CAC 40 falls after French Prime Minister resigns

Neurocrine Biosciences Inc (NASDAQ:NBIX) reported strong quarter-over-quarter growth in its Q2 2025 earnings presentation on July 30, showing a significant rebound from its Q1 performance. The company narrowed its full-year INGREZZA sales guidance while highlighting progress across its expanding neuroscience pipeline.

Quarterly Performance Highlights

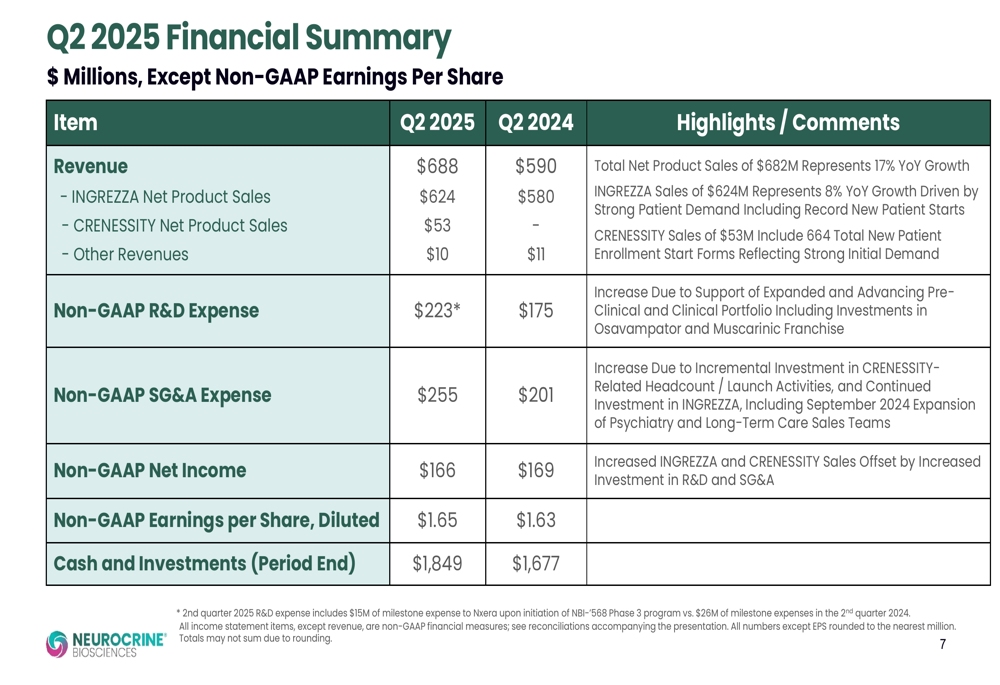

Neurocrine reported total net product sales of $682 million for Q2 2025, representing a 21% increase quarter-over-quarter and a 17% increase year-over-year. INGREZZA, the company’s lead product for tardive dyskinesia and Huntington’s disease chorea, generated $624 million in net sales, up 15% from Q1 and 8% from the same period last year.

The company’s newer product, CRENESSITY for congenital adrenal hyperplasia, contributed $53 million in net sales with 664 total new patient enrollment forms, showing promising early adoption since its recent launch.

As shown in the following financial summary:

"We’re executing from a position of strength," CFO Matt Abernathy had stated during the Q1 earnings call, a sentiment that appears validated by the Q2 results. The company’s stock rose 1.12% in after-hours trading following the announcement, reaching $135.69, according to market data.

