Street Calls of the Week

Introduction & Market Context

Musti Group (HE:MUSTI), the leading Nordic pet care retailer, released its Q1 2025 interim report on May 21, 2025, showing strong sales growth but declining profitability amid challenging consumer conditions. The company’s stock closed at 22.2 on May 20, up 2.54% ahead of the earnings release, reflecting positive market sentiment despite ongoing economic headwinds.

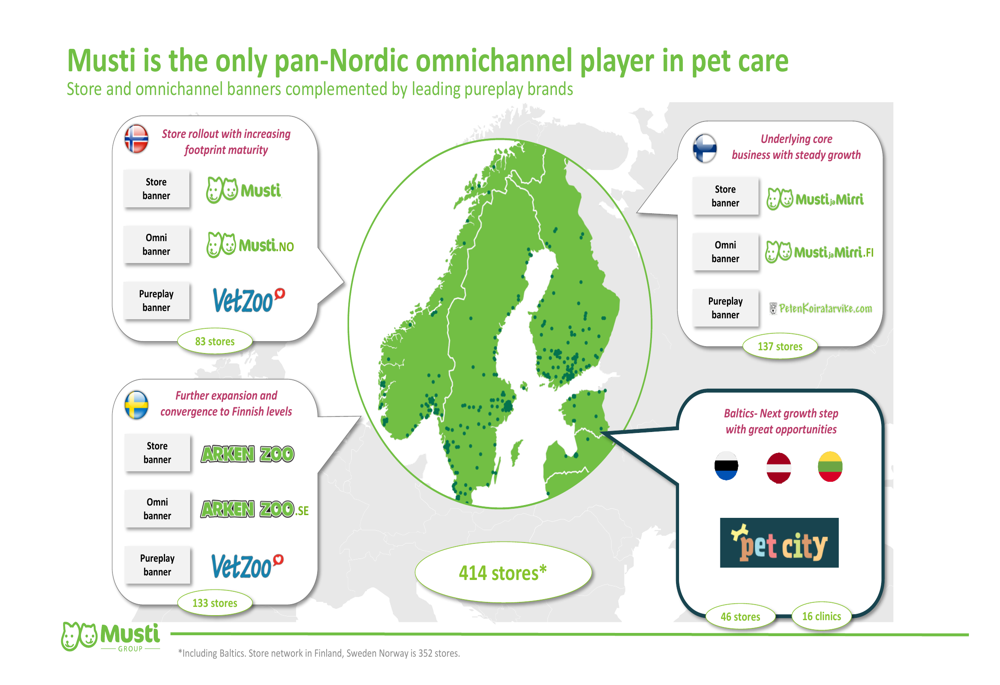

The pan-Nordic pet specialist continues to expand its footprint, now operating 414 stores across Finland, Sweden, Norway, and new markets, reinforcing its position as the dominant omnichannel pet care retailer in the region.

As shown in the following image detailing Musti’s Nordic presence, the company operates under multiple banners including Musti, Musti ja Mirri, Arken Zoo, and Pet City:

