US stock futures inch higher with Q3 earnings on tap

Introduction & Market Context

NeoGenomics Inc . (NASDAQ:NEO) presented its second quarter 2025 financial results on July 29, revealing mixed performance that prompted a significant market reaction. The oncology diagnostics company reported 10% revenue growth but simultaneously reduced its full-year guidance, triggering a 21% plunge in premarket trading.

The company’s shares, which closed at $6.46 on July 28, fell to $5.10 in premarket trading as investors responded to the lowered expectations despite some positive operational metrics. This reaction follows a challenging first quarter when the company missed revenue forecasts but maintained its full-year guidance.

Quarterly Performance Highlights

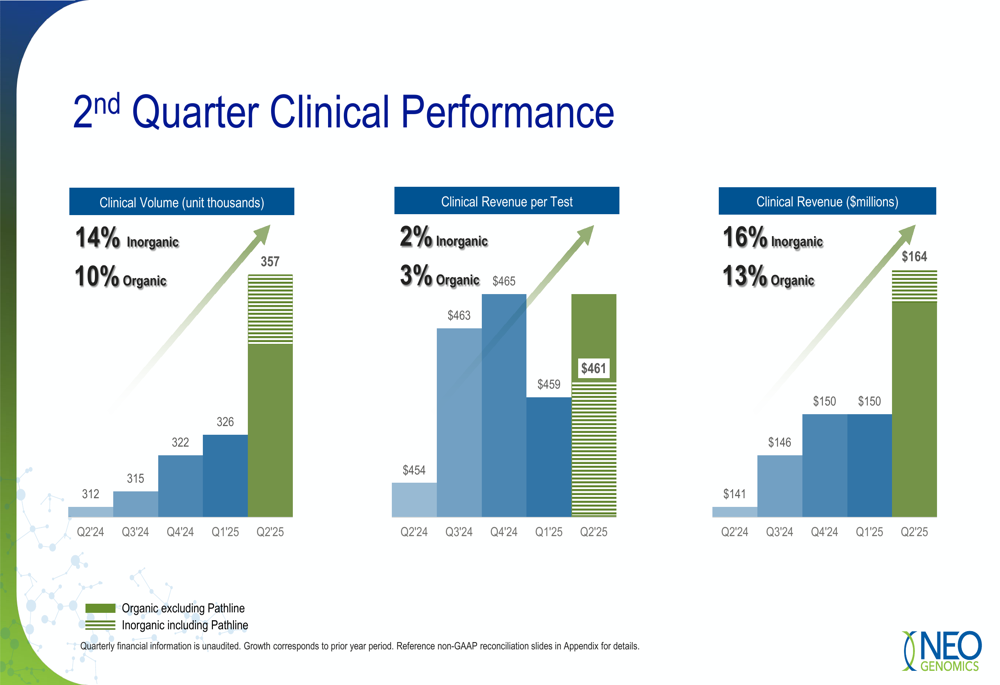

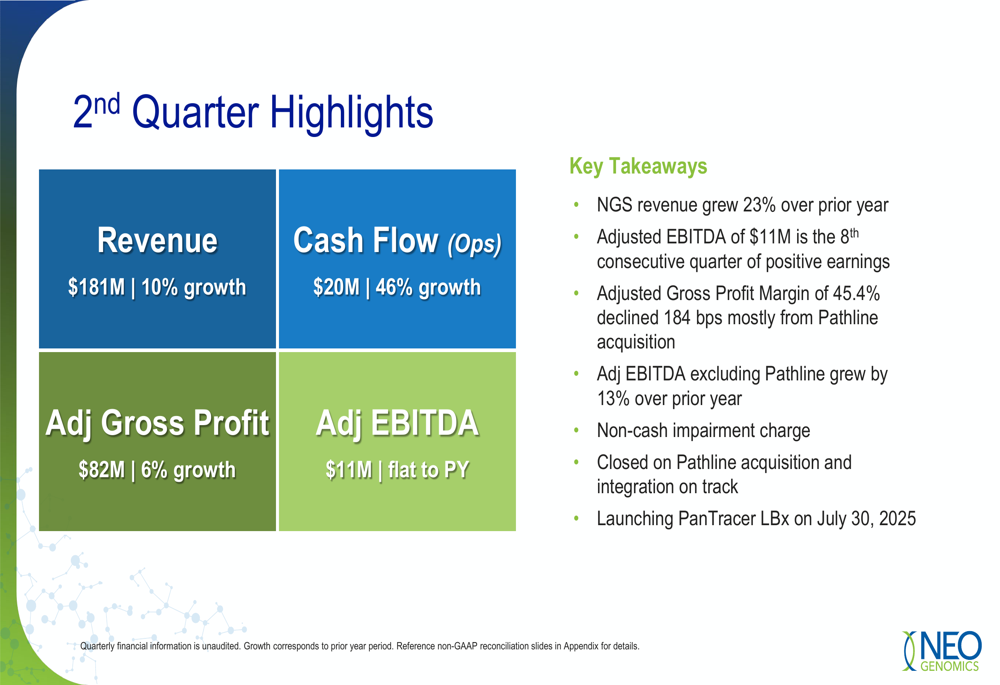

NeoGenomics reported total revenue of $181.3 million for Q2 2025, representing a 10.2% increase from $164.5 million in the same period last year. The clinical business showed particular strength, with volume growing 14% (including inorganic growth) and 10% organically.

