Trump announces 100% chip tariff as Apple ups U.S. investment

Myriad Genetics Inc (NASDAQ:MYGN) presented its second quarter 2025 earnings results on August 5, showing signs of recovery after a challenging first quarter. The genetic testing company reported modest revenue growth and raised its full-year guidance while announcing a strategic pivot toward oncology.

Quarterly Performance Highlights

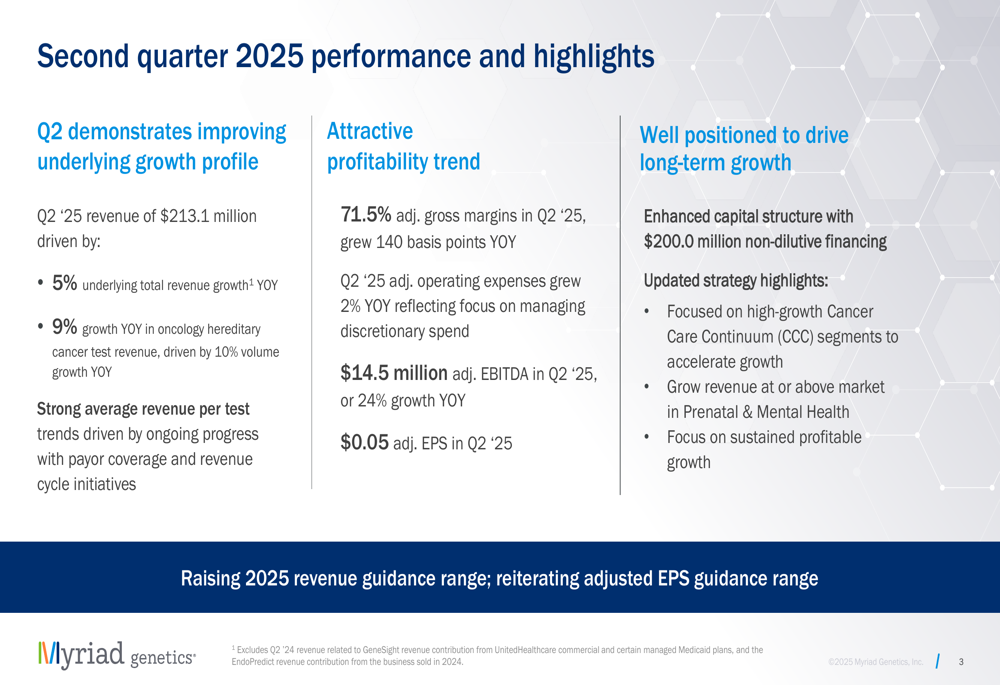

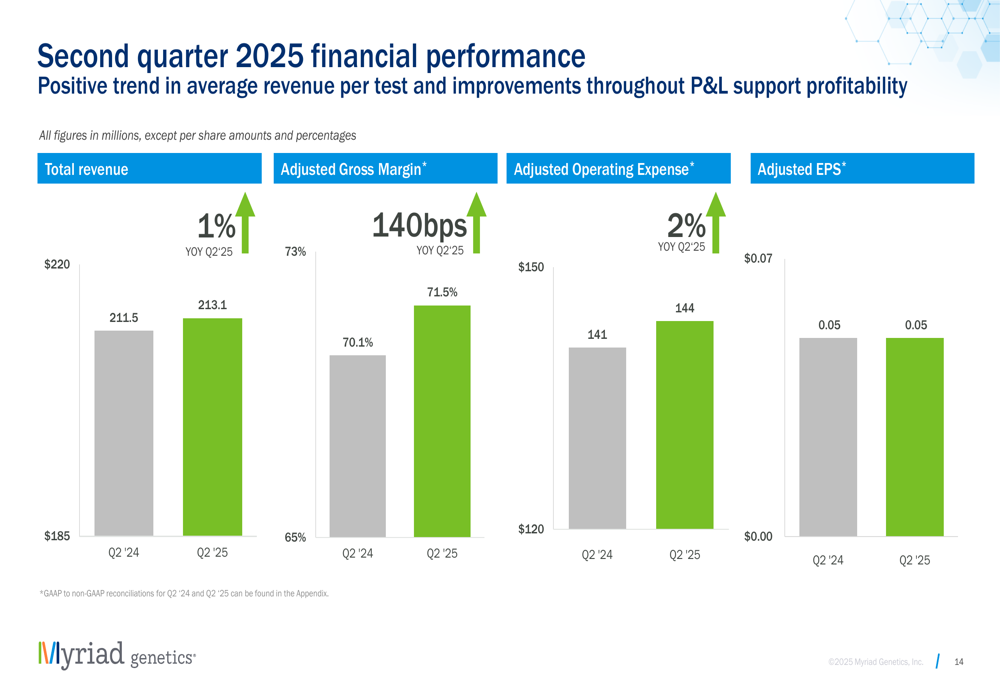

Myriad Genetics reported Q2 2025 revenue of $213.1 million, representing a 1% year-over-year increase. However, when excluding divested businesses and other one-time items, the company achieved underlying revenue growth of 5% compared to the same period last year.

