Asia FX cautious amid US govt shutdown; yen tumbles after Takaichi’s LDP win

Introduction & Market Context

NNIT AS (CPH:NNIT) released its Q2 2025 results presentation on September 4, 2025, revealing a challenging quarter marked by revenue decline amid persistent market uncertainty, particularly in the European region. The company’s stock is currently trading at 61.70 DKK, down 0.48% on the day and hovering near its 52-week low of 60 DKK, reflecting investor concerns about growth prospects.

Despite the revenue challenges, NNIT significantly outperformed earnings expectations with an EPS of $1.34 versus the forecasted $0.77, suggesting effective cost management even as sales faltered. The company’s shares have declined 32.97% year-to-date, indicating broader investor concerns about its growth trajectory.

Quarterly Performance Highlights

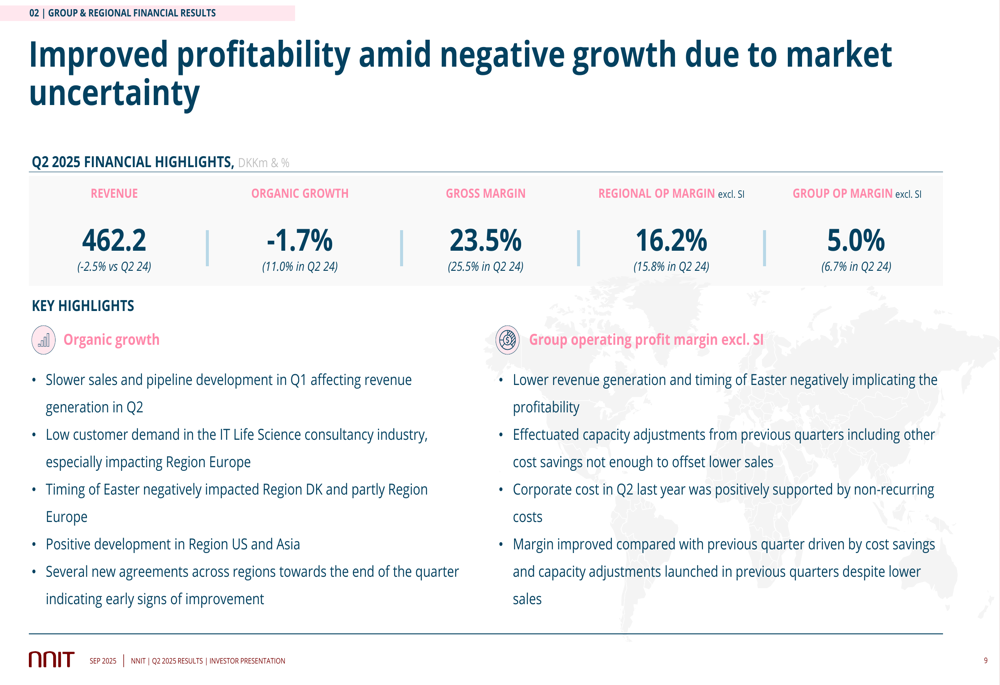

NNIT reported Q2 2025 revenue of 462.2 million DKK, representing a 2.5% decline compared to the same period last year. Organic growth was negative at -1.7%, a significant deterioration from the robust 11.0% growth achieved in Q2 2024.

As shown in the following financial highlights:

Operating profit excluding special items reached 22.9 million DKK, down from 32.0 million DKK in Q2 2024, with the corresponding margin contracting to 5.0% from 6.7%. The gross margin also declined to 23.5% from 25.5% a year earlier, reflecting increased cost pressures.

Despite these challenges, the regional operating profit margin excluding special items improved slightly to 16.2% from 15.8% in the comparable period, demonstrating some success in the company’s cost optimization efforts at the regional level.

Regional Performance Analysis

NNIT’s performance varied significantly across its geographic segments, with Europe showing particular weakness while the US region demonstrated a promising turnaround.

