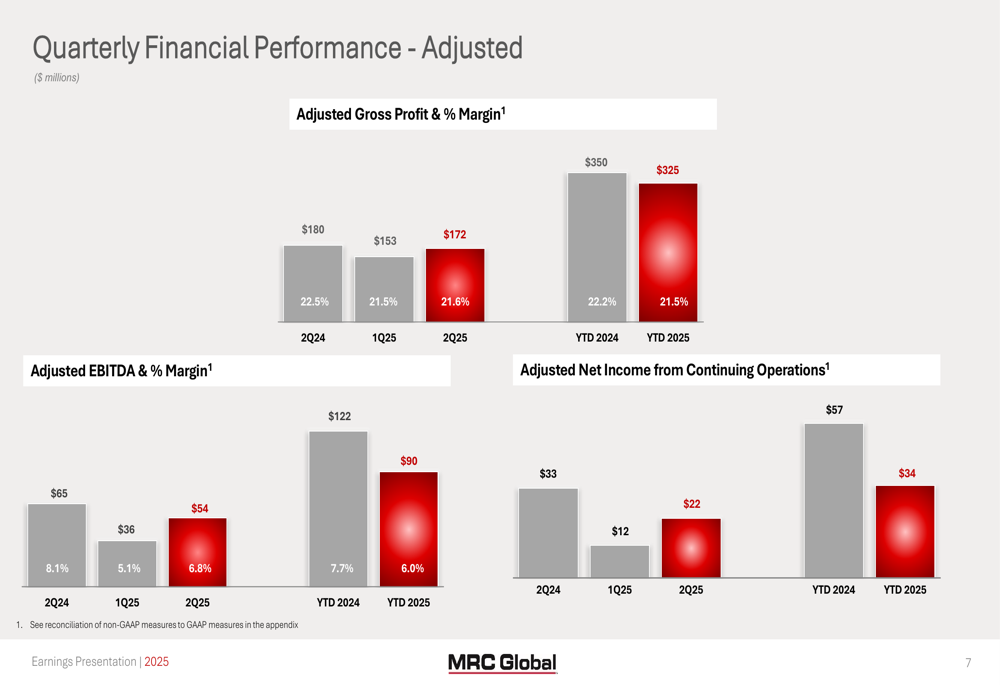

MRC Global’s gross profit for Q2 2025 was $151 million (18.9% of sales), while adjusted gross profit reached $172 million (21.6% of sales). This represents a slight improvement in adjusted gross profit margin compared to Q1 2025 (21.5%), though it remains below the 22.5% achieved in Q2 2024.

The company’s SG&A expenses were $130 million (16.3% of sales), with adjusted SG&A at $124 million (15.5% of sales), showing improved efficiency compared to Q1 2025 when adjusted SG&A was 17.0% of sales.

Diluted earnings per share from continuing operations improved to $0.15 in Q2 2025, up from $0.09 in Q1 2025, but still below the $0.28 reported in Q2 2024. Adjusted net income from continuing operations was $22 million for the quarter, nearly doubling from the $12 million reported in Q1 2025.

The company’s quarterly financial performance on an adjusted basis is illustrated below:

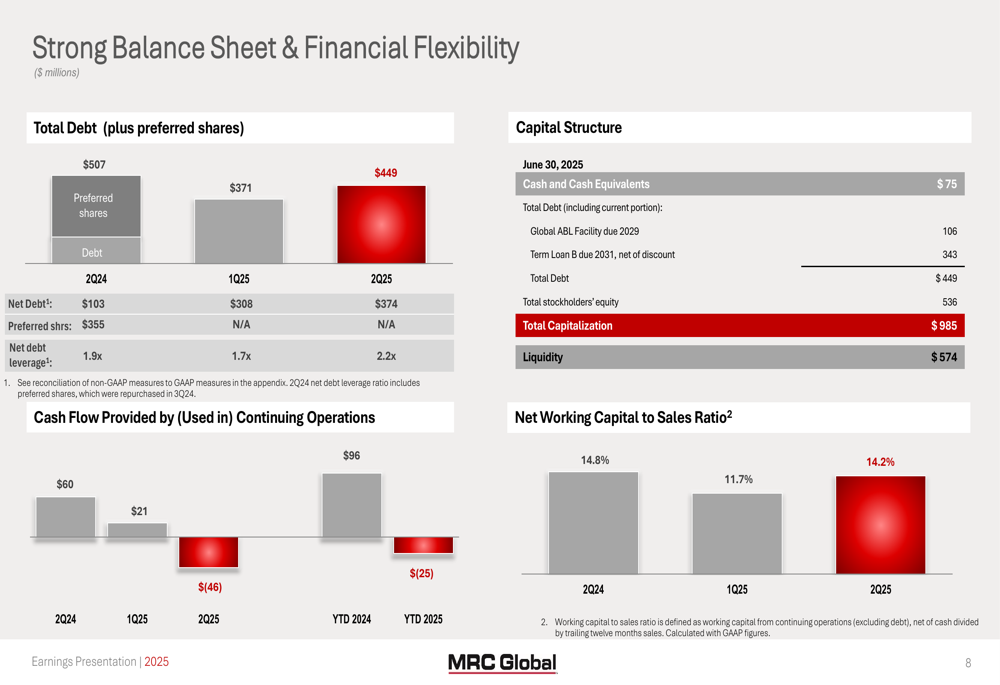

Balance Sheet and Cash Flow

MRC Global maintained a strong balance sheet with total debt of $449 million as of June 30, 2025, up from $371 million at the end of Q1. After accounting for $75 million in cash and cash equivalents, the net debt was $374 million, resulting in a net debt leverage ratio of 2.2x based on trailing twelve months adjusted EBITDA of $170 million. This represents a significant increase from the 0.4x ratio reported a year earlier.

