Raytheon awarded $71 million in Navy contracts for missile systems

Introduction & Market Context

Murphy Oil Corporation (NYSE:MUR) reported second-quarter production that exceeded the high end of guidance, while continuing to advance its international exploration strategy and return capital to shareholders. The company’s stock closed at $23.85 on August 6, 2025, and moved up 0.63% in after-hours trading following the earnings announcement.

President and CEO Eric M. Hambly presented the company’s Q2 2025 results during a conference call and webcast on August 7, highlighting Murphy’s operational achievements and strategic priorities. The presentation comes after Murphy’s Q1 2025 performance, which saw the company beat EPS expectations with $0.56 against a forecast of $0.48.

Quarterly Performance Highlights

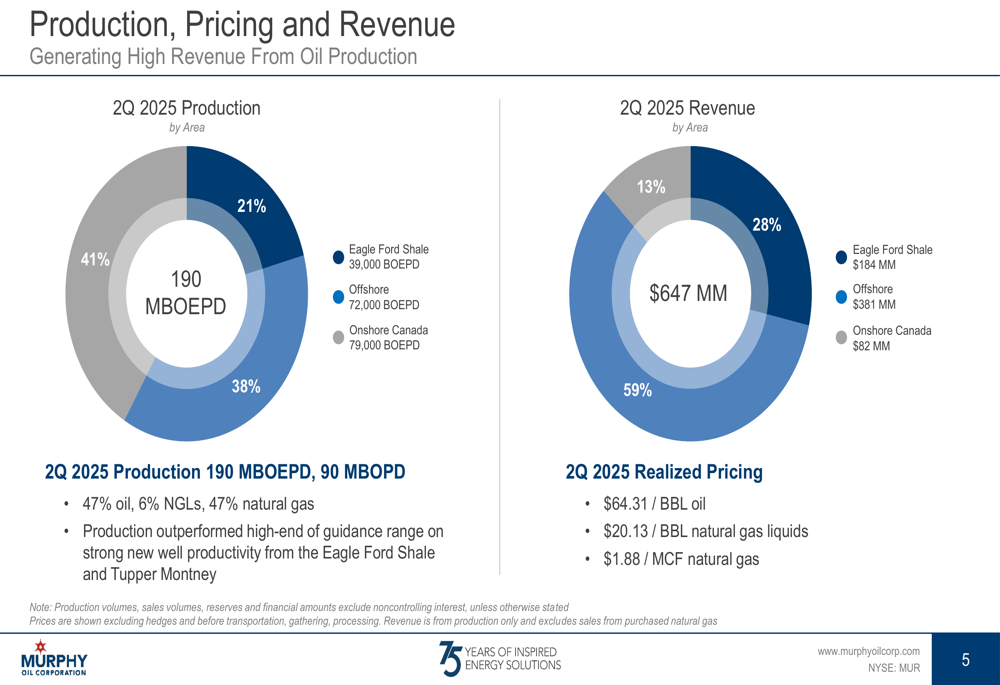

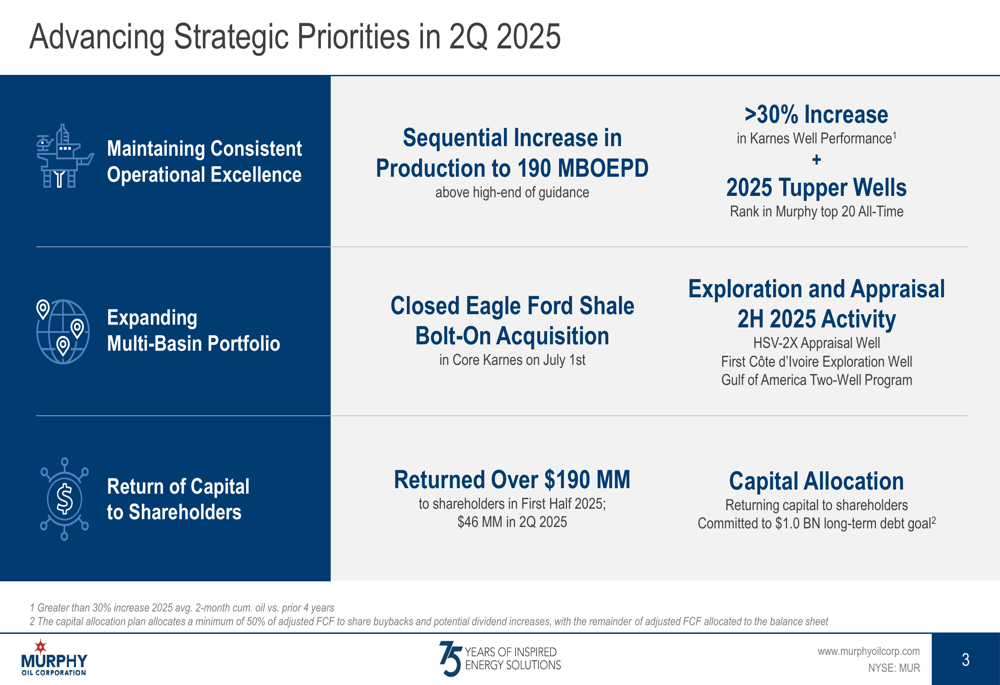

Murphy Oil reported Q2 2025 production of 190 thousand barrels of oil equivalent per day (MBOEPD), exceeding the high end of its guidance range. This represents a significant sequential increase from Q1 2025’s 157 MBOEPD. The production mix consisted of 47% oil, 6% natural gas liquids (NGLs), and 47% natural gas.

