Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

Nokia (NYSE:NOK) released its Q2 2025 financial results on July 24, 2025, revealing a mixed performance across business segments and regions. The telecommunications equipment provider reported results amid ongoing currency challenges and tariff concerns, which have prompted a downward revision to its full-year outlook despite solid underlying business performance in key growth areas.

The company’s stock has faced pressure following the announcement, with shares dropping 6.98% to €3.813 as investors reacted to the lowered guidance. This follows a challenging Q1 where Nokia missed earnings expectations, continuing a period of volatility for the Finnish telecommunications giant.

Executive Summary

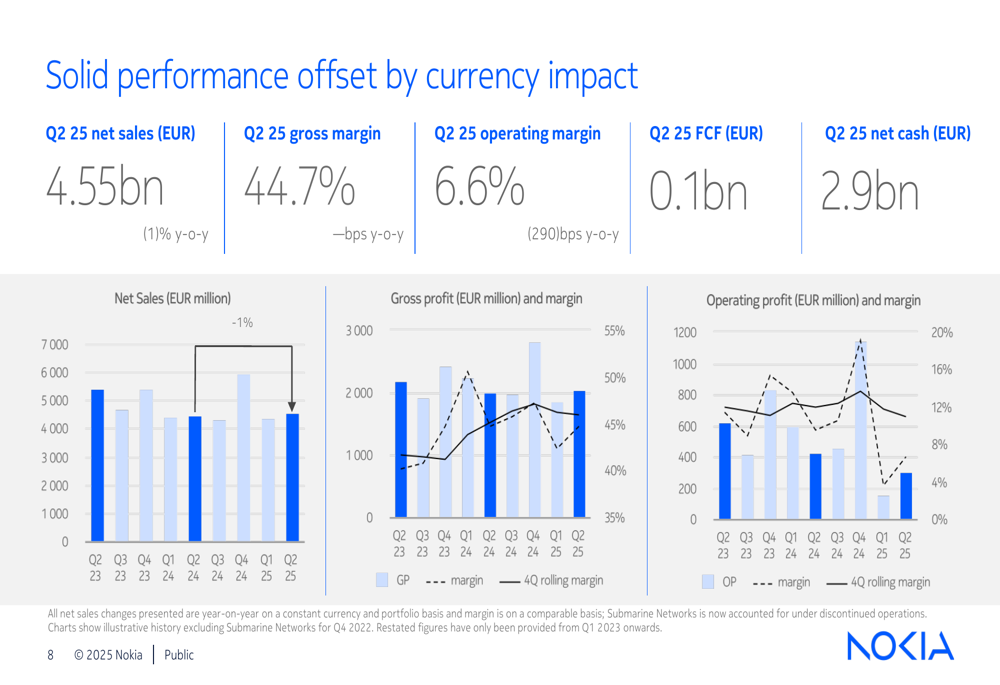

Nokia reported Q2 2025 net sales of €4.55 billion, representing a modest 1% year-over-year decline. The company’s comparable operating profit margin contracted to 6.6%, a significant 290 basis point decrease compared to the same period last year. Free cash flow remained positive at €0.1 billion, while the company maintained a strong net cash position of €2.9 billion.

CEO Justin Hotard emphasized Nokia’s strategic positioning to lead in connectivity during what he termed the "AI supercycle," while acknowledging the impact of external factors on financial performance. The company has lowered its full-year comparable operating profit guidance to €1.6-2.1 billion from the previous €1.9-2.4 billion, primarily due to currency fluctuations and tariff impacts.

As shown in the following financial overview chart:

Quarterly Performance Highlights

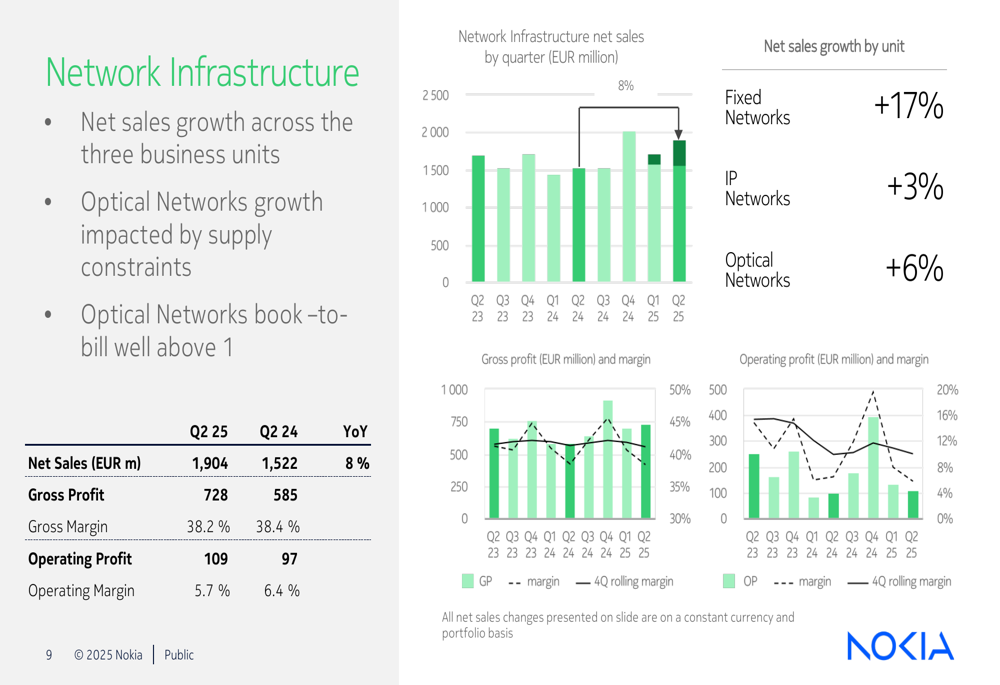

Nokia’s business units delivered divergent results in Q2 2025, with Network Infrastructure and Cloud and Network Services showing strong growth, while Mobile Networks experienced a significant decline.

The Network Infrastructure segment delivered 8% year-over-year growth, with Fixed Networks leading the way at 17% growth. IP Networks grew by 3%, while Optical Networks increased by 6% despite being impacted by supply constraints. The segment maintained a solid gross margin of 38.2%.

The following chart illustrates Network Infrastructure’s performance:

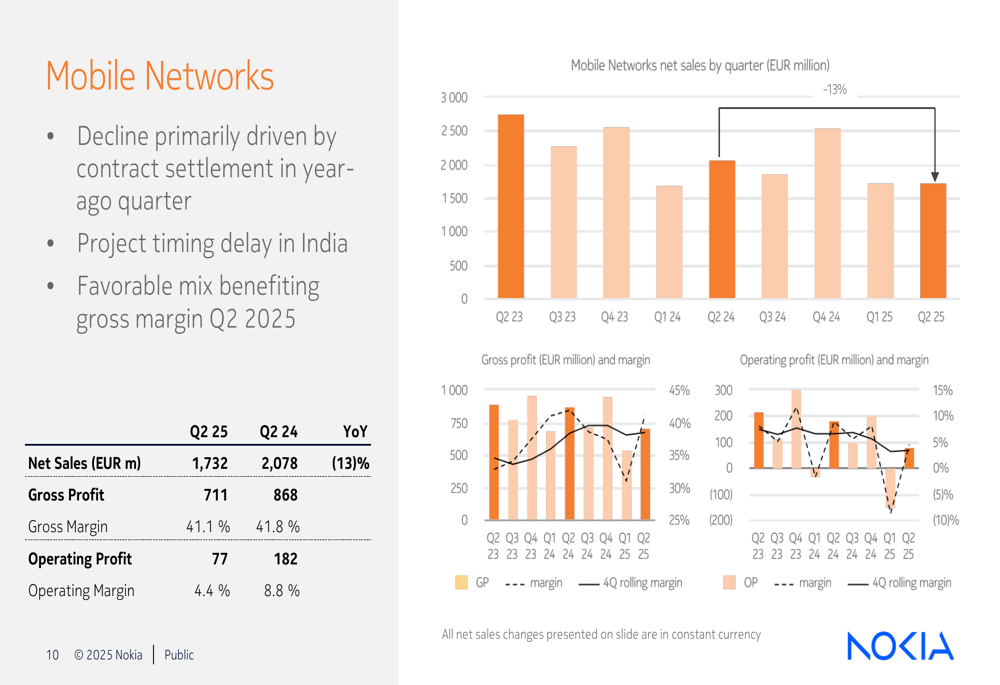

Mobile Networks experienced a 13% year-over-year decline in net sales, which the company attributed primarily to a contract settlement in the year-ago quarter and project timing delays in India. Despite the revenue decline, the segment maintained a relatively strong gross margin of 41.1%, though operating margin fell to 4.4% from 8.8% a year earlier.

