European stocks drop sharply on continued tech valuation concerns

Introduction & Market Context

NETSTREIT Corp (NYSE:NTST) released its Q2 2025 investor presentation, highlighting the company’s portfolio performance, investment activity, and financial position. The presentation comes after the company’s Q1 2025 earnings release, which showed mixed results with an EPS miss but strong revenue growth. Despite falling short of EPS expectations in Q1, NETSTREIT’s stock has shown resilience, trading at $17.95 as of the most recent close.

The net lease REIT continues to focus on necessity-based, discount, and service-oriented retail tenants, positioning itself as a defensive play in the retail real estate sector. With interest rates and economic conditions creating both challenges and opportunities, NETSTREIT emphasized its disciplined approach to growth and portfolio management.

Portfolio Highlights

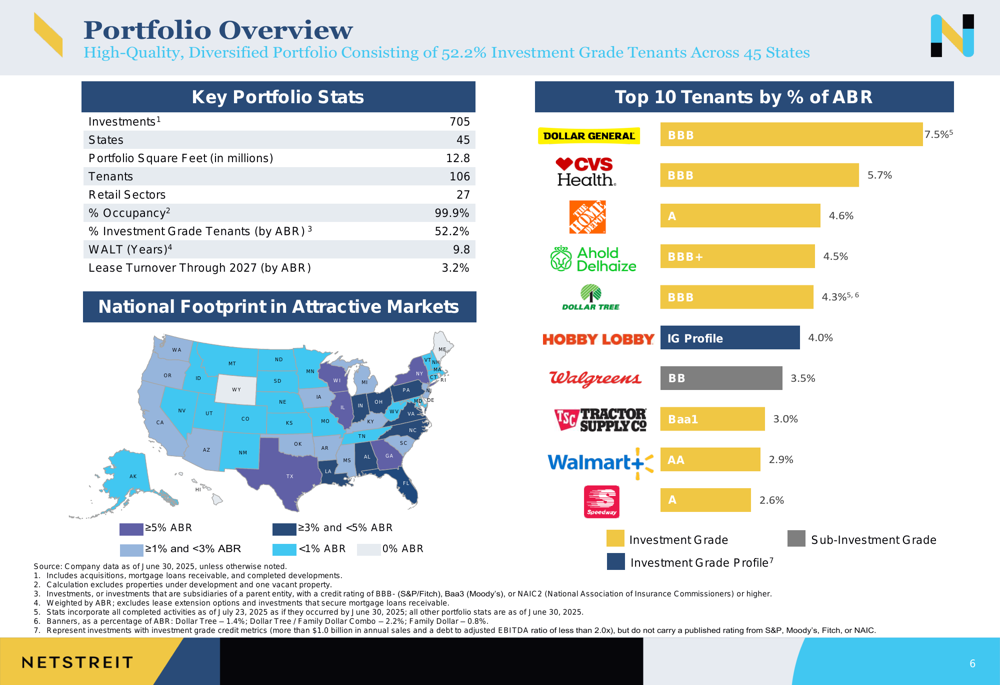

NETSTREIT’s portfolio demonstrates strong fundamentals with a near-perfect occupancy rate and diversified tenant base. As of Q2 2025, the company owns 705 properties across 45 states, totaling 12.8 million square feet. The portfolio maintains a 99.9% occupancy rate with a weighted average lease term of 9.8 years and minimal near-term lease expirations, with only 3.2% of leases set to expire through 2027.

As shown in the following portfolio overview, the company has diversified its tenant base across 106 tenants in 27 retail sectors, with investment grade tenants accounting for 52.2% of annualized base rent (ABR):

The top 10 tenants represent 42.6% of ABR, led by Dollar General (NYSE:DG) (7.5%), CVS Health (NYSE:CVS) (5.7%), and The Home Depot (NYSE:HD) (4.6%). This concentration is within the company’s target of keeping top 10 tenants below 50% of total ABR, demonstrating a balanced approach to tenant exposure.

