Oil prices rebound sharply on smaller-than-feared OPEC+ output hike

Introduction & Market Context

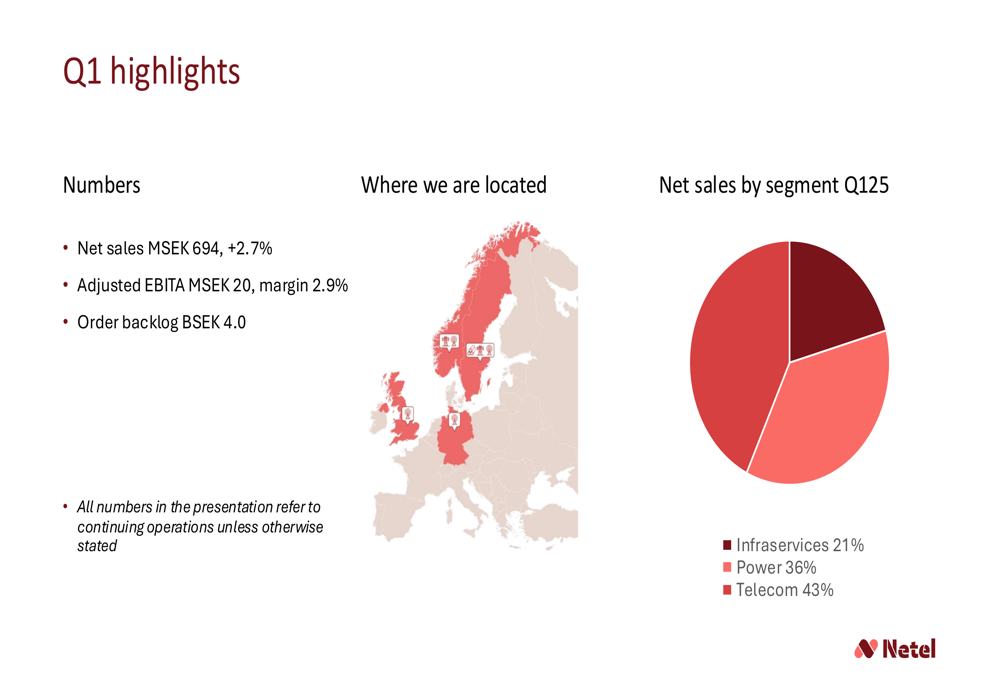

Netel Holding AB (STO:NETEL) presented its Q1 2025 results on April 25, showing modest organic growth of 2.7% amid a strategic shift that includes geographical expansion and revised financial targets. The infrastructure services provider, which focuses on telecom, power, and water/sewage sectors, reported net sales of MSEK 694 and an adjusted EBITA margin of 2.9%, slightly up from 2.8% in the same period last year.

The company is positioning itself to capitalize on what it identifies as strong mega trends in electrification, digitalization, and infrastructure modernization across its Nordic and German markets, while also announcing the planned divestment of its Finnish operations.