Quarterly Performance Highlights

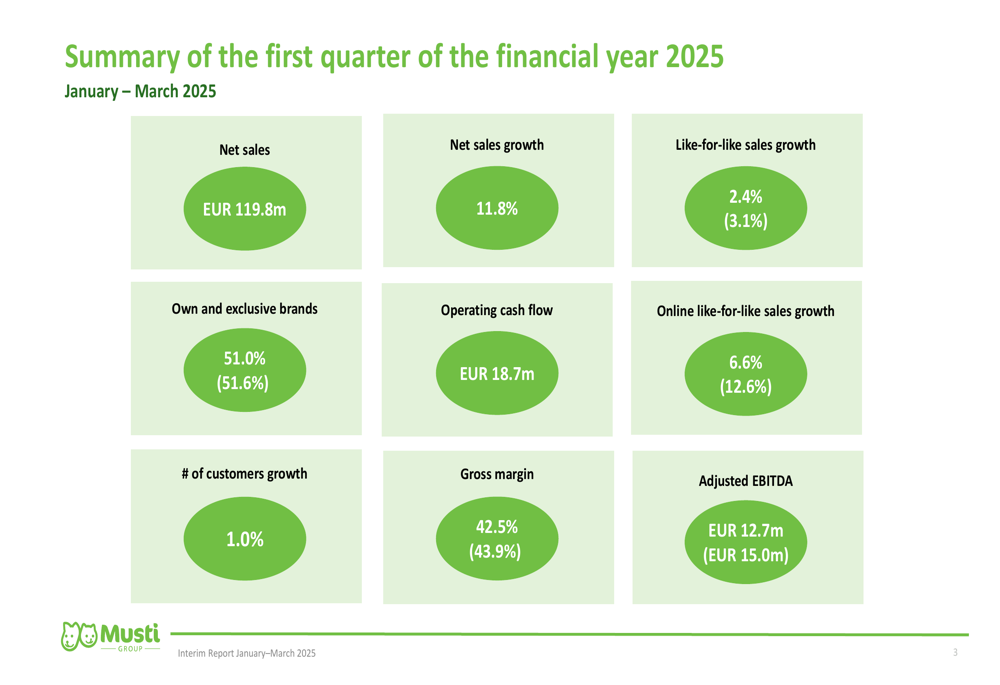

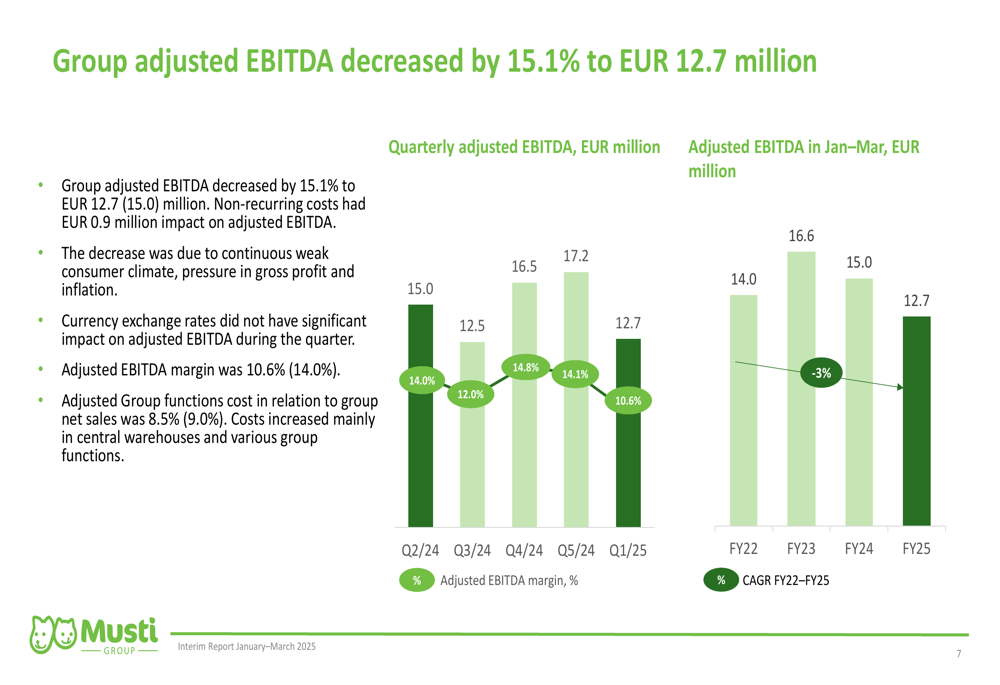

Musti Group reported net sales of EUR 119.8 million for Q1 2025, representing an impressive 11.8% year-over-year increase. However, profitability metrics showed concerning declines, with adjusted EBITDA falling 15.1% to EUR 12.7 million and adjusted EBITDA margin contracting to 10.6% from 14.0% in the same period last year.

The company cited a "continuous weak consumer climate, pressure in gross profit and inflation" as key factors behind the profitability challenges, despite the strong top-line growth.

The following financial summary highlights the key metrics for the quarter:

Like-for-like sales growth was modest at 2.4%, down from 3.1% in the previous year, while online like-for-like sales showed stronger momentum at 6.6%, though this also represented a significant deceleration from the 12.6% growth recorded a year earlier. Customer growth was minimal at just 1.0%, suggesting the company is primarily driving revenue increases through higher spending per customer rather than expanding its customer base.

