Stock market today: S&P 500 falls as job cuts stoke economic fears, tech stutters

Introduction & Market Context

Munters Group AB (STO:MTRS), a global leader in energy-efficient air treatment and climate solutions, presented its Q2 2025 results on July 18, 2025, revealing strong order intake growth despite facing margin pressure. The company’s stock, trading at 113.6 SEK, experienced a slight decline of 0.35% following the release, suggesting mixed market reactions to the results.

The quarter showcased regional divergence in performance, with the Americas driving significant growth in the Data Center Technologies (DCT) segment, while the battery segment faced continued headwinds amid a challenging global environment. Despite these challenges, Munters continued to execute on its strategic initiatives, including facility expansion and sustainability advancements.

As shown in the following quarterly performance overview:

Quarterly Performance Highlights

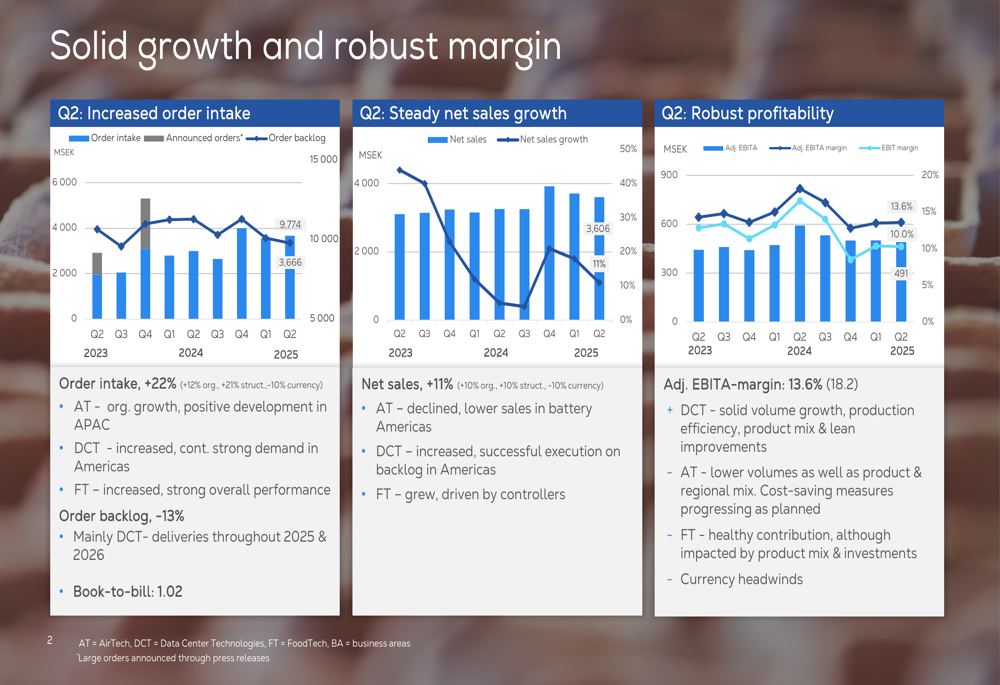

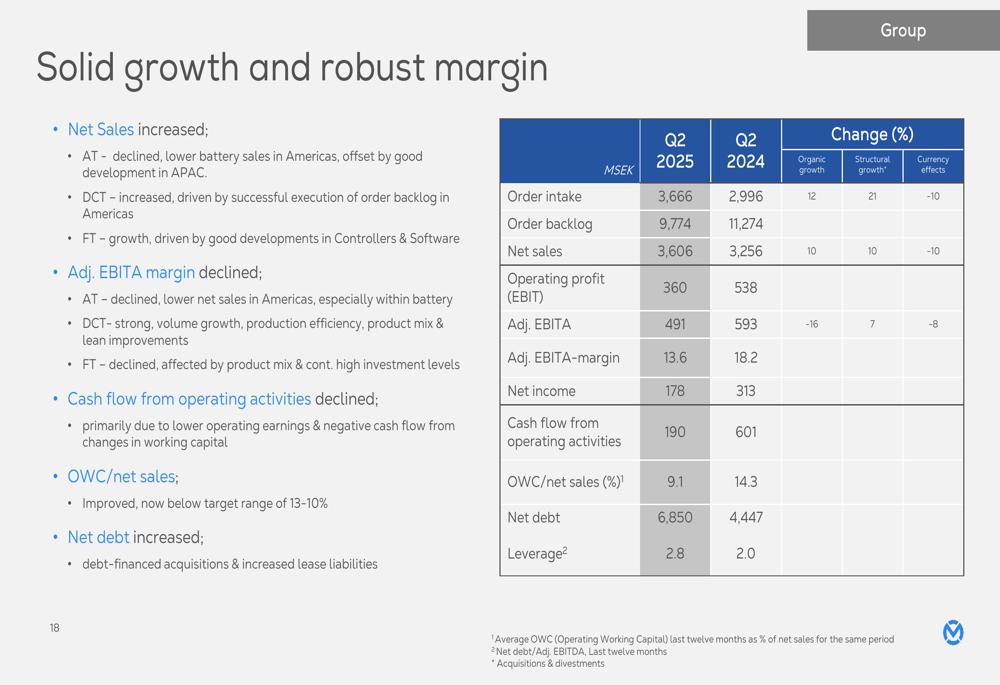

Munters reported substantial growth in Q2 2025, with order intake increasing by 22% (12% organic, 21% structural, -10% currency) to 3,666 MSEK compared to 2,996 MSEK in Q2 2024. Net sales grew by 11% (10% organic, 10% structural, -10% currency) to 3,606 MSEK, demonstrating the company’s ability to execute on its backlog despite challenging market conditions.

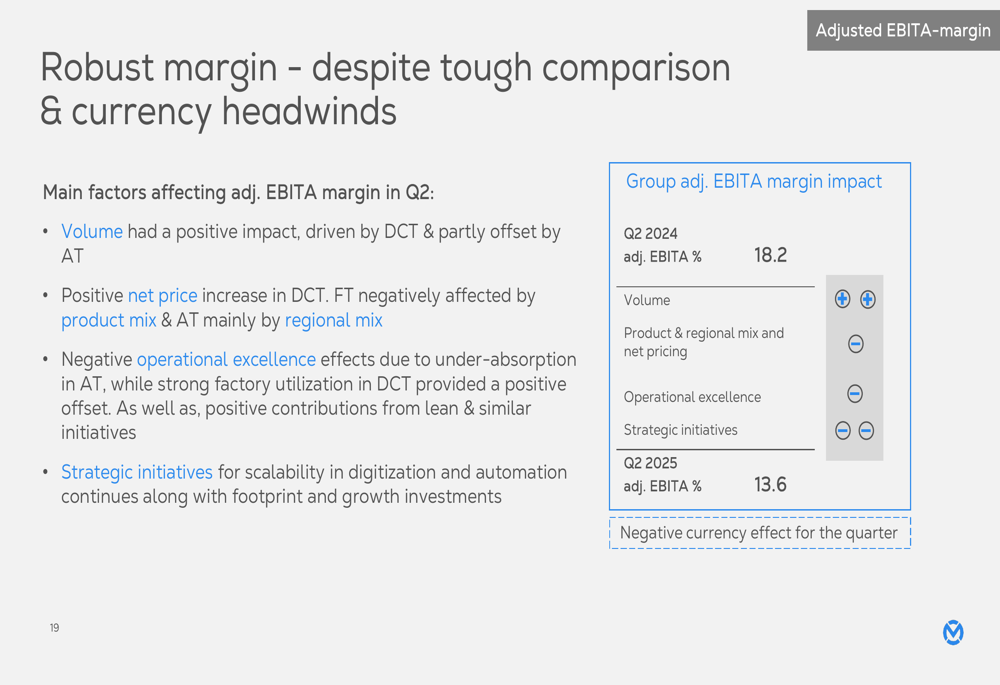

However, profitability metrics showed pressure, with adjusted EBITA margin declining to 13.6% from 18.2% in the previous year. The company attributed this decline to lower sales in Americas, particularly within the battery segment, unfavorable product and regional mix, and ongoing investments in manufacturing footprint.