Quarterly Performance Highlights

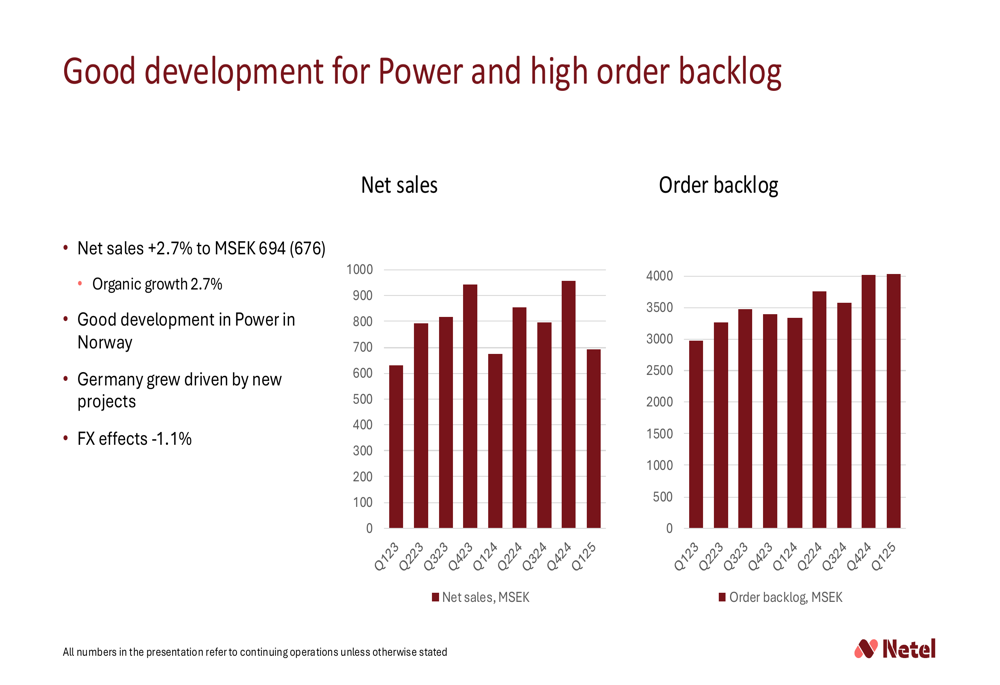

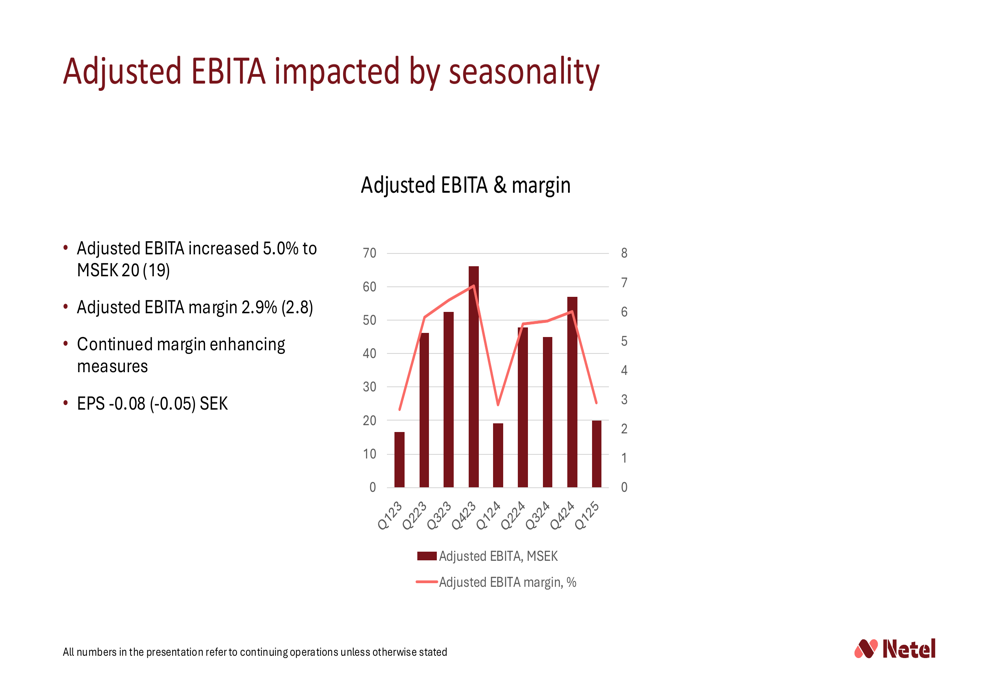

Netel reported organic growth of 2.7% in Q1 2025, with net sales reaching MSEK 694 compared to MSEK 676 in Q1 2024. The company’s order backlog remains strong at BSEK 4.0, providing visibility for future quarters. The adjusted EBITA increased by 5.0% to MSEK 20, with a margin improvement to 2.9% from 2.8% in the prior year.

As shown in the following chart of quarterly net sales and order backlog:

