Stock market today: S&P 500 extends monthly win streak despite Nvidia-led stumble

Introduction & Market Context

nCino, Inc. (NASDAQ:NCNO) released its second quarter fiscal year 2026 results on August 26, 2025, showcasing strong performance across key metrics. The cloud banking software provider reported total revenues of $148.8 million, exceeding analyst expectations and continuing its growth trajectory from the previous quarter. Following the announcement, nCino’s stock saw modest movement in aftermarket trading, down 0.63% to $28.19 after closing the regular session up 1.13% at $28.37.

The company’s performance comes amid ongoing digital transformation in the banking sector, with financial institutions increasingly adopting cloud-based solutions to enhance operational efficiency and customer experience. nCino’s platform, which serves banks, credit unions, and independent mortgage banks, continues to gain traction globally as these institutions modernize their technology infrastructure.

Quarterly Performance Highlights

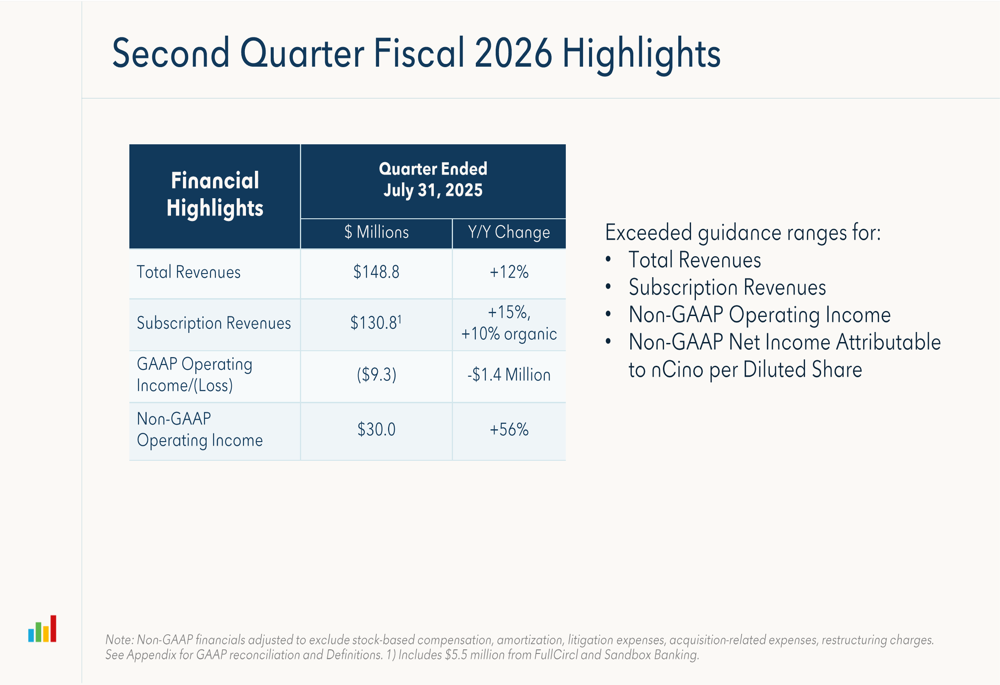

nCino reported total revenues of $148.8 million for Q2 FY26, representing a 12% year-over-year increase. Subscription revenues, which form the core of the company’s business model, reached $130.81 million, up 15% compared to the same period last year and 10% on an organic basis.

As shown in the following chart of quarterly financial highlights:

The company exceeded guidance ranges across all key metrics. While still operating at a GAAP loss of $9.3 million, nCino demonstrated significant improvement in its non-GAAP operating income, which reached $30.0 million, a 56% increase year-over-year. This represents a non-GAAP operating margin of 20%, up from 15% in the same quarter last year.

