Bank of America just raised its EUR/USD forecast

MSA Safety (NYSE:MSA) presented its first quarter 2025 earnings on April 30, showcasing modest growth with some margin pressure while maintaining its annual outlook. The safety equipment manufacturer reported a 4% organic sales increase despite macroeconomic uncertainties, with strong cash flow generation providing financial flexibility.

Quarterly Performance Highlights

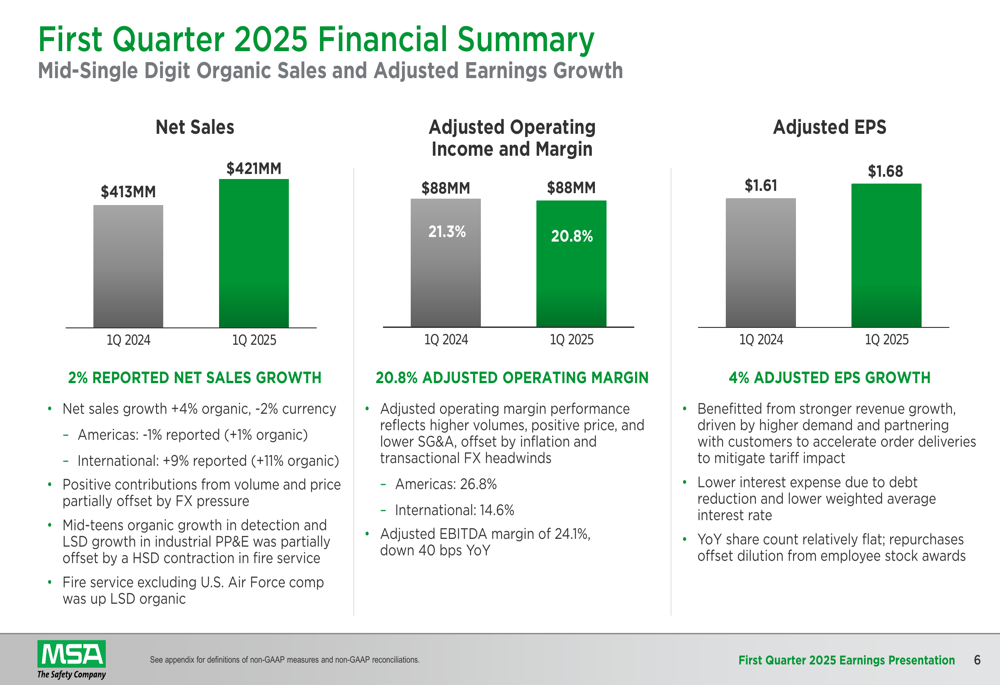

MSA Safety reported net sales of $421 million for the first quarter of 2025, representing a 2% increase on a reported basis and 4% organic growth year-over-year. Adjusted earnings per share reached $1.68, up 4% compared to Q1 2024, while adjusted operating margin contracted slightly to 20.8% from 21.3% in the prior-year period.

"We delivered solid operating performance in the first quarter, demonstrating the resilience of our diverse business model," commented MSA’s management in the presentation materials. The company highlighted a significant win during the quarter, securing a $10 million breathing apparatus contract from Orange County Fire Authority in California.

As shown in the following financial summary chart:

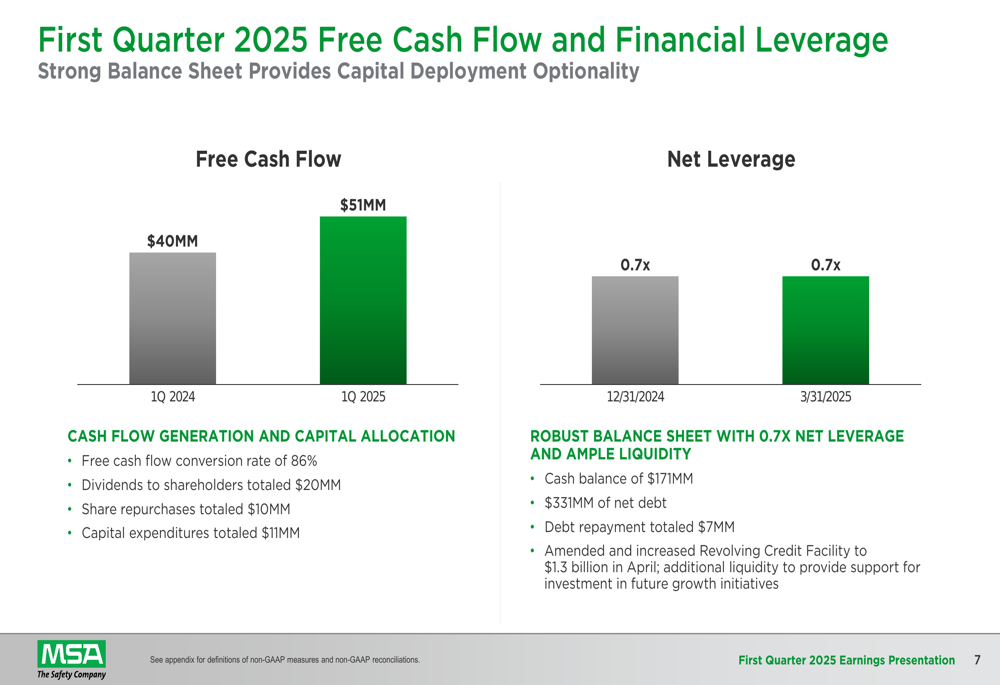

Free cash flow showed notable improvement, increasing to $51 million compared to $40 million in Q1 2024, representing a 27.5% year-over-year increase. The company achieved an 86% free cash flow conversion rate, reflecting efficient working capital management and operational discipline.

The following chart illustrates MSA’s free cash flow performance:

Detailed Financial Analysis

MSA’s financial performance reflects a balance between growth and margin management. The slight contraction in adjusted operating margin (20.8% vs. 21.3% year-over-year) was attributed to gross margin pressure, which was partially offset by SG&A leverage. This suggests the company is navigating inflationary pressures while maintaining cost discipline in other areas.

The company’s balance sheet remains robust with a net leverage ratio of 0.7x, unchanged from December 31, 2024. During the quarter, MSA amended and increased its Revolving Credit Facility to $1.3 billion, enhancing financial flexibility for potential strategic investments and capital allocation priorities.