The company generated $647 million in revenue during the quarter, with offshore operations contributing the largest portion at $381 million (59%), followed by Eagle Ford Shale at $184 million (28%), and Onshore Canada at $82 million (13%).

As shown in the following breakdown of production, pricing and revenue:

Realized commodity prices for the quarter were $64.31 per barrel for oil, $20.13 per barrel for natural gas liquids, and $1.88 per MCF for natural gas. The company attributed its production outperformance to strong new well productivity from Eagle Ford Shale and Tupper Montney operations.

Strategic Initiatives

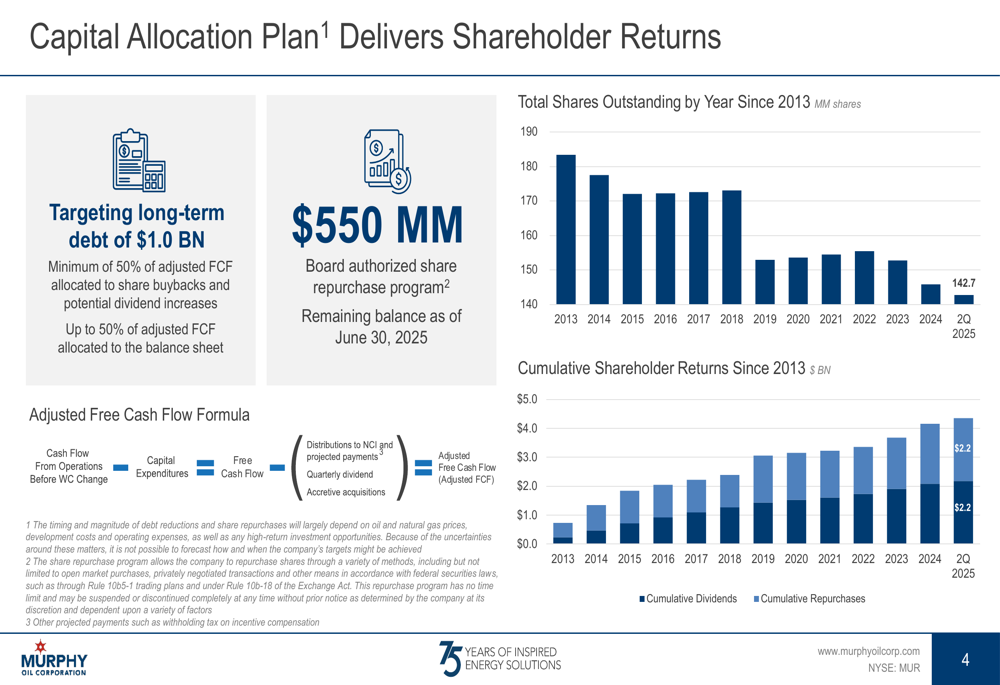

Murphy Oil continues to focus on maintaining a strong balance sheet while returning significant capital to shareholders. The company returned over $190 million to shareholders in the first half of 2025, including $46 million in Q2 alone. Management has committed to allocating at least 50% of adjusted free cash flow to share buybacks and potential dividend increases.