As shown in the following chart of quarterly clinical performance:

The company’s clinical revenue increased by 16% overall (13% organically) to $164 million, while revenue per test improved by 2% to $461. Next-generation sequencing (NGS) revenue was a standout performer, growing 23% year-over-year.

Cash flow from operations showed significant improvement, increasing 46.3% to $20.3 million compared to $13.9 million in Q2 2024. However, adjusted EBITDA remained flat at $10.7 million, and the company reported a net loss of $45.1 million for the quarter.

The quarter’s key financial metrics are summarized in this overview:

Guidance Revision

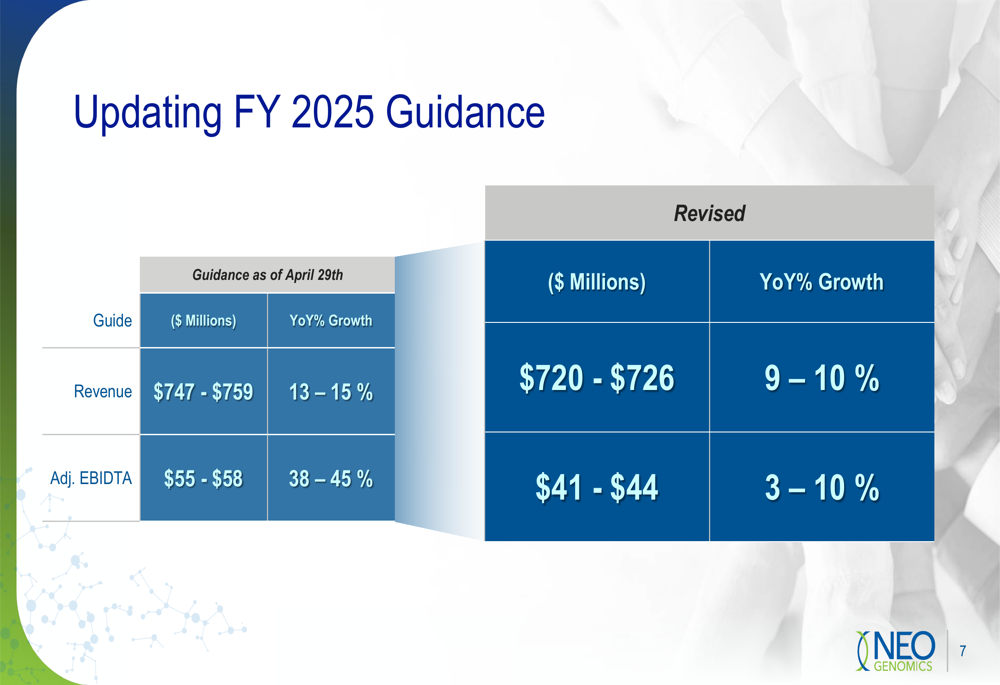

The most significant development in the presentation was NeoGenomics’ substantial reduction in its full-year 2025 guidance. This revision represents a marked change from the company’s position after Q1 results, when it maintained its original outlook despite missing revenue targets.