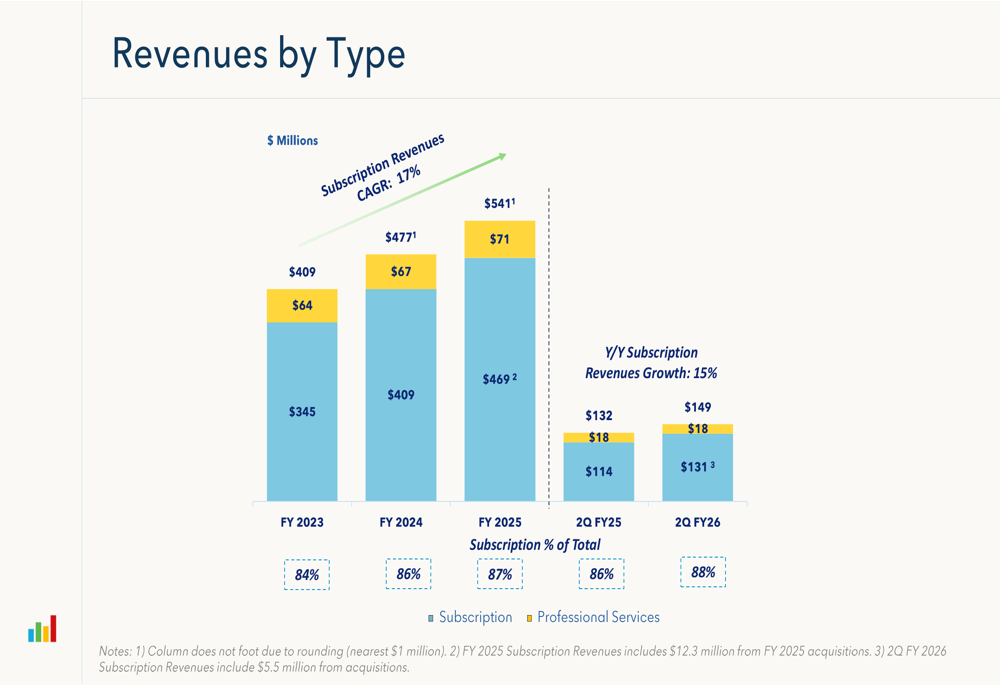

The company’s subscription revenue continues to dominate its revenue mix, now accounting for 88% of total revenue, up from 86% in Q2 FY25. This trend reflects nCino’s successful strategy of prioritizing recurring revenue streams.