The comprehensive financial performance is illustrated in the following group overview:

Cash flow from operating activities declined, primarily due to lower operating earnings and negative cash flow from changes in working capital. Despite these challenges, Munters maintained a book-to-bill ratio of 1.02, indicating continued demand for its products and solutions.

The company’s margin development was impacted by several factors, as shown in this breakdown:

Segment Analysis

AirTech

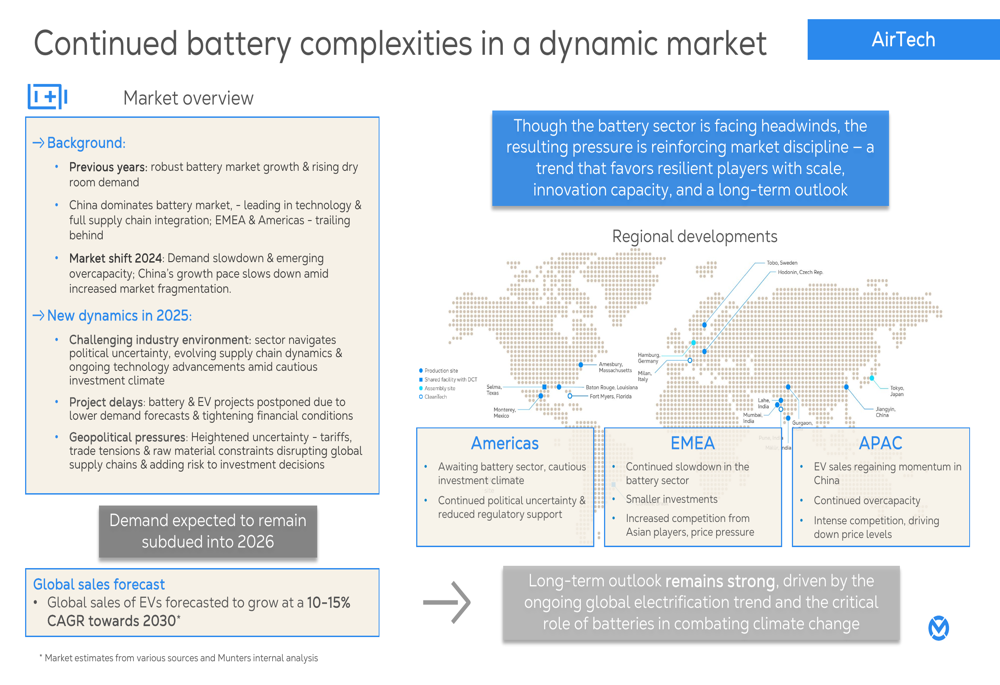

The AirTech segment faced challenges in Q2 2025, with lower battery sales in Americas partially offset by positive development in APAC. The segment experienced uncertainty in Americas, mixed market sentiment in EMEA, and signs of improvement in China despite continued high competition.

Munters highlighted the complexities in the battery market, noting that demand is expected to remain subdued into 2026, although global sales of EVs are forecasted to grow at a 10-15% CAGR towards 2030. The company is implementing margin-enhancing actions to address these challenges.

The battery market dynamics are illustrated in the following slide:

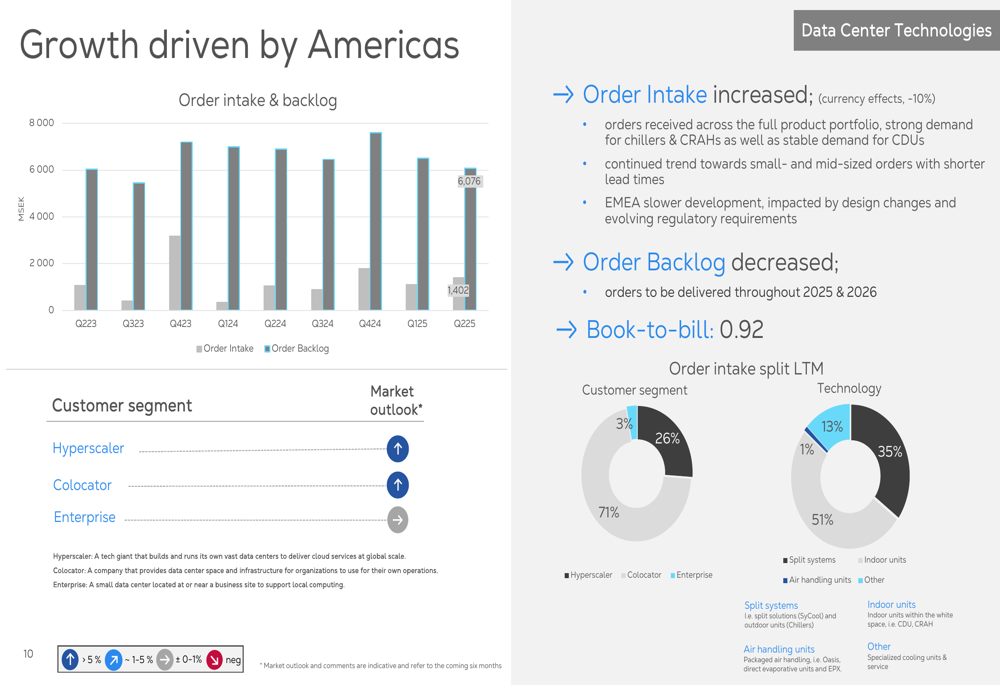

Data Center Technologies (DCT)

The DCT segment emerged as a strong performer in Q2 2025, driven primarily by the Americas region. Order intake increased with orders received across the full product portfolio, particularly strong demand for chillers and CRAHs as well as stable demand for CDUs. Net sales increased due to successful execution of backlog in Americas and demand for chillers, supported by the Geoclima acquisition.

The segment’s customer base consists primarily of hyperscalers (71%) and colocators (26%), with a strong order backlog to be delivered throughout 2025 and 2026. The regional distribution of DCT’s growth is shown here:

Adjusted EBITA margin for DCT remained strong, supported by solid volume growth with high production utilization, favorable product mix, and benefits from lean initiatives. The company is also expanding its chiller offering to unlock regional growth, with US chiller production set to begin in 2026.

