European shares fall: Trump threatens ’massive’ tariff increase on China

Introduction & Market Context

Nordrest Holding AB (NREST), a Swedish foodservice company with operations across the Nordic region, presented its Q2 2025 interim report on August 28, 2025, highlighting substantial revenue growth and strategic expansion initiatives. The company, which describes itself as "the hungriest foodservice company in Sweden," operates with a decentralized model focused on locations with predictable guest flows across various sectors including defense, corporate, education, and healthcare.

The company’s stock closed at 195.2 SEK on August 27, 2025, near its 52-week high of 212 SEK, reflecting investor confidence in its growth strategy and financial performance.

Quarterly Performance Highlights

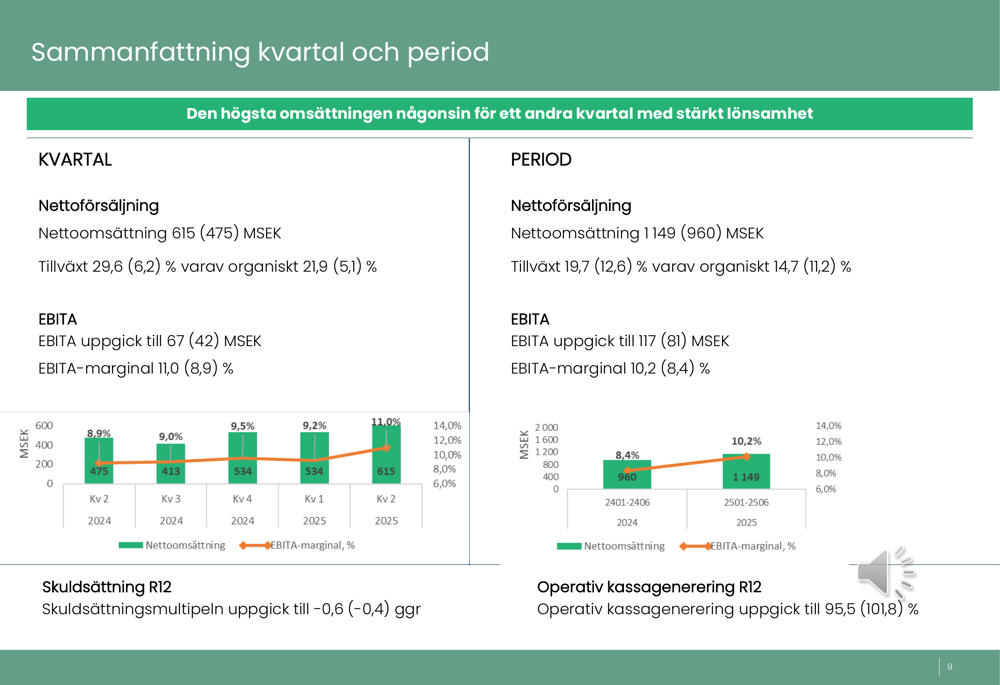

Nordrest reported impressive financial results for Q2 2025, with net sales reaching 615 million SEK, a 29.6% increase compared to 475 million SEK in the same period last year. Organic growth accelerated significantly to 21.9%, up from 5.1% in Q2 2024.

Profitability also improved substantially, with EBITA rising to 67 million SEK from 42 million SEK in the prior-year quarter. The EBITA margin expanded to 11.0%, compared to 8.9% in Q2 2024, exceeding the company’s medium-term target range of 8-10%.

As shown in the following chart of quarterly financial performance:

For the first half of 2025, Nordrest reported net sales of 1,149 million SEK, representing a 19.7% increase from 960 million SEK in H1 2024. EBITA for the six-month period reached 117 million SEK, up from 81 million SEK, with the EBITA margin improving to 10.2% from 8.4%.

The company maintained a strong financial position with a negative leverage ratio (Net Debt/EBITDA) of -0.6x, indicating a net cash position. Operating cash generation remained robust at 95.5% on a trailing twelve-month basis, though slightly down from 101.8% in the comparable period.

