IonQ CRO Alameddine Rima sells $4.6m in shares

Introduction & Market Context

Nordic Mining ASA (OB:NOM) presented its Q2 2025 interim results on August 19, 2025, highlighting the achievement of first commercial revenue while navigating ongoing production ramp-up challenges. The company's stock closed at 18.24 NOK on August 18, down 1.94% ahead of the presentation, reflecting market caution about the company's path to profitability.

The quarter saw mixed market conditions for Nordic Mining's products. Titanium dioxide prices remained flat across most regions compared to Q1, with weak demand in the pigment segment but strong demand for titanium sponge. Meanwhile, the garnet abrasive market has tightened considerably, with growing demand due to supply curtailments from South Africa and delayed commissioning of new production in Australia – creating a favorable environment for Nordic Mining's first garnet shipments.

Quarterly Performance Highlights

The second quarter of 2025 marked several significant milestones for Nordic Mining, most notably the official opening of the Engebø Rutile and Garnet facility and the company's first commercial sale of garnet products. These developments represent crucial steps in the company's transition from construction to commercial operations.

Despite high operational activity throughout the quarter, production output remained limited as the company worked through various technical challenges. A maintenance shutdown was utilized to implement several improvements, particularly addressing underperforming slurry pumps and material handling issues. The company reported one Lost Time Injury (LTI) during the quarter, highlighting ongoing safety challenges during the ramp-up phase.

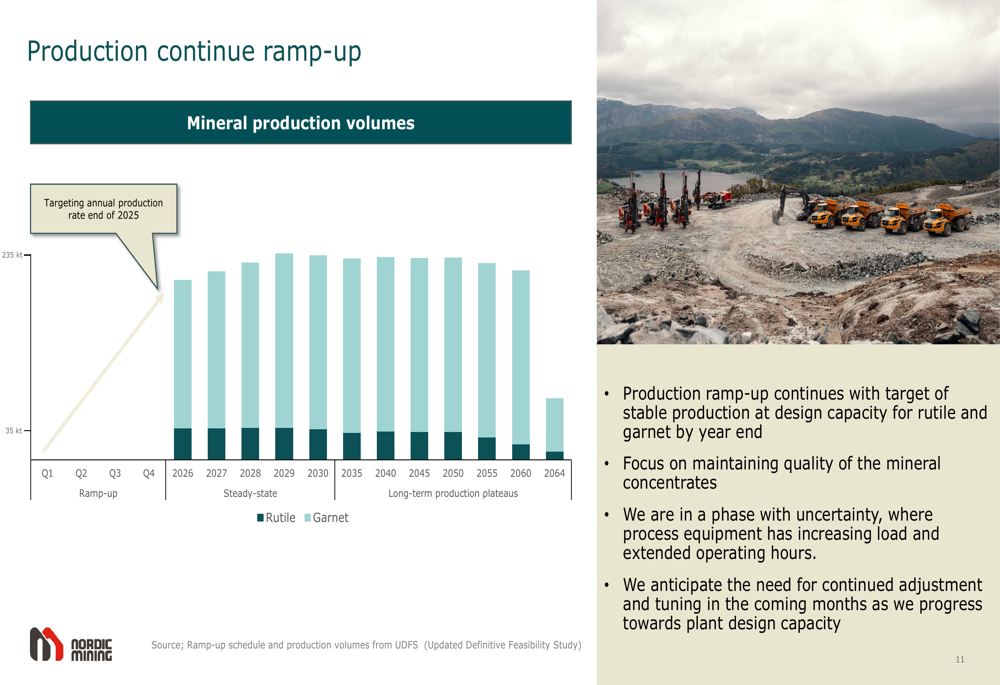

The company continued production of rutile during Q2 and aims to complete its first rutile shipment toward the end of the quarter, adding a second revenue stream to complement garnet sales. Management also noted a favorable verdict in the appeals case between NGOs and the government, though specific details weren't provided in the presentation.