Revenue Growth Drivers

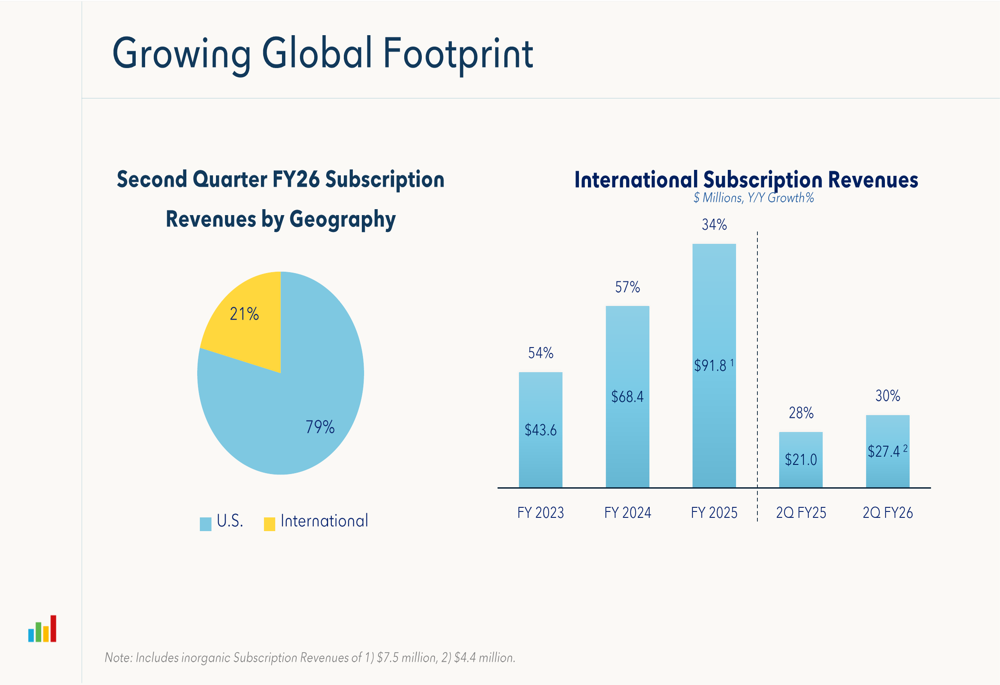

nCino’s growth in the quarter was driven by multiple factors, with international expansion and U.S. mortgage business recovery playing significant roles. International subscription revenues grew 30% year-over-year to reach $27.4 million, now representing 21% of the company’s total subscription revenue.

The company’s global footprint continues to expand, as illustrated in this geographic breakdown:

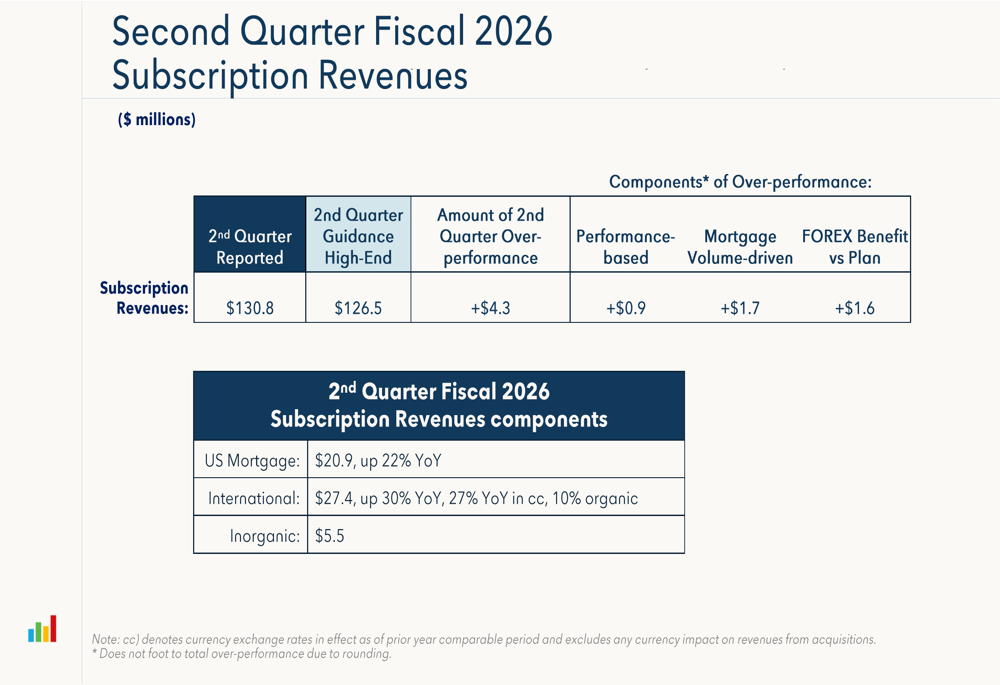

Meanwhile, U.S. mortgage subscription revenues showed strong recovery, growing 22% year-over-year to $20.9 million. This performance exceeded expectations, with mortgage volume-driven factors contributing $1.7 million to the quarter’s over-performance.

The detailed breakdown of subscription revenue performance reveals the sources of the company’s outperformance:

nCino’s Annual Contract Value (ACV), a key indicator of future revenue potential, reached $516.4 million in FY25, representing 13% year-over-year growth. The company’s ACV Net Retention Rate improved to 106% in FY25, up from 102% in FY24, indicating stronger customer retention and expansion.