The Mobile Networks performance is detailed in this chart:

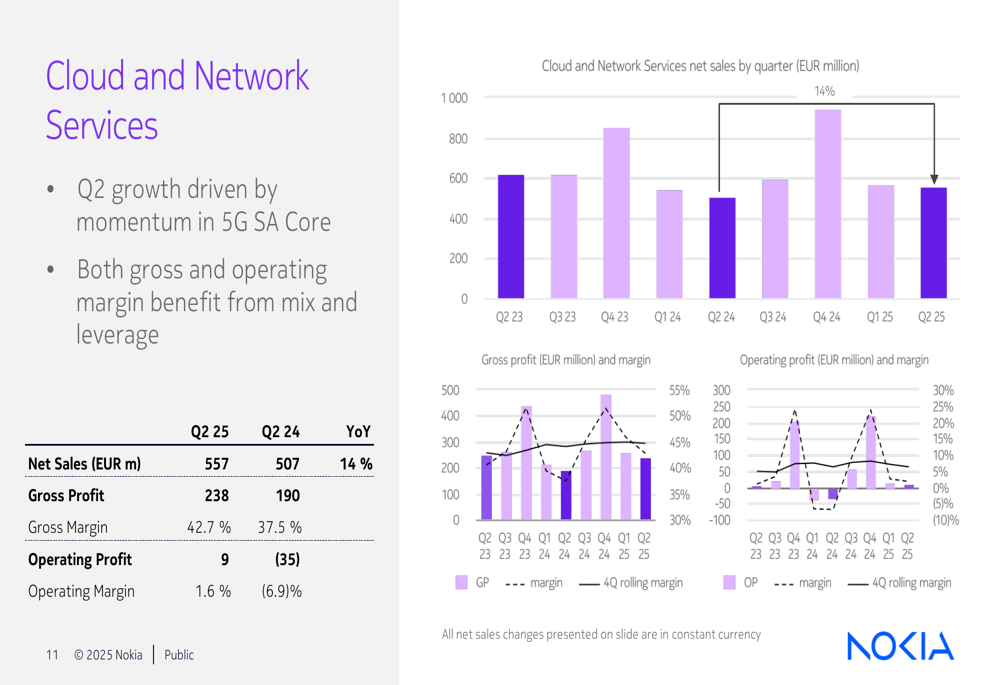

Cloud and Network Services emerged as a bright spot with 14% year-over-year growth, driven by momentum in 5G SA Core deployments. The segment showed significant margin improvement, with gross margin increasing to 42.7% from 37.5% and operating margin turning positive at 1.6% compared to -6.9% in the prior year.

The following chart shows Cloud and Network Services’ strong performance:

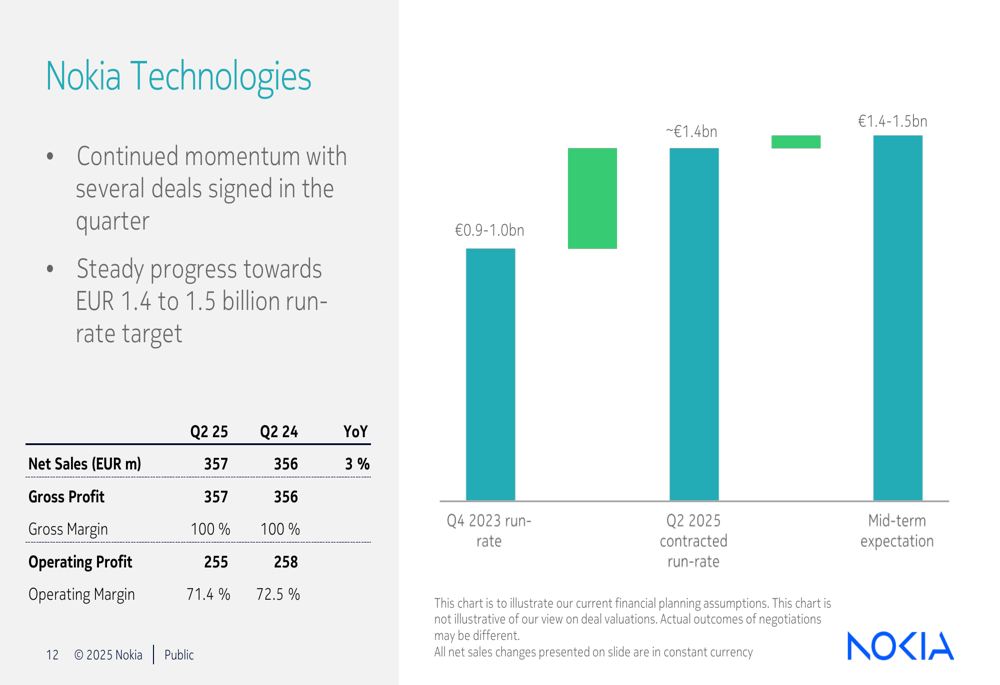

Nokia Technologies, the company’s licensing arm, delivered steady 3% growth with a 100% gross margin and 71.4% operating margin. The segment continues to progress toward its mid-term run-rate target of €1.4-1.5 billion.

As illustrated in this chart showing Nokia Technologies’ progress:

Detailed Financial Analysis

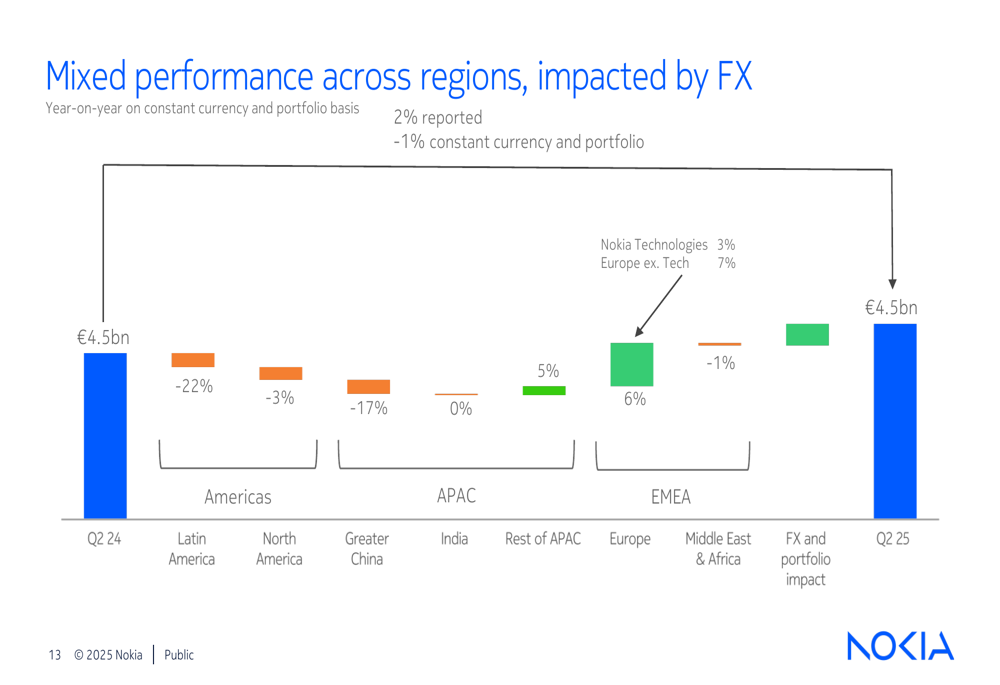

Regional performance revealed significant geographic disparities. Europe (excluding Technologies) showed strong 7% growth, while the Americas declined by 22% and Asia-Pacific fell by 17%. Overall, on a constant currency and portfolio basis, Nokia’s net sales declined by 1%.

