Google launches Gemini Enterprise AI platform for workplace automation

Introduction & Market Context

Newmont Goldcorp Corp (NYSE:NEM) presented its second quarter 2025 results on July 24, 2025, highlighting strong financial performance despite facing operational challenges at its Red Chris project. The gold mining giant reported robust free cash flow generation and continued its commitment to shareholder returns through dividends and share repurchases.

The presentation comes as Newmont’s stock has performed well year-to-date, with fundamentals showing the stock trading at $61.42 as of the presentation date, near its 52-week high of $62.56. In after-hours trading following the presentation, the stock declined slightly by 1.09% to $60.75.

Quarterly Performance Highlights

Newmont delivered strong operational and financial results in Q2 2025, remaining on track to meet its full-year commitments across safety culture, stable operations, and capital returns.

As shown in the following highlights from the company’s presentation:

The company produced 1.5 million ounces of gold and 36,000 tonnes of copper during the quarter. This solid operational performance generated $1.7 billion in free cash flow, enabling Newmont to return $1.0 billion to shareholders while also retiring $372 million of debt. The board approved an additional $3.0 billion share repurchase program, bringing the total authorization to $6.0 billion.

However, the quarter was not without challenges. On July 22, 2025, two fall of ground incidents occurred in the underground work area of the non-producing Red Chris project in British Columbia, Canada. Emergency response protocols were immediately activated, and operations at Red Chris have been suspended while the company focuses on safely recovering team members.

Operational Performance

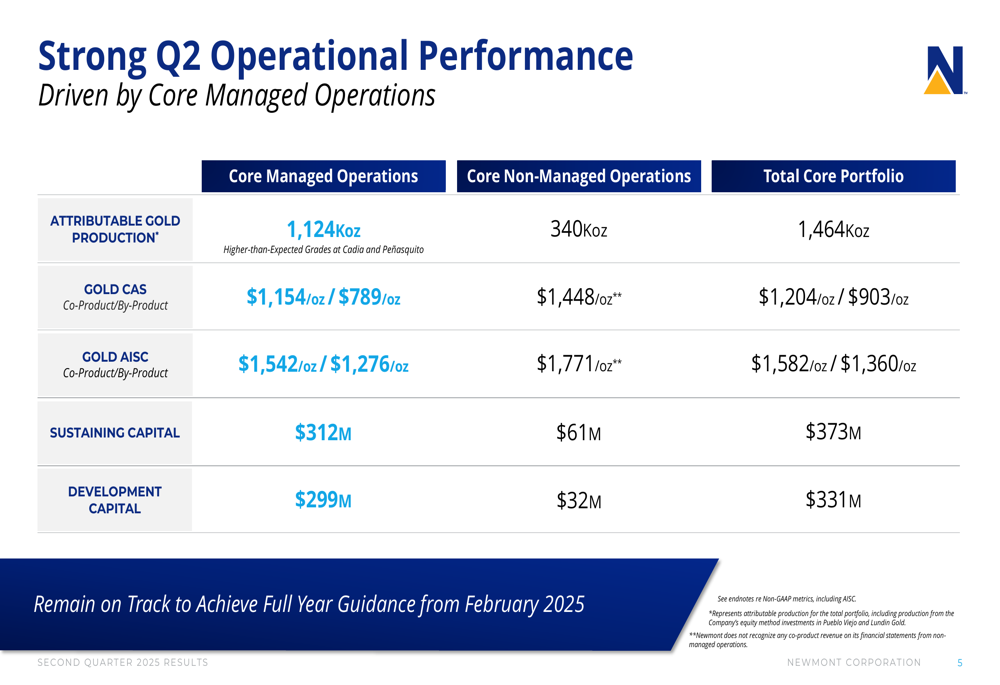

Newmont’s core managed operations drove the company’s strong Q2 performance, as detailed in the following operational breakdown:

The core portfolio delivered 1,464,000 ounces of attributable gold production, with core managed operations contributing 1,124,000 ounces and non-managed operations adding 340,000 ounces. Gold costs applicable to sales (CAS) for the total core portfolio were $1,204 per ounce on a co-product basis and $903 per ounce on a by-product basis. All-in sustaining costs (AISC) were $1,582 per ounce (co-product) and $1,360 per ounce (by-product).