Margin Expansion and Operational Efficiency

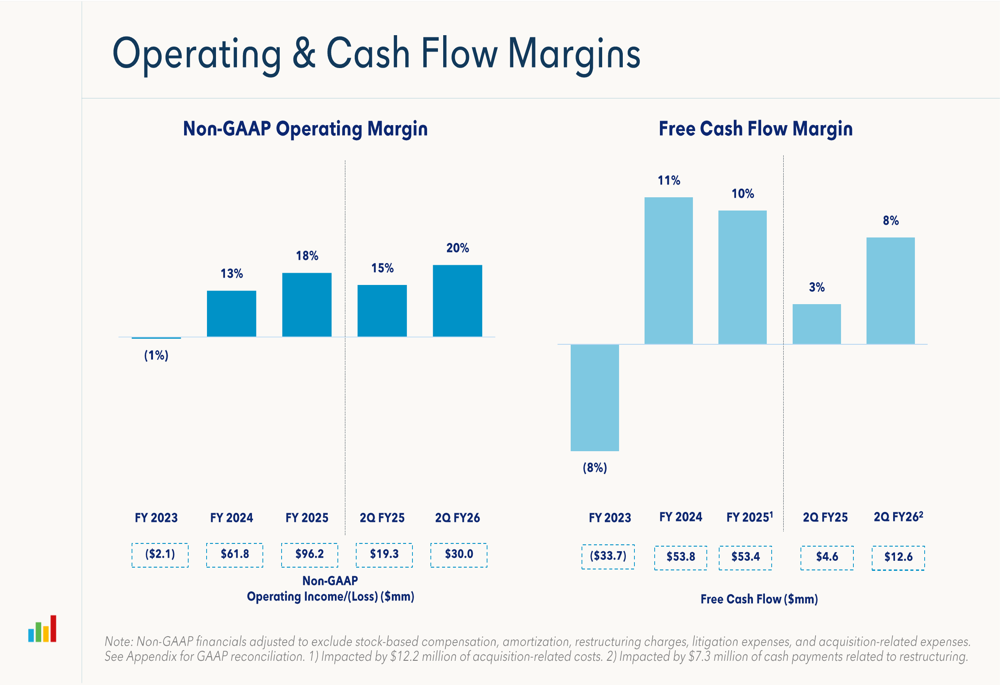

A standout aspect of nCino’s Q2 results was the significant improvement in profitability metrics. Non-GAAP operating margin expanded to 20% in Q2 FY26, up from 15% in the same period last year. This improvement reflects the company’s focus on operational efficiency and disciplined expense management.

The following chart illustrates nCino’s consistent margin improvement trajectory:

Free cash flow more than doubled to $12.6 million, representing 8% of total revenue compared to 3% in Q2 FY25. This improvement in cash generation strengthens nCino’s financial position and provides greater flexibility for strategic investments.