The company’s capital allocation strategy is illustrated in the following slide:

Murphy has reduced its outstanding shares from 174 million in 2013 to 142.7 million in Q2 2025. The company has delivered approximately $3.0 billion in cumulative dividends and around $2.2 billion in cumulative share repurchases since 2013.

On the debt front, Murphy is targeting long-term debt of $1.0 billion, with current debt outstanding at $1.3 billion. The company maintains a conservative financial policy with no near-term debt maturities and a weighted average fixed coupon of 6.10% with 8.9 weighted average years to maturity.

The company has also made significant progress in cost management, achieving greater than $500 million in cumulative G&A savings from 2020 to 2024, and approximately 50% reduction in both G&A per BOE (compared to 2019 baseline) and bond interest expense.

Operational Updates

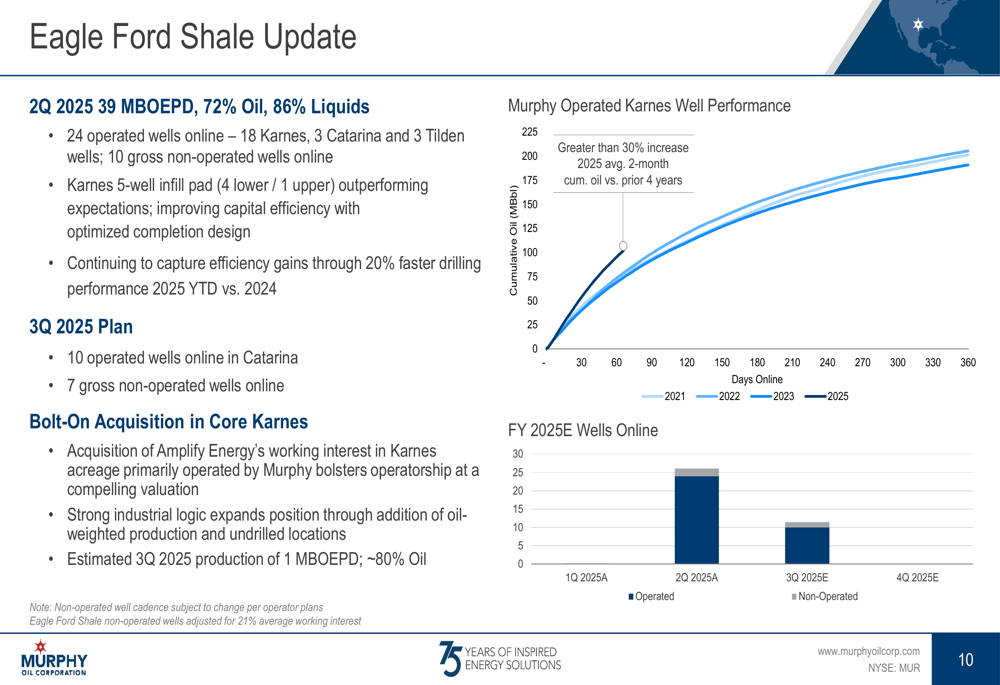

Murphy’s Eagle Ford Shale operations delivered 39 MBOEPD in Q2 2025, with 72% oil and 86% liquids content. The company brought 24 operated wells online during the quarter, including 18 in Karnes, 3 in Catarina, and 3 in Tilden. A Karnes 5-well infill pad is outperforming expectations.

The company closed a bolt-on acquisition of Amplify Energy (NYSE:AMPY)’s working interest in Karnes acreage on July 1st, which is expected to contribute approximately 1 MBOEPD (80% oil) in Q3 2025.

The following slide shows the strong performance of Murphy’s Karnes wells:

In Canada, Murphy’s onshore operations produced 79 MBOEPD in Q2 2025, with 96% natural gas content. The company brought 5 operated wells online and completed its 2025 well program. Tupper Montney reached plant capacity driven by strong new well productivity. Murphy achieved a realized price of $1.65/MCF compared to the $1.21/MCF AECO average, demonstrating effective price diversification.

Offshore operations contributed 72 MBOEPD (82% oil) in Q2 2025, with 66 MBOEPD from the Gulf of America (80% oil) and 6 MBOEPD from offshore Canada (100% oil). The company completed the Samurai #3 and Khaleesi #2 workovers and is progressing with the Marmalard #3 workover.

