Street Calls of the Week

Introduction & Market Context

Norse Atlantic ASA (OL:NORSE) reported strong second-quarter results on August 19, 2025, marking a significant milestone with its first positive EBIT since inception. The airline’s stock responded favorably to the results, rising 9.47% to close at $10.06, continuing its impressive recovery from a 52-week low of $1.50.

The transatlantic carrier has been executing a strategic transformation focused on route optimization and diversifying revenue streams through charter agreements. This approach appears to be bearing fruit as the company delivered substantial improvements across key operational and financial metrics.

Quarterly Performance Highlights

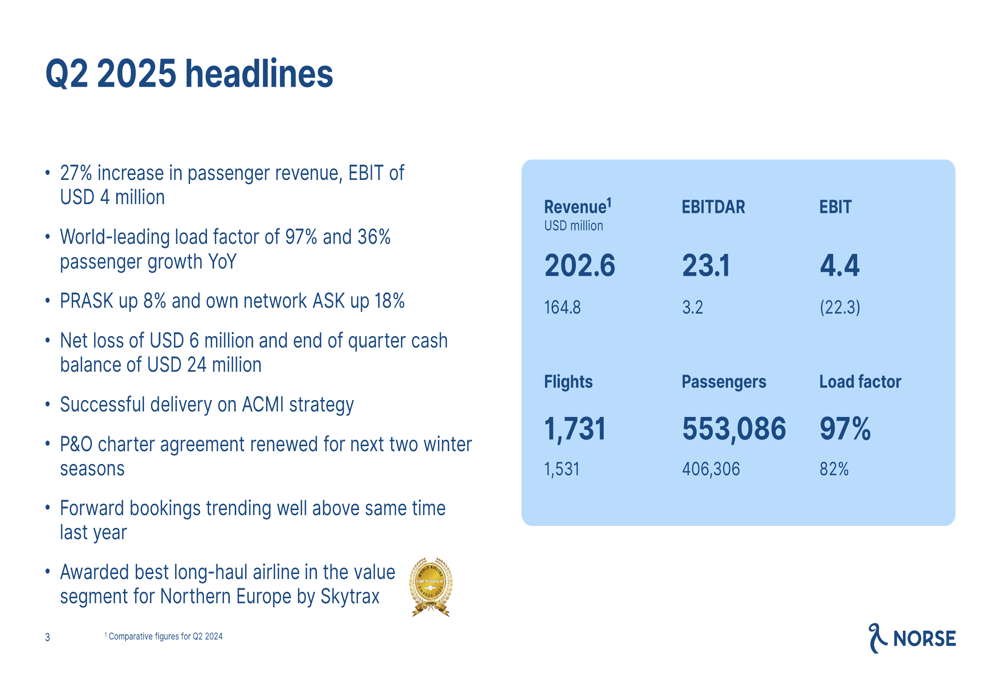

Norse Atlantic reported Q2 2025 revenue of $202.6 million, a 23% increase from $164.8 million in the same period last year. The company achieved a positive EBIT of $4.4 million, a remarkable turnaround from the $22.3 million loss in Q2 2024. Despite this operational improvement, the airline still recorded a net loss of $6 million, though significantly reduced from previous quarters.

