Street Calls of the Week

Introduction & Market Context

Nordic Semiconductor (OB:OL:NOD) reported strong financial results for the second quarter of 2025, with significant year-over-year growth and improved profitability. The company presented its quarterly performance on August 13, 2025, highlighting continued revenue recovery, margin expansion, and strategic acquisitions that position Nordic for long-term growth.

The semiconductor company has maintained its leadership position in the Bluetooth Low Energy market while expanding its product portfolio and transitioning from a hardware-focused business to a complete solutions provider. Despite ongoing macroeconomic uncertainties and potential trade policy changes that could affect end-user demand, Nordic has capitalized on a gradual market recovery over the past year.

Quarterly Performance Highlights

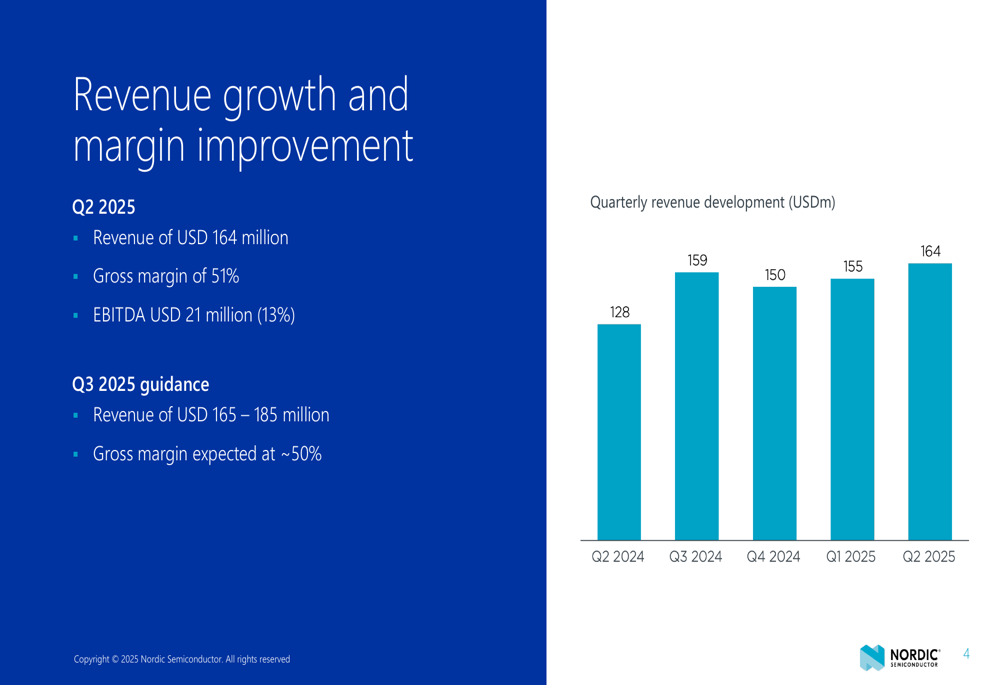

Nordic Semiconductor reported Q2 2025 revenue of $164 million, representing a 28% increase year-over-year and a 6% increase quarter-over-quarter. The company also achieved a gross margin of 50.7%, up from 42.0% in the same quarter last year, and generated EBITDA of $20.8 million (12.7% margin) compared to a negative $7.2 million in Q2 2024.

As shown in the following chart of quarterly revenue development, Nordic has demonstrated consistent growth over the past five quarters:

The company’s performance was driven by strong momentum across key markets, with the Consumer segment accounting for 61% of revenue ($100.3 million, up 15% year-over-year), followed by Industrial and Healthcare at 36% ($59.2 million, up 60% year-over-year), and Other markets at 2% ($4.1 million, up 39% year-over-year).

Nordic’s technology portfolio continues to be dominated by Short-range wireless solutions, which generated $154 million in Q2 2025, while Long-range cellular IoT contributed $8 million and Other revenue streams added $2 million.