Exploration Activities

Murphy Oil continues to advance its exploration strategy, with a focus on international opportunities. The company’s strategic priorities for Q2 2025 include:

In Vietnam, the Hai Su Vang-1X (Golden Sea Lion) discovery encountered 370 feet of net oil pay with a gross resource potential estimated at 170-430 million barrels of oil equivalent (MMBOE). The company plans to spud the Hai Su Vang-2X appraisal well in September.

Murphy is also progressing with the Lac Da Vang (Golden Camel) Field Development Project in Vietnam, where it holds a 40% operated interest. The project has an estimated gross recoverable resource of 100 MMBOE and a capital budget of $110 million for FY 2025. Key milestones include FSO installation expected for Q1 2025, LDV-A platform jacket installation in Q4 2025, and development drilling planned for Q4 2025.

In Côte d’Ivoire, Murphy is targeting the Civette prospect (Block CI-502) for Q4 2025, with gross resource potential estimated between 440 MMBOE and 1,000 MMBOE. The company has secured the Transocean (NYSE:RIG) Deepwater Skyros rig at a rate of $361,000 per day for this exploration activity.

In the Gulf of America, Murphy plans to spud the Cello #1 well in September (40% Murphy operated, $18 million budget) and the Banjo #1 well in early Q4 2025 (40% Murphy operated).

Forward-Looking Statements

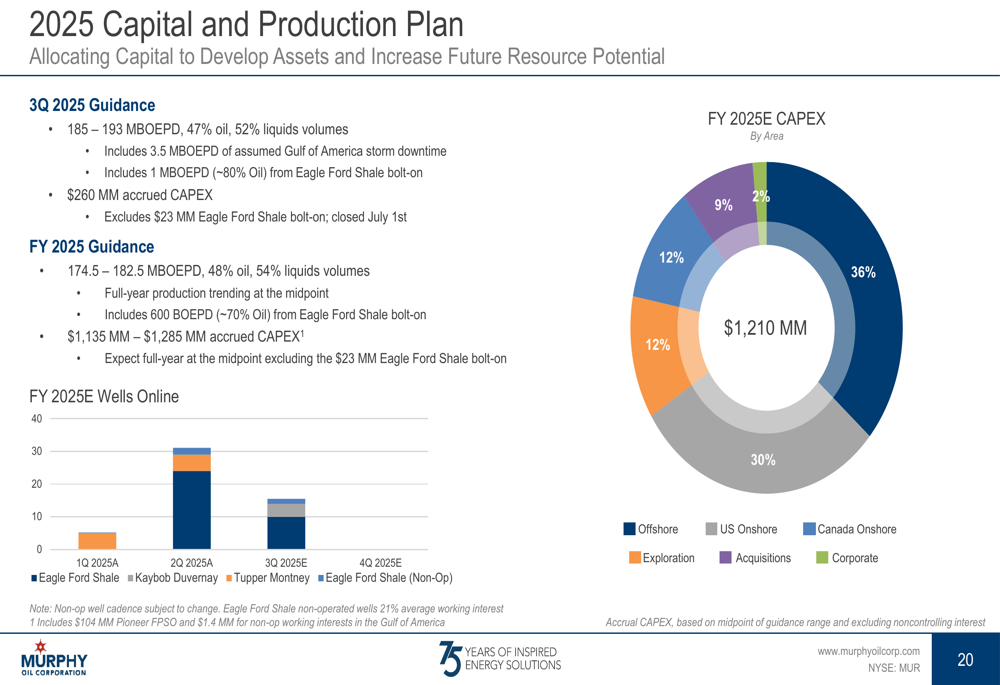

For Q3 2025, Murphy Oil provided production guidance of 185-193 MBOEPD with capital expenditures of $260 million. The company expects full-year 2025 production to average between 174.5 and 182.5 MBOEPD, with 54% liquids content. Full-year capital expenditures are projected at $1,135-$1,285 million.

The following slide outlines the company’s capital and production plan for 2025:

Murphy’s near-term strategy focuses on maintaining modest production by generating low-cost, high-return, and oil-weighted projects. The company is progressing high-margin projects, with Lac Da Vang targeting first oil and continued appraisal of Hai Su Vang.

For the long term, Murphy is prioritizing offshore operations while maintaining well-invested and well-positioned assets in North America. The company is targeting around 15% of annual capital expenditures for exploration activities, with a focus on international opportunities.

Given the company’s strong operational performance in Q2, exceeding production guidance while maintaining its commitment to shareholder returns and debt reduction, Murphy Oil appears well-positioned to execute its strategic priorities for the remainder of 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.