Detailed Financial Analysis

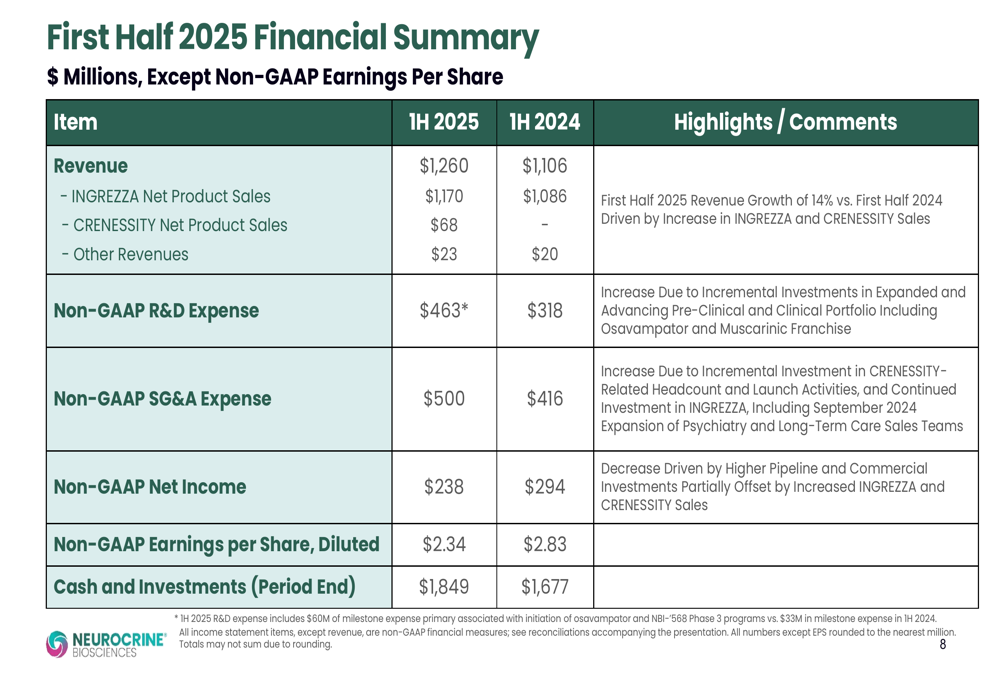

For the first half of 2025, Neurocrine reported total revenue of $1.26 billion compared to $1.11 billion in the first half of 2024, representing a 14% increase. INGREZZA net product sales for the first half reached $1.17 billion, up from $1.09 billion in the same period last year.

The company’s expenses have increased significantly year-over-year, with non-GAAP R&D expenses rising to $223 million in Q2 2025 from $175 million in Q2 2024, and non-GAAP SG&A expenses increasing to $255 million from $201 million. Despite these higher expenses, non-GAAP net income remained relatively stable at $166 million compared to $169 million in Q2 2024, with diluted earnings per share slightly improving to $1.65 from $1.63.

The first half financial performance is detailed in the following summary:

Neurocrine maintains a strong balance sheet with $1.85 billion in cash and investments as of June 30, 2025, up from $1.68 billion a year earlier. This robust financial position supports the company’s ongoing R&D investments and commercial expansion.

Strategic Initiatives

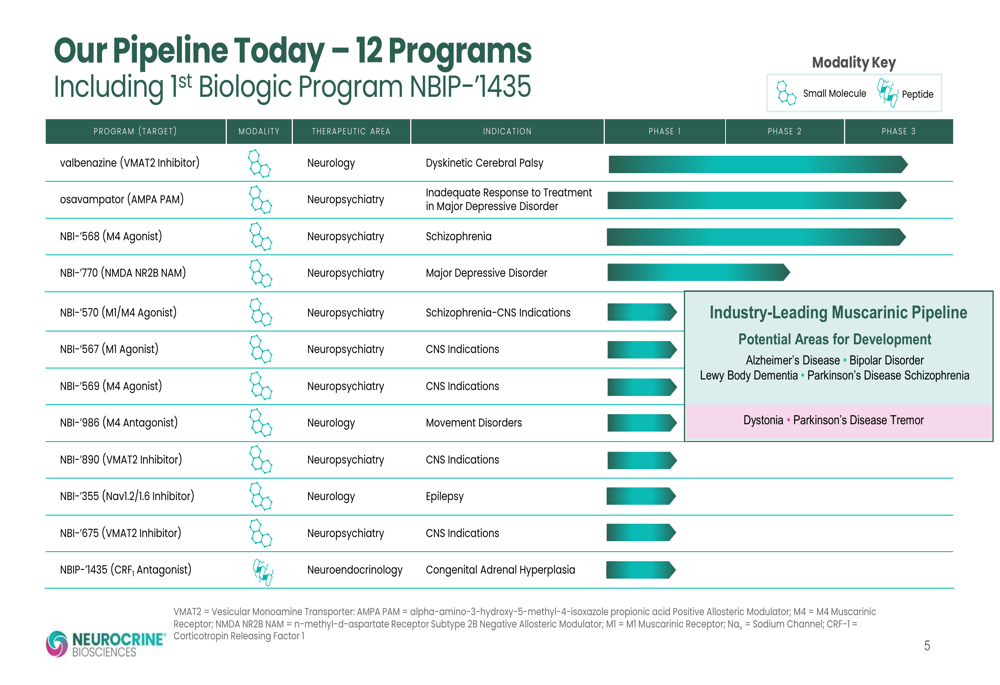

Neurocrine’s pipeline has expanded to include 12 programs across neurology, neuroendocrinology, neuropsychiatry, and neuroimmunology, including the company’s first biologic program. The comprehensive pipeline overview demonstrates the company’s commitment to neuroscience drug development:

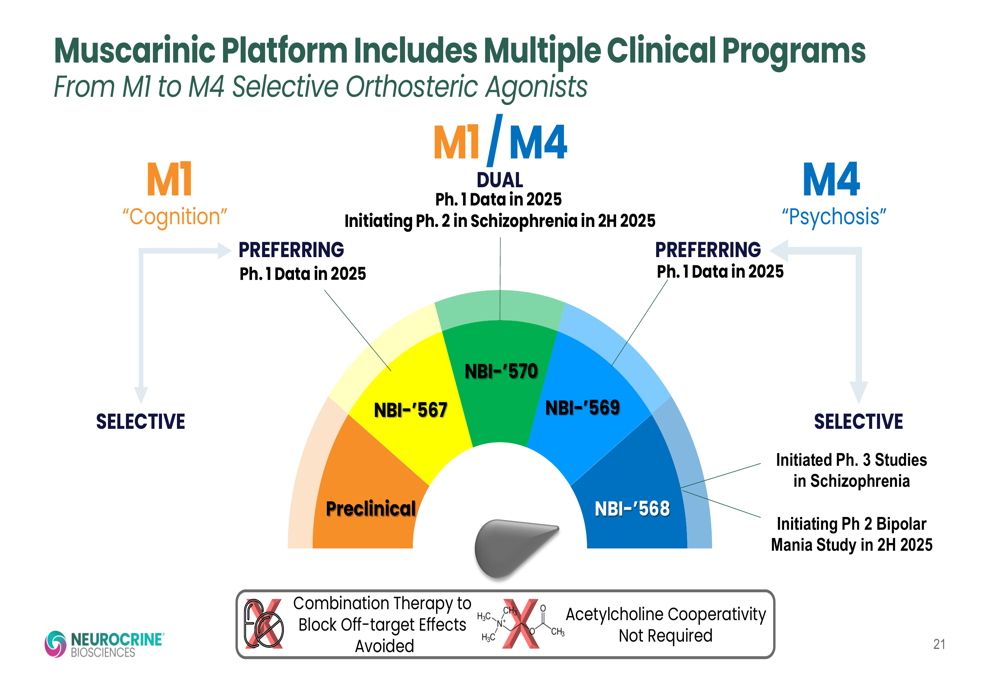

A key focus area is the muscarinic platform, which includes multiple clinical programs targeting different receptors for various neurological conditions:

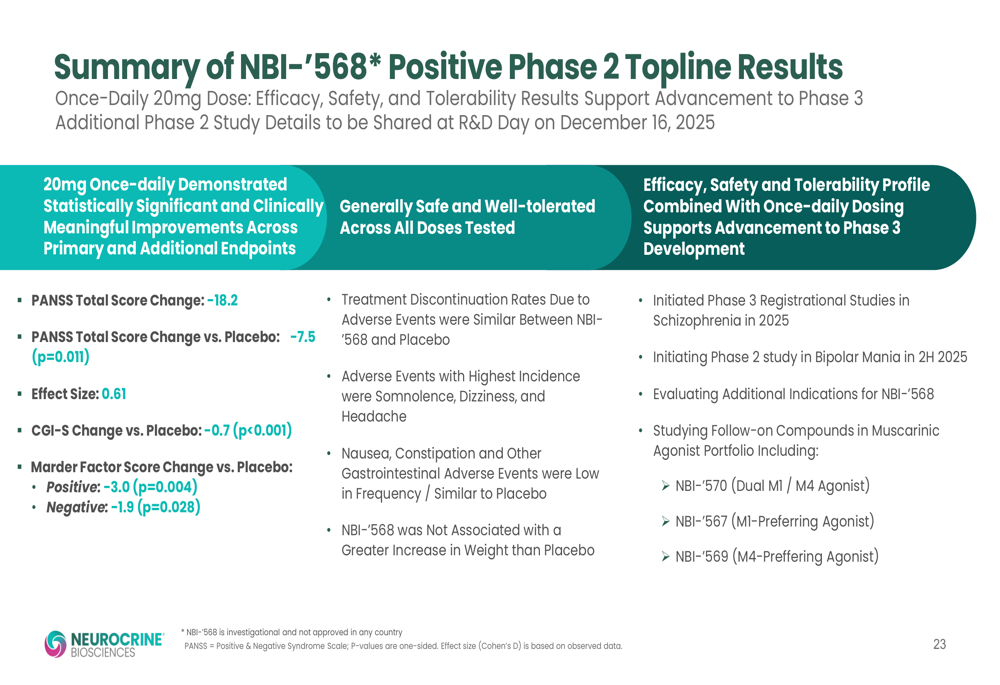

The company has made significant progress with NBI-568, its muscarinic agonist for schizophrenia. Phase 2 results were positive, showing statistically significant improvements across primary and additional endpoints with a favorable safety profile:

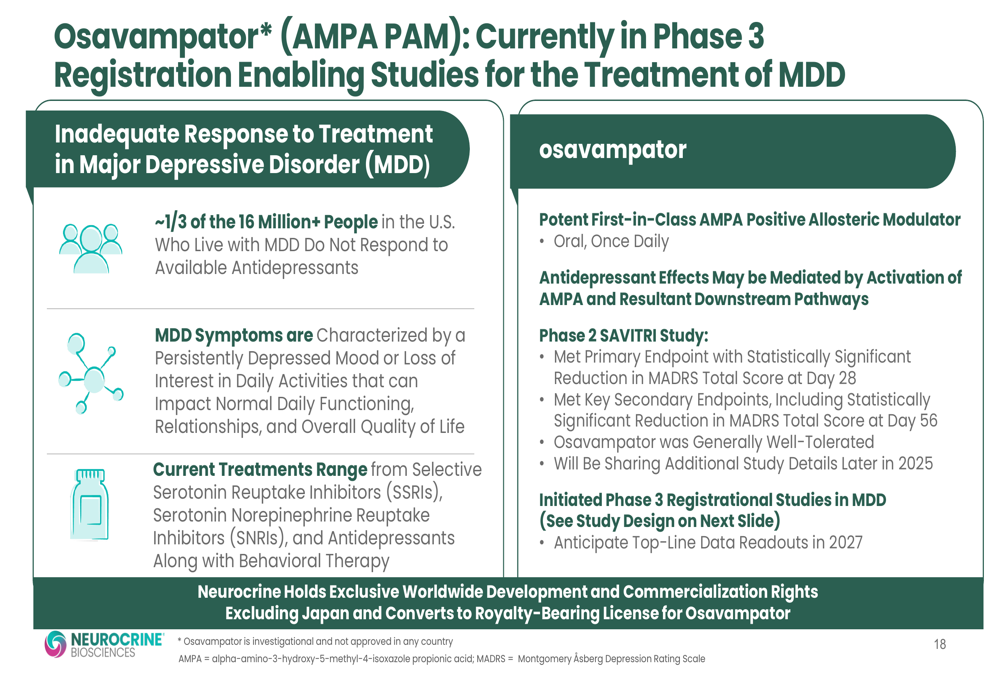

Neurocrine is also advancing Osavampator, a potential treatment for Major Depressive Disorder (MDD). The company has initiated Phase 3 studies following positive Phase 2 results that met both primary and key secondary endpoints:

Forward-Looking Statements

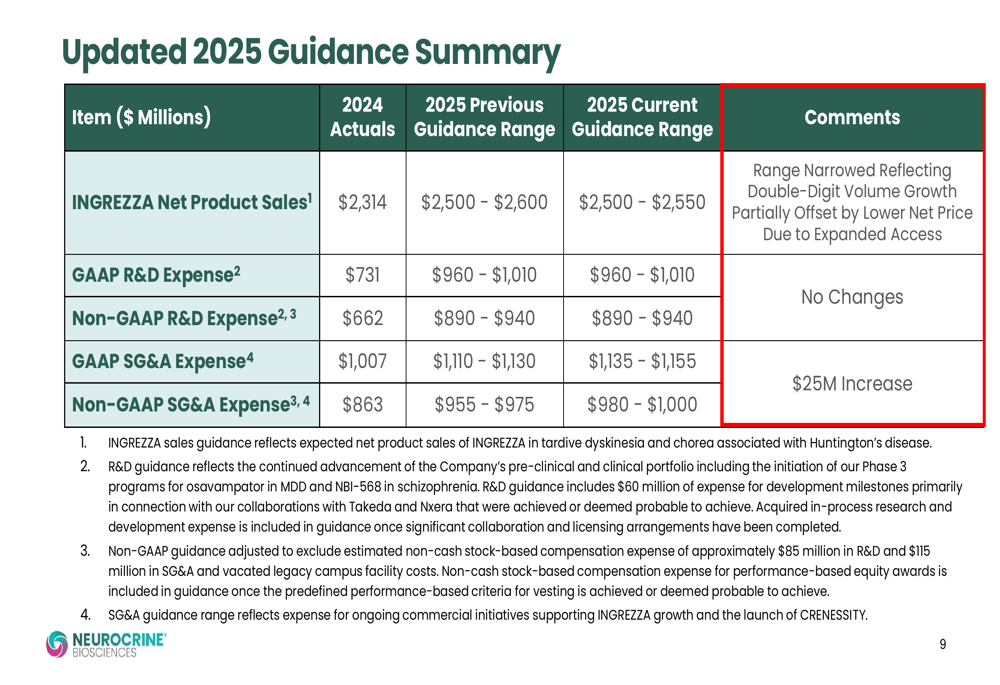

Neurocrine has narrowed its 2025 INGREZZA net product sales guidance from $2.5-$2.6 billion to $2.5-$2.55 billion, suggesting confidence in meeting but not exceeding previous projections. The company has also slightly increased its SG&A expense guidance while maintaining its R&D expense outlook:

Key upcoming milestones include Phase 2 study initiations, topline data expected in Q4 2025, Phase 1 muscarinic agonist results, and an R&D Day scheduled for December 16, 2025, at the company’s headquarters in San Diego.

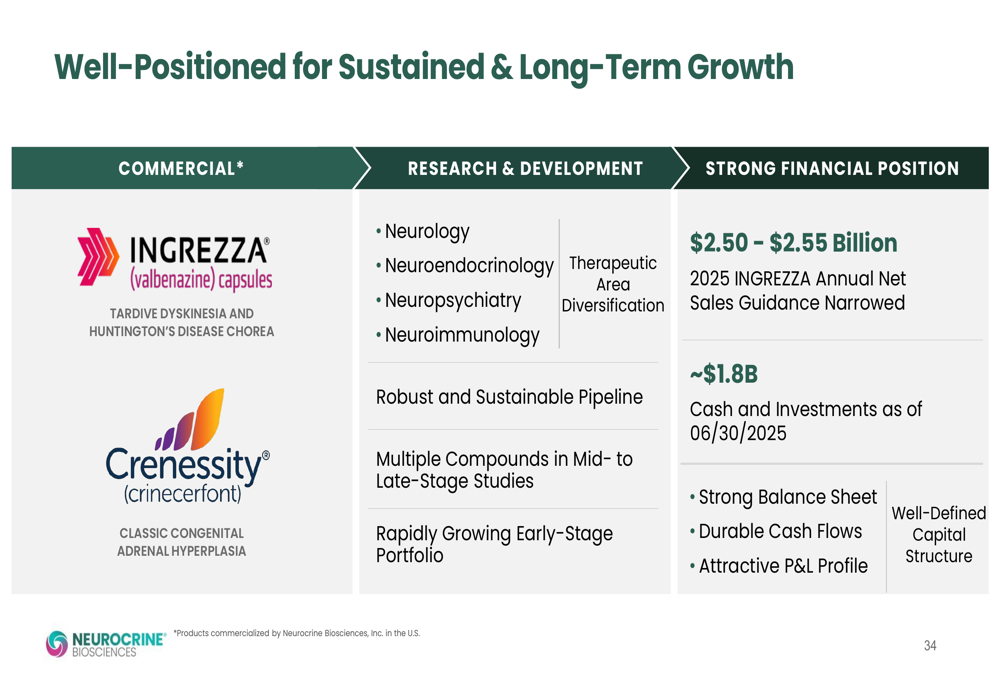

The company’s long-term strategy focuses on sustainable growth through commercial expansion, pipeline advancement, and maintaining financial strength:

This Q2 presentation demonstrates a significant improvement from Q1 2025, when Neurocrine missed earnings expectations with an EPS of $0.70 versus the forecasted $0.77 and revenue of $572.6 million below the anticipated $593.71 million. The strong quarter-over-quarter growth suggests the company has successfully addressed the challenges that affected its Q1 performance.

With multiple late-stage programs advancing and continued commercial growth of its approved products, Neurocrine appears well-positioned to maintain its leadership in the neuroscience space despite increasing R&D and commercial expenses. The narrowed guidance reflects a prudent approach to financial projections while the company continues to invest in its expanding pipeline.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.