Gold prices steady amid Fed rate cut hopes; Trump-Putin talks awaited

Introduction & Market Context

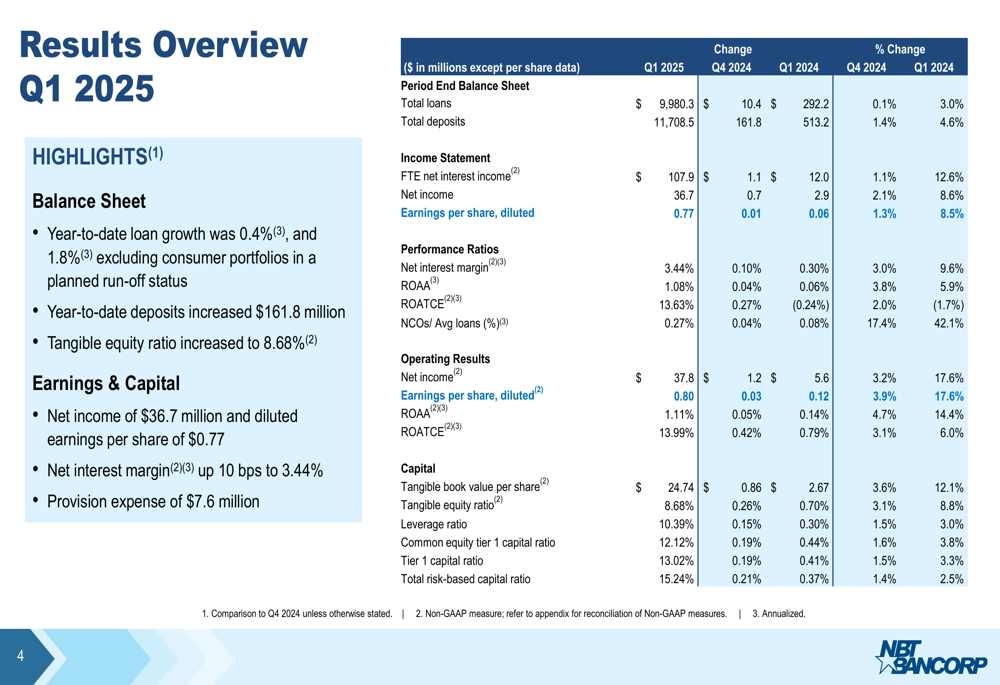

NBT Bancorp Inc . (NASDAQ:NBTB) released its first quarter 2025 earnings presentation on April 25, 2025, highlighting improved financial performance and strategic expansion plans. The company reported earnings per share of $0.77, consistent with the previous quarter’s results, while operating EPS reached $0.80. Despite the solid performance, NBT shares were trading down 1.06% in premarket activity at $41.91, suggesting investors may be taking a cautious approach to the regional banking sector.

The bank’s results come amid a challenging environment for regional financial institutions, as they navigate interest rate uncertainties and increasing competition for deposits. NBT’s focus on diversified revenue streams and strategic expansion appears aimed at addressing these industry headwinds.

Quarterly Performance Highlights

NBT Bancorp delivered positive sequential and year-over-year operating leverage in Q1 2025, with revenues growing 4.4% while expenses declined 1.1% from the previous quarter. Compared to Q1 2024, revenues increased by 11.8% while expenses grew at a slower rate of 7.5%.

