Gold soars to record high over $3,900/oz amid yen slump, US rate cut bets

Introduction & Market Context

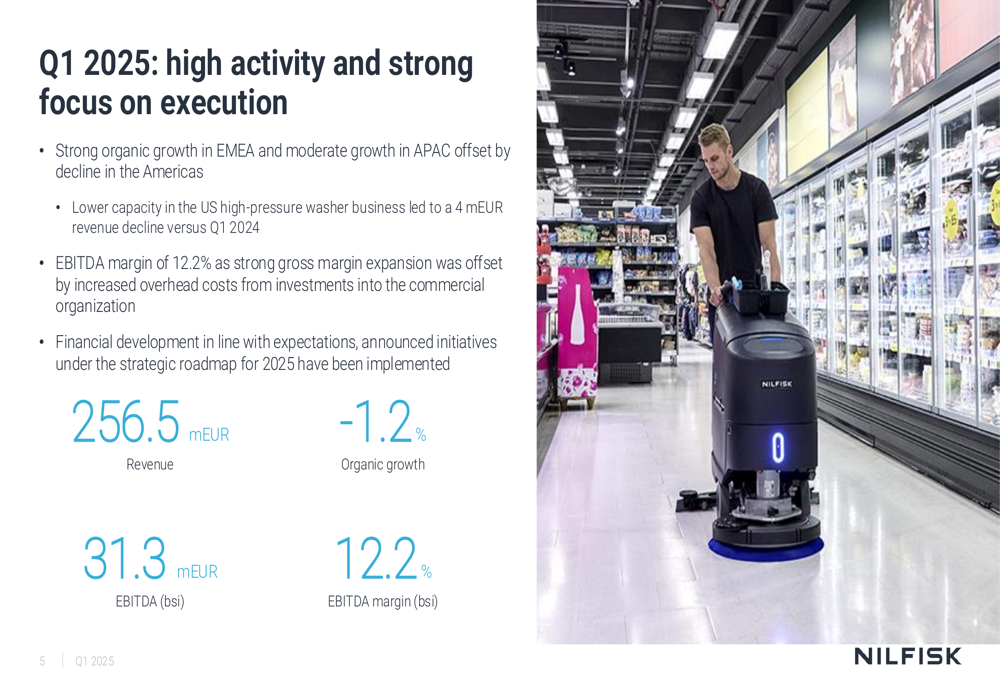

Nilfisk Holding A/S (CPH:NLFSK) presented its Q1 2025 results on May 13, showing mixed performance across regions with shares dropping 2.45% to 87.60 DKK following the announcement. The cleaning equipment manufacturer reported an overall organic revenue decline of 1.2%, despite achieving a record quarterly gross margin of 43.2%.

The company also introduced its new CFO, Carl Bandhold, who joined on March 24 from Profoto, where he served as Deputy CEO and CFO. According to Nilfisk, Bandhold’s appointment does not change the company’s financial guidance for 2025.

Quarterly Performance Highlights

Nilfisk reported Q1 2025 revenue of 256.5 million euros, with an EBITDA of 31.3 million euros, resulting in an EBITDA margin of 12.2%. This represents a margin decline from 13.2% in the same period last year, primarily due to increased overhead costs despite gross margin improvements.

As shown in the following quarterly performance overview:

The company highlighted that these results were in line with expectations, noting that announced initiatives under the strategic roadmap for 2025 have been implemented. However, the US high-pressure washer business experienced lower capacity, leading to a 4 million euro revenue decline compared to Q1 2024.

