Street Calls of the Week

Introduction & Market Context

Musti Group (HE:MUSTI), the leading pan-Nordic pet care retailer, reported strong second-quarter results for fiscal year 2025, with total sales increasing by 17% year-over-year to EUR 121.7 million. The company’s stock responded positively to the earnings announcement, rising 1.49% to EUR 20.50, though still trading closer to its 52-week low of EUR 19.12 than its high of EUR 27.25.

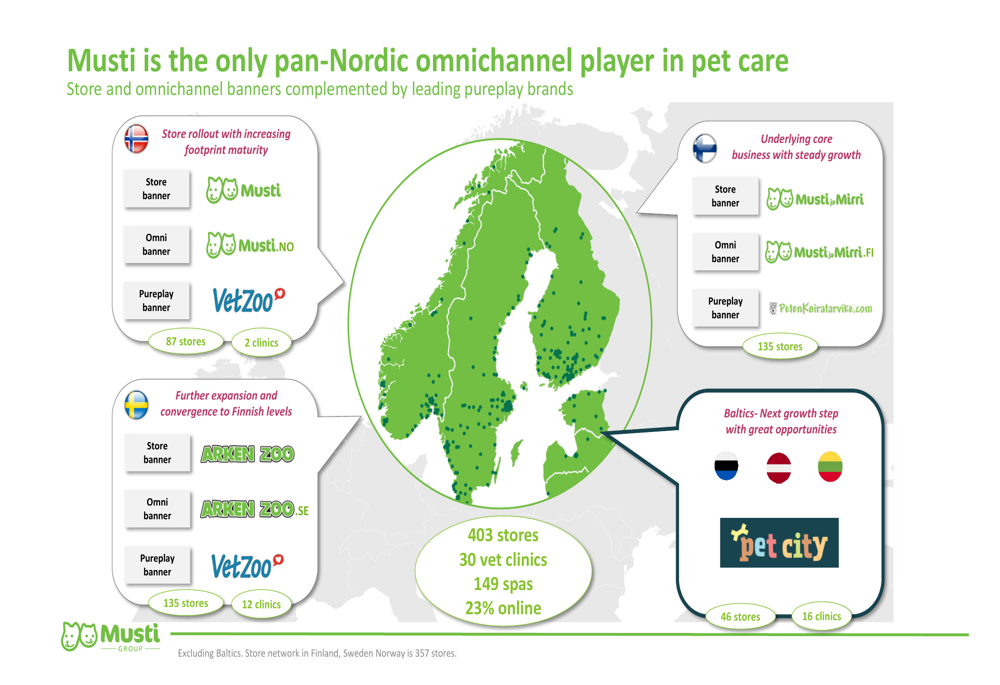

The pet care specialist continues to strengthen its position as the only pan-Nordic omnichannel player in the industry, operating a network of 403 stores complemented by 30 veterinary clinics and 149 pet spas across Finland, Sweden, Norway, and the Baltics. The company’s omnichannel strategy remains robust with online sales accounting for 23% of total revenue.

As shown in the following image detailing Musti’s pan-Nordic presence:

Quarterly Performance Highlights

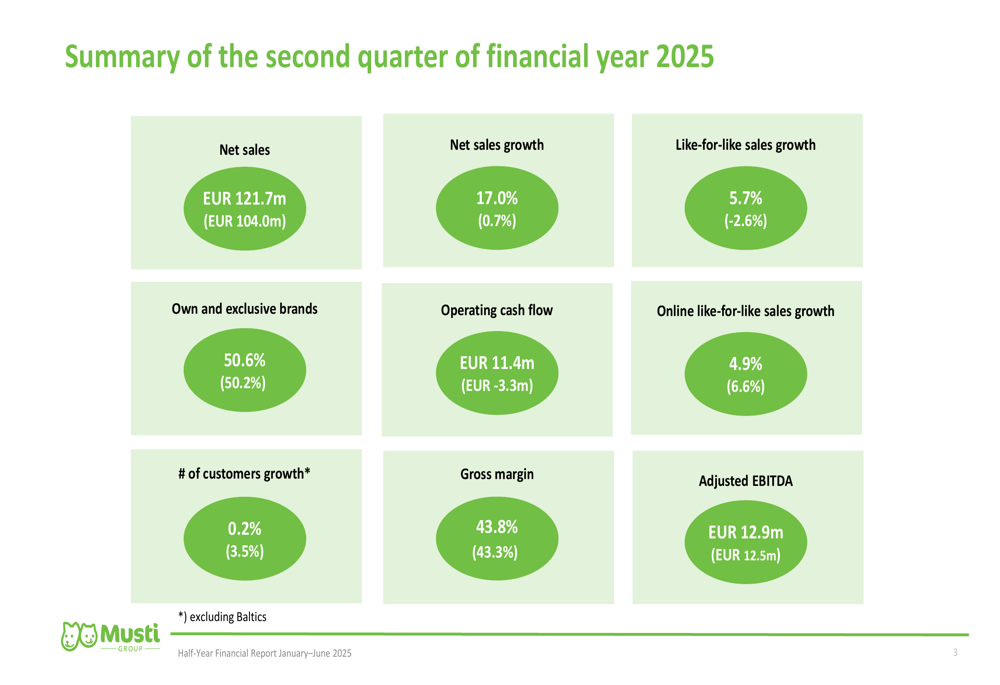

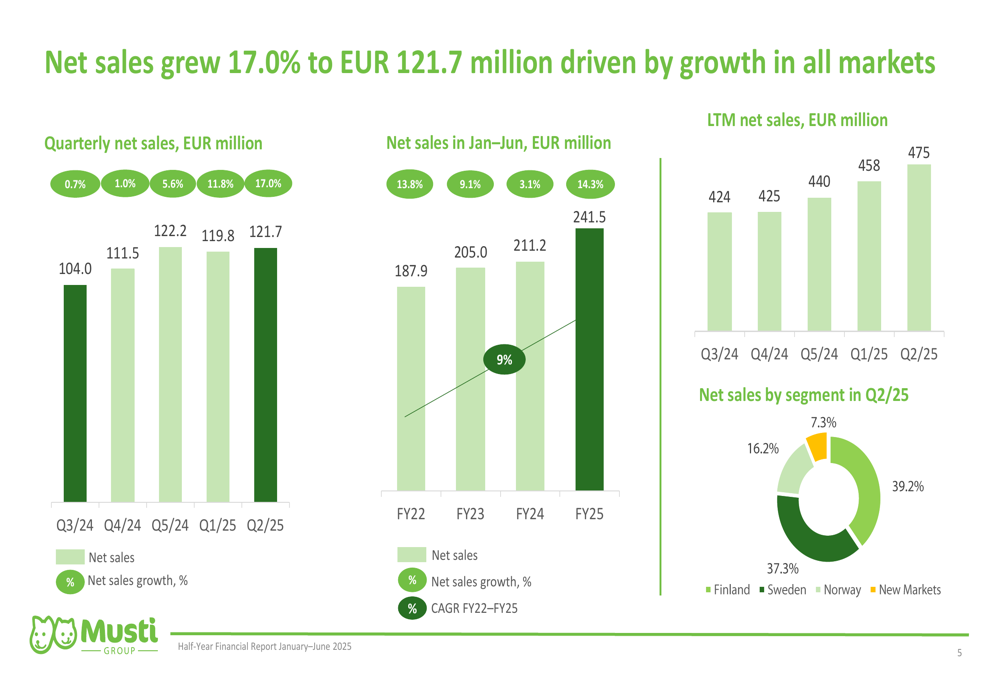

Musti Group delivered solid financial results in Q2 2025, with net sales growing 17.0% to EUR 121.7 million compared to EUR 104.0 million in the same period last year. Like-for-like sales growth, calculated in local currencies, reached 5.7%, a significant improvement from the -2.6% reported in the previous year.

The company’s gross margin improved to 43.8%, up from 43.3% in the comparable period, driven by favorable sales mix, campaign activities, and currency effects. Own and exclusive brands continued to gain traction, accounting for 50.6% of total sales compared to 50.2% in the previous year.