Detailed Financial Analysis

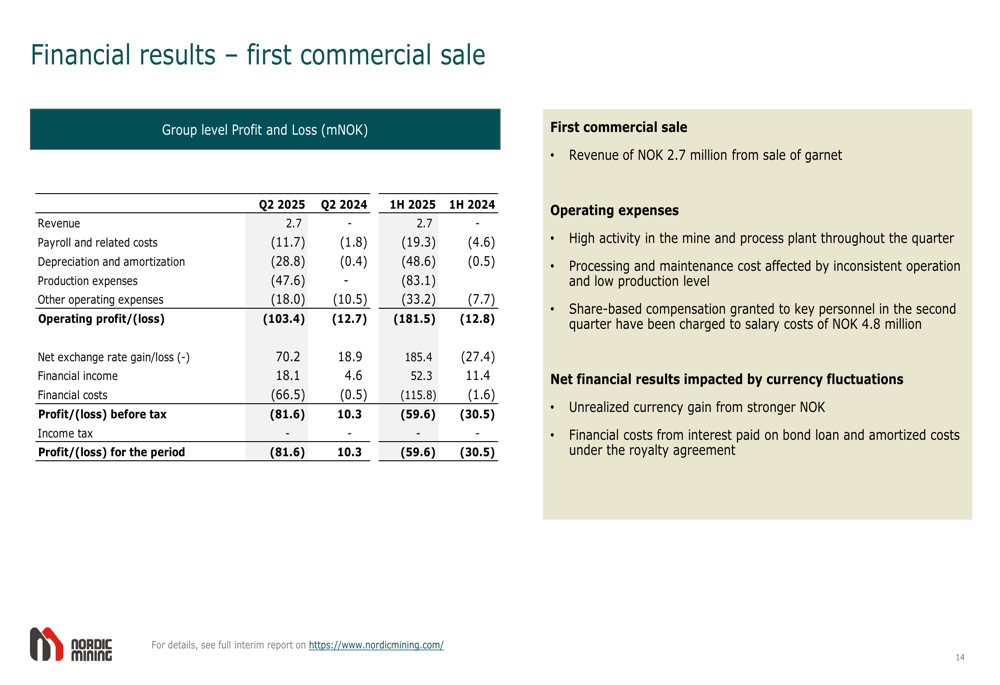

Nordic Mining reported its first commercial revenue of 2.7 million NOK from garnet sales in Q2 2025. However, the company continued to face significant cash burn due to high operational expenses and limited production output. The quarterly financial results showed an operating loss of 103.4 million NOK, with the loss before tax at 81.6 million NOK after accounting for currency fluctuations.

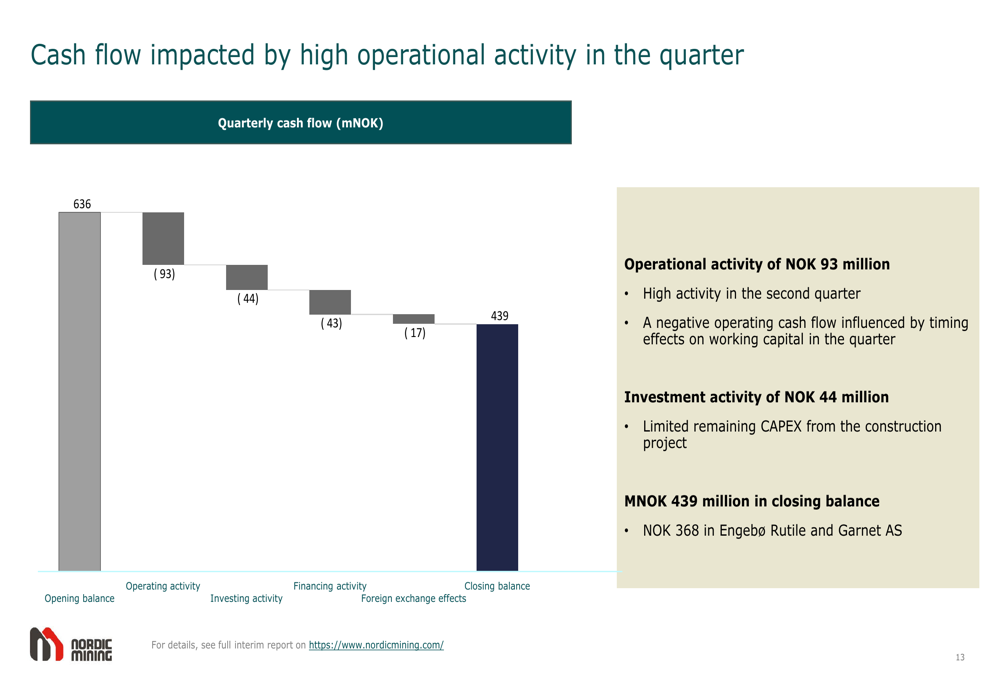

The cash flow statement revealed a substantial reduction in the company's cash position during the quarter. Opening with 636 million NOK, the company ended Q2 with 439 million NOK, representing a 197 million NOK decrease. This decline was attributed to negative operating cash flow (93 million NOK), continued investment activities (44 million NOK), financing activities (43 million NOK), and foreign exchange effects (17 million NOK).