Detailed Financial Analysis

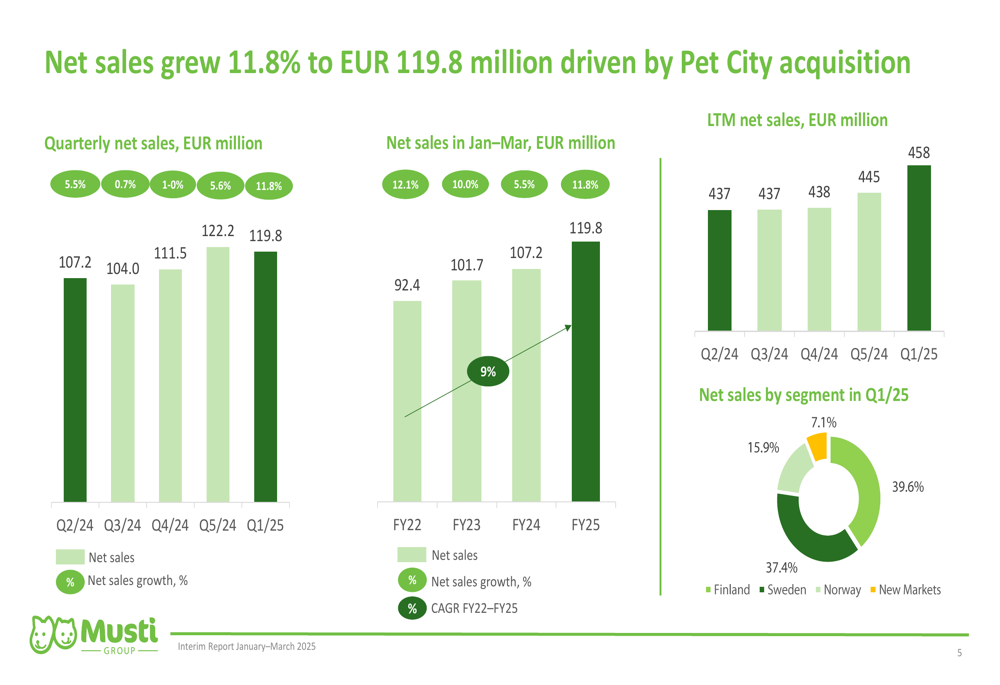

Musti’s net sales have shown consistent growth over recent years, with a compound annual growth rate (CAGR) of 9% from FY22 to FY25. The quarterly trend reveals accelerating growth in the most recent quarter after several periods of more modest expansion.

The following chart illustrates Musti’s net sales growth trajectory and segmentation:

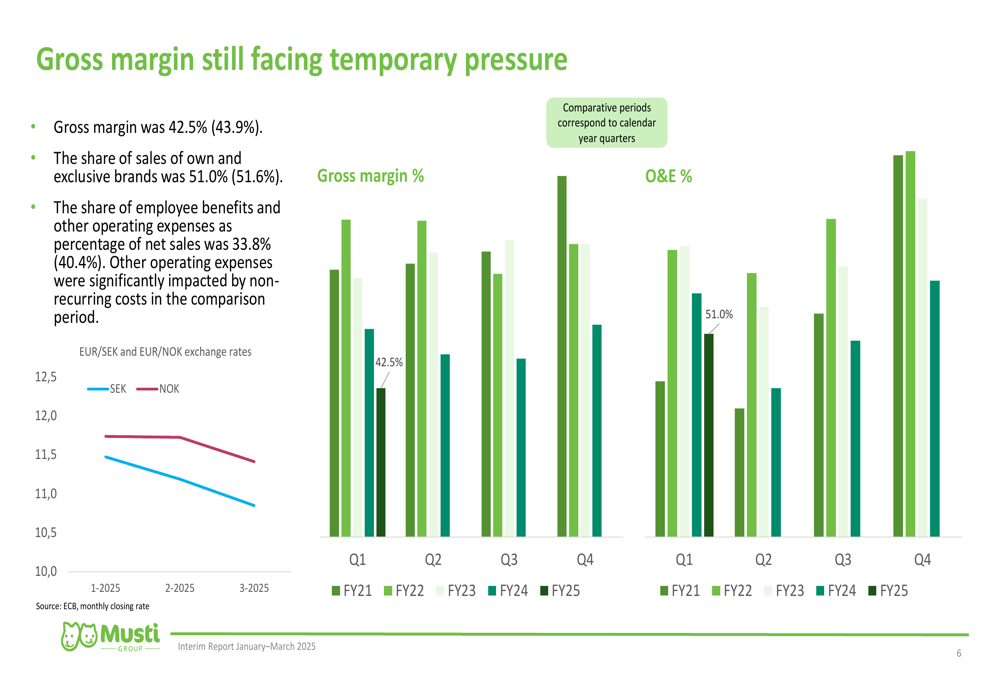

Gross margin contracted to 42.5% from 43.9% in the prior year, reflecting pricing pressures and inflationary impacts on costs. The company’s own and exclusive brands accounted for 51.0% of sales, slightly down from 51.6% a year earlier, which may have contributed to the margin compression as these products typically carry higher margins.

Operating expenses as a percentage of net sales improved to 33.8% from 40.4%, indicating some success in cost control initiatives despite the inflationary environment.

The following chart shows the gross margin and operating expense trends:

Adjusted EBITDA performance has been more concerning, with a negative CAGR of -3% from FY22 to FY25. The Q1 2025 adjusted EBITDA of EUR 12.7 million represents a 15.1% decline from the previous year, with margin compression to 10.6% from 14.0%.

The following chart illustrates the adjusted EBITDA performance:

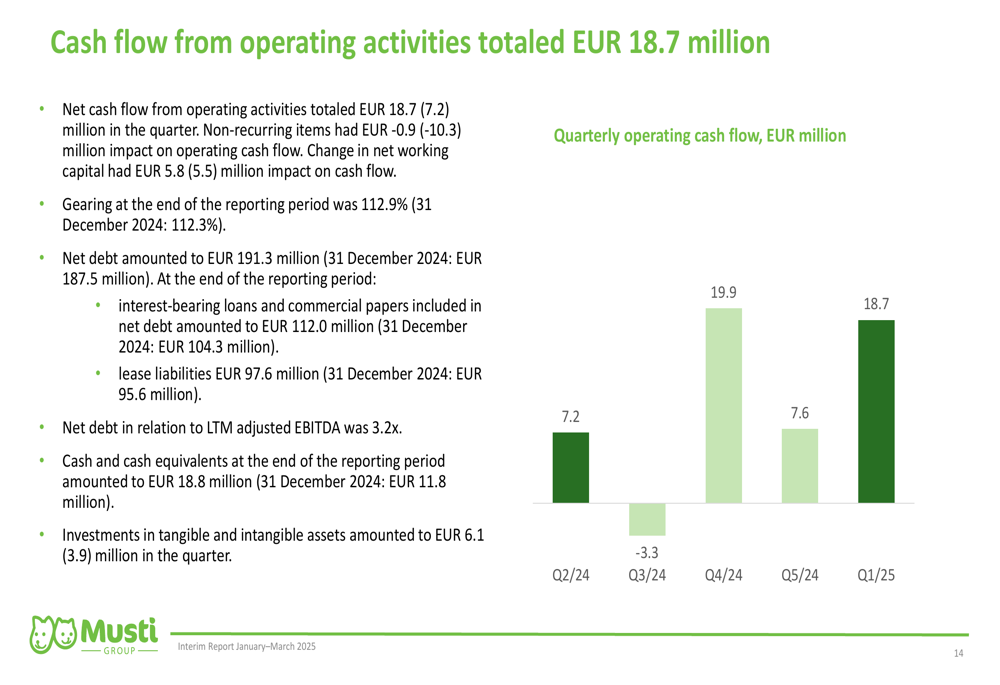

On a positive note, operating cash flow remained strong at EUR 18.7 million, indicating that despite profitability challenges, the company continues to generate healthy cash flows. The company’s net debt stood at EUR 191.3 million with a gearing ratio of 112.9%.