Detailed Financial Analysis

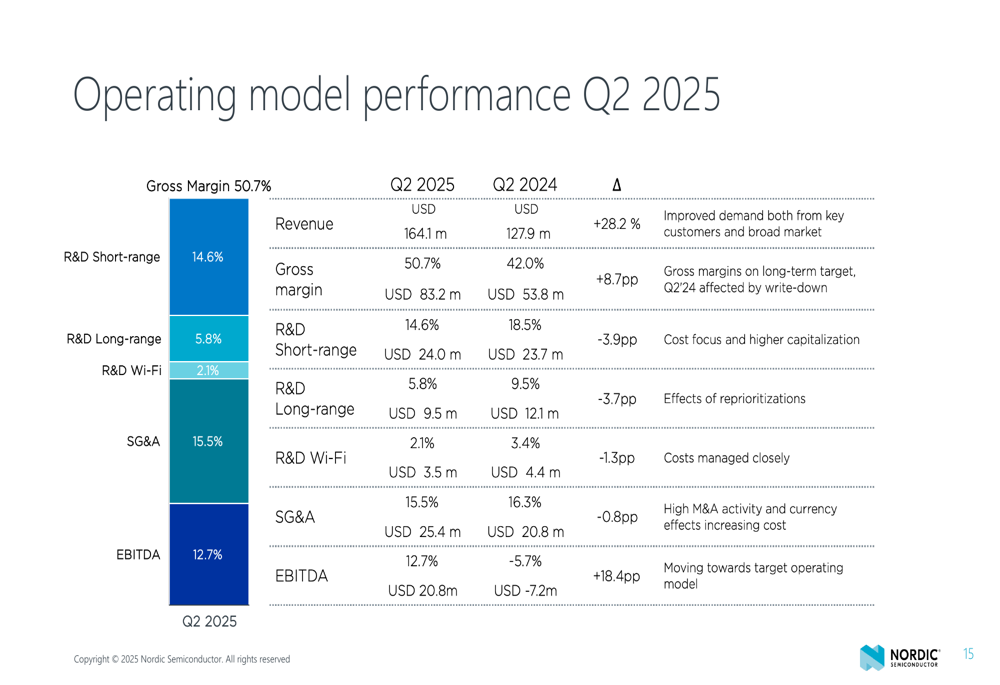

Nordic’s operating model showed significant improvement in Q2 2025 compared to the same period last year. The company maintained disciplined cost management while investing in key growth areas. The following chart illustrates the operating model performance:

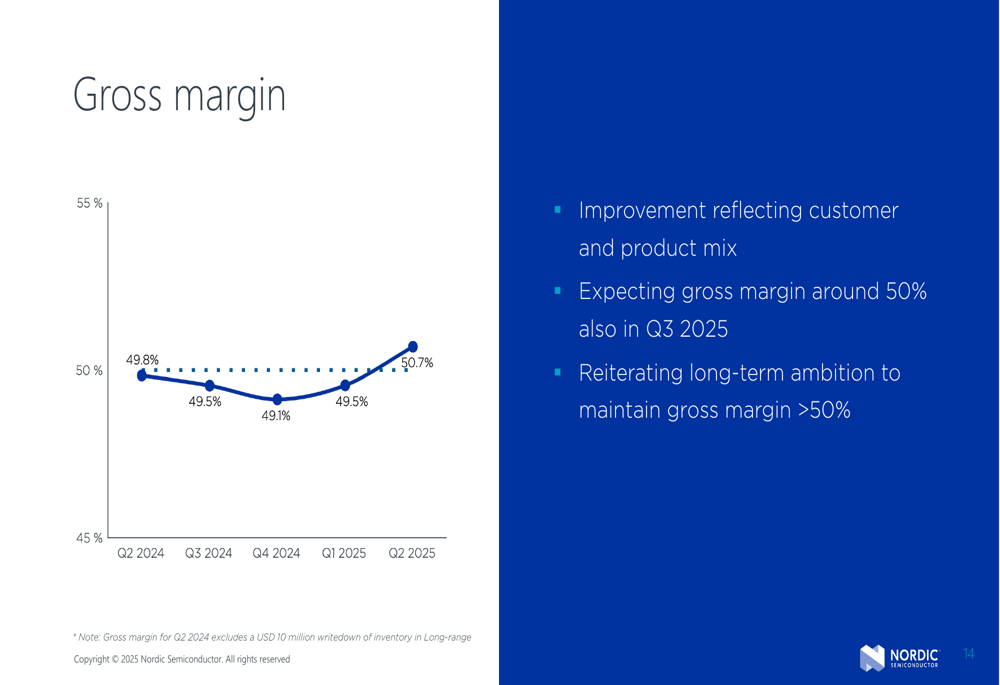

Gross margin has shown a steady improvement trend, reaching 50.7% in Q2 2025, up from 49.5% in the previous quarter. The company attributes this improvement to favorable customer and product mix, and expects to maintain a gross margin around 50% in Q3 2025.