The updated guidance shows:

Revenue expectations were cut from $747-759 million (13-15% growth) to $720-726 million (9-10% growth), while adjusted EBITDA projections were reduced more dramatically from $55-58 million (38-45% growth) to $41-44 million (3-10% growth).

This guidance reduction appears to be the primary driver behind the stock’s sharp decline, as it signals potential challenges in the company’s growth trajectory and profitability improvement plans.

Strategic Initiatives

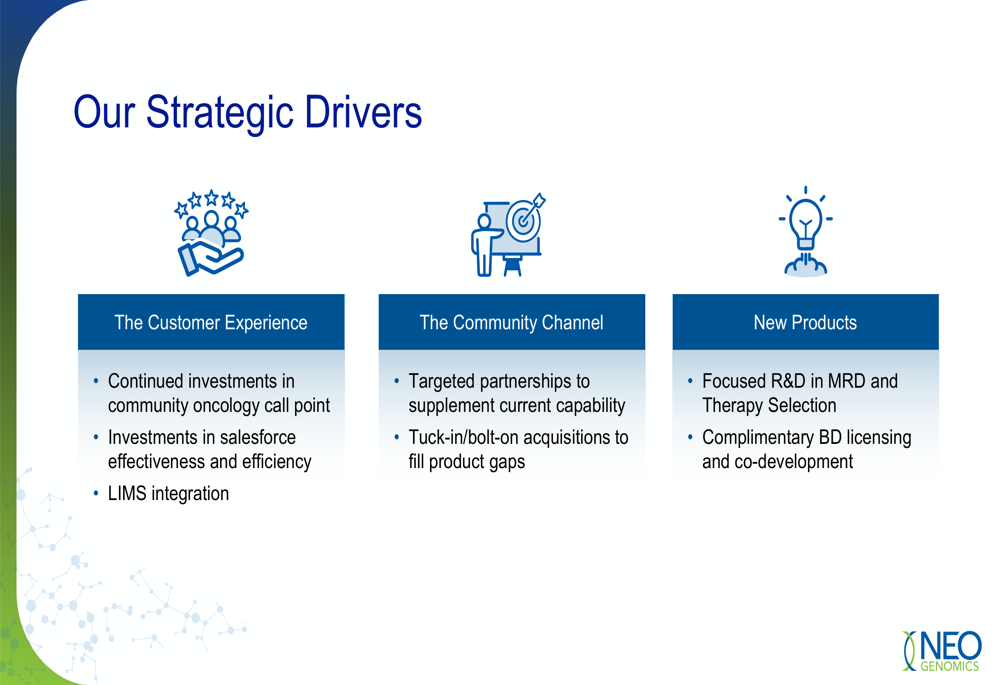

Despite the guidance reduction, NeoGenomics highlighted several strategic initiatives aimed at driving future growth. The company completed its acquisition of Pathline, with integration reportedly on track, though this acquisition was noted as having a negative impact on gross margins.

The company is preparing to launch a new product, PanTracer LBx, on July 30, 2025, as part of its ongoing innovation efforts. Management outlined its strategic focus areas:

NeoGenomics continues to invest in the community oncology channel, which represents a key growth area. The company is pursuing both organic development and strategic acquisitions to enhance its product portfolio, with particular focus on Minimal Residual Disease (MRD) testing and Therapy Selection capabilities.