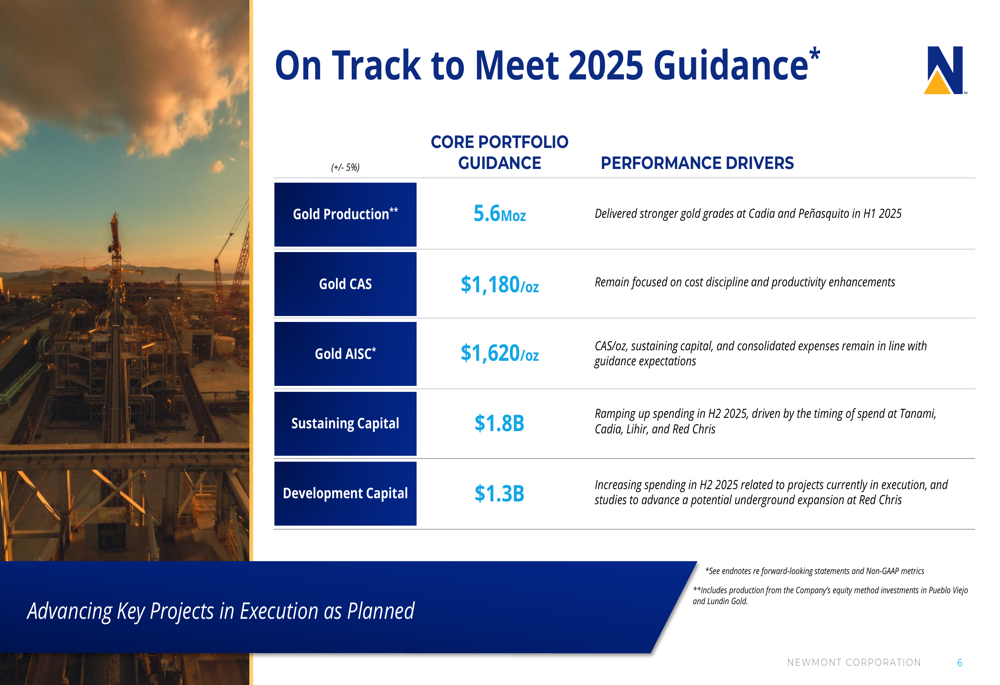

The company emphasized that it remains on track to achieve its full-year guidance provided in February 2025, with the following performance drivers highlighted:

Newmont delivered stronger gold grades at Cadia and Peñasquito in the first half of 2025, contributing to solid production figures. The company continues to focus on cost discipline and productivity enhancements to maintain its cost guidance. Capital expenditures are expected to increase in the second half of 2025, particularly for sustaining capital at Tanami, Cadia, Lihir, and Red Chris.

Financial Results

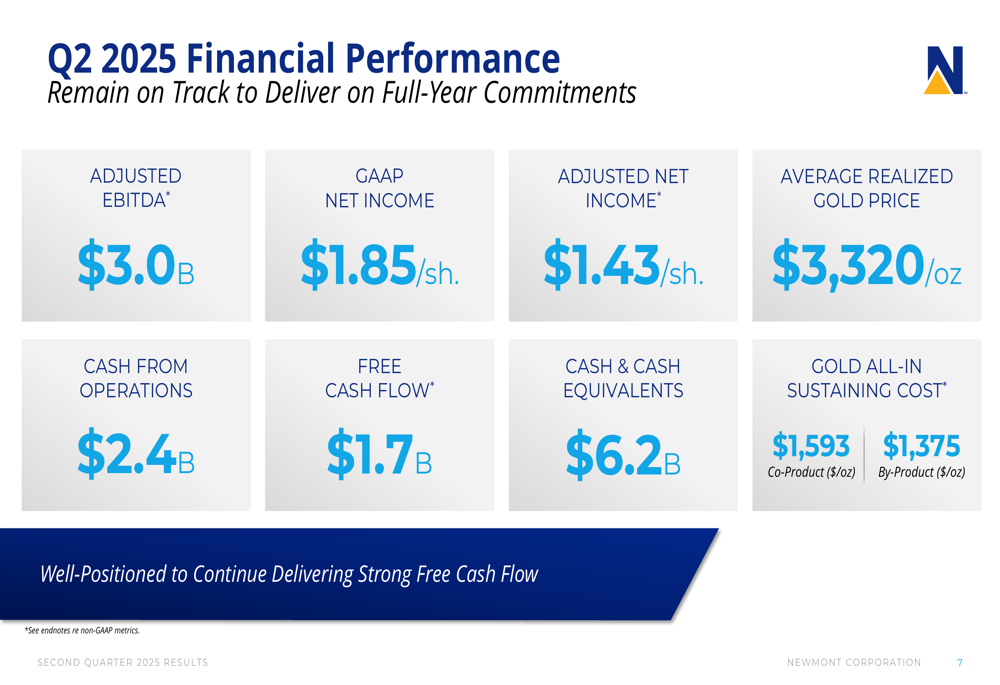

Newmont reported impressive financial metrics for Q2 2025, demonstrating the company’s ability to generate significant cash flow in the current gold price environment:

The company achieved adjusted EBITDA of $3.0 billion and GAAP net income of $1.85 per share, with adjusted net income at $1.43 per share. These strong results were supported by an average realized gold price of $3,320 per ounce. Cash from operations reached $2.4 billion, contributing to the $1.7 billion in free cash flow. The company ended the quarter with $6.2 billion in cash and cash equivalents, up from $4.7 billion reported at the end of Q1 2025.

This represents a significant improvement from Q1 2025, when the company reported free cash flow of $1.2 billion and cash reserves of $4.7 billion, indicating accelerating financial performance.

Capital Allocation & Shareholder Returns

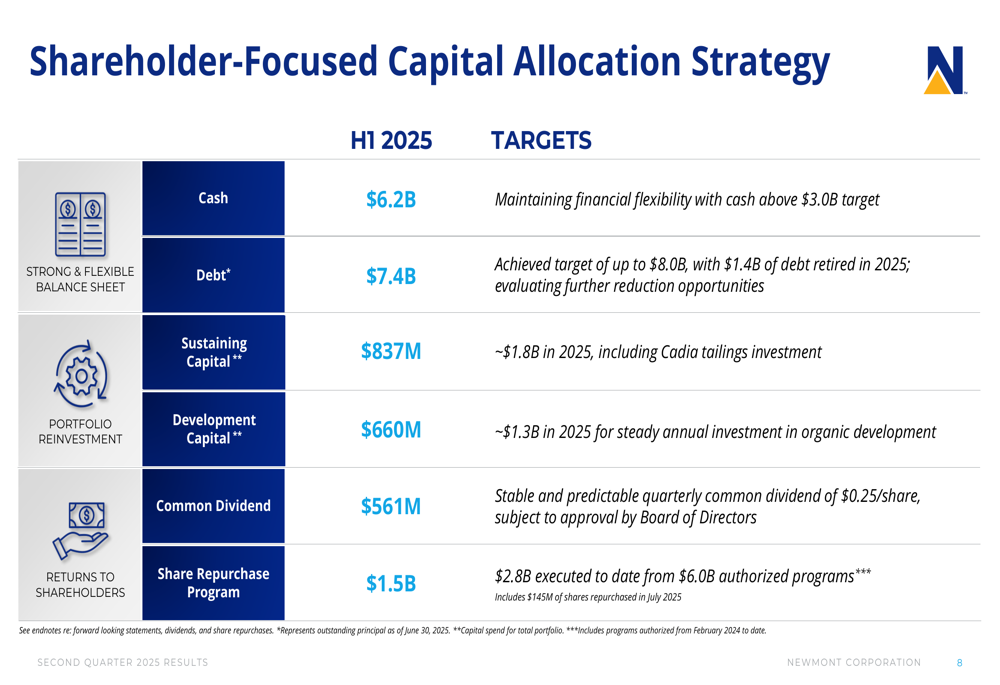

Newmont continues to implement a shareholder-focused capital allocation strategy, balancing reinvestment in the business with returns to shareholders:

The company maintained financial flexibility with $6.2 billion in cash, well above its $3.0 billion target. Debt levels stood at $7.4 billion, below the target of up to $8.0 billion, with $1.4 billion of debt retired in 2025 so far. Newmont is evaluating further debt reduction opportunities.

For the first half of 2025, the company invested $837 million in sustaining capital and $660 million in development capital, with full-year targets of approximately $1.8 billion and $1.3 billion, respectively. Shareholder returns remained a priority, with $561 million paid in common dividends ($0.25 per share quarterly) and $1.5 billion allocated to share repurchases. The company has executed $2.8 billion of its $6.0 billion authorized repurchase programs to date, including $145 million of shares repurchased in July 2025.