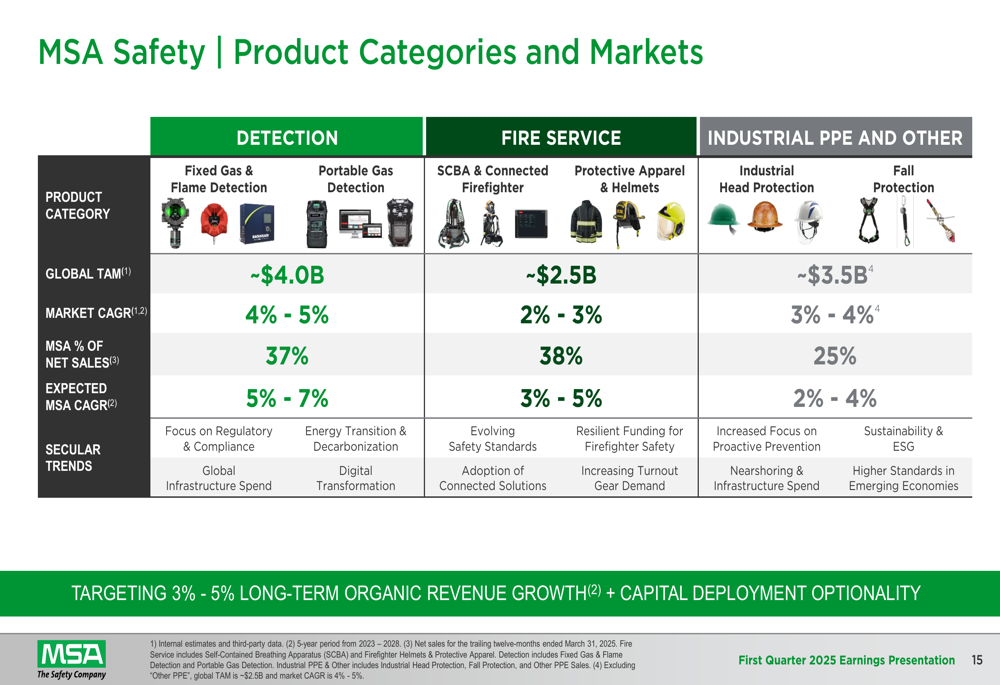

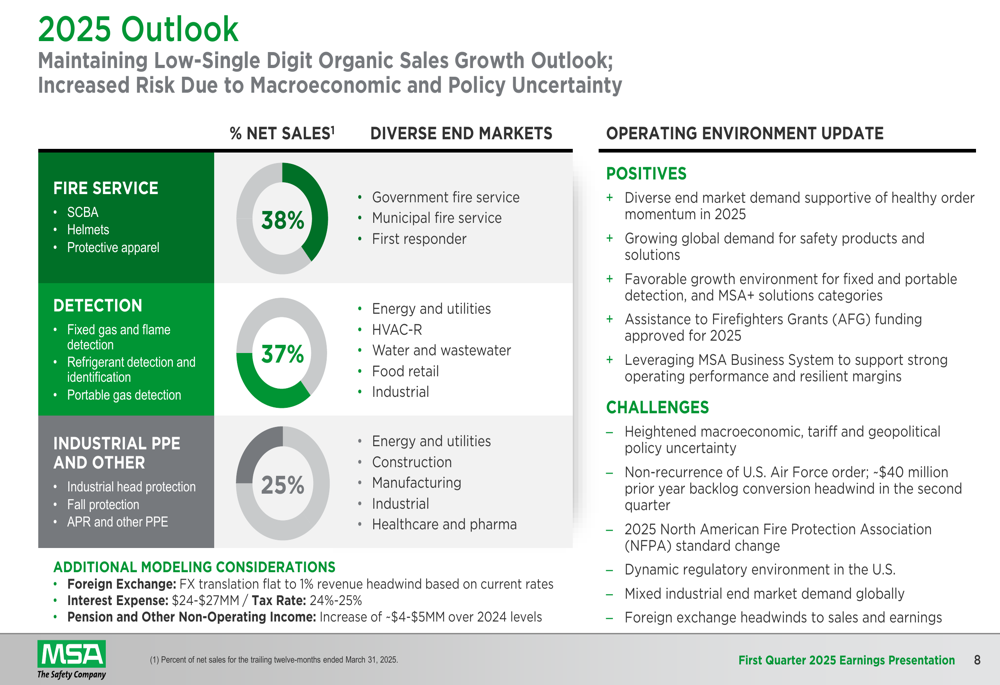

MSA’s product portfolio continues to show diverse performance across segments. The company’s sales are well-balanced across three main categories: Fire Service (38%), Detection (37%), and Industrial PPE and Other (25%), providing resilience against sector-specific downturns.

The following chart breaks down MSA’s product categories and markets:

Strategic Initiatives

MSA’s strategic actions during the quarter focused on three key areas: Safety Leadership and Growth, Commercial and Operational Excellence, and Capital Allocation. The company highlighted enhancements to its G1™ SCBA Platform and Globe turnout jacket at the FDIC (Fire Department Instructors Conference), while also noting mid-teens growth in its detection business.

In response to ongoing trade challenges, MSA reported active tariff mitigation efforts and selective price increases as part of its commercial excellence initiatives. These actions align with the company’s broader "Accelerate" strategy, which emphasizes leadership in premium safety solutions, targeted growth accelerators, operational excellence through the MSA Business System, and effective capital allocation.