Detailed Financial Analysis

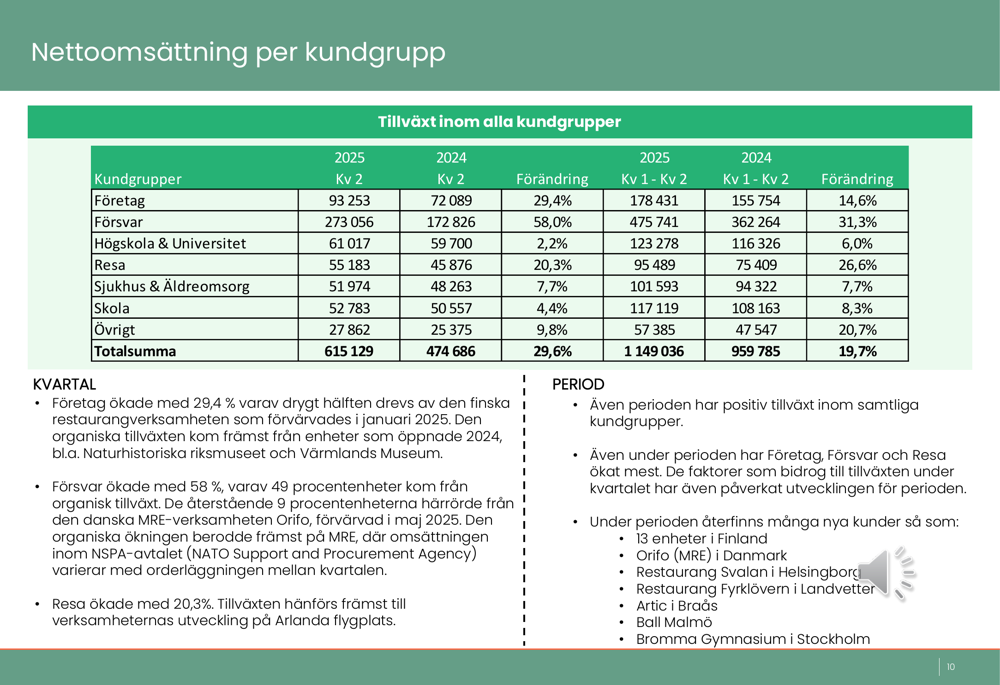

Nordrest achieved growth across all customer segments in Q2 2025, with particularly strong performance in the defense sector, which saw a 58.0% increase in sales compared to Q2 2024. The corporate segment also performed well, with 29.4% growth, while the travel segment grew by 20.3%. Other segments showed more modest growth: hospitals and elderly care (7.7%), schools (4.4%), and higher education (2.2%).

The following breakdown illustrates growth across all customer segments:

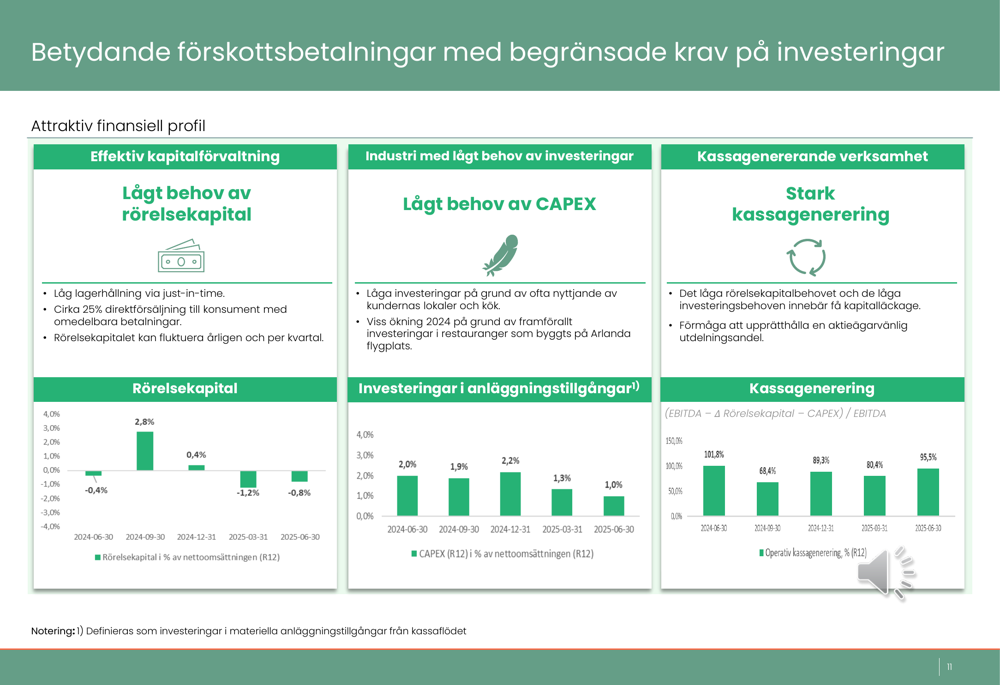

The company’s business model continues to demonstrate capital efficiency with low working capital requirements and minimal investment needs. This translates into strong cash generation, supporting Nordrest’s shareholder-friendly dividend policy of distributing more than 50% of profit after tax.

The company’s financial profile is illustrated in this chart showing capital efficiency metrics:

Strategic Initiatives

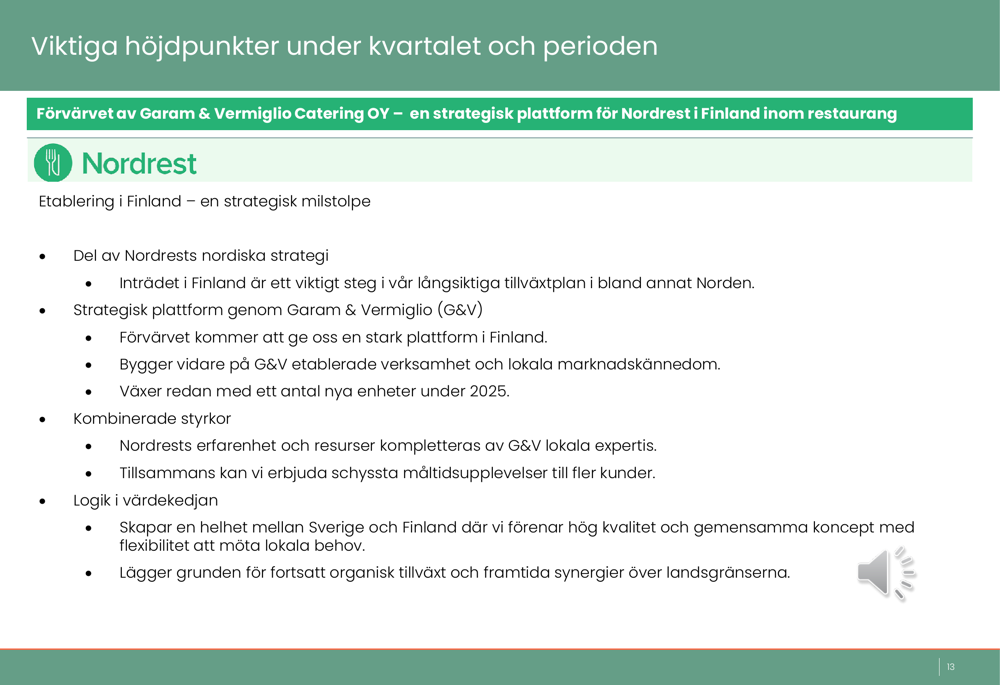

Nordrest highlighted several strategic developments during the quarter that support its Nordic expansion strategy. The company acquired Garam & Vermiglio Catering OY in Finland, establishing a strategic platform in the Finnish restaurant market. This acquisition aligns with Nordrest’s Nordic growth strategy and leverages G&V’s established operations and local knowledge.

