Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Introduction & Market Context

Nexans (EPA:NEXS) (EPA:NEX) presented its H1 2025 results on July 30, 2025, highlighting record financial performance and strong progress in its strategic transformation toward becoming an "Electrification Pure Player." The company’s stock closed at €120.10 on July 29, showing significant appreciation from the €91.15 reported after Q1 results, reflecting growing investor confidence in the company’s strategic direction and financial performance.

CEO Christopher Guérin and Deputy CEO & CFO Jean-Christophe Juillard presented the results, emphasizing the company’s exceptional delivery against its business model and strategic objectives.

Quarterly Performance Highlights

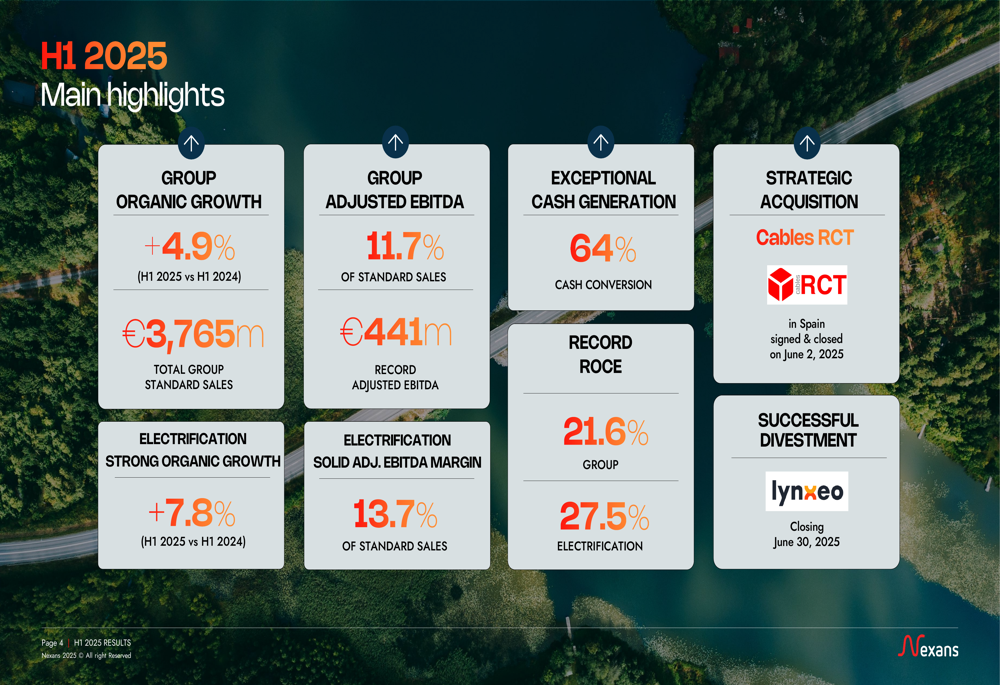

Nexans reported robust H1 2025 results with total Group standard sales of €3,765 million, representing organic growth of 4.9% compared to H1 2024. The company achieved a record adjusted EBITDA of €441 million, equivalent to 11.7% of standard sales.

As shown in the following comprehensive overview of the company’s performance:

Particularly impressive was the company’s cash generation, with a 64% cash conversion rate and record Return on Capital Employed (ROCE) figures of 21.6% for the Group and 27.5% for the Electrification business. These metrics demonstrate Nexans’ operational efficiency and effective capital allocation strategy.