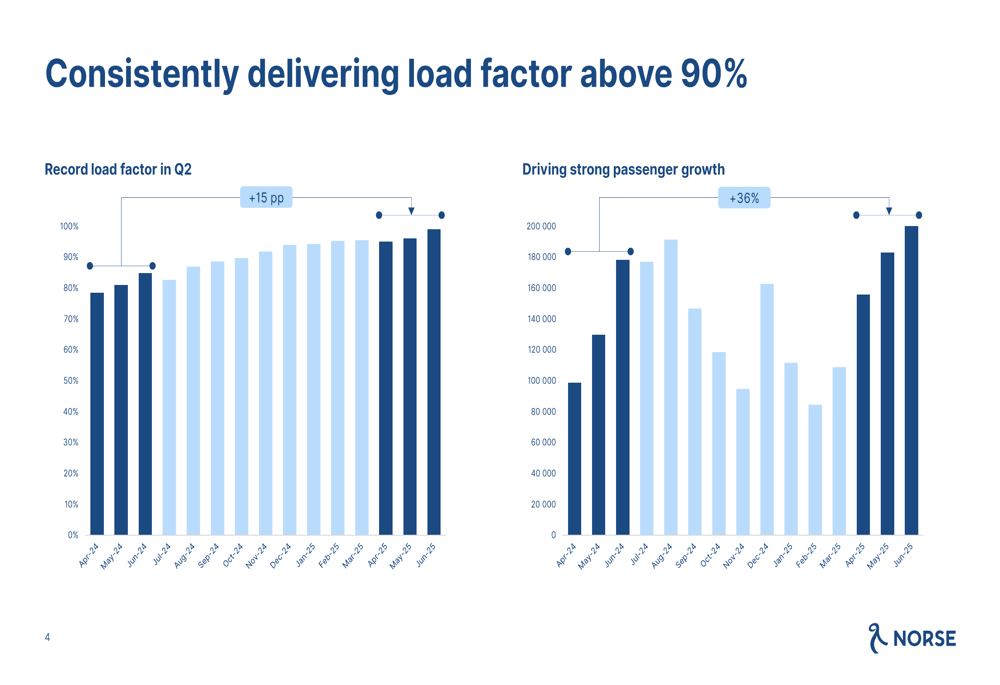

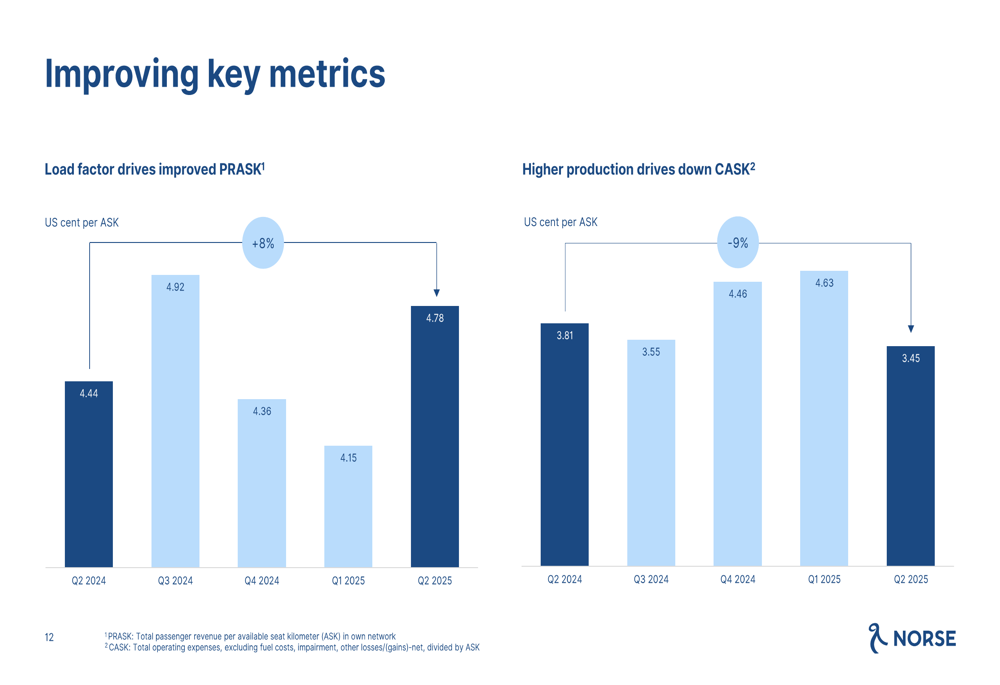

The airline’s operational performance was particularly impressive, achieving a world-leading load factor of 97%, up 15 percentage points year-over-year. Passenger numbers grew by 36% compared to Q2 2024, while the company managed to increase its passenger revenue per available seat kilometer (PRASK) by 8% while simultaneously reducing cost per available seat kilometer (CASK) by 9%.