As shown in the following chart detailing the company’s performance highlights, Myriad saw 9% growth in oncology hereditary cancer test revenue, with test volume increasing by 10%. The company also highlighted improved gross margins and EBITDA growth:

Adjusted gross margins reached 71.5% in Q2, an increase of 140 basis points compared to the same period last year. Adjusted EBITDA grew 24% year-over-year to $14.5 million, while adjusted EPS remained flat at $0.05 per share.

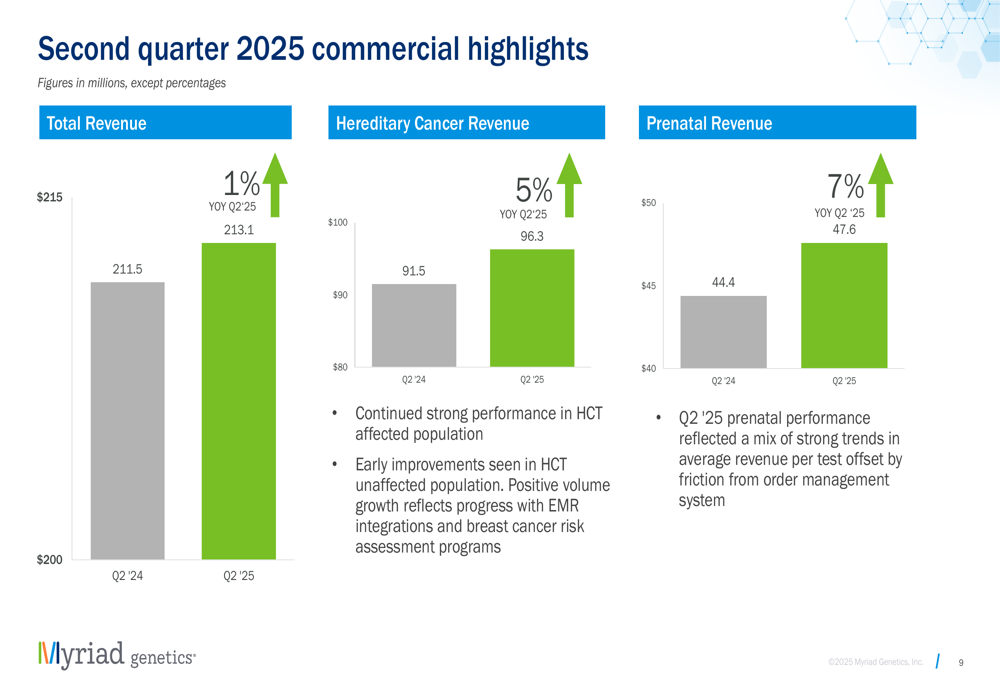

The company’s commercial performance varied across divisions, with the strongest results coming from hereditary cancer testing and prenatal services:

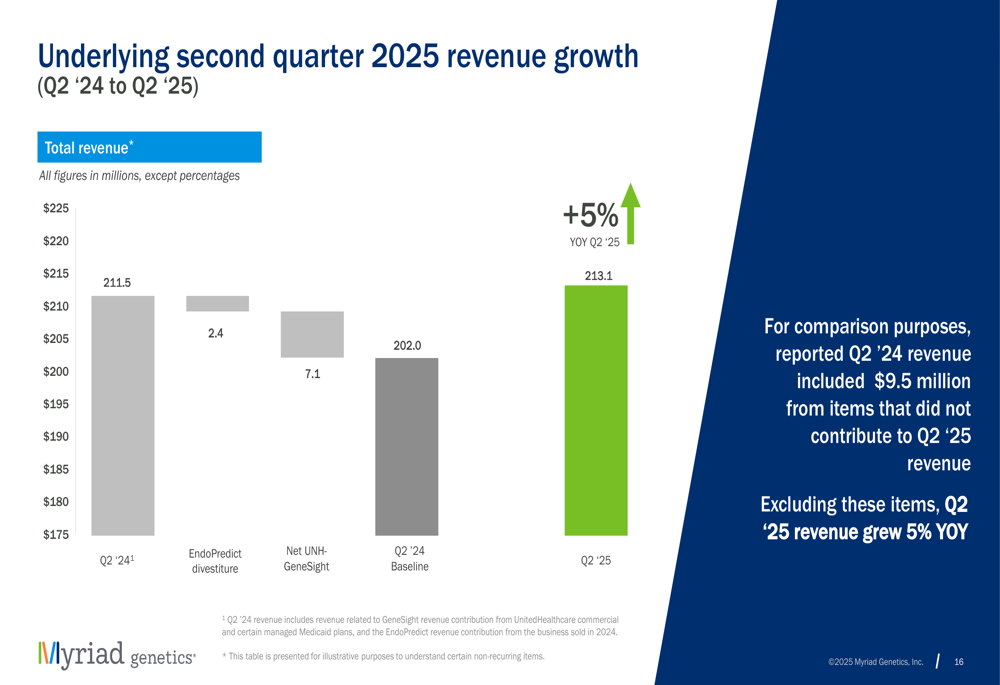

Myriad’s underlying revenue growth becomes clearer when accounting for divested businesses and other items that contributed to Q2 2024 revenue but not to Q2 2025:

This performance represents a notable improvement from Q1 2025, when the company missed revenue expectations with $196 million in revenue (a 3% year-over-year decline) and saw its stock price drop nearly 15% in after-hours trading.

Strategic Initiatives

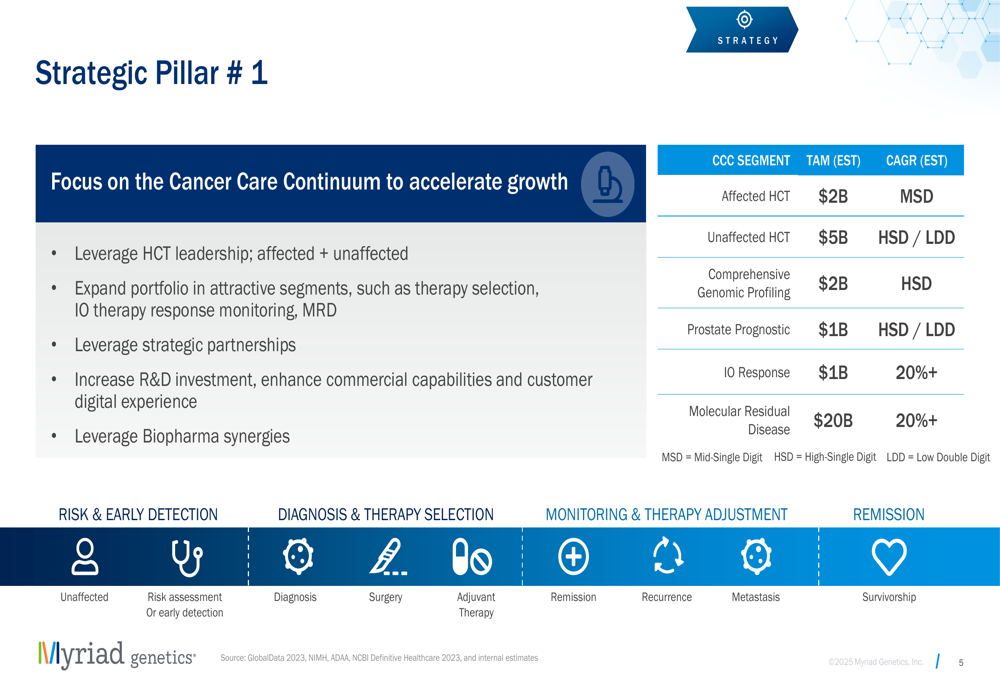

A significant focus of the presentation was Myriad’s updated strategy, which emphasizes the Cancer Care Continuum ( CCC (WA:CCCP)) as a key growth driver. The company outlined three strategic pillars, with the most detailed attention given to expanding its oncology portfolio.

The following slide details the company’s first strategic pillar, focusing on the Cancer Care Continuum:

Myriad plans to leverage its hereditary cancer testing leadership while expanding into high-growth segments like therapy selection, immunotherapy response monitoring, and molecular residual disease (MRD) testing. The company identified particularly strong growth potential in IO Response and MRD, both with projected market growth rates exceeding 20%.