Financial Analysis

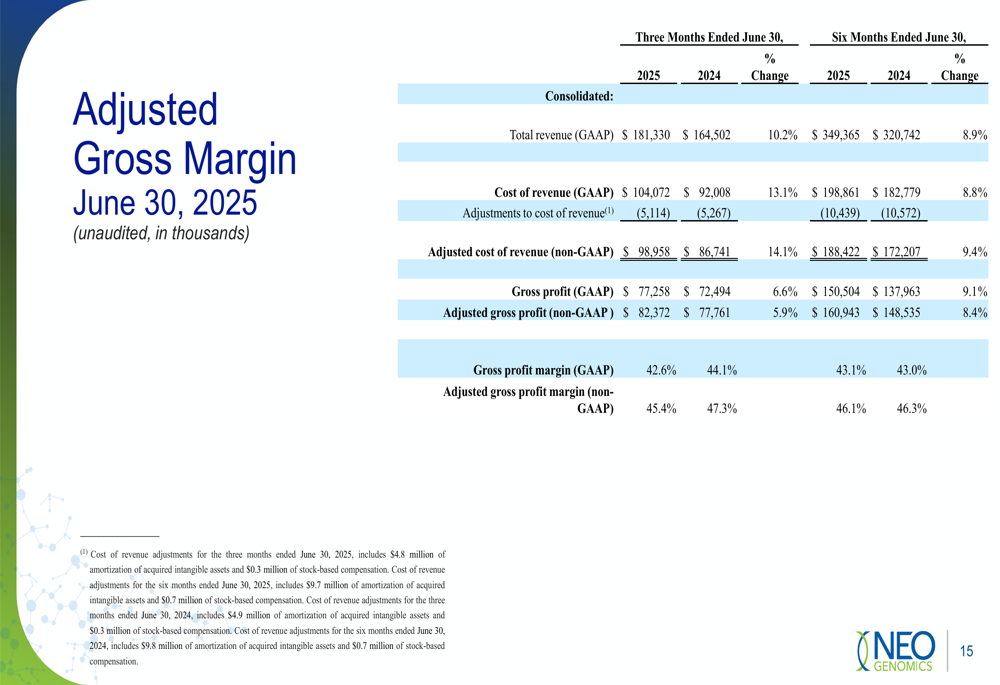

A closer examination of NeoGenomics’ financial performance reveals some concerning trends beneath the headline growth numbers. While revenue increased 10.2%, adjusted gross profit margin declined 184 basis points to 45.4%, primarily attributed to the Pathline acquisition.

The following reconciliation provides insight into the company’s margin performance:

The company’s cash position has deteriorated significantly, with cash and marketable securities totaling $163.7 million at quarter-end, down 57.8% from $387.8 million in the prior year. This decline reflects both operational needs and acquisition-related expenditures.

