S&P 500 cuts losses as Nvidia climbs ahead of results

Introduction & Market Context

NorAm Drilling AS (OB:NORAM) presented its Q1 2025 financial results on May 30, 2025, reporting a significant increase in profitability despite facing headwinds in the Permian Basin drilling market. The company’s shares closed at NOK 22.4 on the presentation day, up 0.67% from the previous close.

The drilling contractor, which specializes in horizontal drilling services in the Permian Basin, highlighted its ability to maintain strong financial performance despite industry-wide challenges, including declining rig counts and reduced well completions in its core operating region.

Quarterly Performance Highlights

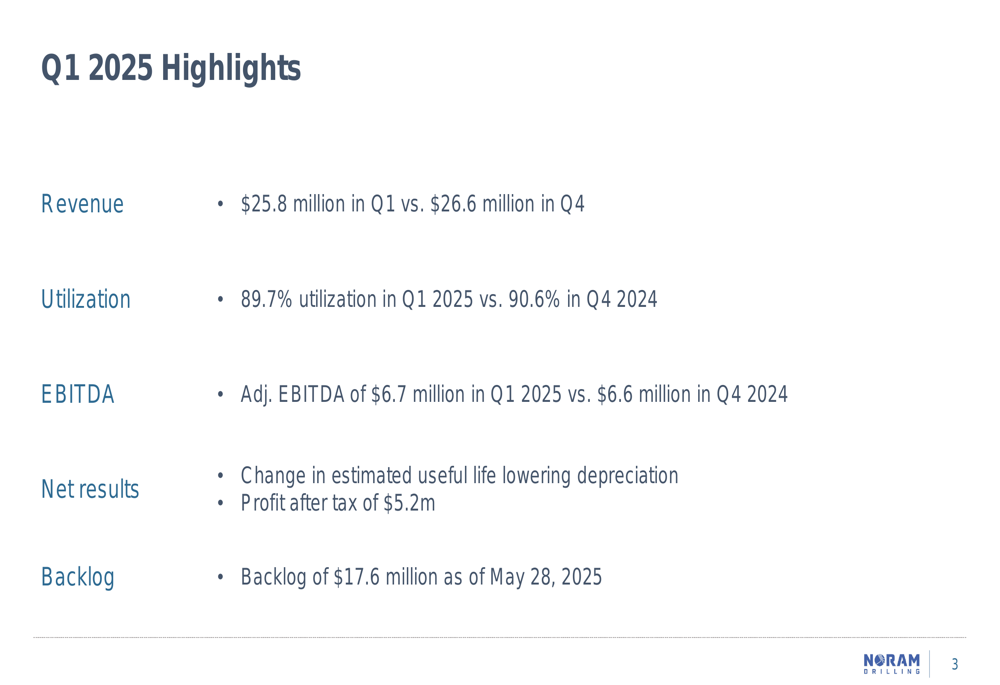

NorAm Drilling reported Q1 2025 revenue of $25.8 million, slightly down from $26.6 million in Q4 2024. Despite this modest revenue decline, the company achieved a substantial improvement in profitability, with profit after tax reaching $5.2 million compared to just $19,000 in the previous quarter.

The dramatic profit improvement was primarily attributed to a change in the company’s estimated useful life policy, which significantly lowered depreciation expenses. Depreciation fell to $1.45 million in Q1 2025 from $4.97 million in Q4 2024, directly boosting operating profit.

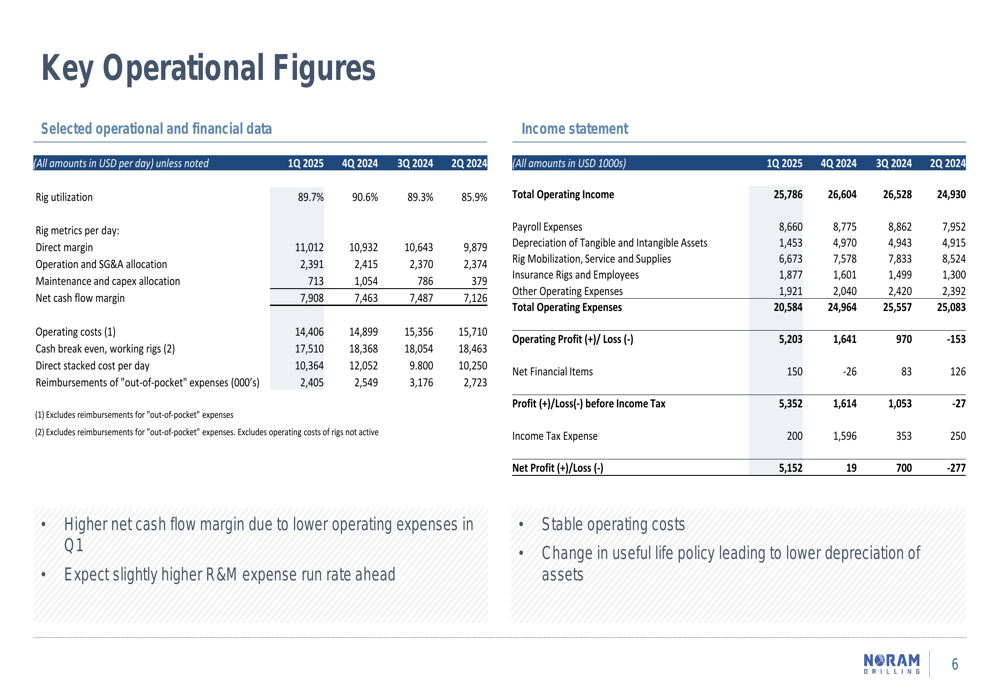

As shown in the following operational and financial data:

Other key performance metrics remained relatively stable. Rig utilization stood at 89.7% in Q1 2025, compared to 90.6% in the previous quarter, while adjusted EBITDA slightly increased to $6.7 million from $6.6 million. The company reported a backlog of $17.6 million as of May 28, 2025.

NorAm’s cash position improved significantly during the quarter, with net cash flow from operations reaching $9.55 million, more than double the $4.11 million generated in Q4 2024. This improvement was attributed to working capital reversals, resulting in a net increase in cash of approximately $4 million.

The company’s financial tables reveal consistent operational performance with improving cash flow margins:

Industry Outlook

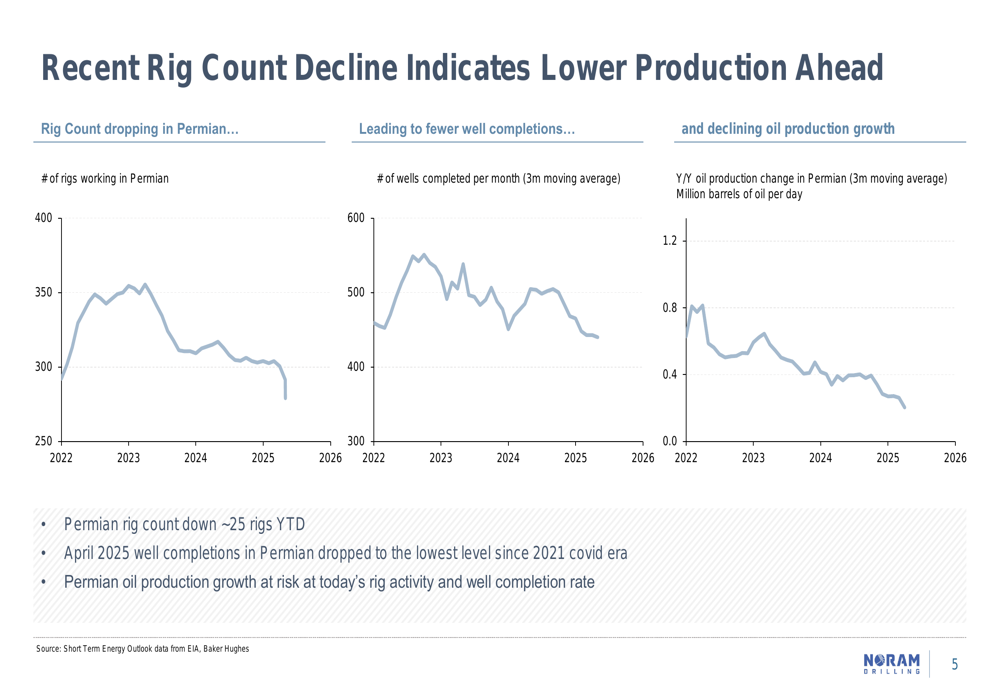

NorAm Drilling’s presentation painted a challenging picture of current market conditions in the Permian Basin. The company highlighted several concerning trends, including a decline of approximately 25 rigs in the Permian year-to-date and April 2025 well completions dropping to their lowest level since the COVID era of 2021.

These trends are illustrated in the following charts showing declining rig counts, fewer well completions, and slowing production growth:

Management noted that Permian oil production growth is at risk given today’s rig activity and well completion rates. The presentation acknowledged a "weaker near-term outlook" due to E&P capital expenditure reductions affecting rig demand in the short term. However, the company expressed expectations that natural gas-related drilling activity would likely increase going forward.