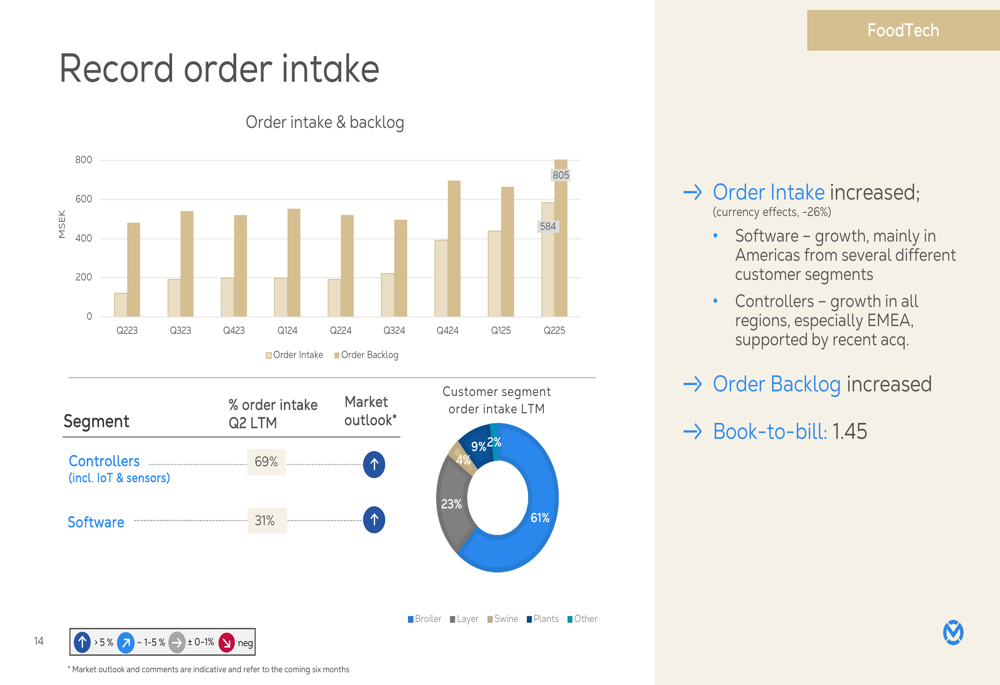

FoodTech

FoodTech reported record order intake in Q2 2025, with growth across all regions, particularly in controllers in EMEA. The segment achieved a book-to-bill ratio of 1.45, indicating strong future revenue potential. Software solutions grew mainly in Americas from several different customer segments, while controllers saw growth in all regions, especially EMEA, supported by recent acquisitions.

The record performance of FoodTech’s order intake is illustrated here:

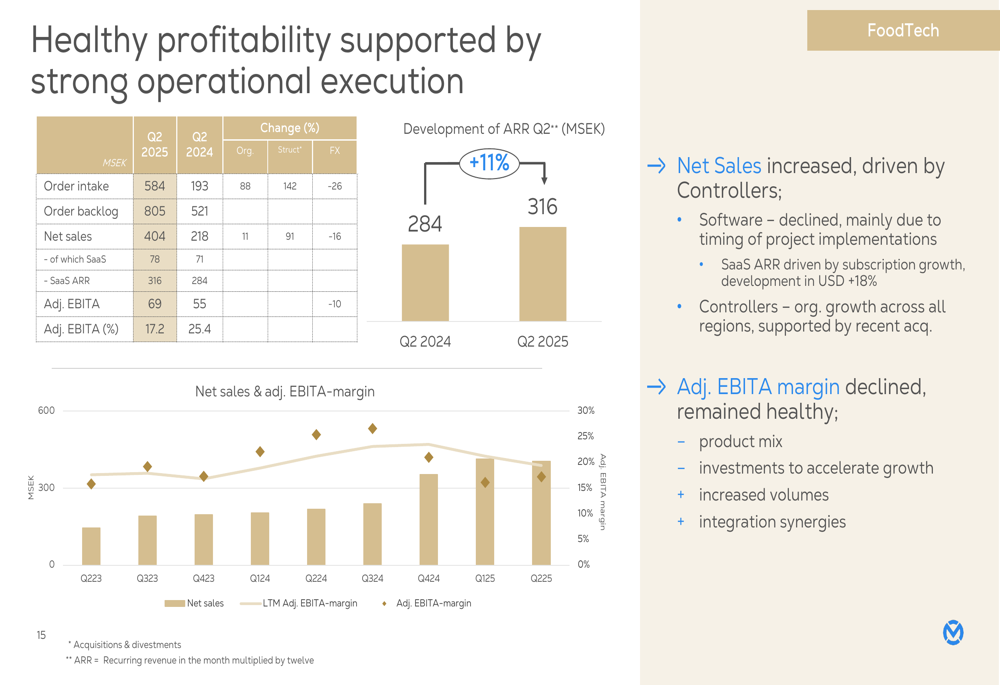

Net sales increased, driven by controllers, although software declined mainly due to timing of project implementations. Adjusted EBITA margin declined but remained healthy, affected by product mix and investments to accelerate growth. The segment’s profitability is shown in the following chart:

Strategic Initiatives and Investments

Munters continued to invest in strategic initiatives to support future growth. A key highlight was the inauguration of the new Amesbury site, which is now the largest Munters facility globally with over 40,000 m² of advanced manufacturing space. The facility will streamline operations, house production for AirTech’s full offering, and features sustainable elements including a fully electric operation and rooftop solar array.

The company also secured its first large-scale order in the growing Direct Air Capture (DAC) technology, enabling removal of CO2 directly from ambient air. This project for a U.S. oil and gas customer aims to capture 500,000 tons of CO2 annually, positioning Munters in the industrial decarbonization market.