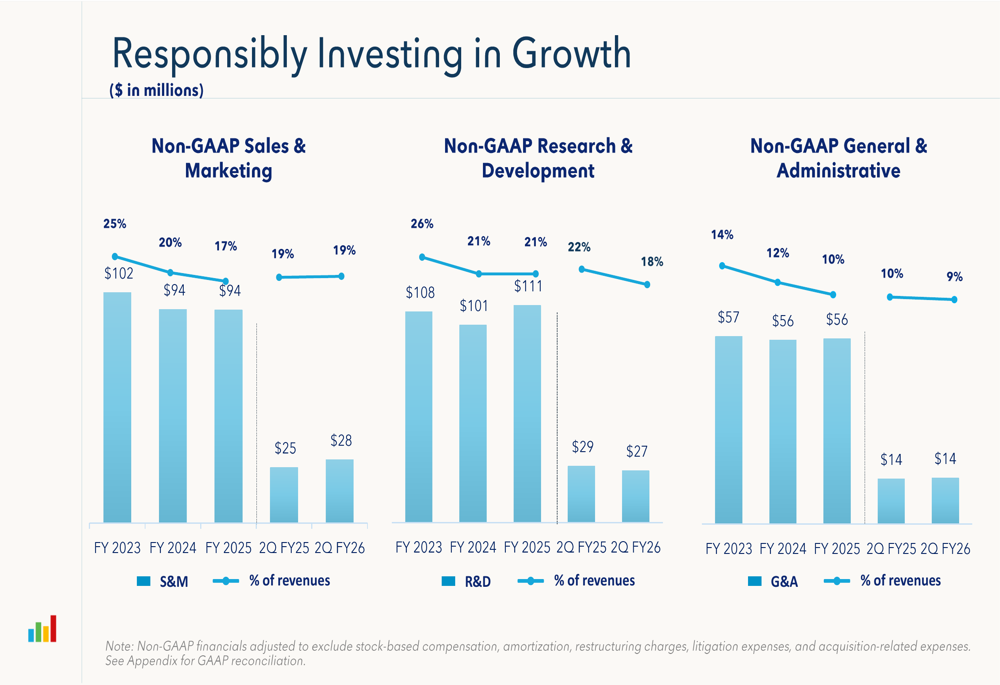

The company has maintained stable gross margins while reducing operating expenses as a percentage of revenue. Research and development expenses decreased from 22% of revenue in Q2 FY25 to 18% in Q2 FY26, while general and administrative expenses declined from 10% to 9%. These efficiency gains have contributed significantly to the improved operating margin.

Customer Base and Market Position

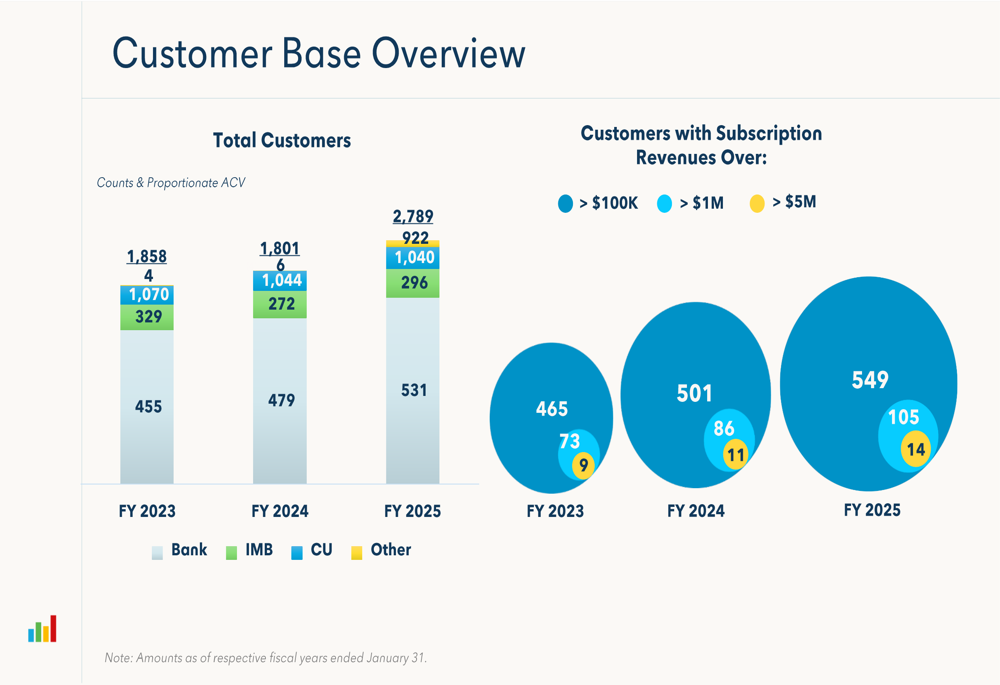

nCino continues to expand its customer base, particularly among higher-value clients. As of FY25, the company had 105 customers with subscription revenues exceeding $1 million, up from 86 in FY24. The number of customers with subscription revenues over $5 million increased to 14, up from 11 the previous year.