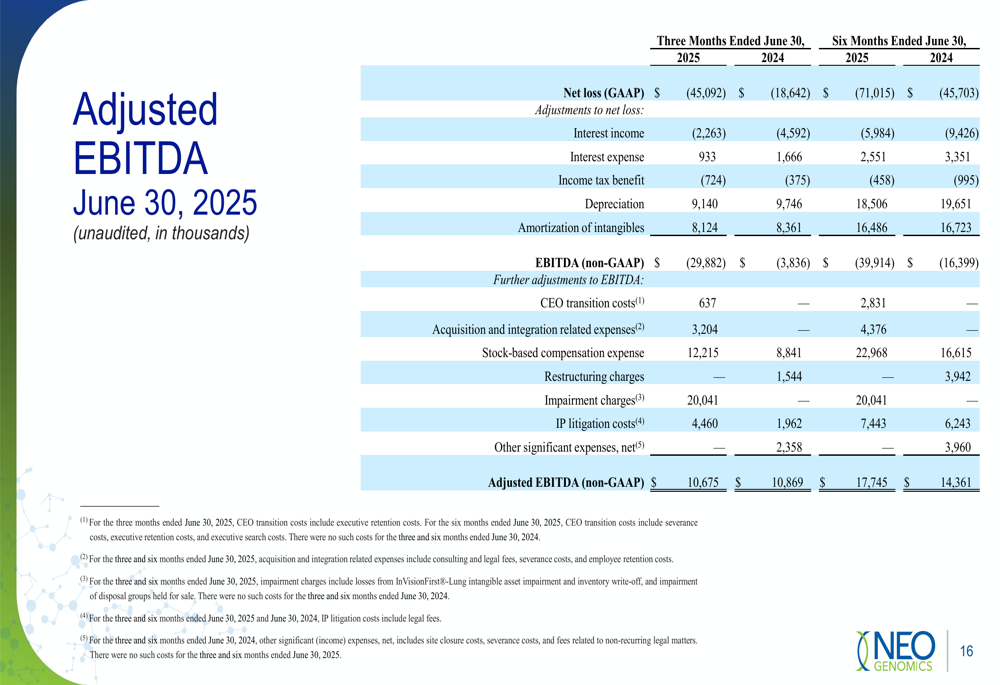

Despite reporting a net loss of $45.1 million, NeoGenomics achieved positive adjusted EBITDA of $10.7 million, marking its eighth consecutive quarter of positive earnings on this metric. The bridge from net loss to adjusted EBITDA is illustrated here:

The reconciliation reveals significant adjustments, including non-cash impairment charges, that transform the substantial GAAP loss into positive adjusted EBITDA.

Forward-Looking Statements

Management emphasized that despite the guidance reduction, NeoGenomics remains positioned as a double-digit growth company with opportunities to capture additional market share. The company highlighted its 16% growth in the clinical business and 23% growth in NGS revenue as indicators of underlying strength.

However, executives acknowledged macroeconomic pressures affecting the non-clinical business segments. The revised guidance suggests these challenges are more significant than previously anticipated, with potential implications for the company’s near-term growth and profitability targets.

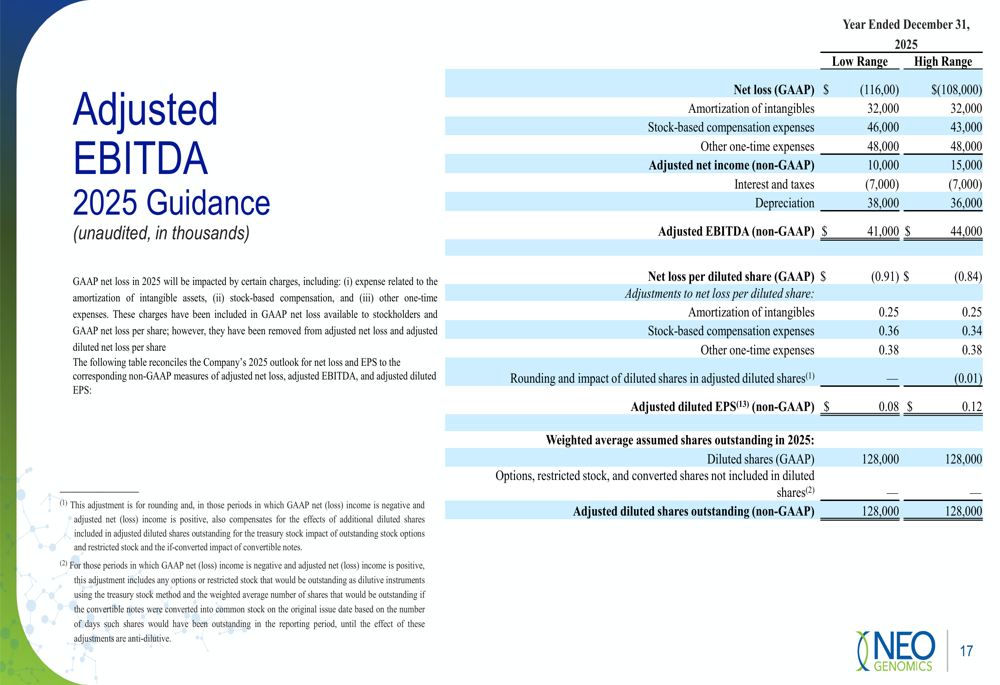

The company’s detailed 2025 EBITDA guidance breakdown provides insight into management’s expectations:

This outlook projects continued net losses on a GAAP basis despite positive adjusted EBITDA, indicating ongoing profitability challenges as the company balances growth investments with operational efficiency.

NeoGenomics’ ability to execute on its strategic initiatives, successfully integrate acquisitions, and navigate market pressures will be critical factors for investors to monitor in the coming quarters as the company works to deliver on its revised expectations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.