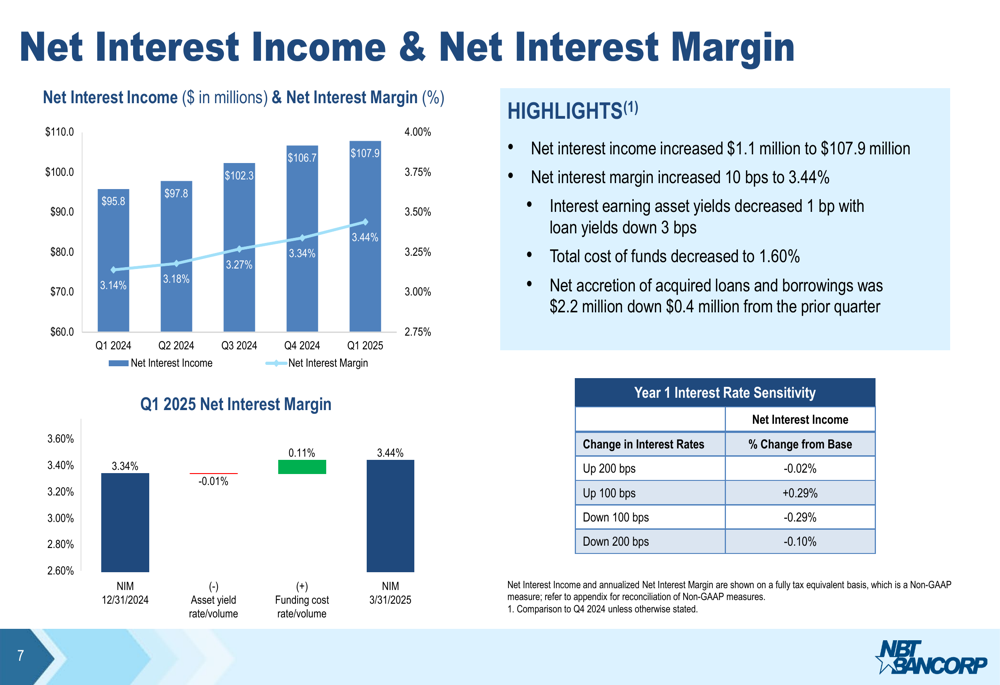

The bank reported total revenue of $155 million, with net interest income growing 1.1% quarter-over-quarter to $107.9 million. The net interest margin improved by 10 basis points to 3.44%, continuing a positive trend observed throughout 2024.

As shown in the following comprehensive overview of Q1 2025 results:

NBT’s balance sheet remained well-positioned with total loans of $9.98 billion and deposits of $11.71 billion at quarter-end. Year-to-date loan growth was modest at 0.4%, though it reached 1.8% when excluding consumer portfolios in run-off status. Deposits grew by $161.8 million or 1.4% since December 31, 2024.

The detailed financial results demonstrate consistent improvement across key metrics:

Detailed Financial Analysis

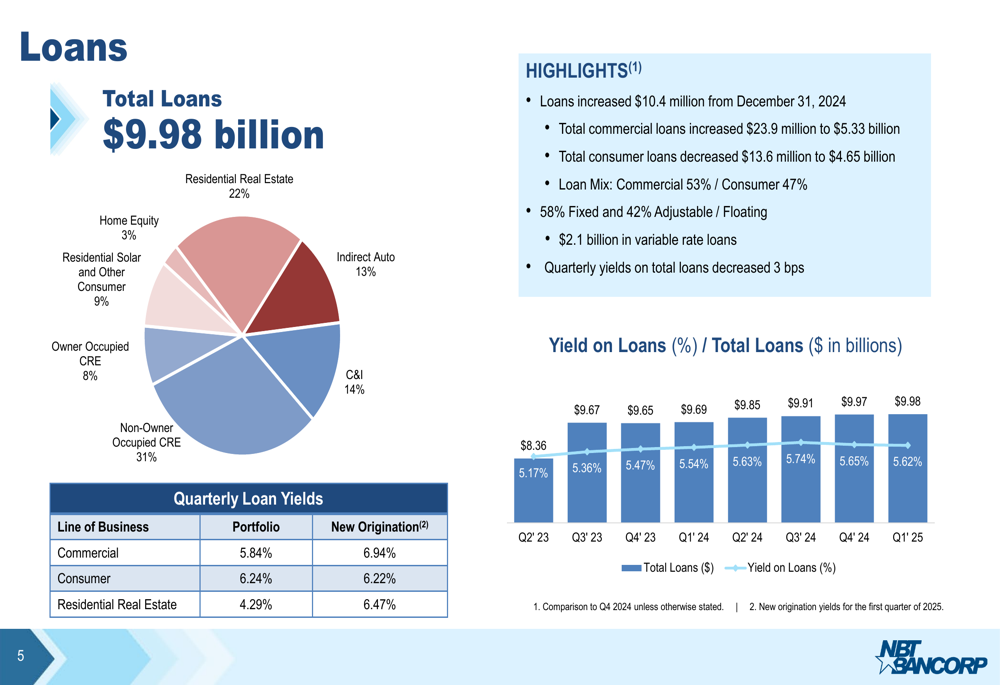

NBT’s loan portfolio maintained a balanced mix between commercial (53%) and consumer (47%) segments. Fixed-rate loans comprised 58% of the portfolio, with the remaining 42% in adjustable or floating-rate instruments. The quarterly yield on total loans decreased slightly by 3 basis points to 5.62%, though new commercial originations continued to come in at higher rates (6.94%).