The following chart shows the evolution of nCino’s customer base:

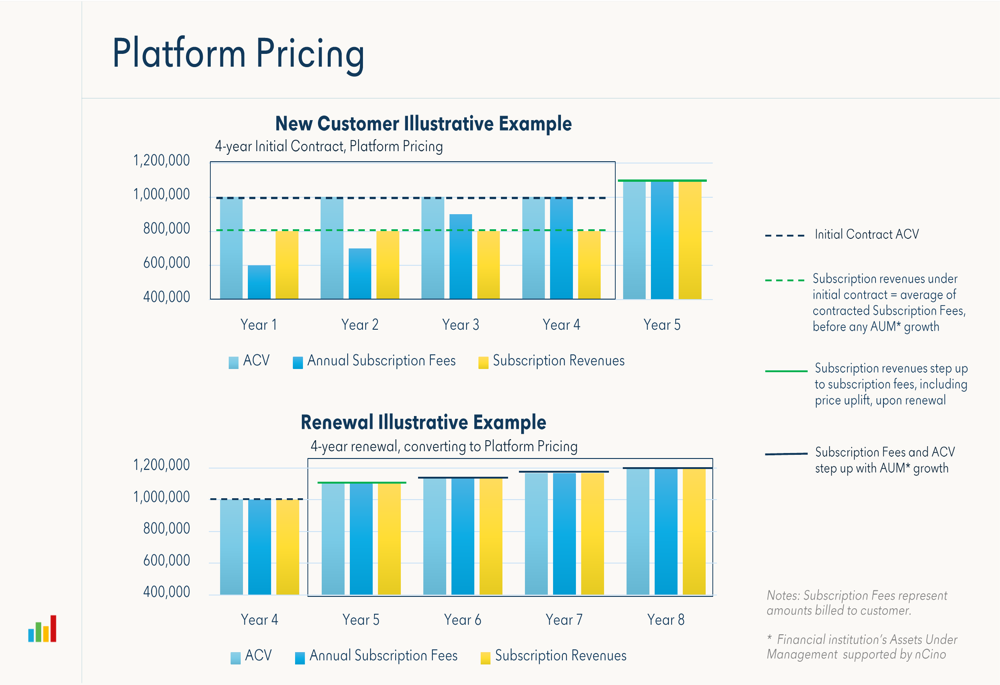

The company’s platform pricing model, which scales with customer growth, positions nCino to benefit from the expansion of its existing clients. This is illustrated in the company’s platform pricing examples:

This pricing approach helps explain nCino’s strong net retention rates and provides a path to continued revenue growth even in a challenging economic environment.