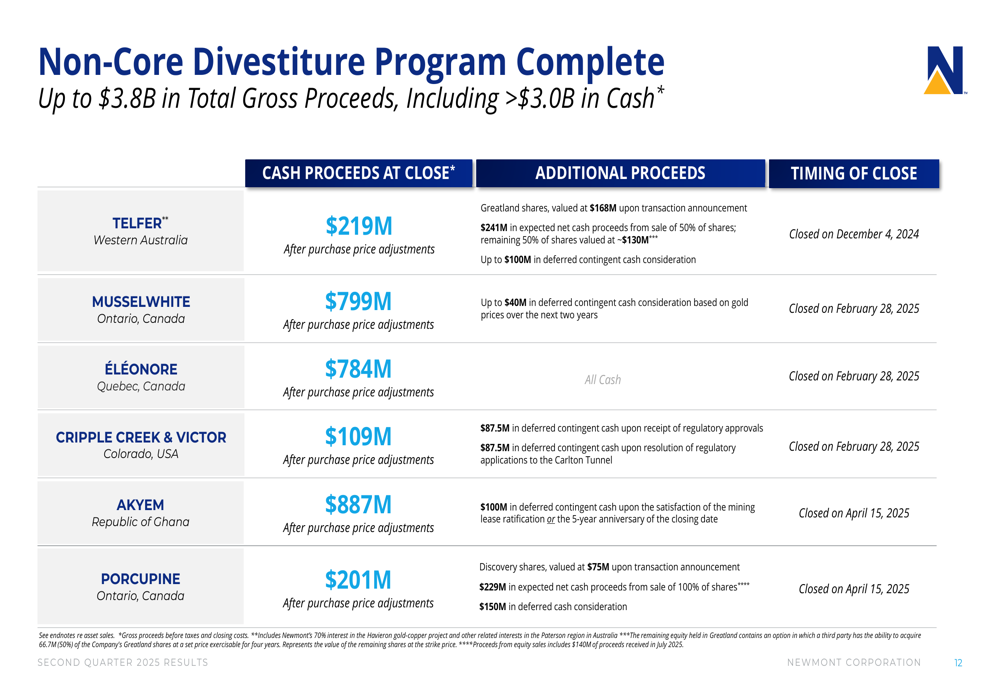

Portfolio Optimization

Newmont has completed its non-core divestiture program, generating significant proceeds to strengthen its balance sheet and focus on core assets:

The divestiture program yielded up to $3.8 billion in total gross proceeds, including over $3.0 billion in cash. Major transactions included the sale of Akyem for $887 million in cash at closing plus $100 million in deferred cash, Musselwhite for $799 million plus up to $40 million in contingent consideration, and Éléonore for $784 million. These strategic divestitures have allowed Newmont to streamline its portfolio and concentrate on its highest-margin, longest-life assets.