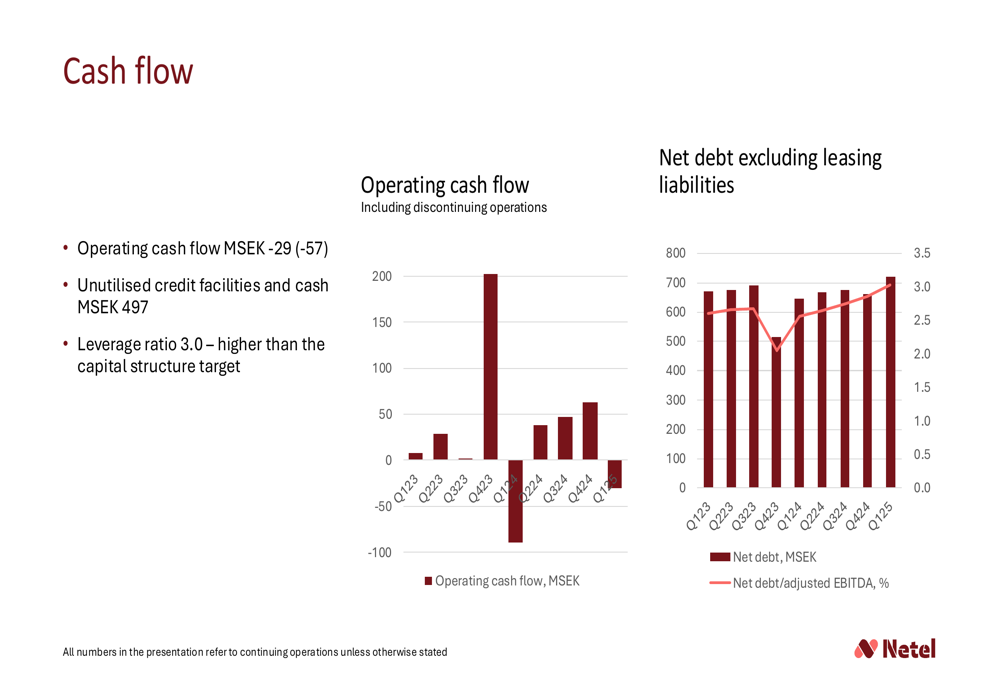

However, earnings per share deteriorated to -0.08 SEK from -0.05 SEK in Q1 2024. Operating cash flow, while still negative at MSEK -29, showed improvement compared to MSEK -57 in the same period last year. The company’s leverage ratio stands at 3.0, exceeding its capital structure target.

The following chart illustrates the adjusted EBITA and margin development:

Cash flow metrics and net debt are presented in this chart:

Netel’s revenue mix continues to be dominated by the Telecom (BCBA:TECO2m) segment, which accounts for 43% of net sales, followed by Power at 36% and Infraservices at 21%.

Segment Performance Analysis

Netel’s three business segments showed divergent performance in Q1 2025, with Power delivering strong sales growth but all segments experiencing margin pressure.

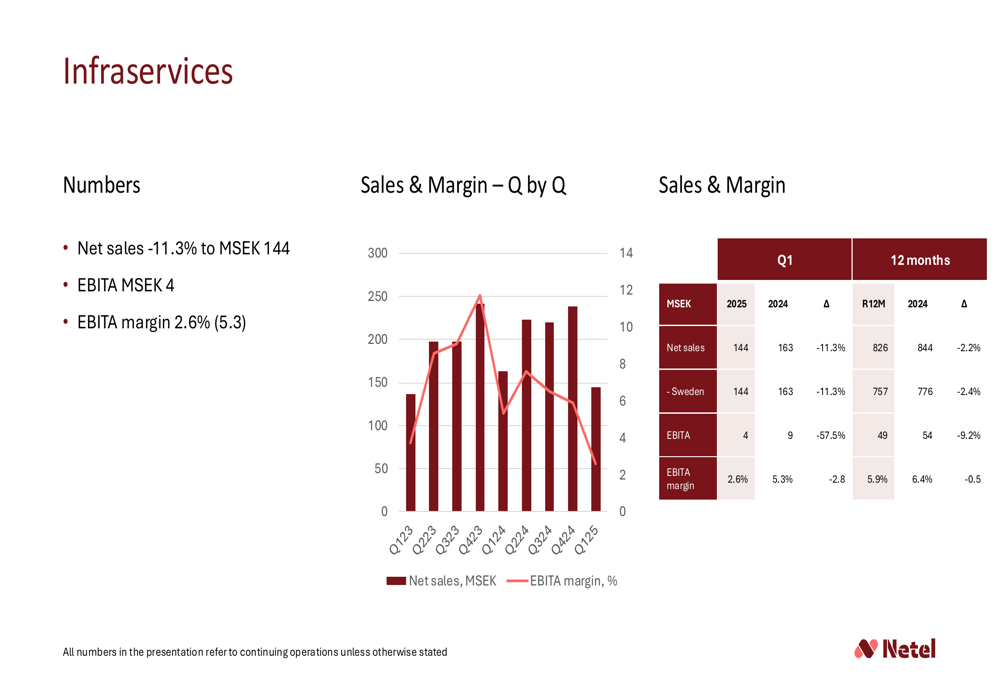

The Infraservices segment, which focuses on water and sewage infrastructure, saw an 11.3% decline in net sales to MSEK 144. More concerning was the significant drop in EBITA margin to 2.6% from 5.3% in the prior year period.