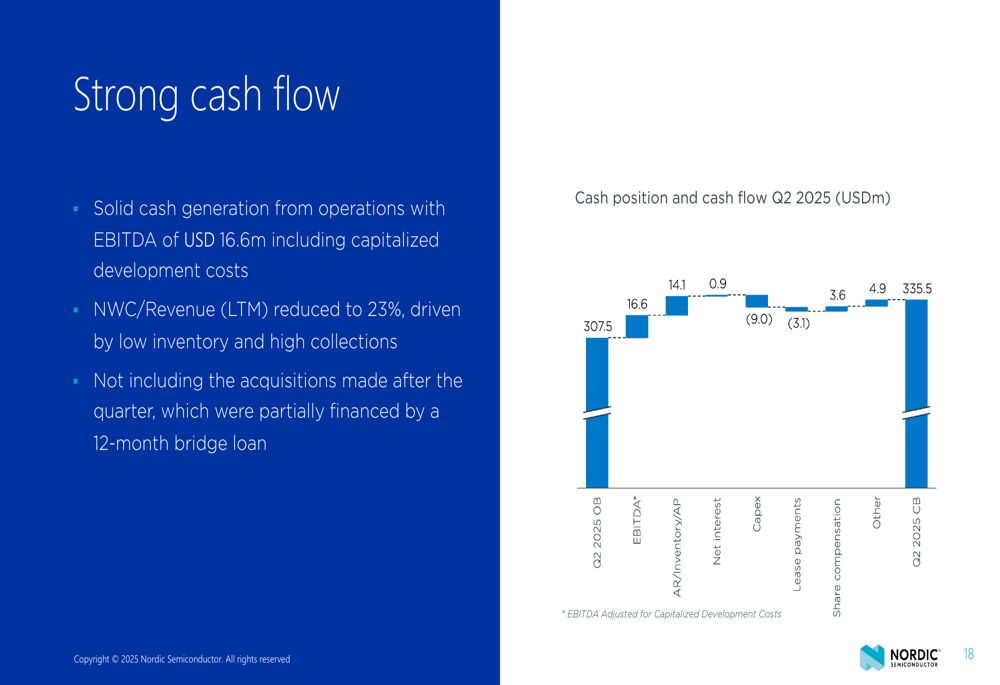

Nordic has demonstrated strong cash flow generation, with EBITDA of $16.6 million (including capitalized development costs) and a reduction in net working capital to 23% of revenue, driven by low inventory and high collections. The company ended Q2 2025 with a cash position of $335.5 million.

The company has maintained flat cash costs year-over-year despite inflationary and currency pressures, partly through a 5% reduction in headcount compared to Q2 2024. While capital expenditures saw a temporary uptick in Q2 driven primarily by supply chain capacity expansions and IT infrastructure investments, capex intensity for the last 12 months remained at 2.8% of revenue.