The following chart illustrates the bank’s loan portfolio composition and yields:

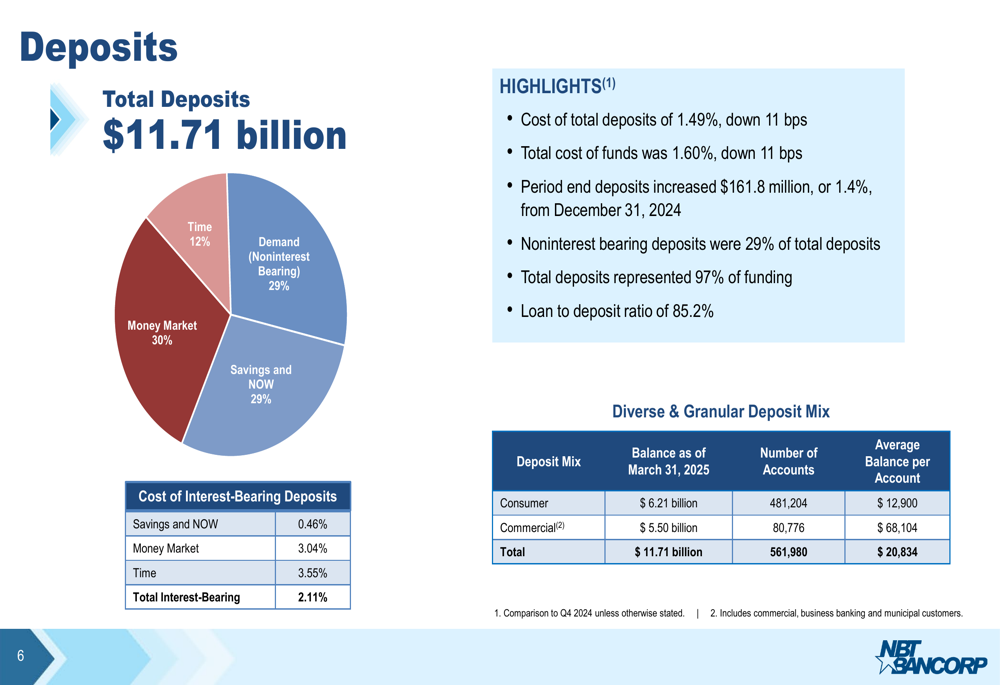

On the funding side, NBT’s deposit base remained diversified with noninterest-bearing demand deposits accounting for 29% of the total. The cost of total deposits decreased by 11 basis points to 1.49%, while the total cost of funds declined to 1.60%. The bank maintained a healthy loan-to-deposit ratio of 85.2%.

The deposit structure is detailed in this breakdown:

A key strength in NBT’s performance was the continued improvement in net interest margin, which has shown consistent growth from 3.14% in Q1 2024 to 3.44% in Q1 2025. This expansion was primarily driven by lower funding costs, as illustrated in the following chart:

Noninterest income represented 31% of total revenue, above peer levels, reaching $47.6 million for the quarter. This marked a 10% increase from Q1 2024, reflecting the bank’s success in diversifying revenue streams beyond traditional lending activities.

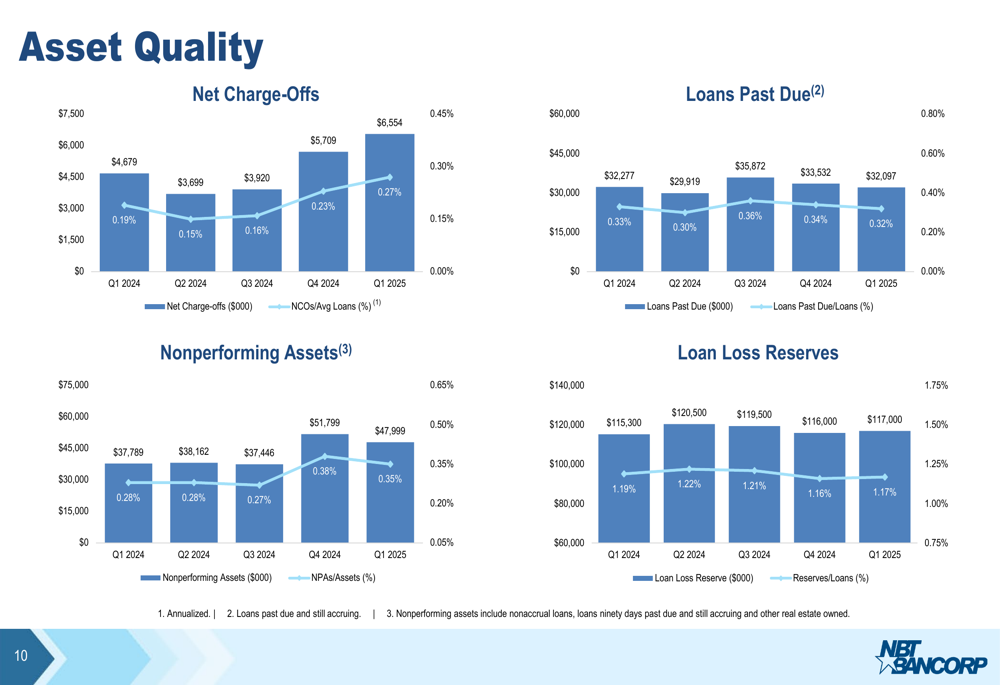

Asset quality metrics showed some mixed signals, with net charge-offs at 0.45% of average loans and nonperforming assets at 0.35% of total assets. The bank maintained loan loss reserves at 1.17% of total loans, providing a cushion against potential credit deterioration.