Forward Guidance and Outlook

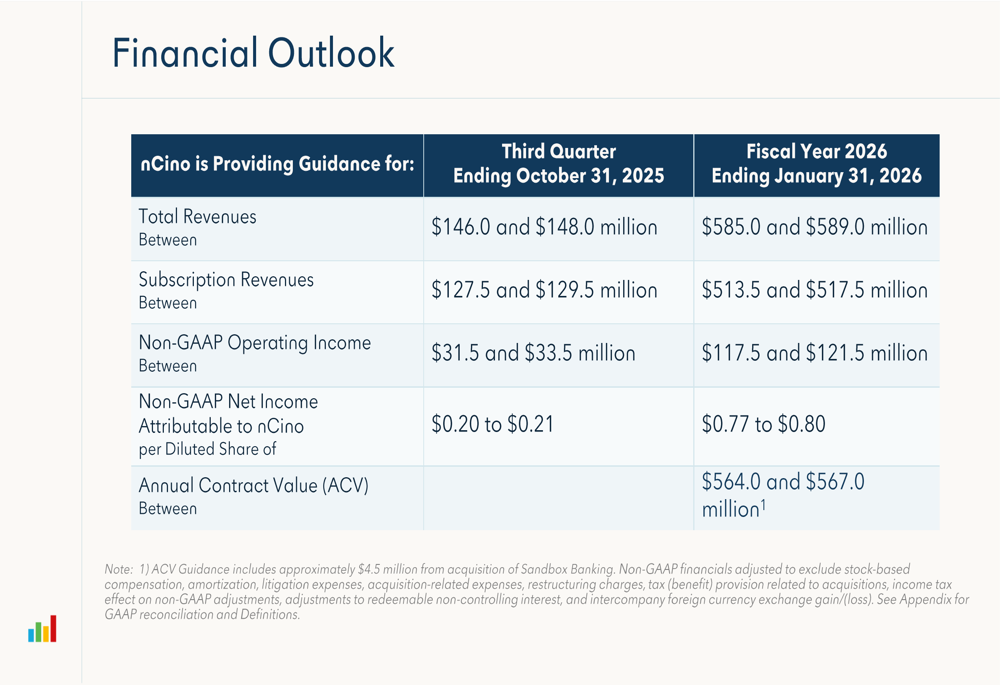

Based on its strong performance in the first half of the fiscal year, nCino has raised its full-year guidance. For fiscal year 2026, the company now expects total revenues between $585.0 and $589.0 million, representing approximately 9% year-over-year growth.

The detailed financial outlook is presented in the following table:

For the third quarter ending October 31, 2025, nCino anticipates total revenues between $146.0 and $148.0 million and subscription revenues between $127.5 and $129.5 million. Non-GAAP operating income is expected to be between $31.5 and $33.5 million.

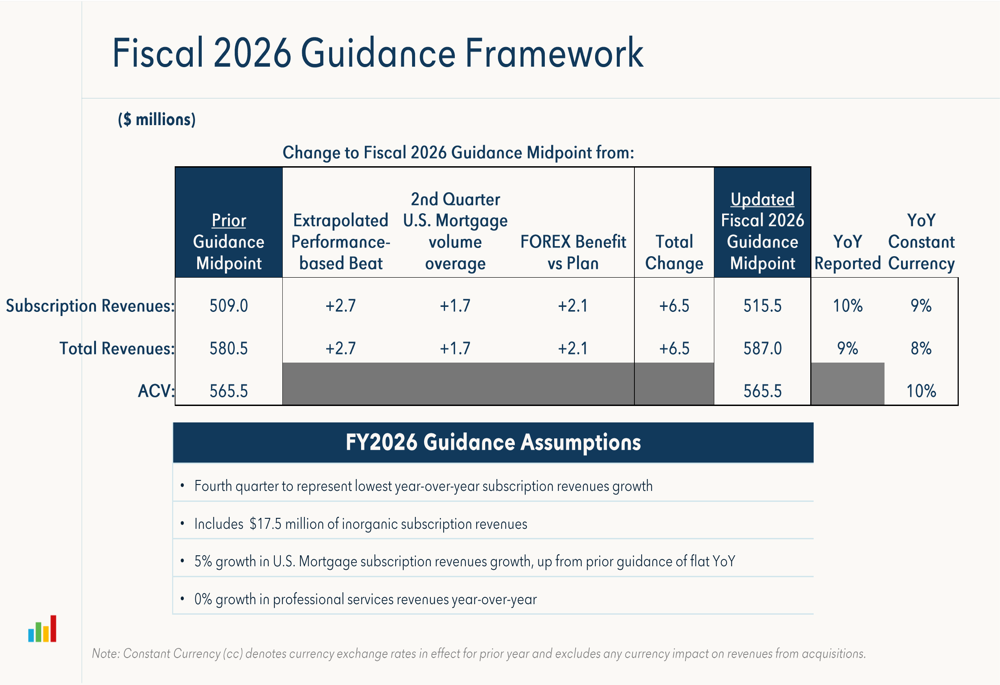

The company has also updated its fiscal 2026 guidance framework, projecting ACV growth of 10% and subscription revenue growth of 9-10% in constant currency:

While the outlook is generally positive, nCino noted that the fourth quarter is expected to represent the lowest year-over-year subscription revenues growth, consistent with cautionary notes from previous earnings reports. This suggests potential headwinds in the latter part of the fiscal year, though the company’s overall trajectory remains strong.

nCino’s Q2 FY26 results demonstrate continued execution of its growth strategy, with particular strength in international markets and improved profitability metrics. The company’s focus on subscription revenue growth, operational efficiency, and strategic expansion positions it well in the competitive cloud banking software market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.