In the FoodTech segment, Munters achieved strategic milestones in the layer segment, securing a large-scale order from a major egg producer in China for controllers and signing a SaaS contract including implementation with a leading global egg producer for its software solutions.

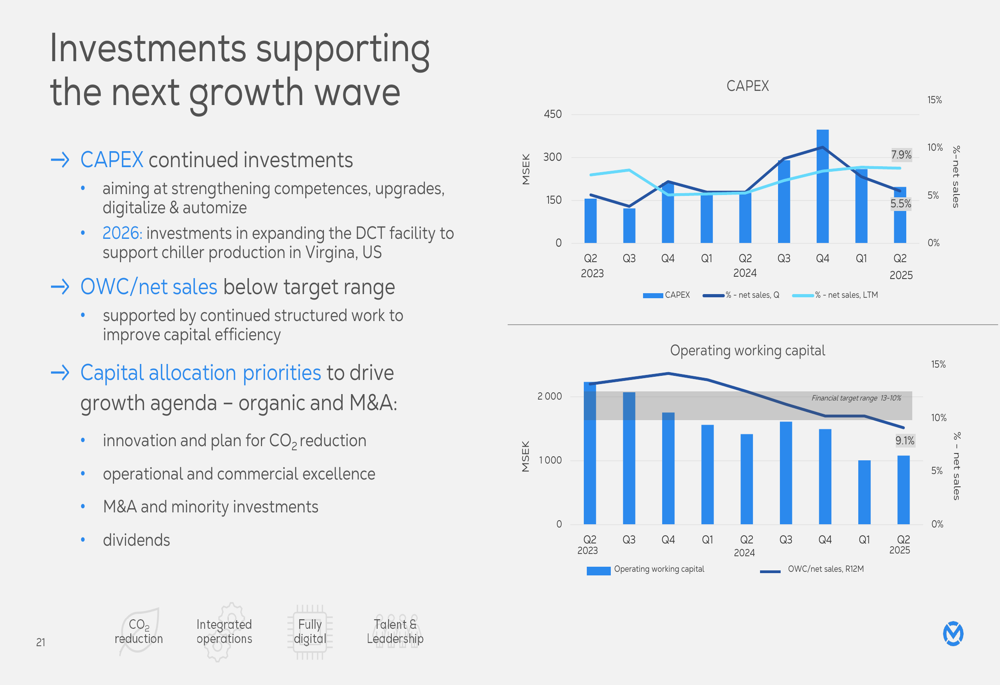

Financial Position and Outlook

Munters maintained a focus on cash management during Q2 2025, although cash flow from changes in working capital declined. The company’s leverage ratio stood at 2.8x, with a diversified funding base. Capital allocation priorities continue to drive the growth agenda, both organically and through M&A activities.

The company’s financial position and capital allocation are shown in the following slide:

Munters established an MTN-program and Green Bond Framework, with the first issuance under the program supporting the goal of diversifying funding sources and advancing sustainable investments. This aligns with the company’s sustainability agenda and 2030 targets.

Looking ahead, Munters remains committed to its financial targets, showing progression in currency-adjusted growth (+21%) despite challenges in maintaining the adjusted EBITA margin (13.6%). The company’s service ambition remains in line with its strategic direction, focusing on growing its large globally installed base, continuous innovation, digital offering with AI controls and connectivity, and energy upgrades and spare parts.

According to CEO Klas Forsström, as quoted in the earnings call transcript, "We are positioned for the next phase of sustainable and profitable growth," highlighting the success of recent mergers and acquisitions. Forsström also emphasized the company’s ambitious goals, stating, "We are closer to a potential of $10 billion than $5 billion."

Despite current challenges, particularly in the battery segment and margin pressure, Munters continues to invest in strategic initiatives aimed at long-term growth, with analysts maintaining a strong buy consensus and setting price targets between $14.13 and $20.93, suggesting potential upside from current levels.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.