The strategic rationale for the Finnish acquisition is detailed in the following slide:

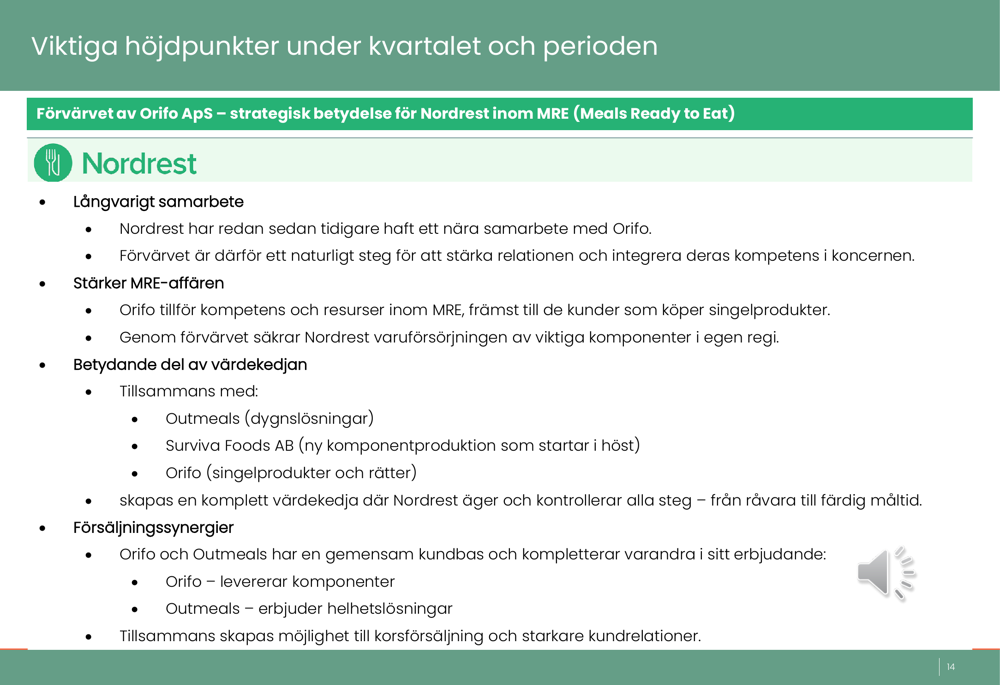

Additionally, Nordrest acquired Orifo ApS in Denmark to strengthen its Meals Ready to Eat (MRE) business. This acquisition integrates expertise and secures the supply of components for Nordrest’s MRE operations. Together with Outmeals and Surviva Foods AB, this creates a complete value chain where Nordrest controls all steps of the process.

The benefits of the Orifo acquisition are outlined in this slide:

In a significant development for its defense sector business, Nordrest extended its agreement with the Swedish Armed Forces until March 31, 2028, with an option for an additional year. This extension provides revenue stability in one of the company’s fastest-growing segments.