For its other business segments, Myriad aims to grow revenue at or above market rates in Prenatal and Mental Health while maintaining disciplined investment. The company also emphasized its focus on sustained profitable growth through financial discipline and operational efficiency.

Financial Analysis

Despite the positive underlying trends, Myriad reported a significant GAAP net loss of $330.5 million for Q2 2025, primarily due to a $316.7 million goodwill and long-lived asset impairment charge. This non-cash charge reflects adjustments to the company’s balance sheet valuations.

The company’s financial performance metrics show improvement in key areas:

Myriad also announced an enhanced capital structure with a new $200 million credit facility, boosting its liquidity position. The initial tranche of $125 million has already been accessed, with an option for an additional $75 million. After transaction fees and paying down existing debt, the company estimates its total potential liquidity at approximately $205.9 million.

The company’s stock closed at $3.98 on August 5, 2025, down 2.76% for the day. In after-hours trading, the stock moved up slightly by 0.5% to $4.00. MYGN remains near its 52-week low of $3.76, reflecting ongoing investor caution despite the improved quarterly results.

Forward-Looking Statements

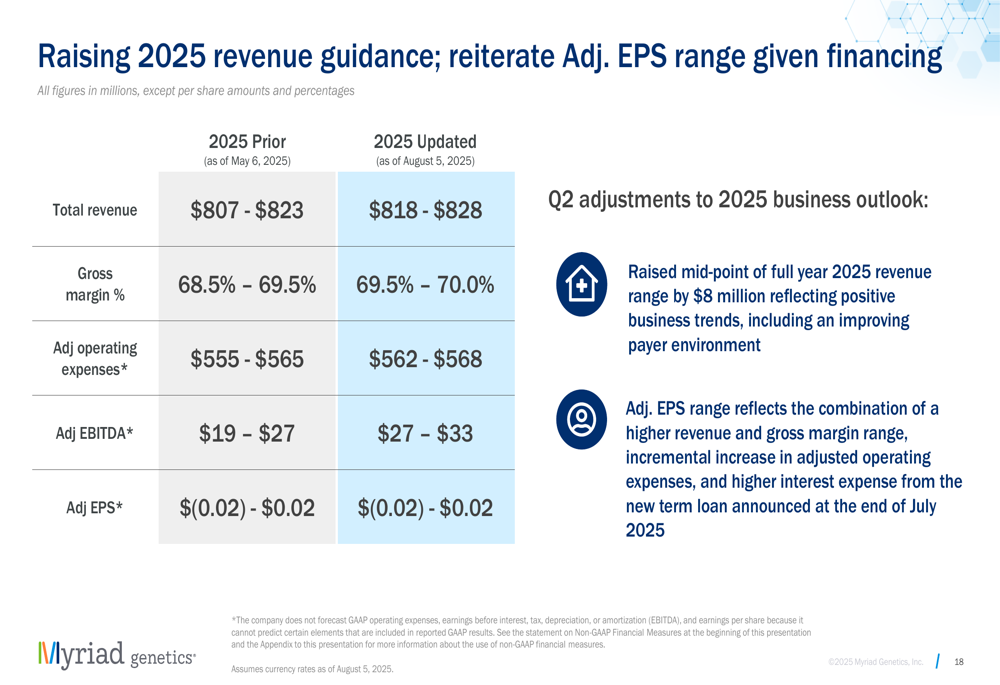

Based on the improved performance in Q2, Myriad raised its full-year 2025 guidance:

The company increased its revenue guidance to $818-$828 million, up from the previous range of $807-$823 million. Gross margin guidance was raised to 69.5%-70.0%, up from 68.5%-69.5%, and adjusted EBITDA guidance was increased to $27-$33 million, up from $19-$27 million. Adjusted EPS guidance remained unchanged at $(0.02)-$0.02.

The raised guidance suggests growing confidence in the company’s strategic direction and operational execution after a difficult start to the year. Myriad’s focus on the Cancer Care Continuum appears to be a key element of its recovery strategy, leveraging its established position in hereditary cancer testing while expanding into higher-growth oncology segments.

The company also highlighted ongoing efforts to support sustainable pricing through revenue cycle improvements, investments in pre-authorization teams, and engagement with payers. Myriad secured 49 new coverage policies and medical policy expansions year-to-date, which should help stabilize revenue per test going forward.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.