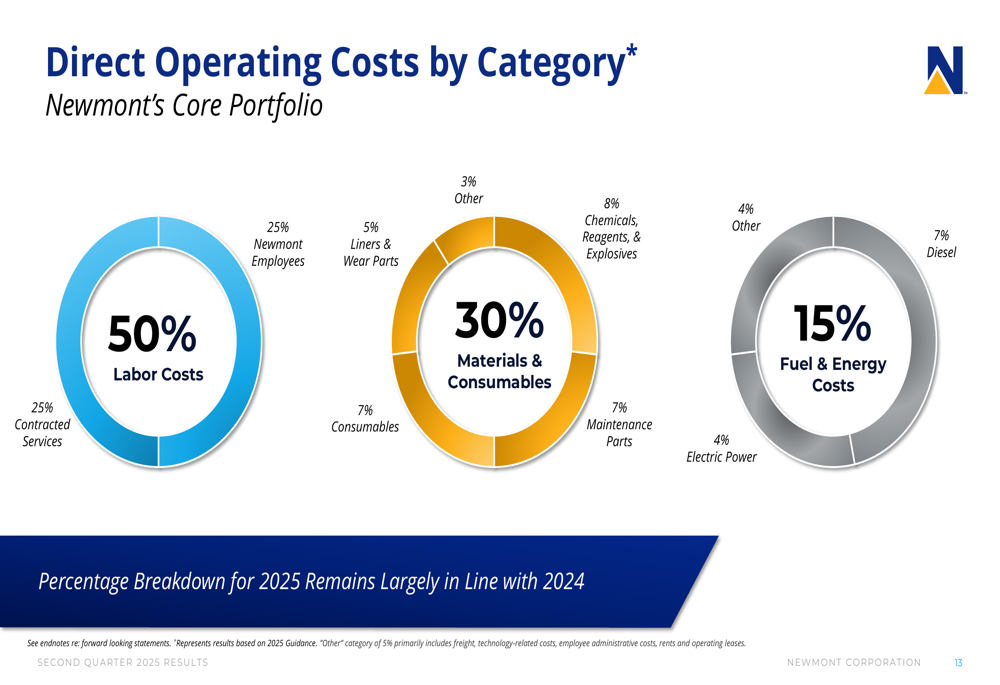

Cost Structure & Guidance

Newmont provided insights into its cost structure and reaffirmed its full-year 2025 guidance:

Labor costs represent the largest component of direct operating costs at 50%, followed by materials and consumables at 30%, and fuel and energy costs at 15%. This breakdown remains largely consistent with 2024, indicating stable cost management despite inflationary pressures in the mining industry.

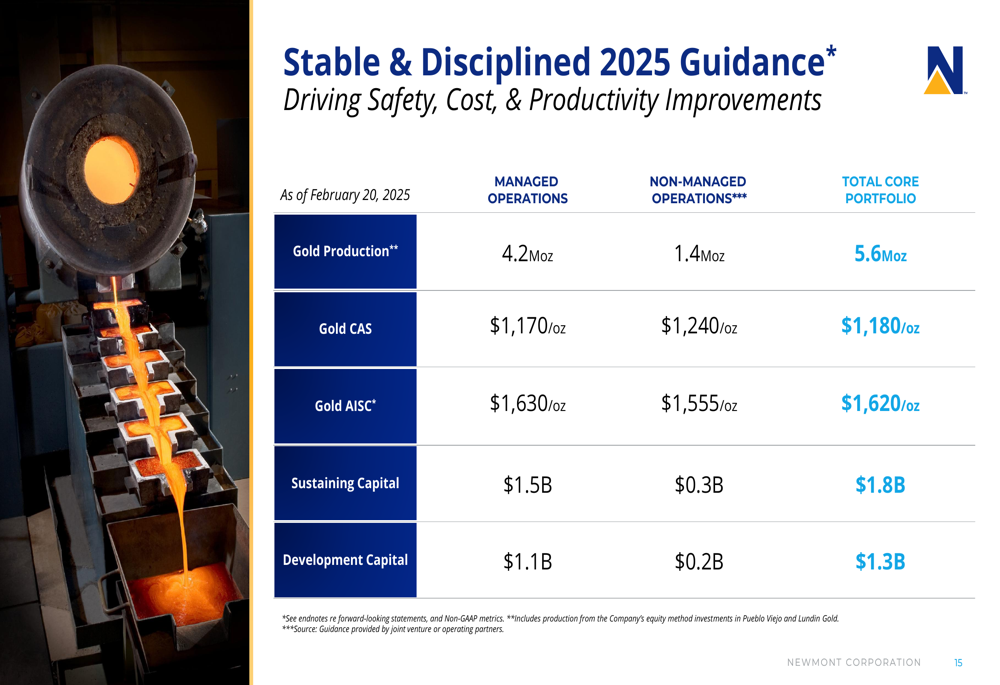

The company’s full-year 2025 guidance remains unchanged from February:

Newmont expects to produce 5.6 million ounces of gold in 2025, with 4.2 million ounces from managed operations and 1.4 million ounces from non-managed operations. Gold CAS is projected at $1,180 per ounce, with AISC at $1,620 per ounce. The company plans to invest $1.8 billion in sustaining capital and $1.3 billion in development capital across its portfolio.

Challenges & Outlook

While Newmont’s financial performance has been strong, the company faces challenges, particularly with the recent incident at Red Chris. The company is concentrating efforts on the safe recovery of team members and has received support from the industry in responding to the incident.

Looking forward, Newmont expects to deliver on its full-year commitments, with a focus on growing free cash flow, returning capital to shareholders, and strengthening its balance sheet. The company anticipates higher production in the second half of 2025 at several operations, including Cerro Negro, Brucejack, and Merian, offsetting expected lower grades at operations like Ahafo South, Lihir, and Cadia.

Newmont’s performance in Q2 2025 demonstrates its ability to generate significant cash flow and deliver shareholder returns while navigating operational challenges. The company’s strong balance sheet and disciplined capital allocation approach position it well to continue executing its strategy in the current gold price environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.