As shown in the following chart highlighting key performance indicators:

The company’s ability to consistently improve load factors has been a key driver of its financial turnaround. The following visualization demonstrates this upward trend:

Detailed Financial Analysis

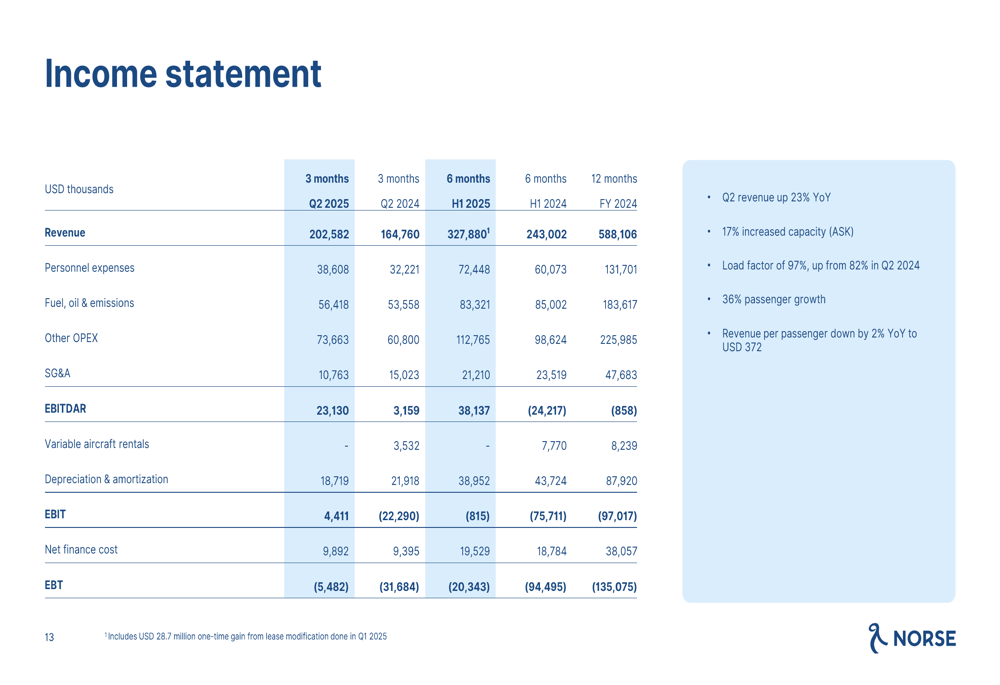

Norse Atlantic’s income statement reveals significant improvements across multiple metrics. EBITDAR increased to $23.1 million, compared to just $3.2 million in Q2 2024. The company managed to control personnel expenses despite growth, with a more modest increase to $38.6 million from $32.2 million year-over-year. Notably, SG&A expenses decreased to $10.8 million from $15 million in the same period last year, demonstrating improved operational efficiency.

The detailed income statement provides a comprehensive view of the financial performance:

The company’s cash flow position has also strengthened considerably. Operating cash flows before working capital movements reached $24.9 million in Q2 2025, compared to just $2 million in Q2 2024. The end-of-quarter cash balance stood at $24 million, up from $23 million at year-end 2024, with available liquidity of $44 million.