The following regional breakdown illustrates these geographic trends:

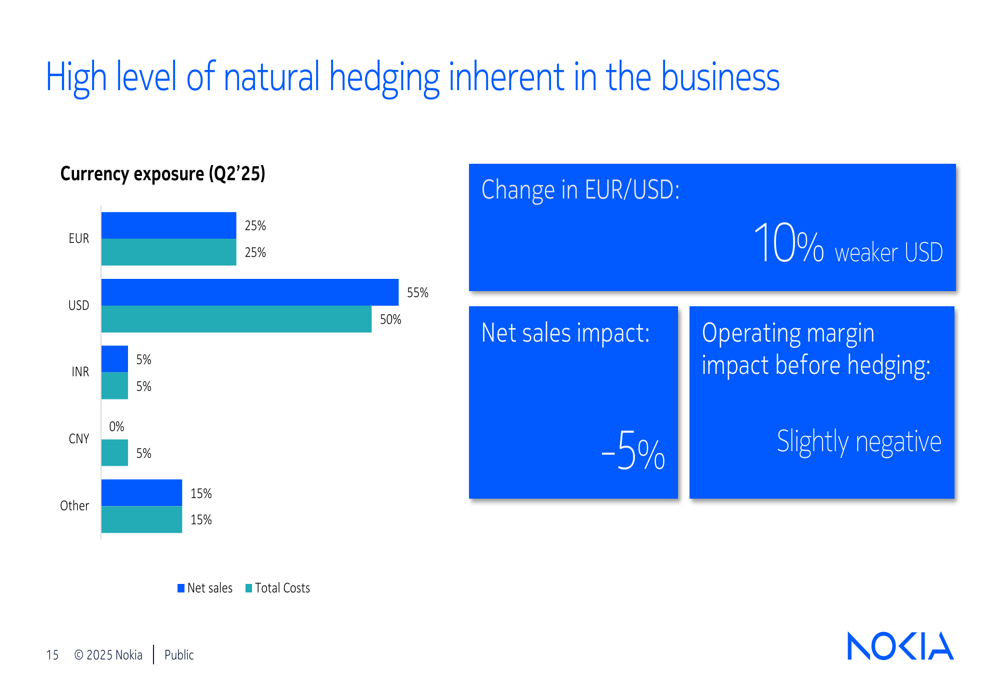

Currency exposure remains a significant factor in Nokia’s financial performance, with 55% of the company’s exposure in USD, 25% in EUR, 5% in INR, and 15% in other currencies. The company noted that a 10% weaker USD would impact net sales by approximately -5% with a slightly negative effect on operating margin before hedging.

This chart shows Nokia’s currency exposure and potential impacts:

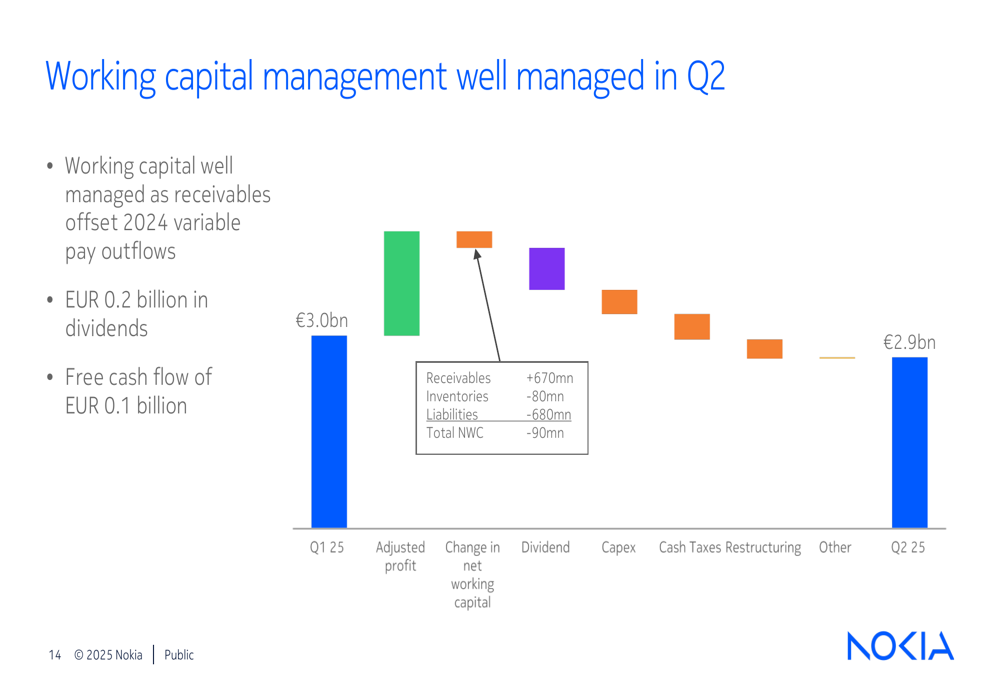

Working capital was well-managed during the quarter, with receivables offsetting variable pay outflows from 2024. The company paid €0.2 billion in dividends while generating €0.1 billion in free cash flow. Net cash position stood at €2.9 billion at quarter-end, down slightly from €3.0 billion in Q1 2025.