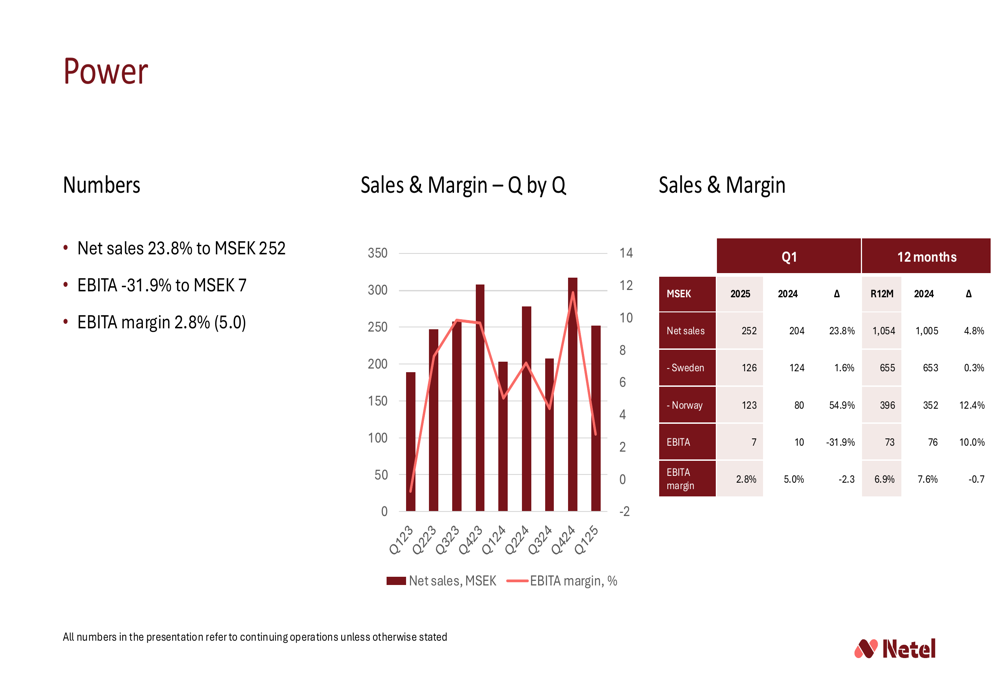

In contrast, the Power segment delivered impressive sales growth of 23.8% to MSEK 252, driven particularly by strong performance in Norway. However, EBITA declined by 31.9%, resulting in a margin compression to 2.8% from 5.0% in Q1 2024.

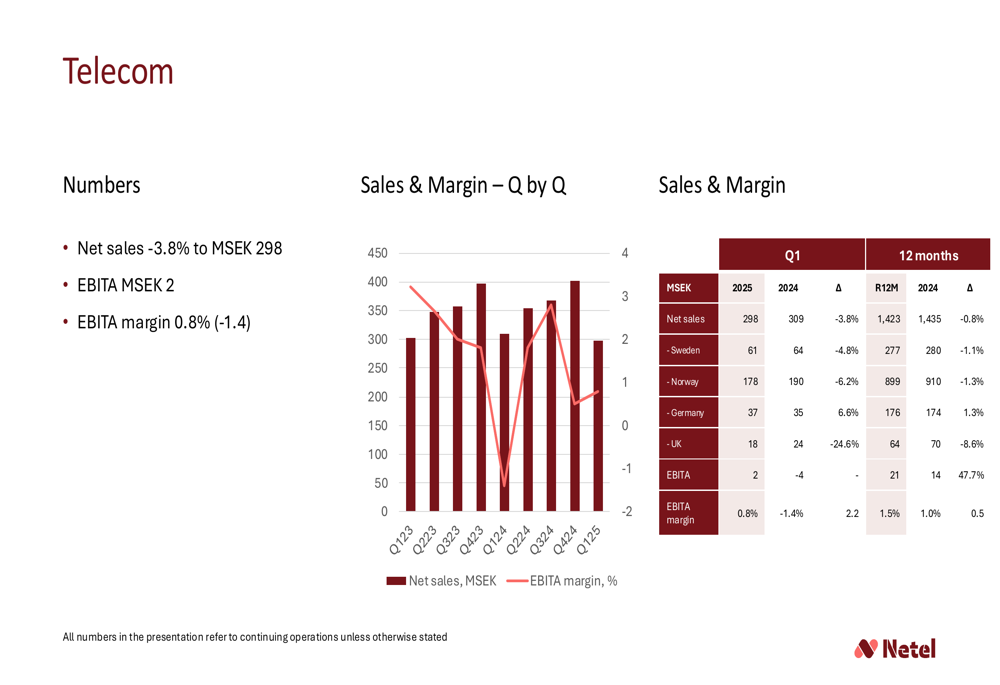

The Telecom segment experienced a 3.8% decline in net sales to MSEK 298. Despite the revenue contraction, the segment managed to improve its EBITA margin to 0.8% from -1.4% in the same period last year, indicating some progress in efficiency initiatives.