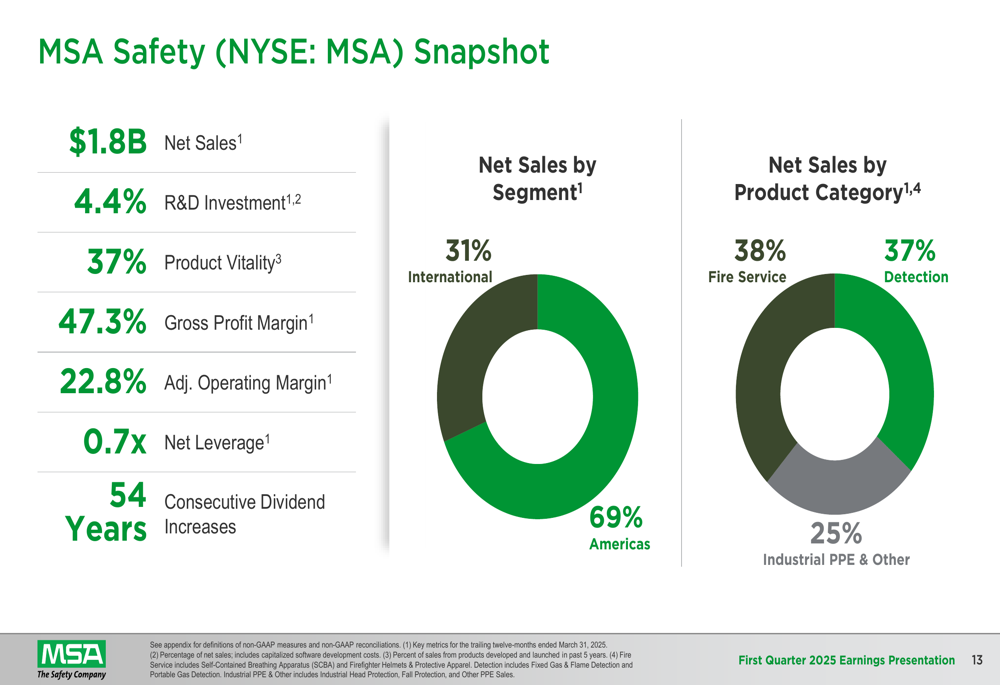

The company’s long-term snapshot reveals its market position and financial profile:

MSA continues to invest in research and development, with R&D investment at 4.4% of sales, supporting a product vitality rate of 37% (percentage of sales from products introduced within the past five years). This innovation focus is central to the company’s competitive positioning in the safety equipment market.

Forward-Looking Statements

Looking ahead, MSA maintained its outlook for low-single-digit organic sales growth in 2025, though management noted increased risk due to macroeconomic and policy uncertainty. The company identified several positive factors in its operating environment, including fire service demand, detection growth, and emerging market opportunities, balanced against challenges such as industrial market softness and project timing uncertainties.

The following slide details MSA’s 2025 outlook:

Beyond 2025, MSA outlined ambitious 2028 financial targets, including:

- Revenue growth to $2.1-$2.3 billion

- Operating margin expansion to 23.5%-25.0%

- EPS growth to $10.00-$11.00

- Capital deployment optionality exceeding $1.5 billion

These targets are visualized in the following chart:

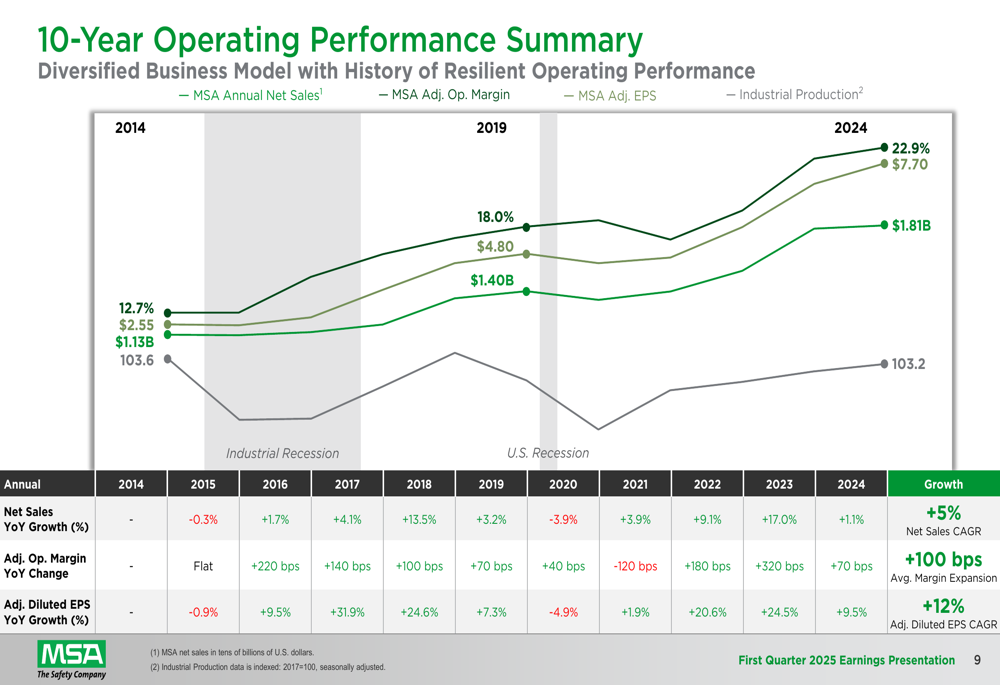

MSA’s 10-year performance track record provides context for these forward-looking targets, showing a consistent history of growth and margin expansion. Over the past decade, the company has achieved a 5% net sales CAGR, 100 basis points of average margin expansion, and a 12% adjusted diluted EPS CAGR, demonstrating resilience through various industrial cycles.

The company’s stock closed at $154.26 on April 29, 2025, representing a 1.09% increase on the day. This places the stock above its 52-week low of $127.86 but still well below its 52-week high of $200.61, suggesting potential upside if the company executes on its strategic initiatives and growth targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.