The following summary highlights key financial metrics for the second quarter:

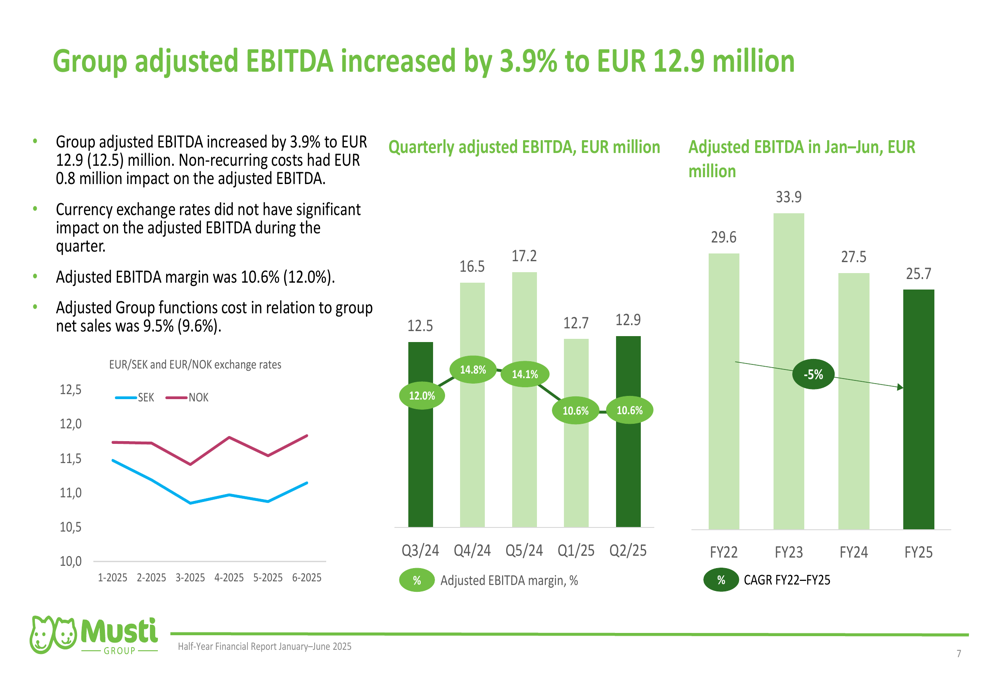

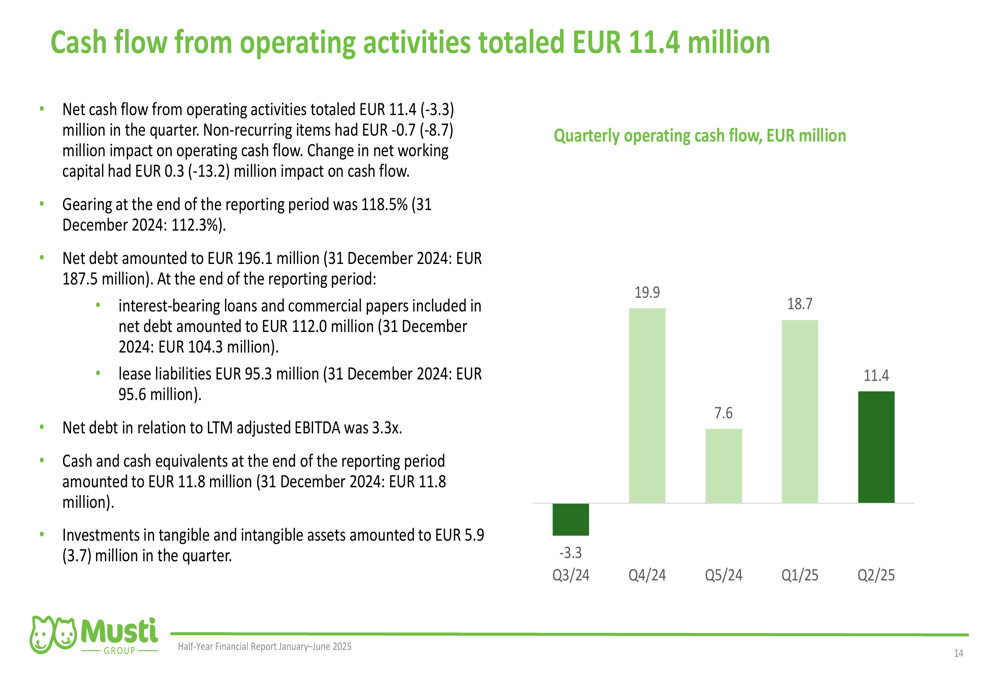

Adjusted EBITDA increased by 3.9% to EUR 12.9 million, including non-recurring costs of EUR 0.8 million. However, the adjusted EBITDA margin decreased to 10.6% from 12.0% in the previous year, reflecting investments in growth initiatives. Operating cash flow showed remarkable improvement, reaching EUR 11.4 million compared to negative EUR 3.3 million in the same period last year.

