Tonix Pharmaceuticals stock halted ahead of FDA approval news

Introduction & Market Context

Nature’s Sunshine Products, Inc. (NASDAQ:NATR) presented its second-quarter 2025 financial results on July 31, 2025, reporting substantial growth in net income despite some operational headwinds. The company’s stock closed at $14.41 on the day of the presentation, down 3.4% from the previous close, but still well above its 52-week low of $10.81.

Following a strong first quarter that exceeded market expectations, Nature’s Sunshine continued to show resilience in Q2, with notable performance in key international markets, particularly Japan, while maintaining its strong balance sheet with zero debt.

Quarterly Performance Highlights

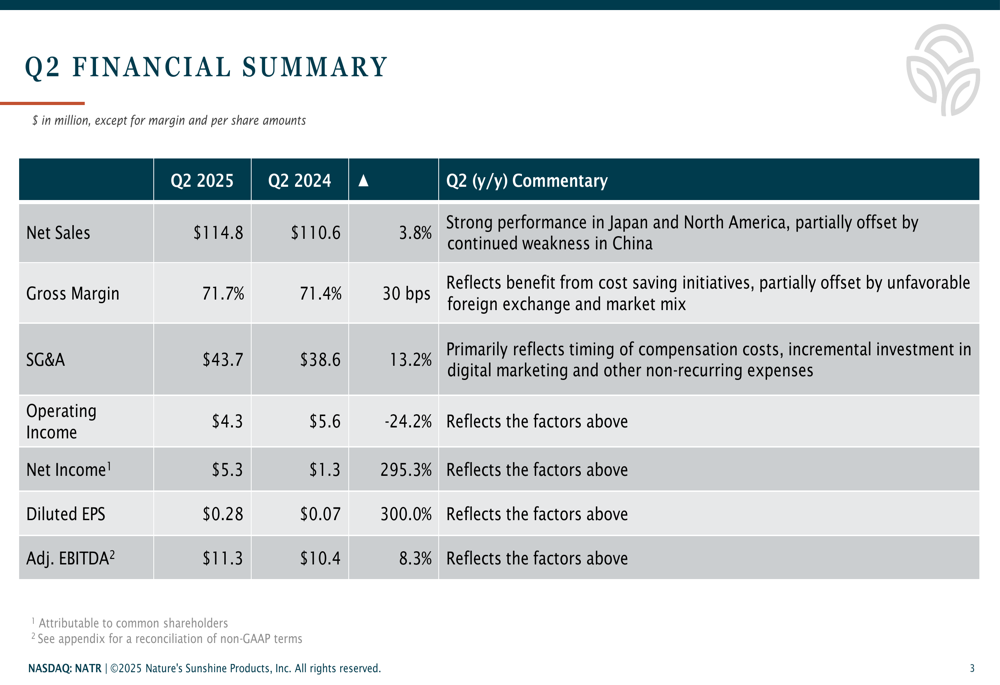

Nature’s Sunshine reported Q2 2025 net sales of $114.8 million, representing a 3.8% increase compared to $110.6 million in the same period last year. The company’s gross margin improved slightly to 71.7%, up 30 basis points from 71.4% in Q2 2024, reflecting the impact of cost-saving initiatives that were partially offset by foreign exchange fluctuations and market mix changes.

Most impressively, net income surged 295.3% to $5.3 million, compared to $1.3 million in Q2 2024, while diluted earnings per share tripled to $0.28 from $0.07 in the prior-year period. Adjusted EBITDA increased 8.3% to $11.3 million.

As shown in the following financial summary:

Despite the strong bottom-line results, operating income declined 24.2% to $4.3 million, down from $5.6 million in Q2 2024. This decrease was primarily driven by a 13.2% increase in selling, general and administrative expenses, which rose to $43.7 million due to the timing of compensation costs, increased digital marketing investments, and non-recurring expenses.