Strategic Initiatives

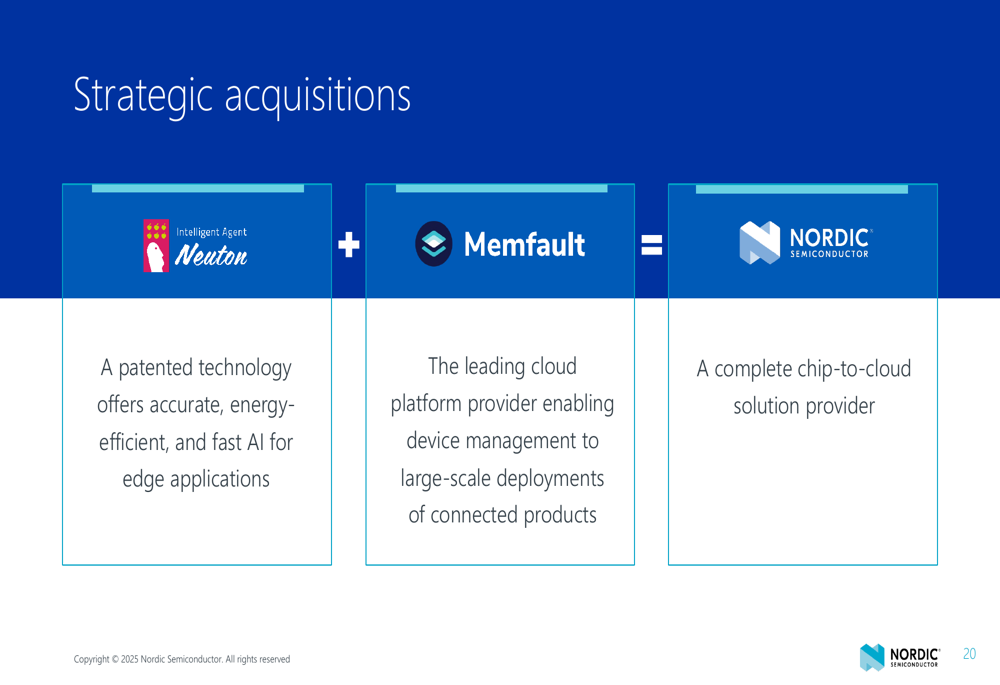

A key highlight of Nordic’s Q2 2025 presentation was the announcement of strategic acquisitions that accelerate the company’s transformation from a hardware provider to a complete solutions partner. Nordic acquired Neuton, which offers patented technology for accurate, energy-efficient, and fast AI for edge applications, and Memfault, a leading cloud platform provider enabling device management for large-scale deployments of connected products.

As shown in the following slide, these acquisitions position Nordic as a complete chip-to-cloud solution provider:

Nordic claims to be the first semiconductor company to combine best-in-class hardware, software, edge AI, and cloud services, enabling customers to build, deploy, and upgrade connected products to meet evolving requirements and increasing software complexity.

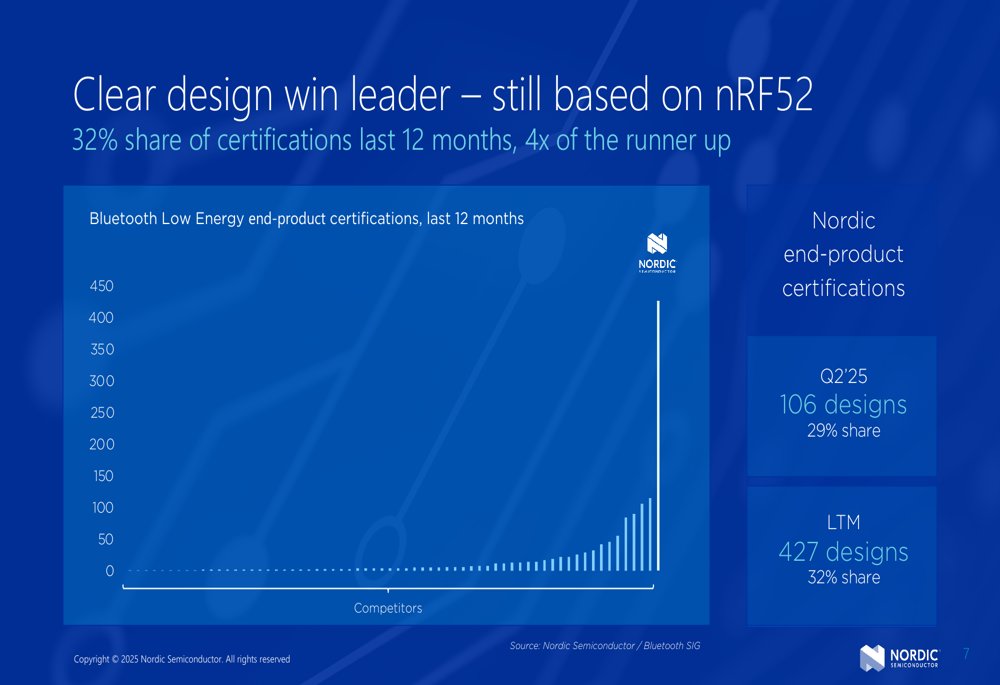

The company also maintains its leadership position in Bluetooth Low Energy design wins, with a 32% share of certifications over the last 12 months—four times that of the runner-up. Nordic reported 106 design wins in Q2 2025 (29% market share) and 427 designs over the last twelve months (32% market share).