The regional breakdown reveals these contrasting trends:

Region Europe experienced a substantial decline with organic growth of -13.7%, a stark reversal from the 12.3% growth recorded in Q2 2024. Despite this revenue challenge, the regional operating margin improved to 16.8% from 14.8%, suggesting effective cost management.

In contrast, Region US showed encouraging signs of recovery with 4.1% organic growth, compared to a -15.2% contraction in Q2 2024. The US region also achieved the highest operating margin at 21.7%, up significantly from 14.9% a year earlier.

Region Asia maintained positive organic growth of 4.4%, though this represented a slowdown from 6.4% in Q2 2024, while its operating margin declined to 7.1% from 13.2%. Region Denmark posted modest growth of 2.4%, a significant deceleration from the 27.3% growth achieved in Q2 2024, with operating margin declining to 15.3% from 17.4%.

Strategic Initiatives & Cost Optimization

NNIT highlighted several strategic initiatives aimed at improving operational efficiency and positioning the company for future growth despite current market challenges.

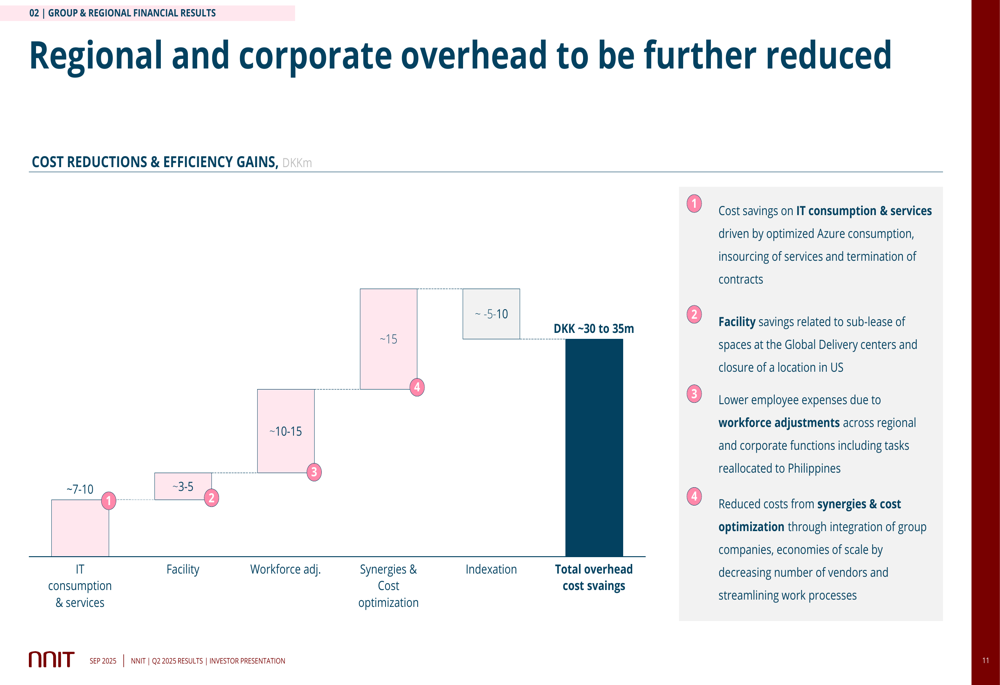

The company is implementing comprehensive cost reduction measures targeting savings of approximately 30-35 million DKK:

These cost optimization efforts span multiple areas including IT consumption and services, facility management, workforce adjustments, and synergies from acquisitions. The company also emphasized its progress in implementing a new organizational structure, integrating recent acquisitions (SL Controls and Excellis), and deploying new ERP and HR systems.