The following chart illustrates the company’s adjusted EBITDA development:

Geographic Segment Analysis

Musti Group’s performance varied across its geographic segments, with all markets contributing to overall growth. Net sales by segment in Q2 2025 were distributed as follows: Finland 37.3%, Sweden 16.2%, Norway 7.3%, and New Markets (Baltics) 39.2%.

As illustrated in the following net sales growth chart:

Finland, the company’s most established market, saw net sales increase by 6.0% to EUR 47.7 million, with impressive like-for-like sales growth of 8.4%. Adjusted EBITDA in Finland increased marginally by 0.5% to EUR 10.6 million, with the EBITDA margin slightly decreasing to 22.2% from 23.4%.

In Sweden, net sales grew by 7.8% to EUR 45.4 million, benefiting from a EUR 1.3 million positive impact from a stronger SEK exchange rate. Like-for-like sales growth in Sweden was more modest at 0.5%. Adjusted EBITDA increased by 5.4% to EUR 7.4 million, with the margin slightly decreasing to 16.3% from 16.6%.

Norway emerged as the standout performer with net sales increasing by 16.9% to EUR 19.8 million, driven by strong like-for-like sales growth of 12.3% and the ramp-up of recently opened stores. Adjusted EBITDA in Norway increased by 22.5% to EUR 4.6 million, with the margin improving to 23.5% from 22.4%.

The newly established New Markets segment, which includes the Baltic operations through the Pet City acquisition completed in November 2024, contributed EUR 8.8 million in net sales with an adjusted EBITDA of EUR 0.8 million and a margin of 9.3%. The company noted that ongoing integration activities impacted the segment’s performance during the quarter.

Financial Position and Cash Flow

Musti Group’s financial position remained stable, with significant improvement in operating cash flow. Net cash flow from operating activities totaled EUR 11.4 million, compared to negative EUR 3.3 million in the same period last year. This improvement was primarily driven by better working capital management, which had a positive impact of EUR 0.3 million compared to a negative EUR 13.2 million impact in the previous year.

The following chart illustrates the quarterly operating cash flow:

The company’s gearing ratio at the end of the reporting period was 118.5%, up from 112.3% on December 31, 2024. Net debt amounted to EUR 196.1 million, compared to EUR 187.5 million at the end of 2024. Net debt in relation to last twelve months adjusted EBITDA was 3.3x.

Investments in tangible and intangible assets increased to EUR 5.9 million from EUR 3.7 million in the same period last year, reflecting the company’s continued focus on expansion and store network development.

Strategic Initiatives and Outlook

Musti Group continues to execute its growth strategy focused on expanding its store network, enhancing its online platform, and growing its veterinary clinics and spa services. During the quarter, the company opened six directly operated stores, acquired one third-party store, and closed two stores.

The integration of Pet City in the Baltics remains a key focus area, with management noting that "during the second quarter, the financial performance improved as the integration process continued." The Baltic expansion represents a significant growth opportunity for Musti Group, adding 46 stores and 16 clinics to its network.

According to the earnings call transcript, CEO David Rönnberg emphasized the company’s competitive edge, stating, "We are growing much faster than everyone else in our countries." Meanwhile, CFO Robert Berglund highlighted a strategic shift, noting, "We need to now really switch focus on to profitable growth."

The company’s overall strategy appears to be working, with strong sales growth across all markets and improved gross margins. However, the declining adjusted EBITDA margin suggests that balancing growth investments with profitability remains a challenge. As Musti Group continues to expand its footprint in the Nordics and Baltics, investors will be watching closely to see if the company can maintain its growth momentum while improving its profitability metrics.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.