Strategic Initiatives & Outlook

Netel highlighted several strategic initiatives during its presentation, including new customer acquisitions and geographical expansions. The company secured new framework agreements across all three segments:

- In Infraservices, a new three-year framework agreement with Sigtuna Vatten & Renhållning for water and sewage network modernization

- In Power, a framework agreement with Glitre Nett in Norway, establishing a new organization in Mandal, Agder County

- In Telecom, an expanded framework agreement with Tele2 (ST:TEL2b) in Sweden covering installation, service, and maintenance of broadband networks

The company also mentioned ongoing implementation of digital tools and systems, positioning sustainability as a competitive advantage, and noted it is not exposed to potential trade tariffs.

Regarding the Finnish operations, Netel confirmed that the divestment is proceeding according to plan and is expected to be completed during 2025. The Finnish business reported net sales of MSEK 34 in Q1 2025, down from MSEK 38 in the prior year, with a net loss after tax of MSEK 4.

Revised Financial Targets

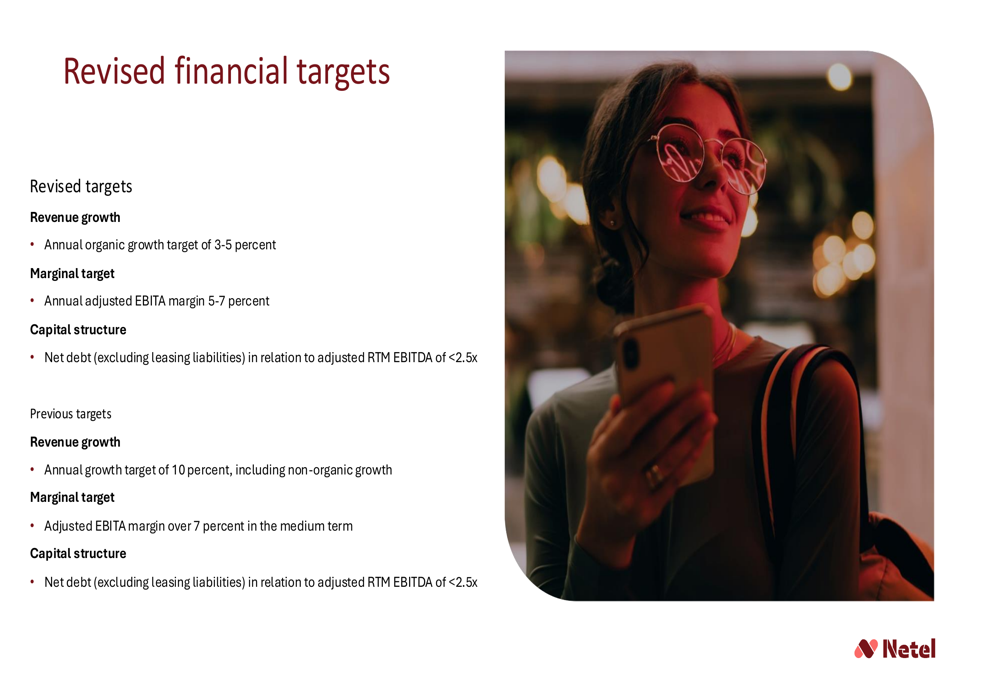

Perhaps the most significant announcement in the presentation was Netel’s downward revision of its financial targets. The company has reduced its annual growth target from 10% (which included non-organic growth) to 3-5% organic growth. Similarly, the adjusted EBITA margin target has been lowered from "over 7% in the medium term" to 5-7%.

The following slide details both the revised and previous financial targets:

The capital structure target remains unchanged, with net debt (excluding leasing liabilities) in relation to adjusted RTM EBITDA targeted at less than 2.5x, though the current ratio of 3.0 exceeds this target.

These revised targets suggest a more conservative outlook from management, focusing on organic growth and operational efficiency rather than the previous emphasis on acquisitions. The company’s current performance, with 2.9% EBITA margin, indicates significant work ahead to reach even the lower end of the revised 5-7% margin target.

As Netel celebrates its 25th anniversary in 2025, the company faces both challenges and opportunities in its quest to strengthen its position in the Nordic and German infrastructure markets while improving profitability and cash flow generation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.