Forward-Looking Statements

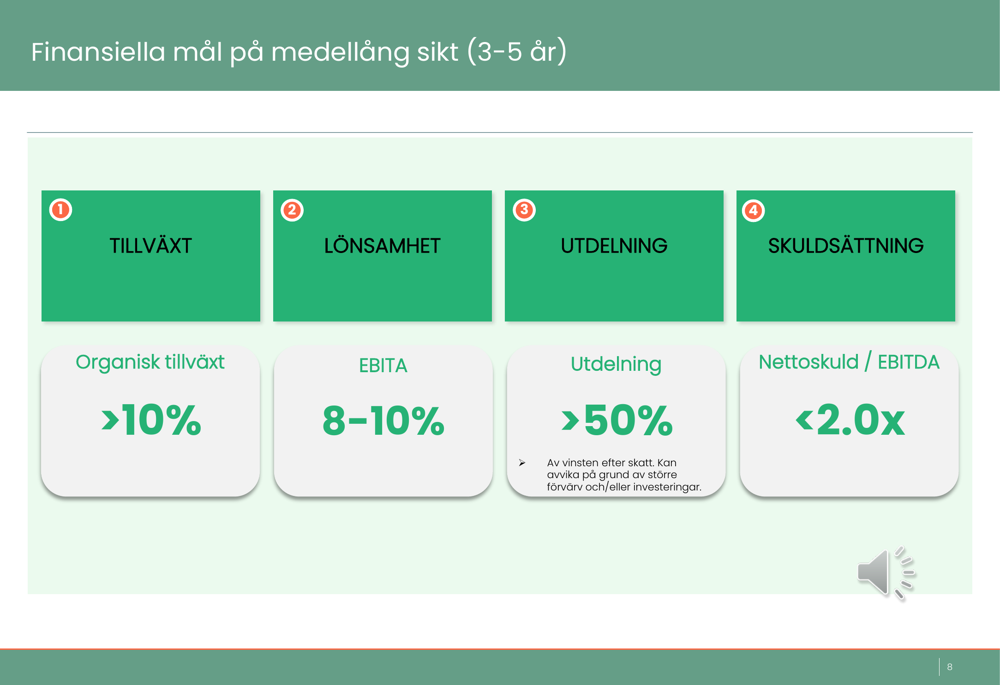

Nordrest reaffirmed its medium-term financial goals for the next 3-5 years, targeting organic growth exceeding 10%, an EBITA margin of 8-10%, and a dividend payout of more than 50% of profit after tax. The company aims to maintain a leverage ratio (Net Debt/EBITDA) of 2.0x, though it currently operates with a net cash position.

The company’s financial targets are clearly presented in this slide:

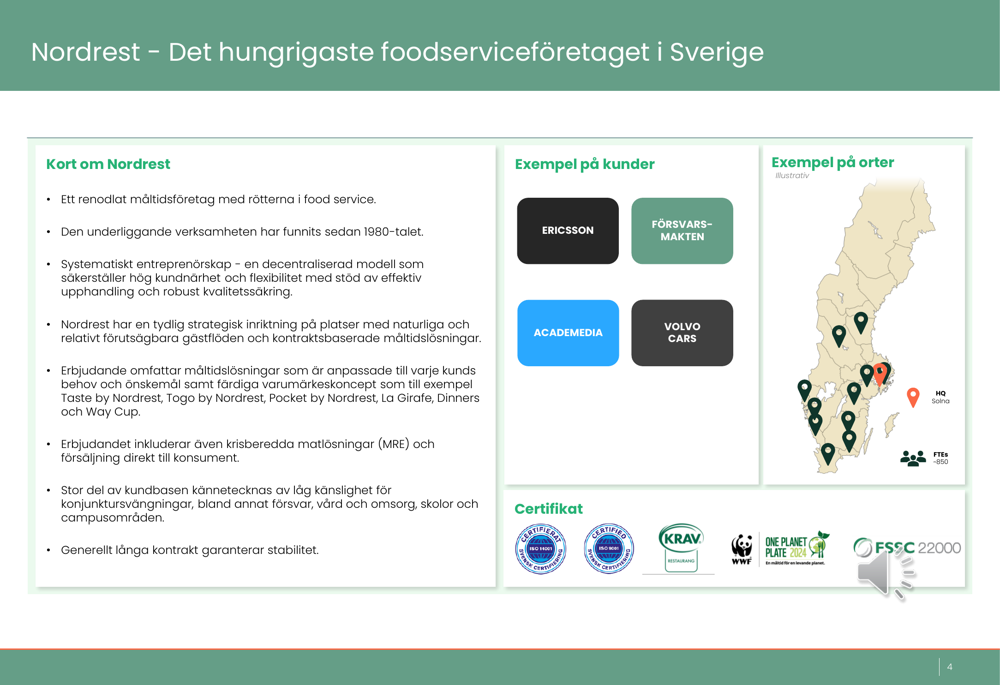

Nordrest’s business model focuses on locations with natural guest flows to minimize marketing costs and improve planning. The company serves a diverse customer base that is relatively insensitive to economic cycles, including defense, corporate, education, healthcare, and travel sectors.

The company’s overview and customer base are illustrated in this comprehensive slide:

With its recent acquisitions in Finland and Denmark, along with the extended contract with the Swedish Armed Forces, Nordrest appears well-positioned to continue its growth trajectory across the Nordic region while maintaining strong profitability and cash generation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.