Strategic Position

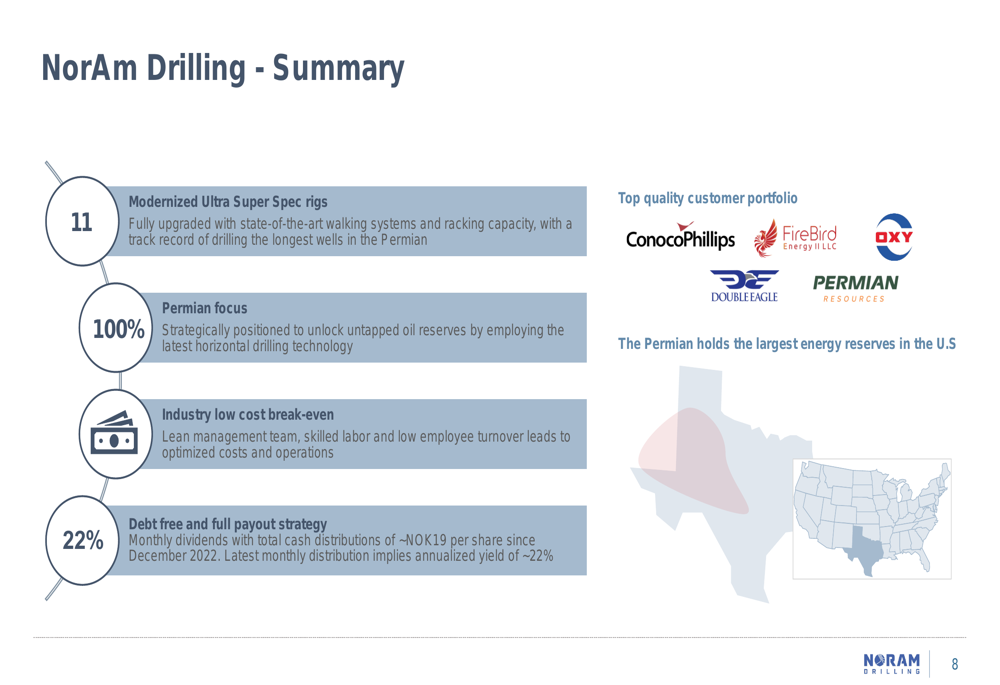

Despite the challenging market environment, NorAm Drilling emphasized its strong strategic positioning within the industry. The company highlighted its fleet of modernized "Ultra Super Spec" rigs, fully upgraded with state-of-the-art walking systems and enhanced racking capacity. Management noted the company’s track record of drilling the longest wells in the Permian Basin.

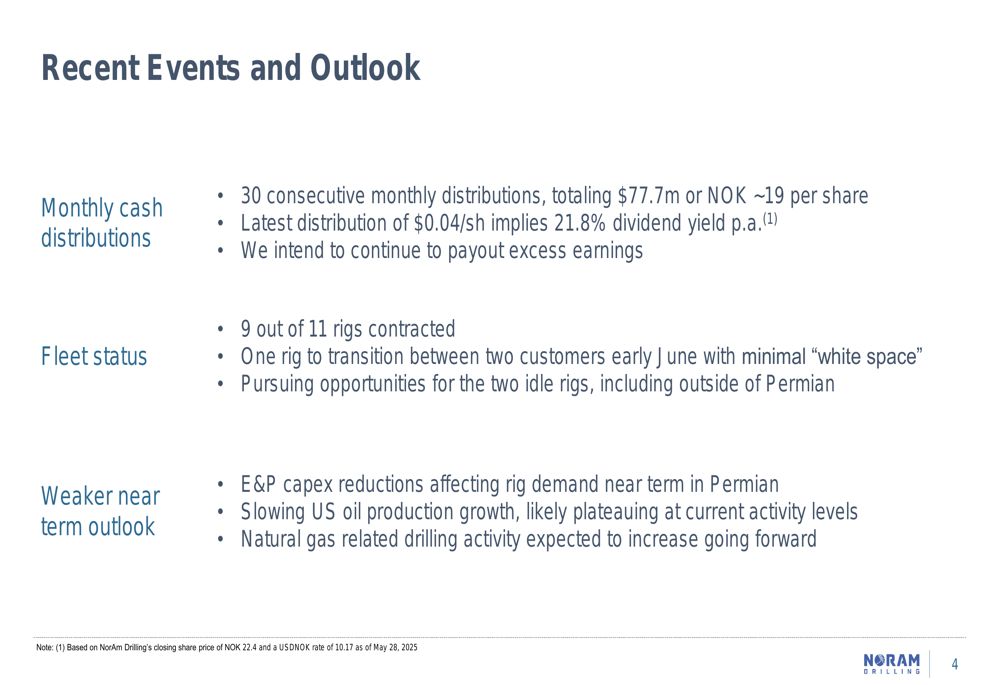

NorAm’s current fleet status shows 9 out of 11 rigs contracted, with one rig scheduled to transition between two customers in early June with minimal downtime. The company is actively pursuing opportunities for its two idle rigs, including potential work outside the Permian Basin.

The following slide summarizes NorAm’s key strategic attributes:

A key component of NorAm’s market positioning is its capital allocation strategy. The company has maintained 30 consecutive monthly cash distributions, totaling $77.7 million or approximately NOK 19 per share since December 2022. The latest distribution of $0.04 per share implies an annualized dividend yield of 21.8%, an attractive proposition for income-focused investors.

Forward-Looking Statements

Looking ahead, NorAm Drilling expressed its intention to continue its policy of distributing excess earnings to shareholders through dividends. However, management acknowledged near-term challenges, noting that U.S. oil production growth is likely slowing and possibly plateauing at current activity levels.

The company’s balance sheet remains strong, with no debt and total equity of $58.7 million as of Q1 2025. This financial flexibility positions NorAm to weather the current market uncertainty while maintaining its dividend policy.

As shown in the company’s recent events and outlook slide:

While the company faces industry headwinds, its high utilization rate, strong cash flow generation, and debt-free status provide a solid foundation for navigating the challenging market environment. Investors will be watching closely to see if NorAm can maintain its impressive dividend yield as the Permian Basin drilling market continues to evolve.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.