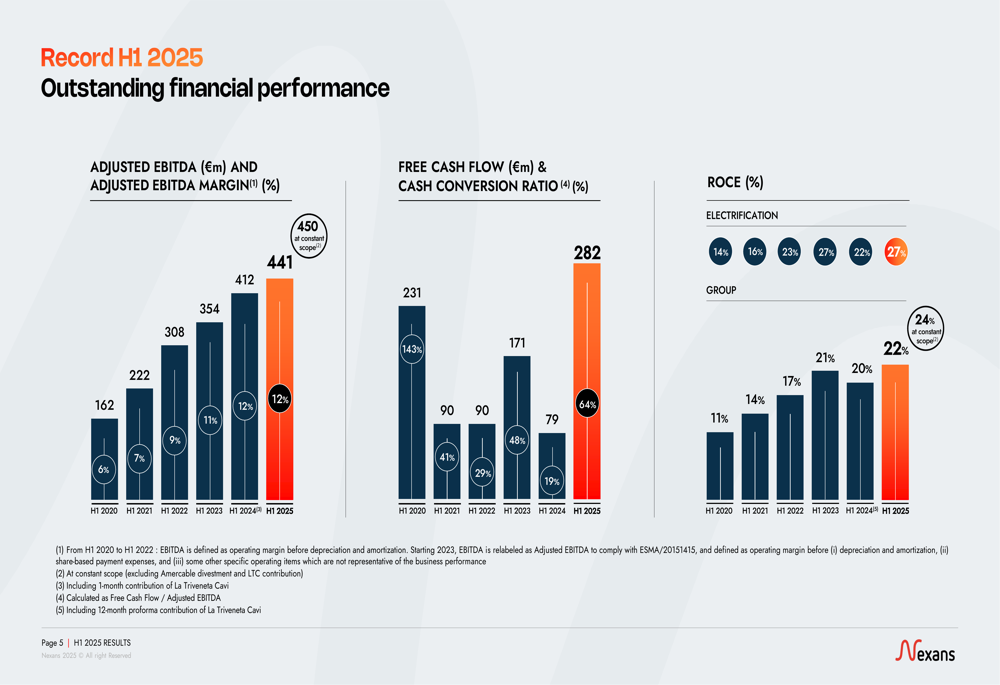

The company’s financial performance has shown consistent improvement over recent years, as illustrated in this chart:

Detailed Financial Analysis

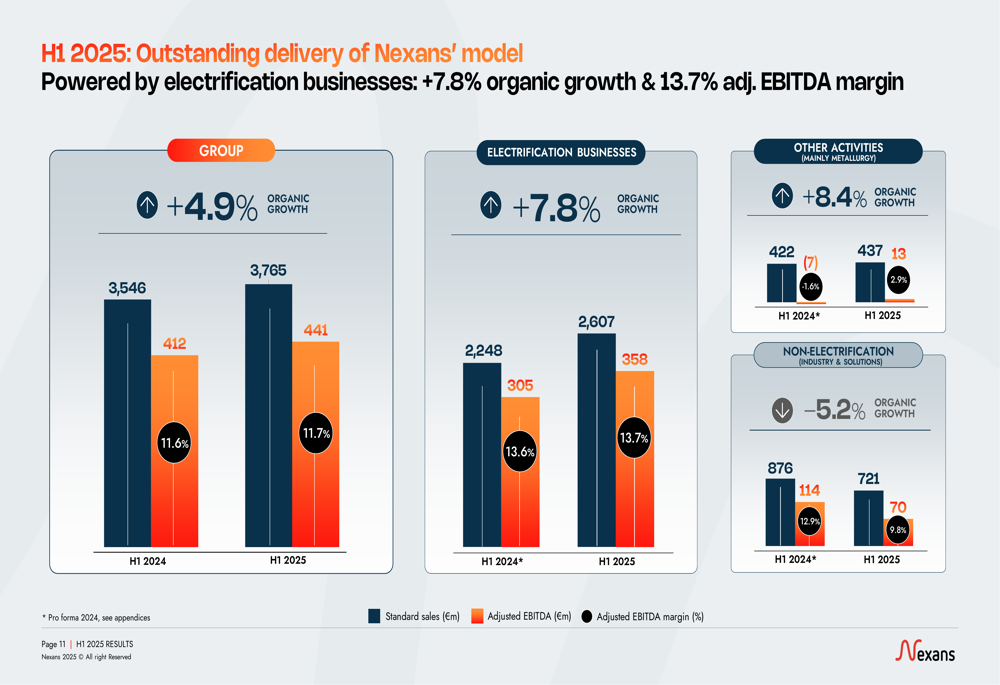

Nexans’ performance varied across its business segments, with Electrification businesses showing particularly strong results. The Electrification segment, which includes PWR-Transmission, PWR-Grid, and PWR-Connect, achieved organic growth of 7.8% and an adjusted EBITDA margin of 13.7%.