The following waterfall chart details the changes in Nokia’s cash position:

Forward-Looking Statements

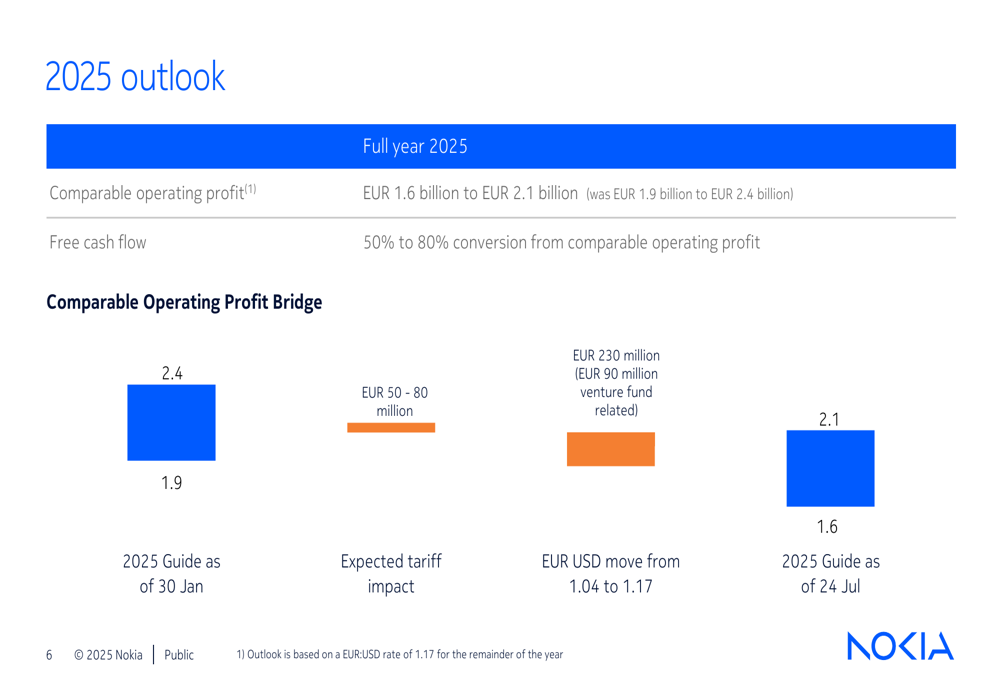

Nokia has revised its full-year 2025 outlook, lowering comparable operating profit guidance to €1.6-2.1 billion from the previous €1.9-2.4 billion. This adjustment reflects several factors, including the impact of the EUR/USD exchange rate movement from 1.04 to 1.17 (approximately €230 million impact, including €90 million venture fund-related) and expected tariff impacts of €50-80 million.

Despite these headwinds, the company maintained its free cash flow conversion guidance at 50-80% of comparable operating profit. Management expressed optimism about the demand environment, projecting strong growth in Network Infrastructure, growth in Cloud and Network Services, and largely stable net sales in Mobile Networks.

The following bridge chart illustrates the factors affecting Nokia’s revised outlook:

Nokia highlighted several commercial wins across its business units, including an 800G ZR/ZR+ hyperscaler award in Optical Networks, maintaining the #1 position in SP Edge Routing and OLT, 5G deals with Elisa and Optus, and core wins with Bharti Airtel (NSE:BRTI), Elisa, O2 Czech Republic, and Vodafone (NASDAQ:VOD) Qatar.

The company also announced that its next Capital Markets Day will take place in New York on November 19, 2025, where it is expected to provide further details on its strategic direction and financial targets.

As Nokia navigates these currency and tariff challenges, the company’s ability to execute on its growth initiatives in Network Infrastructure and Cloud and Network Services will be crucial to offsetting the headwinds that have prompted this guidance revision.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.