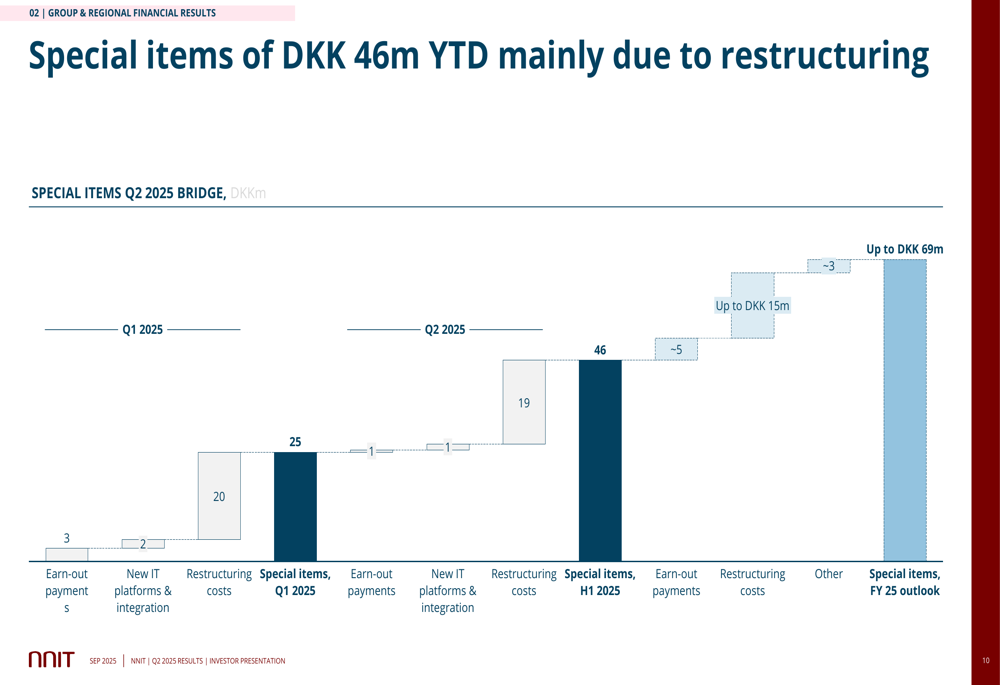

Special items, primarily related to restructuring efforts, totaled 46 million DKK year-to-date:

These expenses reflect the company’s ongoing transformation initiatives, which management believes will position NNIT for improved performance as market conditions stabilize.