The following chart breaks down performance by business segment:

The PWR-Transmission business was the standout performer with 21.7% organic growth and an adjusted EBITDA margin of 11.8%. This segment also reported a significant backlog of €7.8 billion, providing visibility until 2028. The PWR-Grid segment achieved 5.6% organic growth with an impressive 15.9% adjusted EBITDA margin, while PWR-Connect delivered stable sales with 0.2% organic growth but improved profitability with a 13.7% adjusted EBITDA margin.

In contrast, the Non-Electrification segment (mainly Industry & Solutions) experienced a 5.2% organic decline, though it maintained a solid adjusted EBITDA margin of 9.8%.

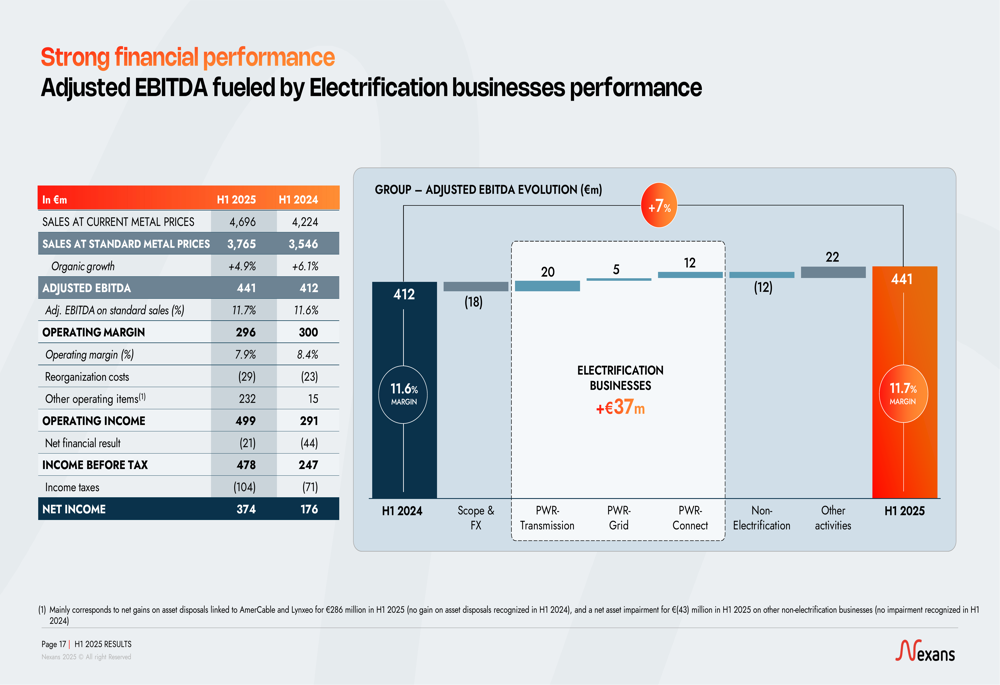

The company’s adjusted EBITDA bridge shows the contributions from different segments:

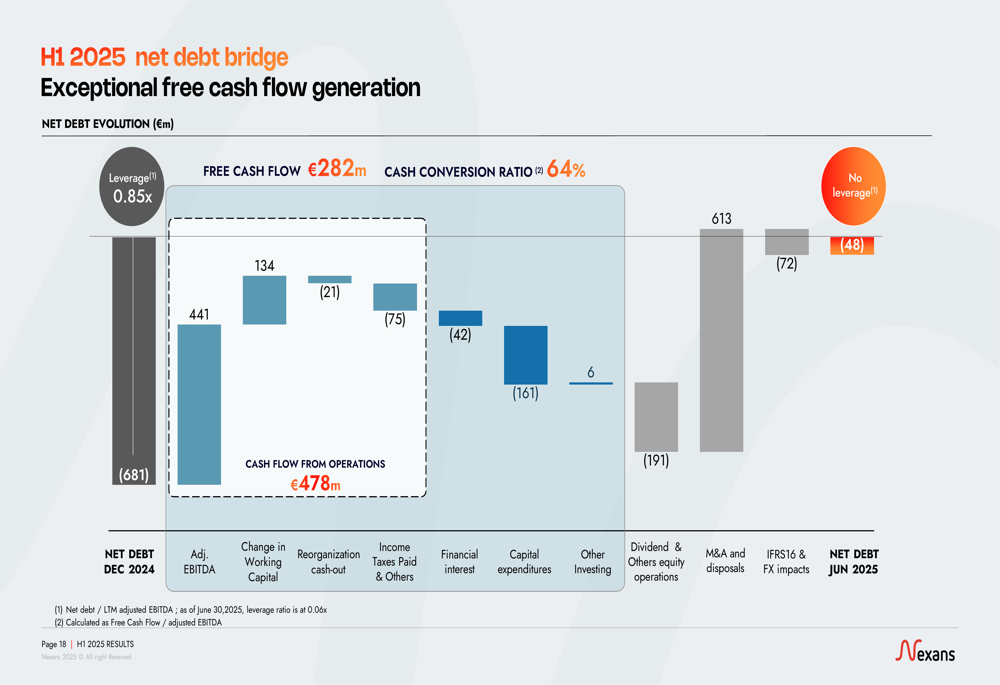

Nexans maintained a very strong balance sheet, with cash and cash equivalents of €2,040 million as of June 30, 2025, up from €1,254 million at the end of 2024. The company’s net debt evolution demonstrates its exceptional cash management:

Strategic Initiatives

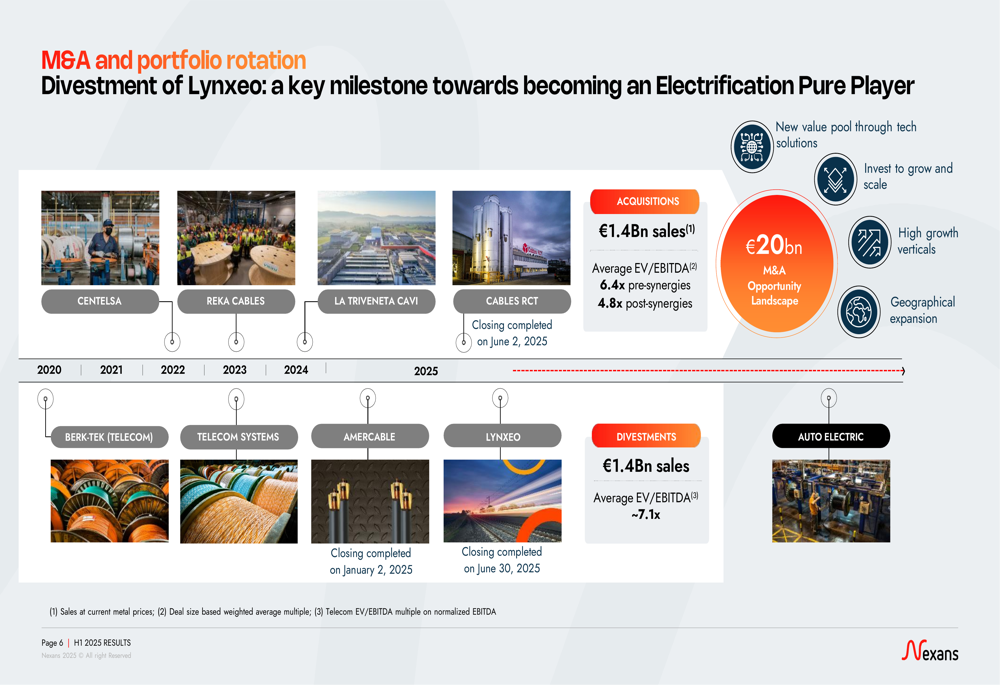

Nexans continues to execute its strategic transformation toward becoming an Electrification Pure Player. In H1 2025, the company completed two significant transactions: the acquisition of Cables RCT in Spain (closed on June 2, 2025) and the divestment of Lynxeo (closed on June 30, 2025).

The company’s M&A and portfolio rotation activities are illustrated in the following chart:

Since initiating its transformation strategy, Nexans has completed acquisitions totaling €1.4 billion in sales, with an average EV/EBITDA multiple of 6.4x pre-synergies and 4.8x post-synergies. The company has also divested businesses with €1.4 billion in sales at an average EV/EBITDA multiple of approximately 7.1x.