The following chart shows the quarterly operating cash flow:

Segment Performance

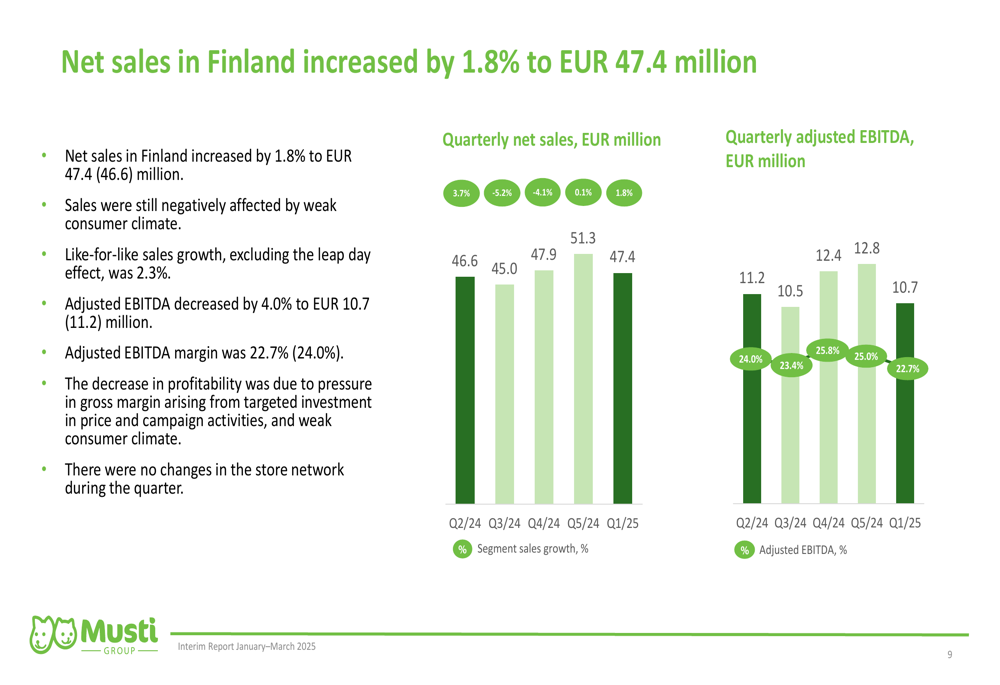

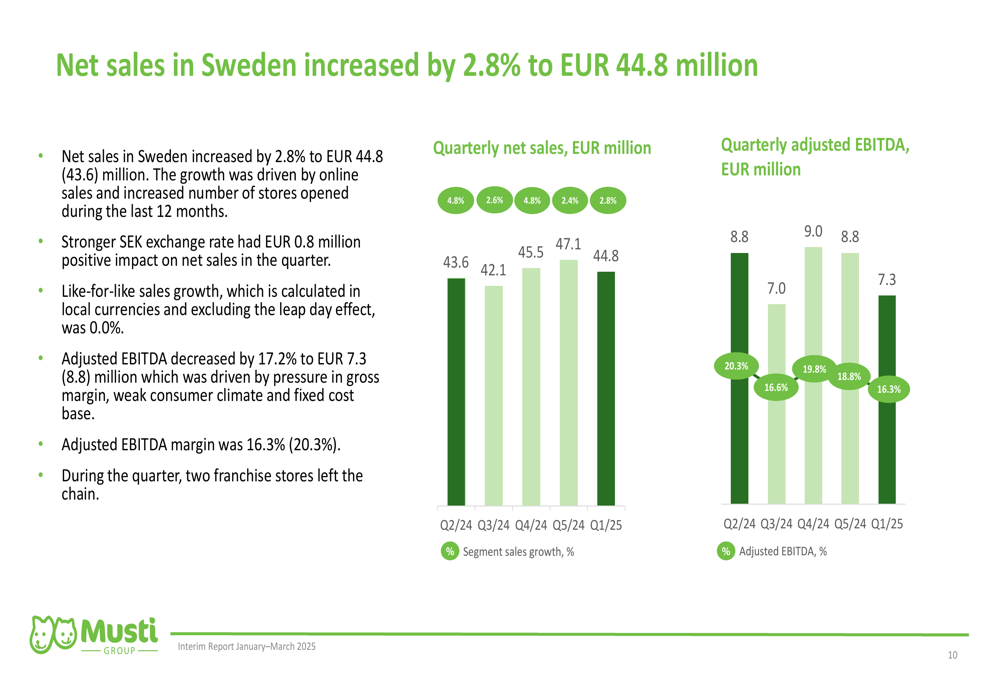

Musti Group’s performance varied significantly across its geographic segments, with Norway showing the strongest growth while Finland and Sweden faced greater profitability challenges.