Segment Performance Analysis

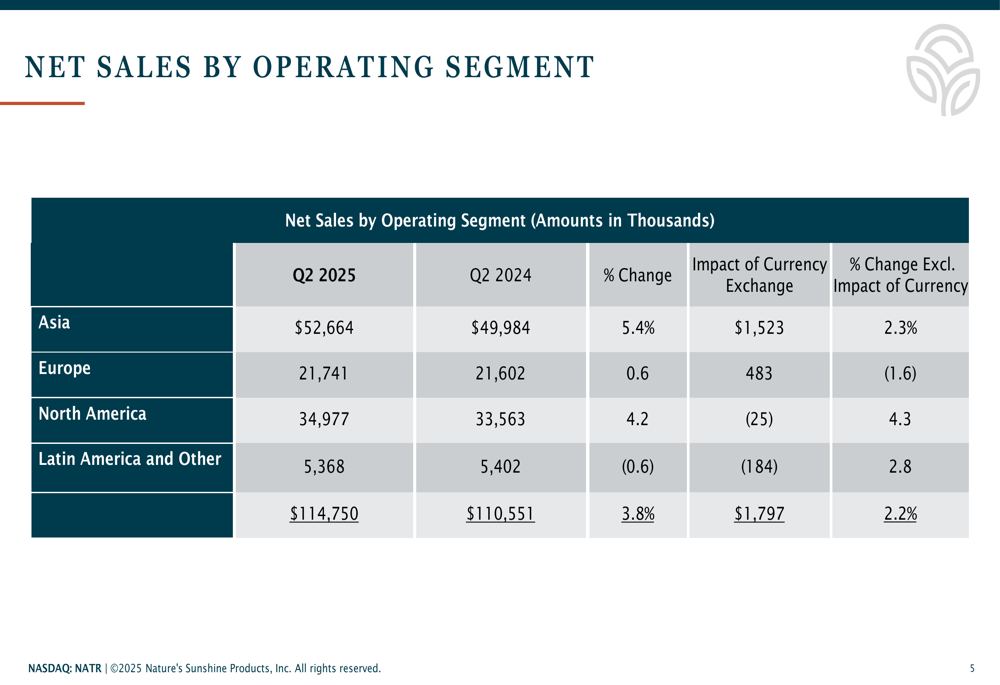

Nature’s Sunshine’s performance varied significantly across its geographic segments, with Asia and North America driving growth while other regions showed mixed results. The Asia segment led with a 5.4% increase in net sales to $52.7 million, or 2.3% growth when excluding currency impacts. This performance was primarily driven by strong results in Japan, though partially offset by weakness in China.

North America also performed well, with sales increasing 4.2% to $35.0 million. Europe showed modest growth of 0.6% to $21.7 million, though sales declined 1.6% when excluding currency effects. The Latin America segment experienced a slight decline of 0.6% to $5.4 million, though it would have shown 2.8% growth excluding currency impacts.

The following breakdown illustrates the company’s segment performance:

Balance Sheet and Cash Position

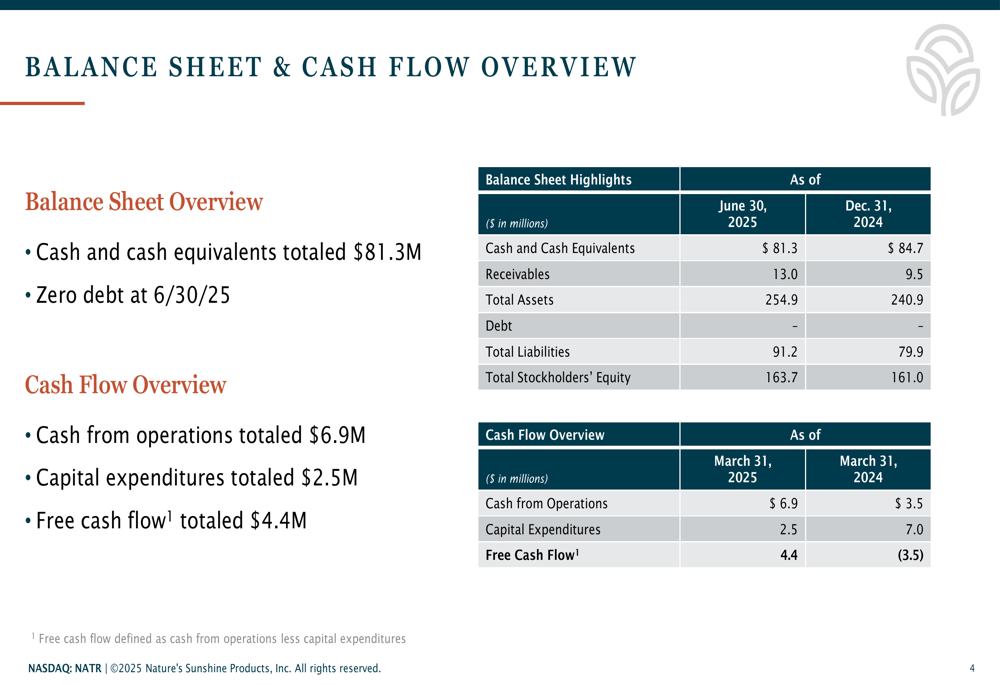

Nature’s Sunshine maintained a strong financial position with $81.3 million in cash and cash equivalents as of June 30, 2025, compared to $84.7 million at the end of 2024. The company continues to operate with zero debt, providing significant financial flexibility.

Total (EPA:TTEF) assets increased to $254.9 million from $240.9 million at the end of 2024, while stockholders’ equity rose slightly to $163.7 million from $161.0 million.

The company’s cash flow metrics showed improvement, with cash from operations reaching $6.9 million for the three months ended March 31, 2025, nearly double the $3.5 million generated in the same period of 2024. Capital expenditures decreased significantly to $2.5 million from $7.0 million, resulting in free cash flow of $4.4 million compared to negative $3.5 million in the prior year.

The following table provides a detailed overview of the company’s balance sheet and cash flow:

Historical Performance and Growth Strategy

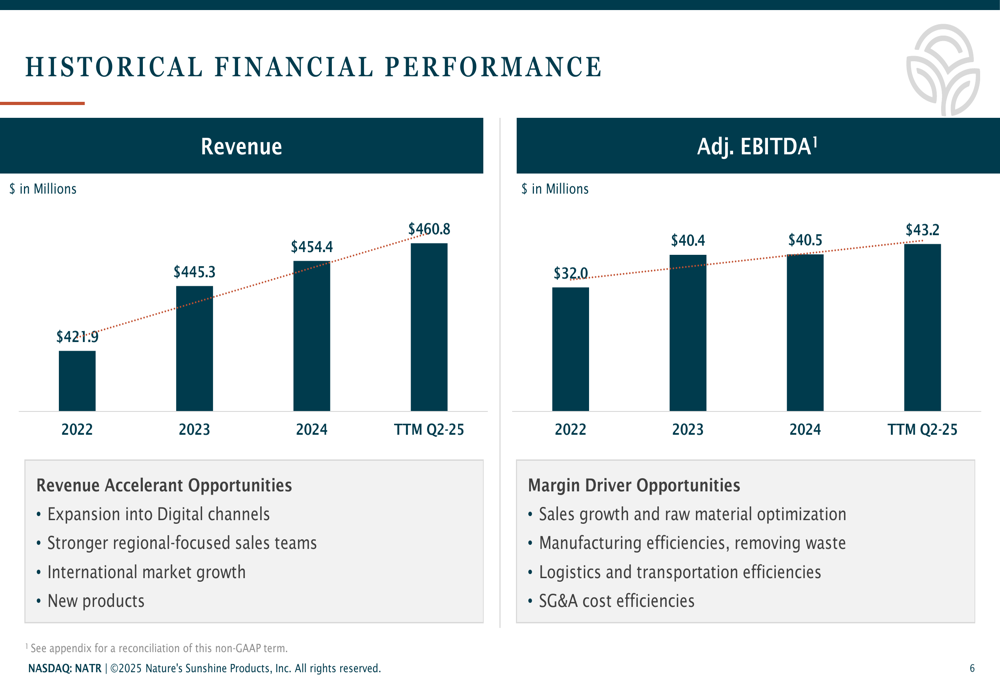

Nature’s Sunshine has demonstrated consistent revenue growth over the past several years, with trailing twelve-month revenue reaching $460.8 million as of Q2 2025, up from $454.4 million in 2024 and $445.3 million in 2023. Similarly, adjusted EBITDA has shown steady improvement, reaching $43.2 million for the trailing twelve months ended Q2 2025, compared to $40.5 million in 2024.

The company has identified several opportunities to accelerate revenue growth, including expansion into digital channels, strengthening regional sales teams, pursuing international market growth, and developing new products. Additionally, Nature’s Sunshine is focusing on margin improvement through sales growth and raw material optimization, manufacturing efficiencies, logistics improvements, and SG&A cost efficiencies.

The following chart illustrates the company’s historical financial performance and growth opportunities:

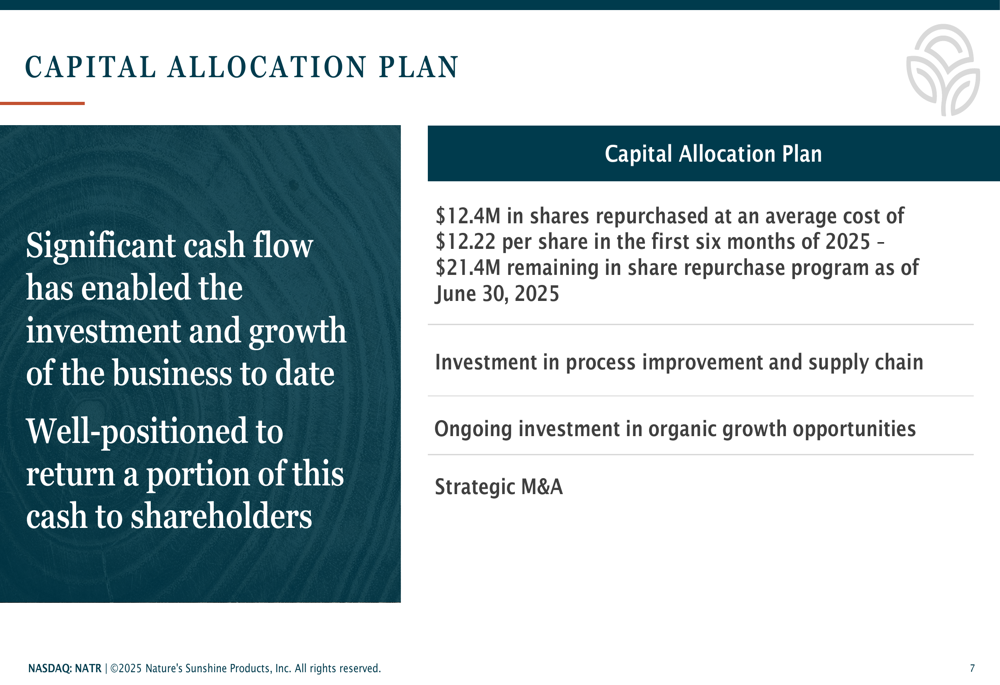

Capital Allocation Strategy

Nature’s Sunshine has been actively returning capital to shareholders while maintaining investments in growth initiatives. During the first six months of 2025, the company repurchased $12.4 million in shares at an average cost of $12.22 per share, with $21.4 million still remaining in the share repurchase program as of June 30, 2025.

The company’s capital allocation plan also includes investments in process improvement and supply chain optimization, ongoing investments in organic growth opportunities, and potential strategic mergers and acquisitions.