Regional Performance Analysis

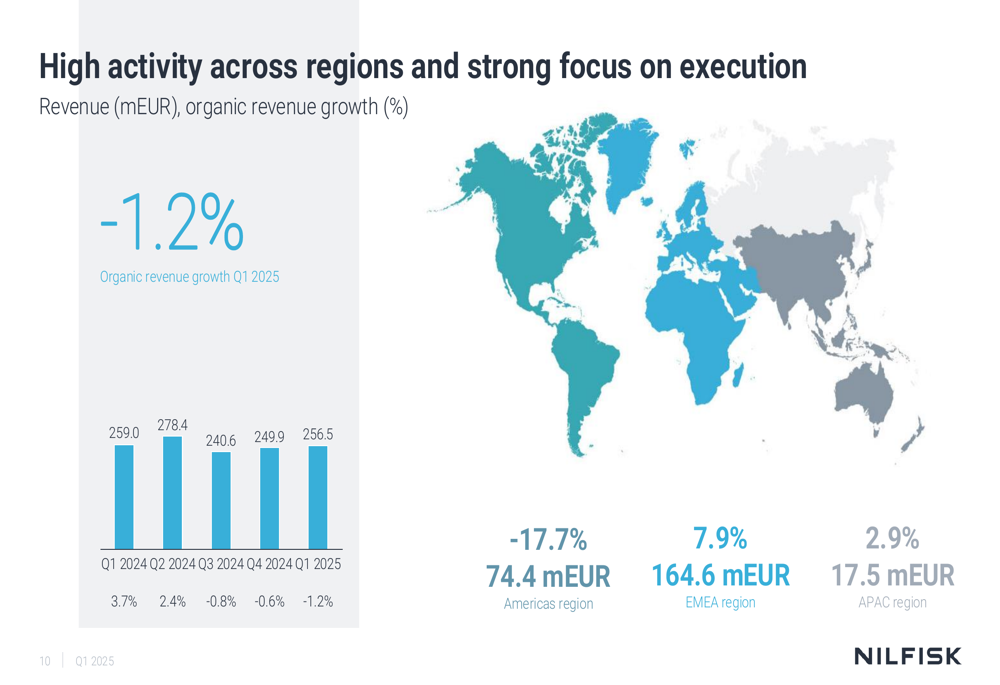

Nilfisk’s performance varied significantly across regions, with EMEA showing strong growth while Americas faced substantial challenges. The company’s regional revenue breakdown reveals these disparities:

EMEA emerged as the strongest performer with 7.9% organic growth, generating 164.6 million euros in revenue. The company attributed this to effective commercial execution and expects this positive momentum to continue.

In stark contrast, the Americas region experienced a 17.7% organic decline, with revenue falling to 74.4 million euros. This weakness was driven by high backlog release in Q1 2024, lower revenue in the US high-pressure washer business, and continued soft demand. The company noted that the outlook for this region remains uncertain due to tariff concerns.

APAC returned to growth with a modest 2.9% organic increase, generating 17.5 million euros in revenue. This improvement follows what Nilfisk described as a challenging 2024, with growth driven by pockets of increased demand.

Strategic Initiatives & Outlook

Nilfisk outlined its strategic roadmap for 2025, focusing on three key areas: improving its competitive position in North America, enhancing the operating model, and executing structural efficiency improvements.

The comprehensive strategic plan includes:

For North America specifically, the company is focusing on increasing sales density, refreshing the product portfolio, strengthening product delivery, and implementing organizational changes. The US high-pressure washer business is now being presented as assets held for sale, indicating a potential divestiture.

Nilfisk is also addressing supply chain challenges related to geopolitical uncertainties and tariffs:

The company maintains its 2025 outlook, projecting organic revenue growth of 1% to 3% and an EBITDA margin before special items of 13% to 14%. These projections assume stable market conditions in EMEA, neutral development in the US versus 2024, moderate growth in APAC, and the ability to offset tariffs.