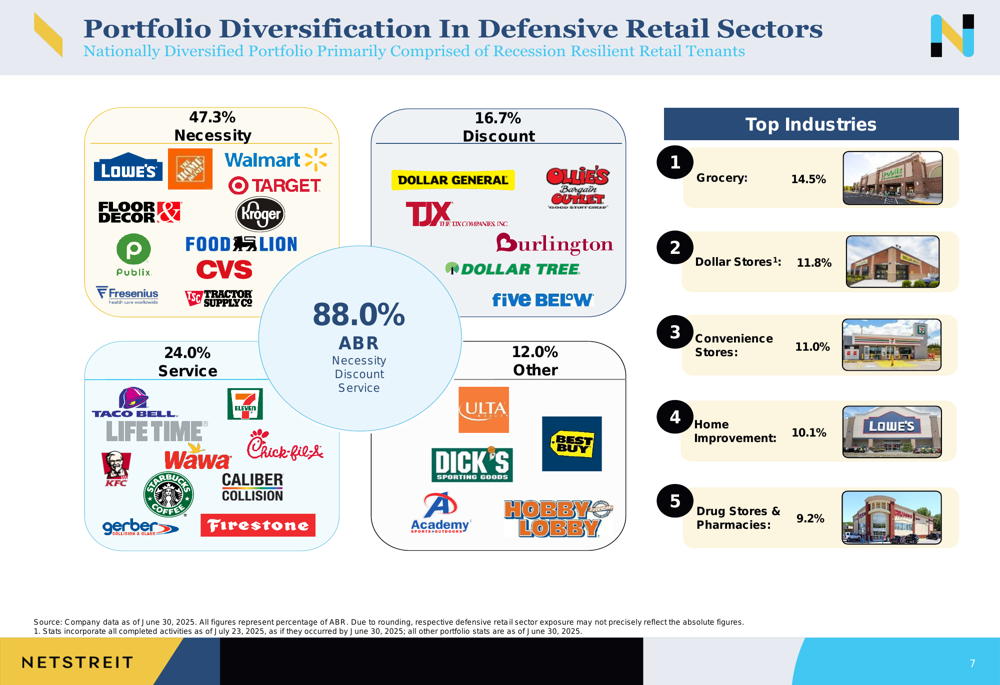

NETSTREIT’s portfolio is strategically focused on defensive retail sectors, with 47.3% in necessity-based tenants, 16.7% in discount retailers, and 24.0% in service-oriented tenants. This positioning aligns with the company’s emphasis on e-commerce-resistant retail categories that have demonstrated resilience across economic cycles.

Investment Strategy & Recent Activity

The company’s investment approach focuses on properties with strong tenant credit profiles, solid real estate fundamentals, and healthy unit-level profitability. NETSTREIT employs what it calls "Bell Curve Investing," targeting inefficiently priced assets that may not be highly marketed or may involve transaction structures that limit the buyer pool.

In Q2 2025, NETSTREIT completed 32 investments with an average size of $3.7 million and a weighted average cash cap rate of 7.8%. This represents a continuation of the company’s strong investment pace, which has averaged $104 million in net investments per quarter since Q3 2020.

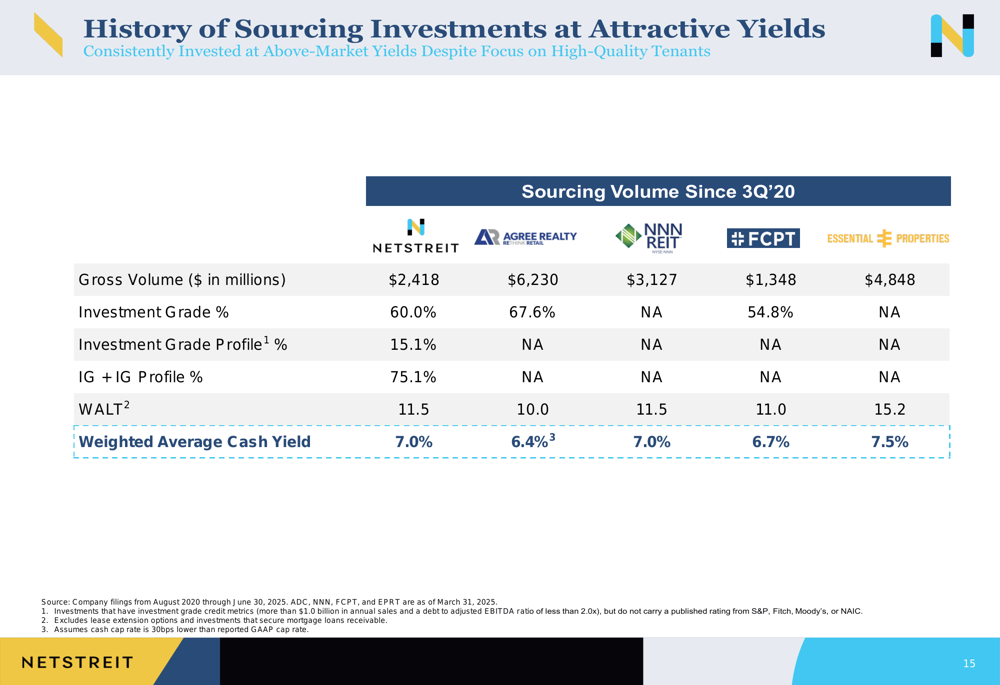

The following chart illustrates the company’s history of sourcing investments at attractive yields compared to peers:

Since Q3 2020, NETSTREIT has maintained a weighted average cash yield of 7.0% on its investments, outperforming peers like Agree Realty (NYSE:ADC) (6.4%) and FCPT (6.7%). The company has also been active in portfolio optimization, completing $60.4 million in dispositions in Q2 2025 at a 6.5% cash cap rate.

Portfolio Health & Credit Quality

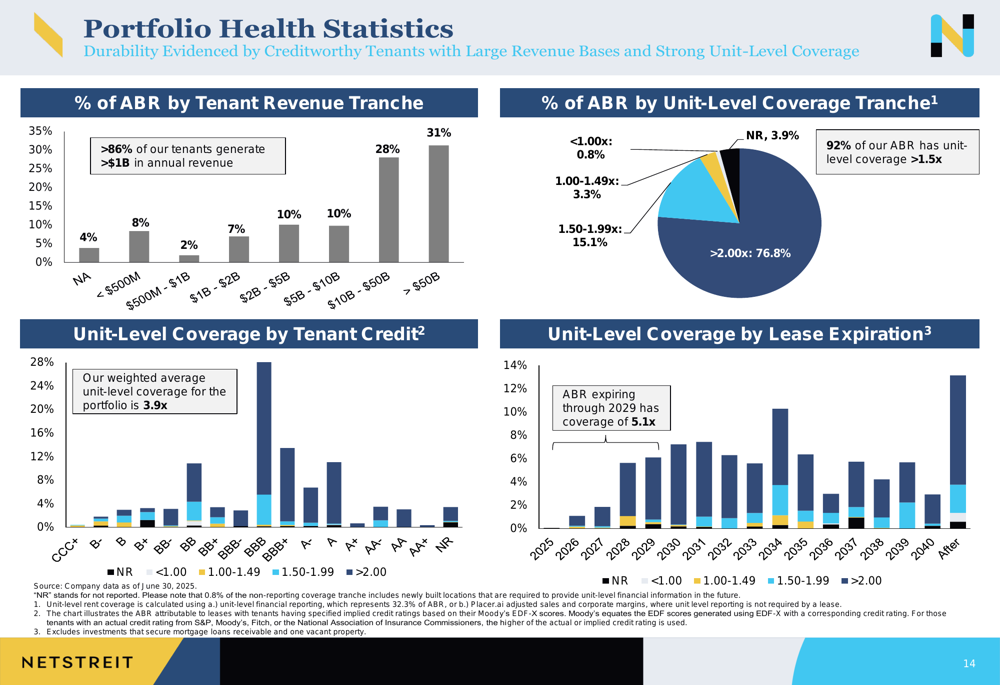

NETSTREIT emphasizes strong tenant credit underwriting and unit-level profitability in its investment decisions. The company reported that 92% of its ABR has unit-level coverage exceeding 1.5x, indicating strong tenant performance at the property level. Additionally, more than 86% of tenants generate over $1 billion in annual revenue.

The following chart provides a detailed breakdown of the portfolio’s health statistics:

The company has experienced minimal credit issues, with only one portfolio tenant (Big Lots (NYSE:BIG)) experiencing a credit event since the company’s initial equity raise in Q4 2019. This event is projected to cause $404,000 in lost ABR, representing just 4 basis points of annualized credit loss over 5.5 years.