The company used $46 million in operating cash during Q2, primarily due to inventory purchases and higher receivables, contrasting with the $21 million generated in Q1 2025 and $60 million in Q2 2024. Despite this cash usage, MRC Global maintained strong liquidity of $574 million.

The company continued to return cash to shareholders, repurchasing $15 million worth of shares during the quarter. The net working capital to trailing twelve-month sales ratio stood at 14.2%.

The balance sheet strength and financial flexibility are detailed in the following chart:

Strategic Initiatives

The announced combination with DNOW represents a transformative strategic move for MRC Global. The merger is expected to create a larger, more competitive entity in the energy and industrial solutions space, with combined pro forma revenue of $5.3 billion on a trailing twelve-month basis.

The company expects to achieve approximately $70 million in annual cost synergies within three years of closing, which is anticipated in the fourth quarter of 2025. This strategic combination follows a challenging period for MRC Global, which missed earnings expectations in Q1 2025, and appears to be part of a broader strategy to strengthen its market position and improve operational efficiency.

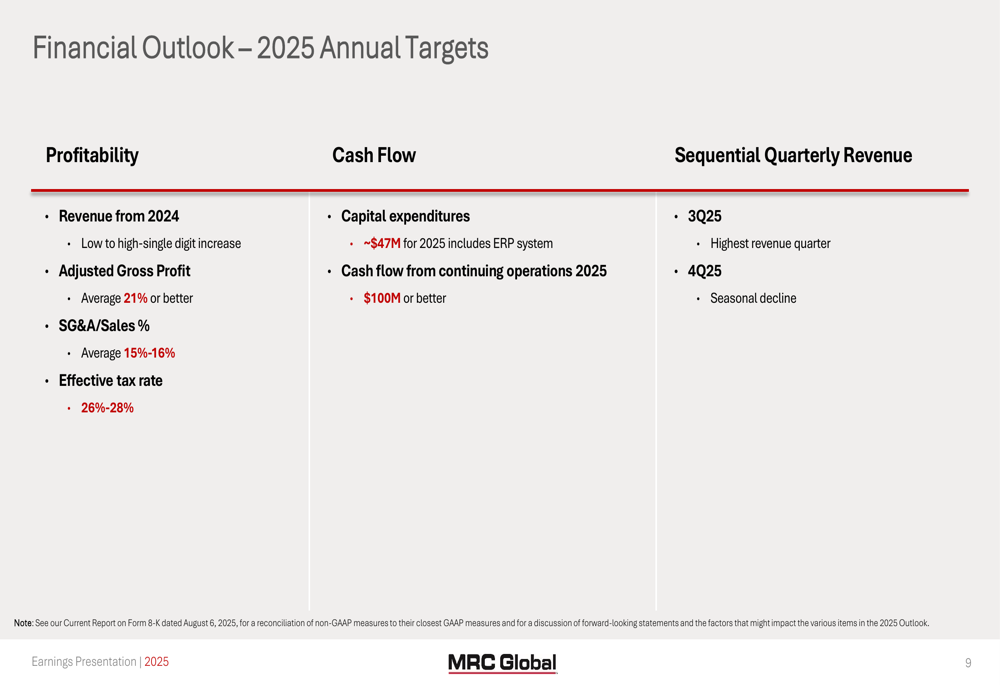

Forward-Looking Statements

Looking ahead, MRC Global provided guidance for the remainder of 2025, expecting low to high single-digit revenue growth compared to 2024. The company anticipates adjusted gross profit margins to average 21% or better, with SG&A as a percentage of sales averaging between 15% and 16%.

For the sequential quarterly outlook, MRC Global expects the third quarter of 2025 to be its highest revenue quarter, followed by a seasonal decline in the fourth quarter. The company projects cash flow from continuing operations for 2025 to be $100 million or better, with capital expenditures of approximately $47 million, including investments in its ERP system.

The financial outlook for 2025 is summarized in the following slide:

Market Reaction

The market appears to be responding positively to MRC Global’s Q2 2025 results and strategic announcements. The stock was up 5.15% in premarket trading to $15.10, building on the previous day’s 2.5% gain that closed at $14.36. This positive reaction suggests investors are encouraged by the sequential improvement in performance and the strategic combination with DNOW.

The stock’s recovery brings it closer to its 52-week high of $15.59, representing a significant rebound from its 52-week low of $9.234. The positive market sentiment indicates confidence in the company’s ability to execute its strategic initiatives and deliver on its financial targets for the remainder of 2025, following the disappointing Q1 results that had previously pressured the stock.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.