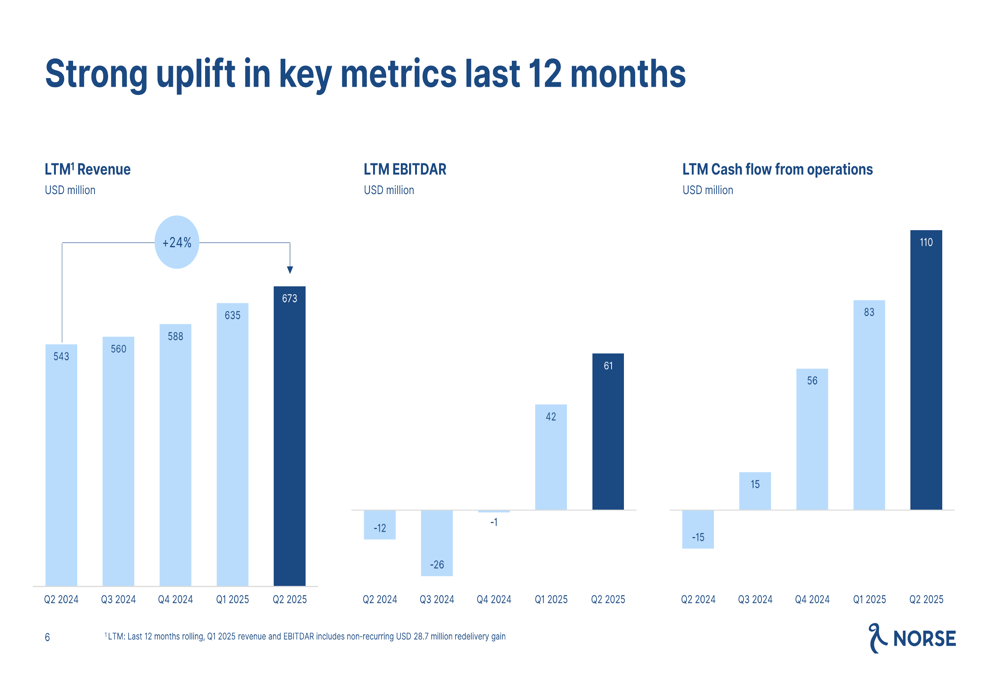

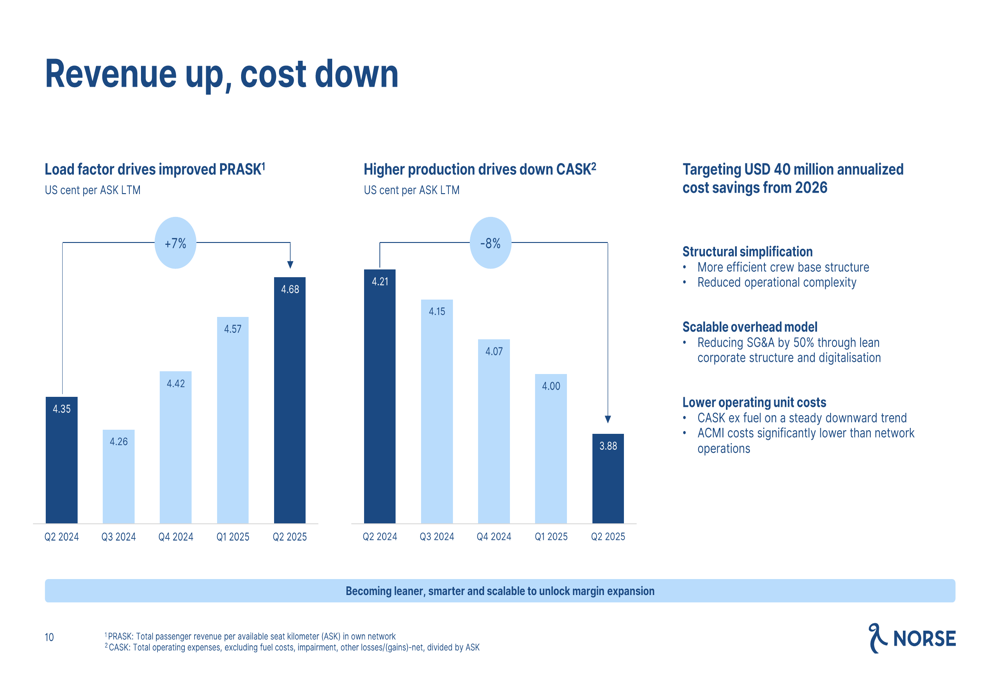

Looking at longer-term trends, Norse Atlantic has demonstrated consistent improvement in key metrics over the past 12 months:

The company has made significant progress in improving its revenue generation while simultaneously reducing costs. PRASK increased to 4.92 US cents in Q2 2025 from 4.55 US cents in Q2 2024, while CASK decreased to 3.45 US cents from 3.81 US cents during the same period:

Strategic Initiatives

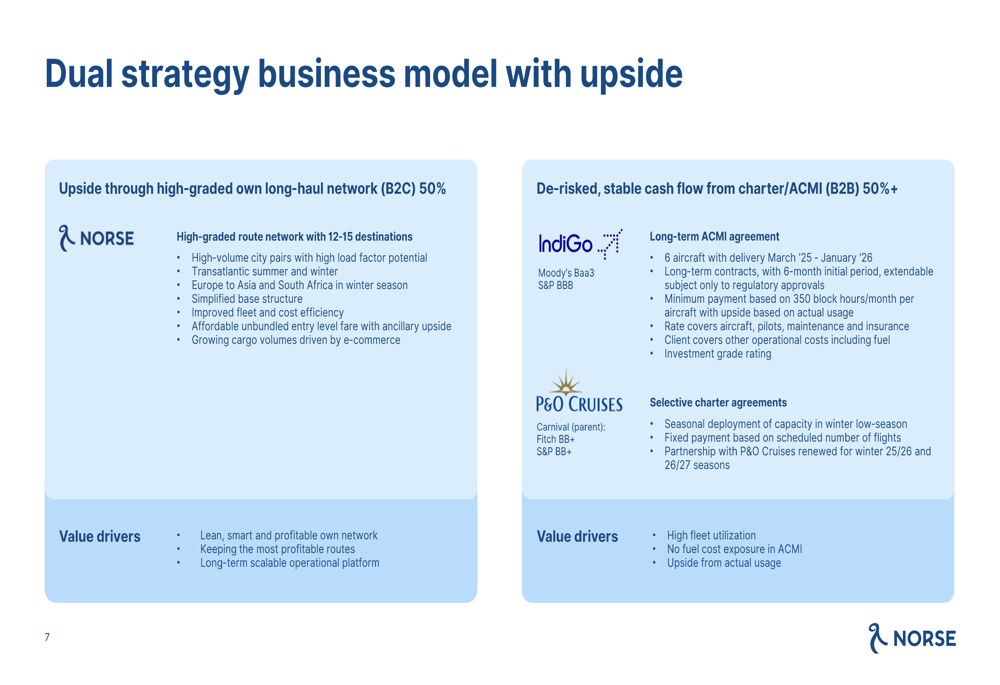

Norse Atlantic’s business model is built on a dual strategy that balances growth opportunities with risk mitigation. The company allocates approximately 50% of its capacity to its own long-haul network (B2C), focusing on high-volume city pairs and transatlantic routes. The remaining 50%+ is dedicated to charter and ACMI (Aircraft, Crew, Maintenance, and Insurance) agreements with partners like IndiGo and P&O Cruises, providing more stable and predictable cash flows.

The following illustration outlines this strategic approach:

A key element of the company’s strategy involves optimizing its route network by focusing on the most profitable destinations. Norse Atlantic plans to shift less profitable routes to ACMI operations while maintaining the highest-performing routes in its own network. The company has scheduled aircraft deliveries to IndiGo starting in September 2025, with five aircraft to be delivered by January 2026.

The airline is also targeting $40 million in annualized cost savings from 2026 through structural simplification, a scalable overhead model, and lower operating unit costs. Current aircraft utilization stands at approximately 75% of target capacity, with plans to increase this to 93%, representing a 24% increase in total production.

As shown in the following revenue and cost trend analysis:

Forward-Looking Statements

Norse Atlantic is aiming to deliver full-year profitability in 2025, building on its positive EBIT achievement in Q2. The company reports that forward bookings are trending well above the same time last year, suggesting continued strong demand for its services.

The renewal of the P&O charter agreement for the next two winter seasons provides additional revenue stability, while the successful execution of the ACMI strategy with partners like IndiGo reduces risk exposure. The company was also recently awarded "Best Long-haul Airline in the Value Segment for Northern Europe" by Skytrax, potentially enhancing its brand reputation and customer acquisition efforts.

Looking ahead, Norse Atlantic’s focus remains on high-grading its route network to drive profitability, replacing lower-margin routes with stable charter/ACMI contributions, and continuing to improve operational efficiency. While the company has made significant progress toward profitability with its first positive EBIT, challenges remain in achieving consistent net profits and strengthening its balance sheet position.

The company’s stock performance suggests growing investor confidence in this strategic direction, with shares now trading near their 52-week high of $10.10, representing a remarkable recovery from earlier lows. As Norse Atlantic continues to execute its dual strategy business model and drive operational improvements, investors will be watching closely to see if the positive EBIT in Q2 2025 marks the beginning of sustainable profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.