Financial Position

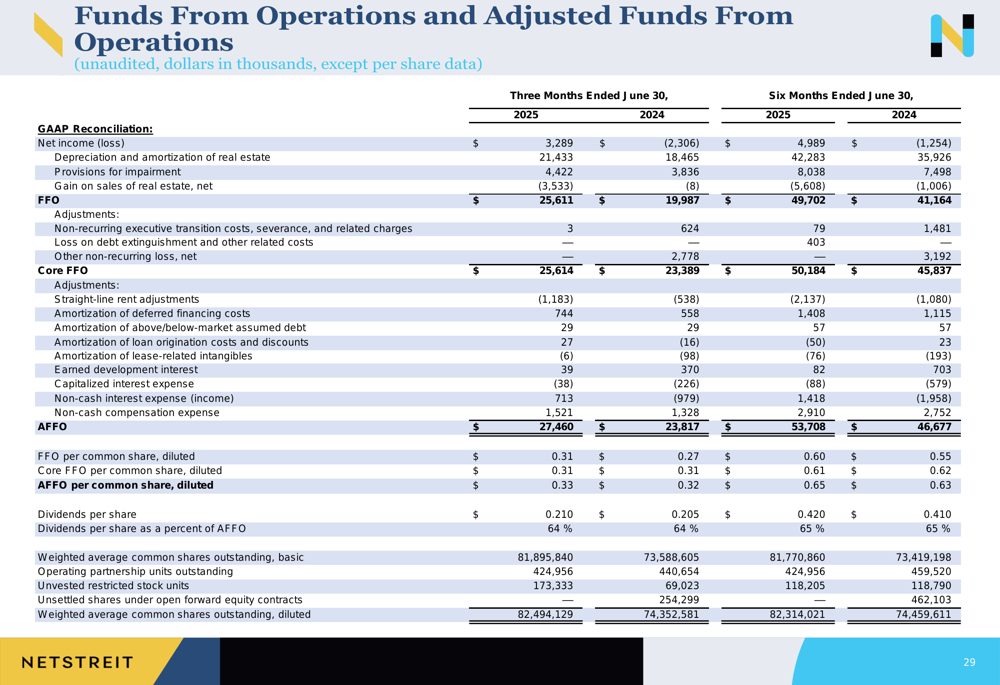

NETSTREIT maintains a conservative balance sheet with $594 million in total liquidity and a debt maturity schedule that extends to 2030, with no significant maturities until 2028. The company’s leverage ratio stands at 4.6x adjusted net debt to annualized adjusted EBITDAre, within its target range of 4.5x to 5.5x.

The following financial metrics highlight the company’s performance in terms of funds from operations (FFO) and adjusted funds from operations (AFFO):

This financial discipline aligns with management’s comments during the Q1 2025 earnings call, where CEO Mark Mannheimer emphasized, "We will not sacrifice our balance sheet for growth, nor will we grow for the sake of asset growth without an appropriate level per share earnings growth."

Competitive Positioning

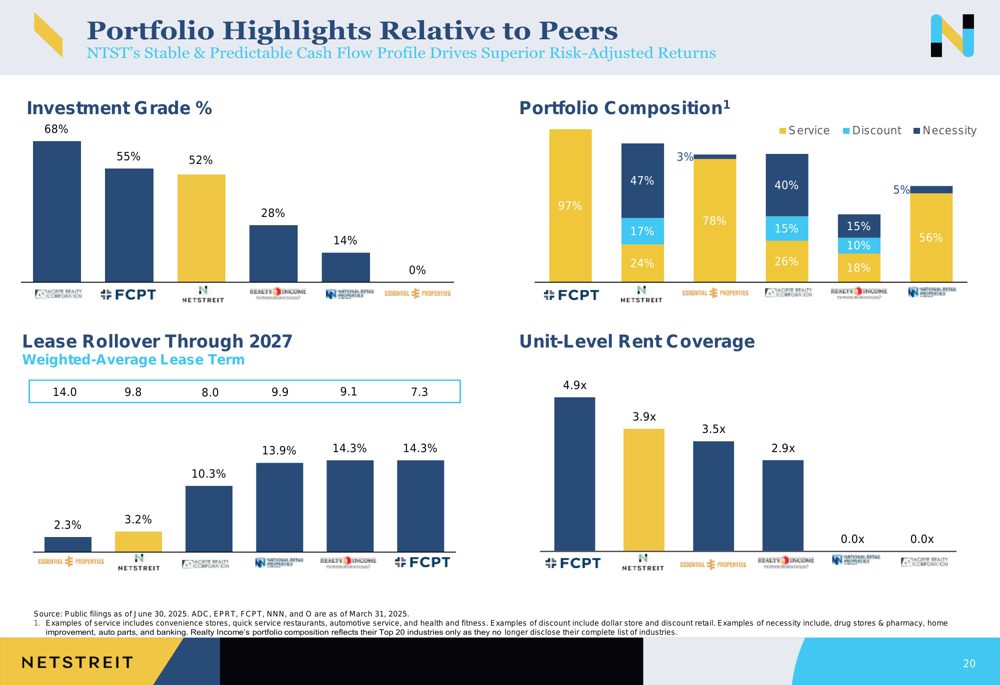

NETSTREIT positions itself as a defensive net lease REIT with a focus on high-quality tenants and properties. The company’s portfolio metrics compare favorably to peers in several key areas, as illustrated in the following comparison:

While NETSTREIT’s investment grade percentage (52%) is lower than some competitors like Agree Realty (68%), the company maintains strong unit-level rent coverage at 3.9x. The company’s weighted average lease term of 9.9 years is shorter than Agree Realty’s 14 years, but NETSTREIT compensates with higher cash yields on new investments.