As outlined in the company’s capital allocation plan:

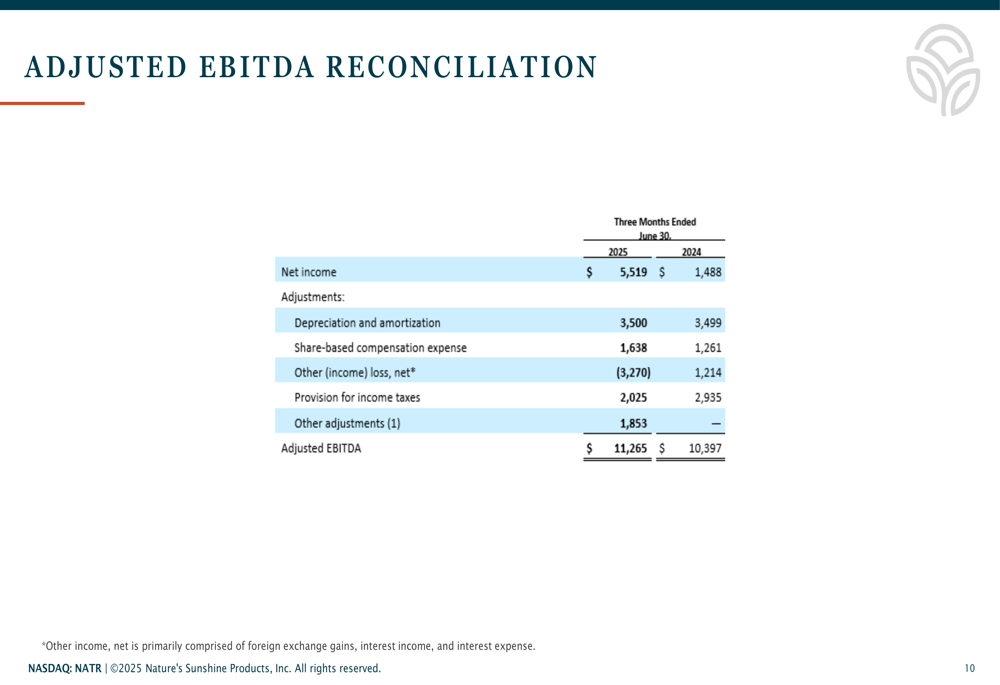

Adjusted EBITDA Reconciliation

To provide a clearer picture of its operational performance, Nature’s Sunshine presented a detailed reconciliation of net income to adjusted EBITDA. For Q2 2025, the company reported net income of $5.5 million, which was adjusted for depreciation and amortization ($3.5 million), share-based compensation expense ($1.6 million), other income (-$3.3 million), provision for income taxes ($2.0 million), and other adjustments ($1.9 million) to arrive at adjusted EBITDA of $11.3 million.

This represents an 8.3% increase from the adjusted EBITDA of $10.4 million reported in Q2 2024, demonstrating the company’s improved operational efficiency despite challenges in some areas.

The following table provides a detailed reconciliation of net income to adjusted EBITDA:

Forward-Looking Statements

Nature’s Sunshine’s presentation included forward-looking statements regarding growth opportunities and strategic initiatives. Building on its Q1 performance, where the company provided guidance for full-year 2025 net sales between $445 million and $470 million and adjusted EBITDA between $38 million and $44 million, Nature’s Sunshine appears to be on track to meet these targets based on its Q2 results.

The company’s strong cash position and zero debt provide flexibility to navigate potential challenges while continuing to invest in growth initiatives and return capital to shareholders. However, investors should note the contrast between rising net income and declining operating income, suggesting that non-operational factors played a significant role in the bottom-line improvement this quarter.

Nature’s Sunshine’s continued focus on digital expansion, international growth, and operational efficiencies positions the company to potentially overcome the operational challenges highlighted in this quarter’s results, though market uncertainties and regional performance variations remain factors to watch in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.