Finland, the company’s most mature market, saw modest net sales growth of 1.8% to EUR 47.4 million, with like-for-like sales growth of 2.3%. Adjusted EBITDA decreased by 4.0% to EUR 10.7 million, though the segment still maintains the highest profitability with a 22.7% adjusted EBITDA margin.

Sweden reported net sales growth of 2.8% to EUR 44.8 million, with flat like-for-like sales (0.0%). The segment experienced a substantial 17.2% decline in adjusted EBITDA to EUR 7.3 million, with margin compression to 16.3% from 19.7% in the previous year.

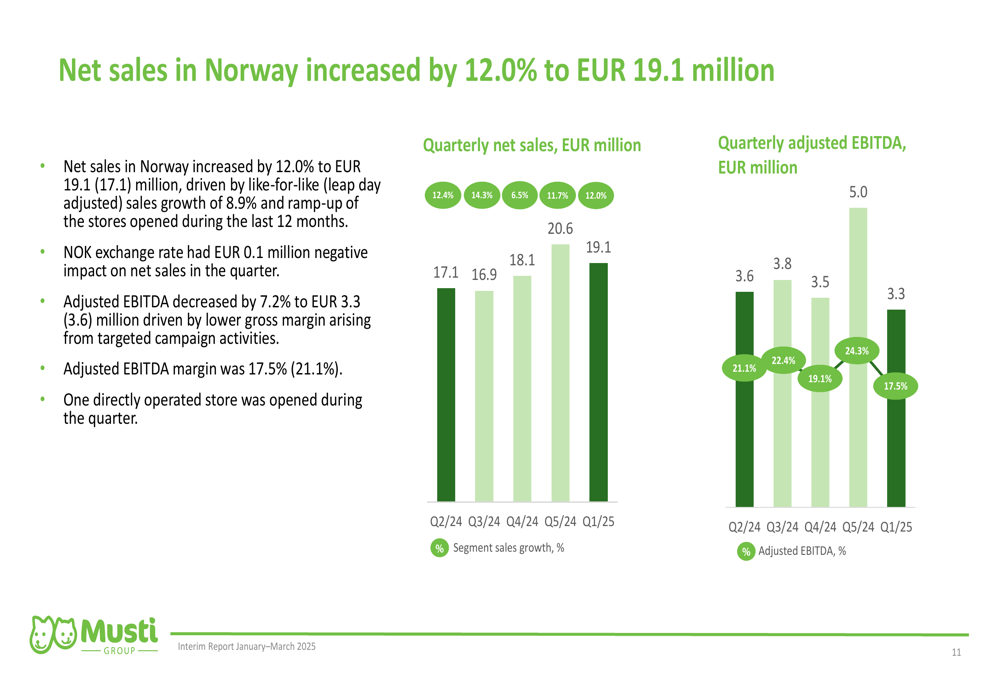

Norway emerged as the strongest performing segment, with net sales increasing 12.0% to EUR 19.1 million. However, even this growth market saw adjusted EBITDA decline by 7.2% to EUR 3.3 million, with margins contracting to 17.5% from 21.1% a year earlier.

The New Markets segment, which includes the Pet City acquisition completed in November 2024, contributed EUR 8.5 million in net sales with an adjusted EBITDA of EUR 0.5 million and a margin of 5.6%. This segment represents a significant growth opportunity but currently operates at lower margins than the established Nordic markets.

Forward-Looking Statements

Musti Group provided limited forward guidance in the presentation, focusing primarily on historical performance. The company did announce that its Half-Year Financial Report for January-June 2025 will be published on July 28, 2025.

The company’s Q1 results suggest a challenging operating environment with strong top-line growth but significant margin pressures. While Musti continues to expand its store network and grow sales, the declining profitability metrics will likely be a key focus for investors in the coming quarters.

The Pet City acquisition appears to be contributing to overall growth but at lower margins than the core business. The company’s ability to improve profitability while maintaining sales momentum will be crucial for future performance, particularly given the weak consumer climate and ongoing inflationary pressures mentioned in the presentation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.