The company’s earnings growth trajectory also compares favorably to peers:

Outlook & Forward Guidance

Based on the Q1 2025 earnings report, NETSTREIT has raised its AFFO per share guidance to $1.28-$1.30 for 2025, signaling confidence in its operational strategies and investment plans. The company anticipates net investment activity between $75 million and $125 million for the year, with an expected rent loss of approximately 75 basis points.

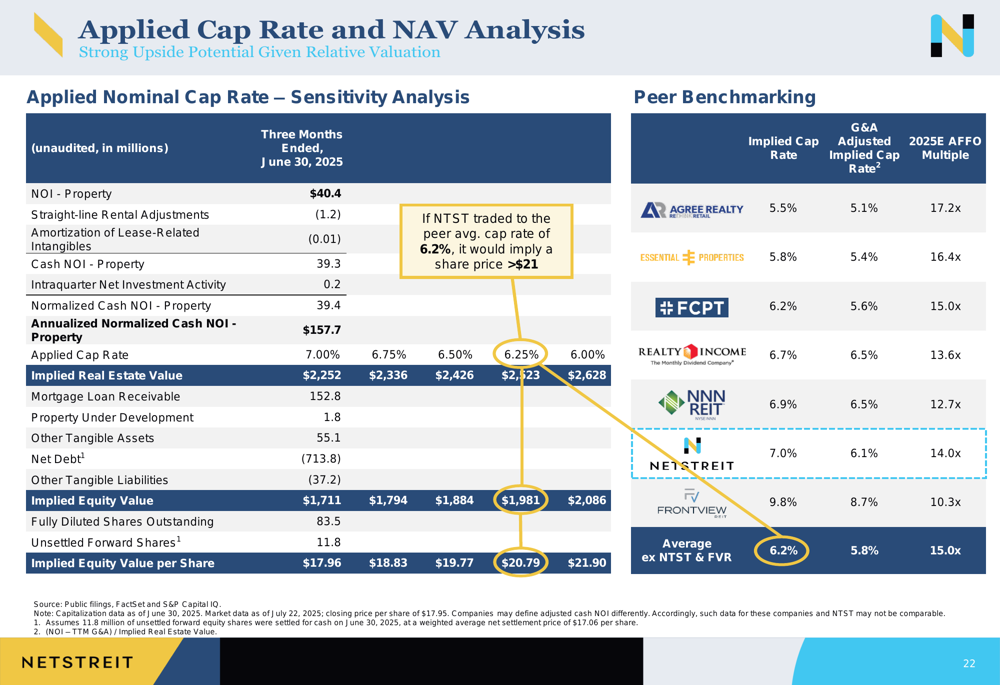

The company’s NAV analysis suggests a target share price above $21, representing potential upside from the current trading level of $17.95:

Challenges & Risks

Despite the overall positive presentation, NETSTREIT faces several challenges. The Q1 2025 earnings showed an EPS miss of $0.02 versus the expected $0.06, indicating pressure on profitability despite strong revenue growth. The company’s recurring G&A expenses increased by 5% year-over-year to $5.1 million in Q1, highlighting the need for cost management.

Additionally, the company’s exposure to tenants like Dollar General (7.5% of ABR) and CVS Health (5.7% of ABR) represents concentration risk, though this is within the company’s target limits. The shift toward lower investment grade percentage in recent acquisitions (25.7% IG+IGP in Q2 2025 versus 97.2% in Q3 2023) may also signal a changing risk profile in the pursuit of higher yields.

As noted in the Q1 earnings call, tariff uncertainties and broader economic conditions pose challenges to market conditions, potentially impacting investment decisions and tenant performance.

Conclusion

NETSTREIT’s Q2 2025 presentation portrays a company with a resilient portfolio, disciplined investment approach, and strong financial position. The 99.9% occupancy rate and 7.8% cash cap rate on new investments highlight the company’s ability to source attractive deals in the competitive net lease space.

While the Q1 2025 earnings results showed some challenges in profitability, the company’s revenue outperformance and raised guidance suggest confidence in its strategic direction. As NETSTREIT continues to execute its investment strategy and manage its portfolio, investors will be watching for improvements in bottom-line performance to match the company’s strong top-line growth and portfolio metrics.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.