The acquisition of Cables RCT strengthens Nexans’ footprint in Spain and provides complementary assets with substantial synergy potential. Cables RCT generated €133 million in revenue in 2024 and employs 175 people.

Nexans also reported success with its ACT 2025 employee share ownership plan, achieving a 46% participation rate worldwide (up from 33% in ACT 2022). Employee shareholding now represents approximately 5% of Nexans’ capital, compared to the SBF120 average of 2.7%.

Forward-Looking Statements

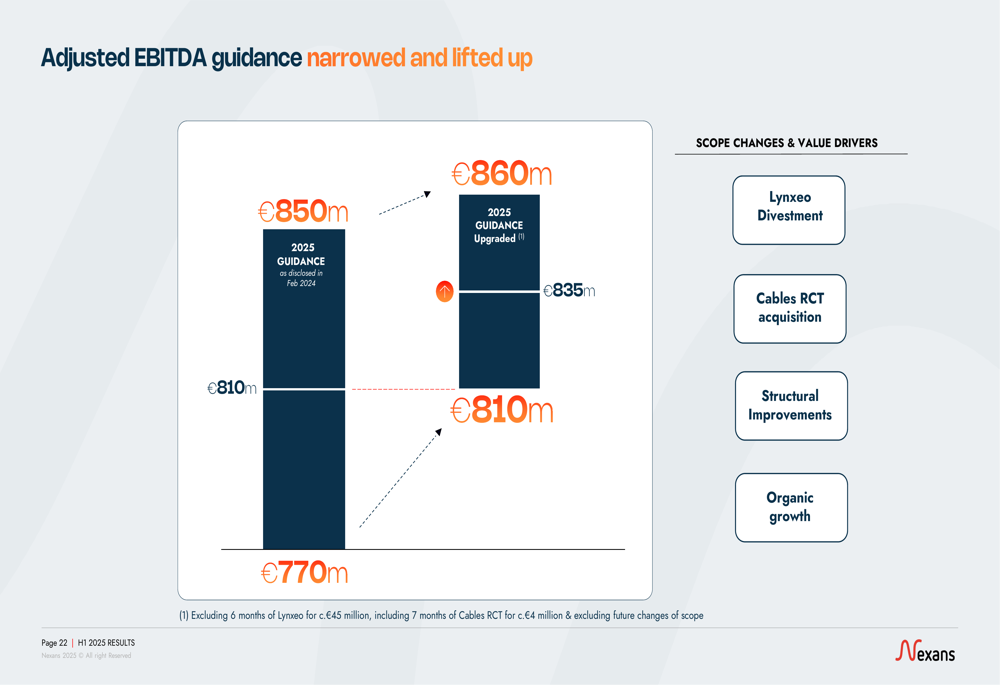

Based on its strong H1 2025 performance, Nexans has upgraded its full-year guidance. The company now expects adjusted EBITDA of €810-860 million (previously €770-850 million) and free cash flow of €275-375 million (previously €225-325 million).

The upgraded guidance is presented in the following chart:

The factors contributing to the guidance upgrade include structural improvements, organic growth, and the net effect of the Lynxeo divestment and Cables RCT acquisition, as illustrated here:

Looking further ahead, Nexans has maintained its 2028 guidance, targeting adjusted EBITDA of €1,150 million (+/-€75 million), organic sales growth of 3-5% in Electrification, free cash flow conversion above 45%, ROCE above 20%, and a dividend payout ratio of at least 30%.

The company’s strategic focus remains on the growing electrification market, driven by the net-zero transition, grid renewal and strengthening, and the increasing demand for smart and safe buildings. With its balanced geographic footprint and diversified end-markets, Nexans is well-positioned to capitalize on these long-term trends.

Nexans’ detailed segment performance for H1 2025 compared to H1 2024 shows improvements across most business units:

With its strong financial performance, strategic portfolio transformation, and upgraded guidance, Nexans continues to demonstrate effective execution of its strategy and is well-positioned for sustainable growth in the electrification market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.