Financial Analysis

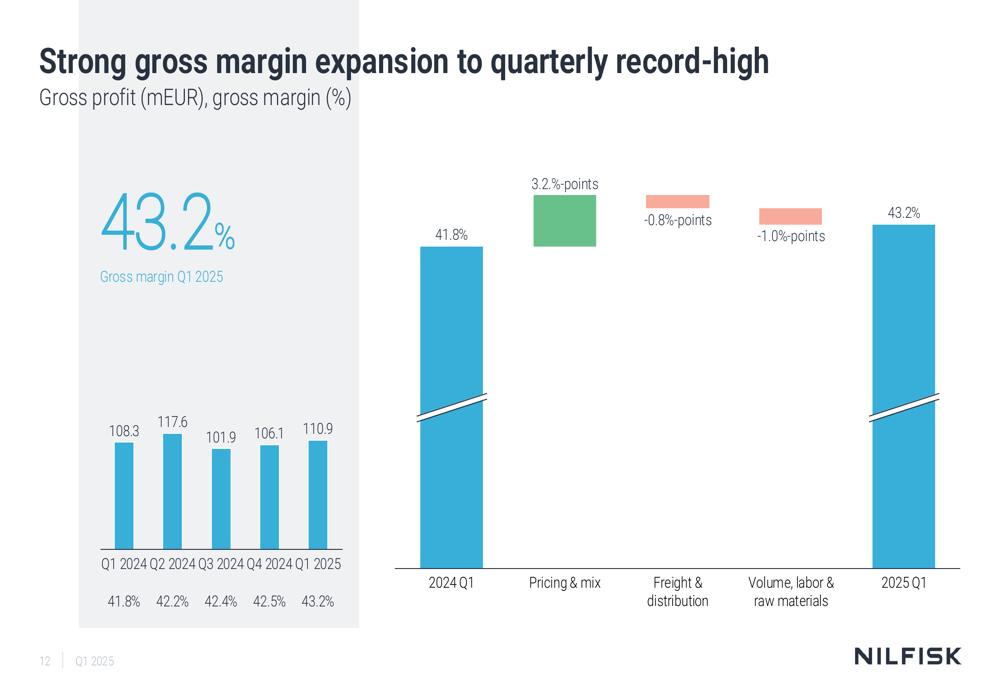

Nilfisk achieved a record quarterly gross margin of 43.2% in Q1 2025, showing consistent improvement from 41.8% in Q1 2024:

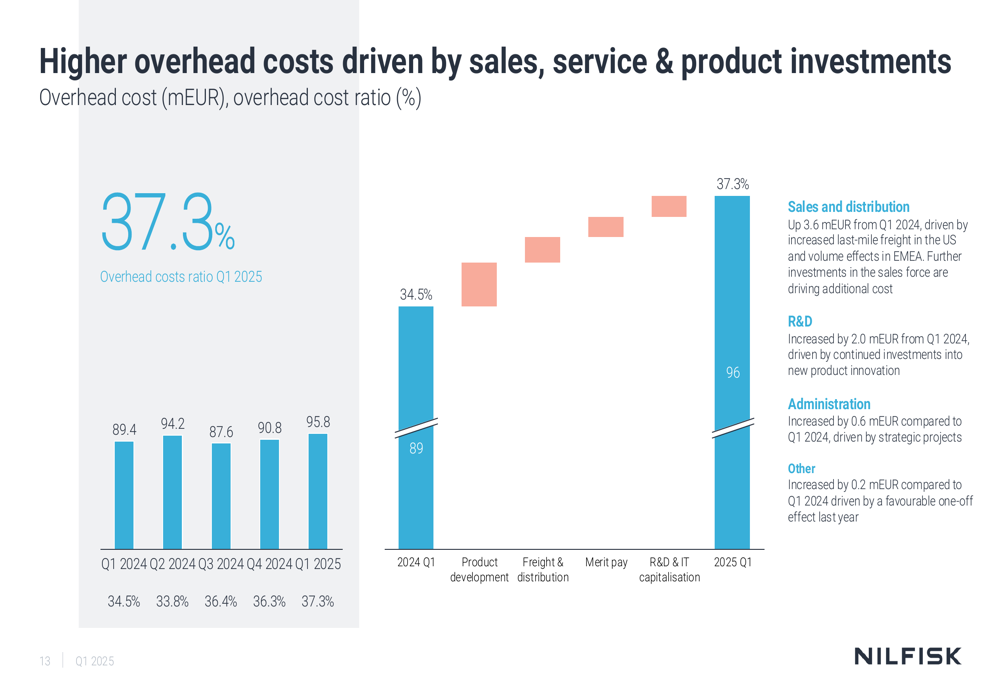

This margin expansion was driven by favorable pricing and mix effects, along with improvements in freight and distribution costs. However, these gains were offset by rising overhead costs, which increased to 37.3% of revenue compared to 34.5% in Q1 2024:

The increased overhead costs were attributed to investments in sales, service, and product development, as well as merit pay increases and changes in R&D and IT capitalization.

Working capital changes drove a negative free cash flow of 19.8 million euros in Q1 2025, with gearing at 2.2x. This represents a deterioration from previous quarters and may be contributing to investor concerns reflected in the stock price decline.

Despite these challenges, Nilfisk’s management expressed confidence in the company’s ability to execute its strategic initiatives and maintain its full-year guidance. The overhead cost reduction program scheduled to start in Q2 2025 is expected to help address some of the margin pressure experienced in the first quarter.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.