This cash burn rate represents a concerning trend compared to Q1 2025, when the company reported a net cash flow increase of 169 million SEK and raised 349 million SEK through a TAP bond issue. The continued negative cash flow underscores the challenges Nordic Mining faces in reaching its previously stated goal of becoming cash flow positive by 2026.

Strategic Initiatives

Following the July maintenance shutdown, Nordic Mining implemented several technical improvements to address production bottlenecks. The company modified underperforming slurry pumps to achieve design flow rates and made adjustments to bulk material handling transfer chutes to improve material flow, reduce spillage, and increase operational time.

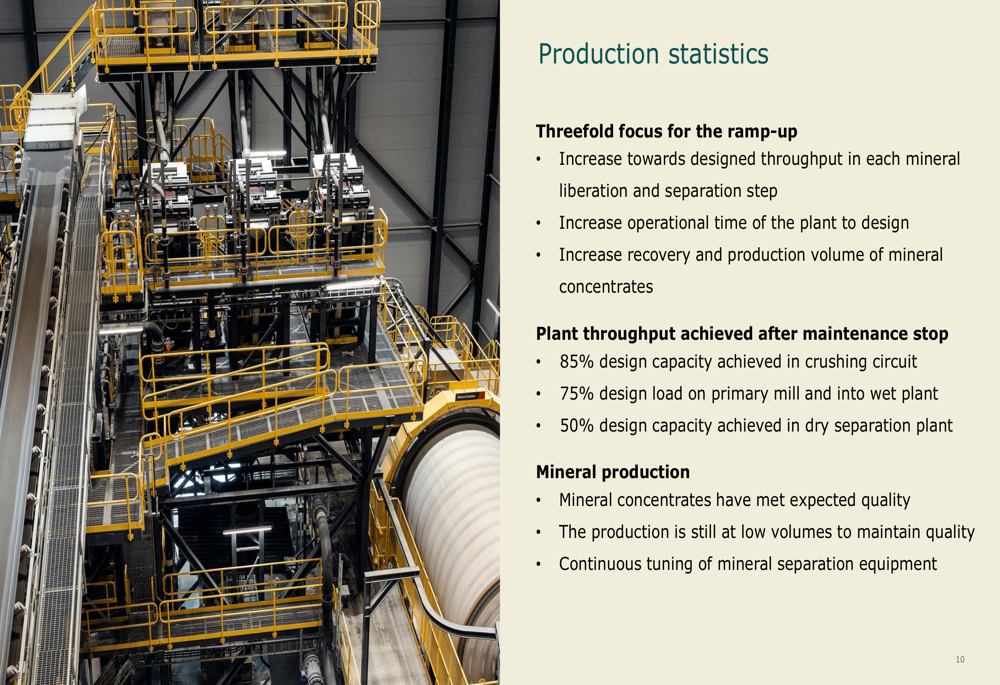

These improvements have yielded some positive results, with plant throughput reaching 85% of design capacity in the crushing circuit, 75% of design load on the primary mill, and 50% of design capacity in the dry separation plant. While these figures represent progress, they also highlight the significant gap remaining before the facility reaches full operational capacity.

The company's production ramp-up strategy focuses on three key areas: increasing designed throughput, extending operational time, and improving recovery/production volume. Management emphasized that mineral concentrates have met expected quality standards, though production volumes remain low as the company continues tuning separation equipment.

Forward-Looking Statements

Nordic Mining maintains its commitment to reaching stable production at design capacity for both rutile and garnet by the end of 2025. The company's target annual production rate by end-2025 is 235 kilotonnes, with steady-state production projected to continue until 2064, indicating a substantial mine life.

The presentation acknowledged ongoing uncertainty during the ramp-up phase, noting the need for increasing load and extended operating hours, with continued adjustments anticipated. The company is also working on an updated strategy, though specific details were not provided in the Q2 presentation.

When compared to statements from Q1 2025, where management confidently projected becoming cash flow positive by 2026, the Q2 presentation suggests a more cautious outlook given the significant cash burn and ongoing production challenges. Investors will likely be watching closely to see if Nordic Mining can accelerate its production ramp-up and reduce operational expenses to achieve its long-term financial goals.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.