The following chart details the bank’s asset quality trends:

Strategic Initiatives

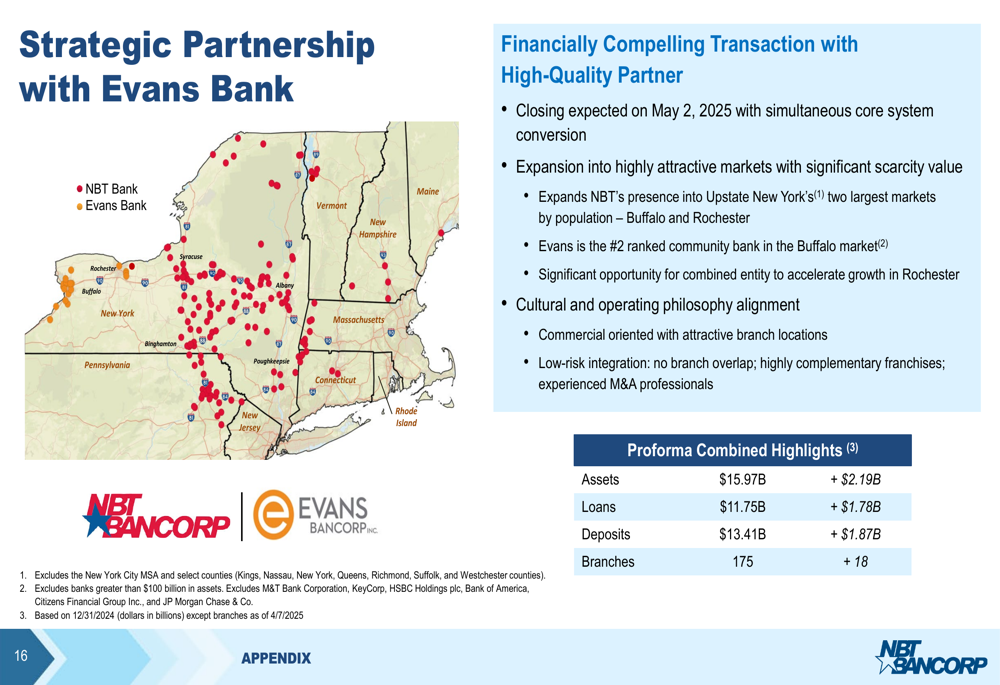

The most significant strategic development highlighted in the presentation was NBT’s pending acquisition of Evans Bank, scheduled to close on May 2, 2025, with a simultaneous core system conversion. This transaction will expand NBT’s presence into Buffalo and Rochester, the two largest markets by population in Upstate New York.

Evans Bank is currently the second-ranked community bank in the Buffalo market, providing NBT with an established presence in this key region. The combined entity will have approximately $15.97 billion in assets, $11.75 billion in loans, $13.41 billion in deposits, and 175 branches.

The details of this strategic partnership are outlined here:

NBT also highlighted the economic development potential in its markets, particularly the "Upstate NY Semiconductor Chip Corridor." The presentation noted a $6.1 billion investment supporting Micron Technology (NASDAQ:MU)’s plans to invest up to $100 billion over the next 20 years in a campus near Syracuse, which could create significant economic opportunities in NBT’s footprint.

Forward-Looking Statements

Looking ahead, NBT appears well-positioned for continued growth with its strengthened capital position and strategic expansion. The bank’s tangible equity ratio increased to 8.68%, while tangible book value per share grew to $24.74, up 3.6% from the previous quarter.

The Evans Bank acquisition represents a significant growth opportunity, though integration challenges will need to be managed carefully. The bank’s ability to maintain its positive operating leverage while successfully incorporating the new markets will be crucial to its performance in the coming quarters.

NBT’s interest rate sensitivity appears balanced, with a modest impact projected from potential rate changes. According to the presentation, a 100 basis point increase in interest rates would result in a 0.29% increase in net interest income, while a similar decrease would cause a 0.29% decline.

The bank’s diversified revenue streams, with nearly one-third coming from noninterest income sources, provide some insulation against interest rate volatility. However, the slight decline in loan yields and the competitive deposit environment could present challenges going forward.

As NBT moves into the remainder of 2025, investors will likely focus on the successful integration of Evans Bank, the bank’s ability to maintain margin expansion, and its performance in capitalizing on the economic development opportunities in its expanded footprint.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.