Nordic continues to expand its product portfolio, announcing the launch of the nPM1304 PMIC (Power Management Integrated Circuit), designed for next-generation, space-constrained applications with ultra-small batteries. The company also reported strong customer design pipeline for its nRF54L, nRF54H, nRF9151, and new PMIC offerings, with multiple new innovative products planned for launch within the nRF54 Series in the second half of 2025.

Forward-Looking Statements

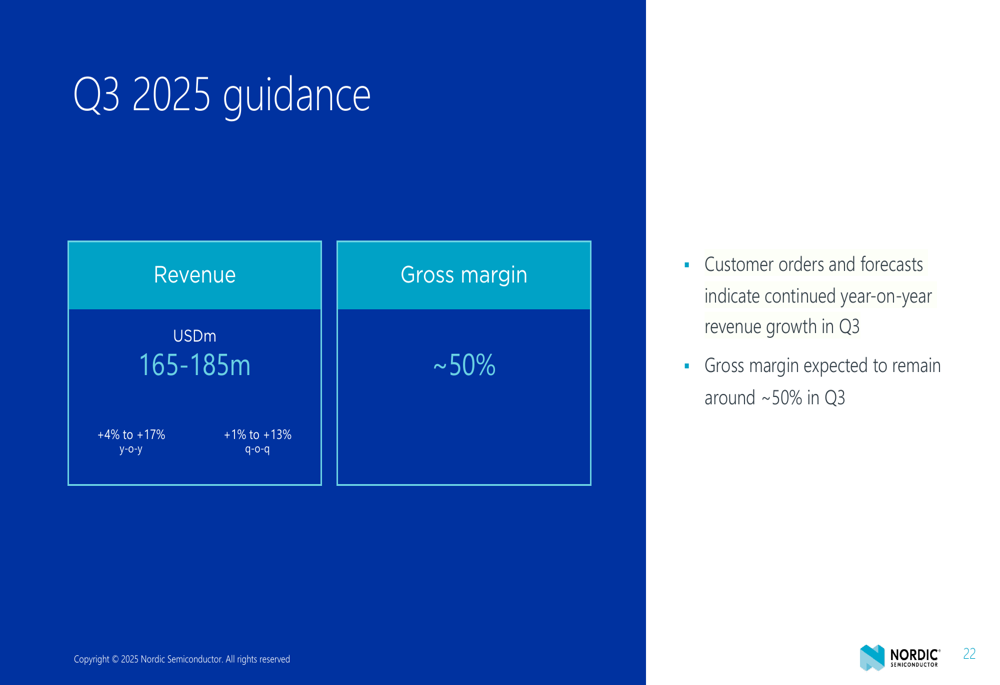

Looking ahead to Q3 2025, Nordic Semiconductor provided revenue guidance of $165-185 million, representing 4-17% year-over-year growth and 1-13% quarter-over-quarter growth. The company expects gross margin to remain around 50% in the third quarter.

Management indicated that customer orders and forecasts suggest continued year-on-year revenue growth in Q3, though they noted that macroeconomic uncertainty persists, with trade policy changes and tariffs potentially affecting end-user demand.

The company also highlighted that while its new product launches and acquisitions will have limited revenue impact in 2025, they are expected to accelerate growth from 2026 onward. The acquisitions will increase quarterly operating expenses by approximately $4 million starting in Q3 2025.

Nordic’s long-term ambition remains to maintain gross margins above 50%, with a continued focus on cost management to improve overall profitability. The company’s strategic transformation into a complete solutions provider, combined with its market leadership in Bluetooth Low Energy and expanding product portfolio, positions Nordic Semiconductor for sustained growth despite ongoing market challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.