Outlook & Forward Guidance

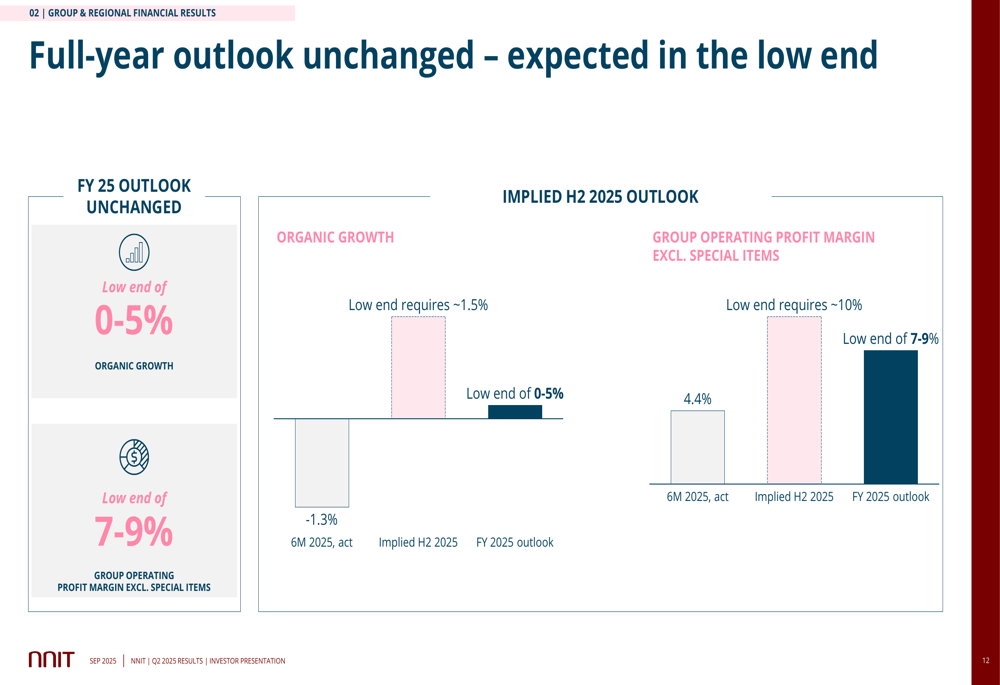

Despite the challenging Q2 results, NNIT maintained its full-year outlook for 2025, though it now expects results to be at the lower end of the guidance range. The company projects organic growth of 0-5% (revised down from the previous 7-10% forecast in February) and a group operating profit margin excluding special items of 7-9%.

The revised outlook and implied second-half performance are illustrated in the following chart:

Management cited "early signs of improvement" including important contract wins during Q2 and the US region’s return to growth. However, they acknowledged the continued slowdown in the IT Life Science consultancy industry, which represents a core market for NNIT.

CEO Peer noted during the earnings call, "We see early signs of improvement and some new contracts were won," while CFO Carsten highlighted that the "biggest uncertainty is in the region Europe," underscoring the geographic disparity in performance and outlook.

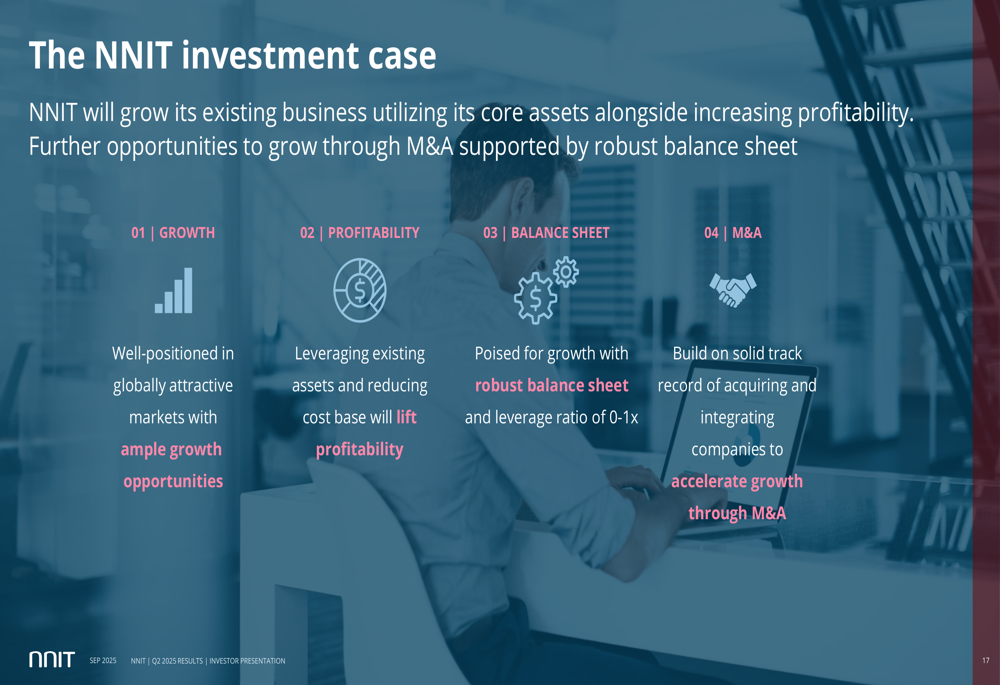

NNIT’s investment case continues to focus on growth in its core life sciences and Danish public sector markets, with potential for further expansion through acquisitions supported by what management describes as a robust balance sheet:

As NNIT navigates through this period of market uncertainty, investors will be closely watching whether the company can deliver on its revised outlook and successfully execute its strategic initiatives to return to sustainable growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.