Fannie Mae, Freddie Mac shares tumble after conservatorship comments

Introduction & Market Context

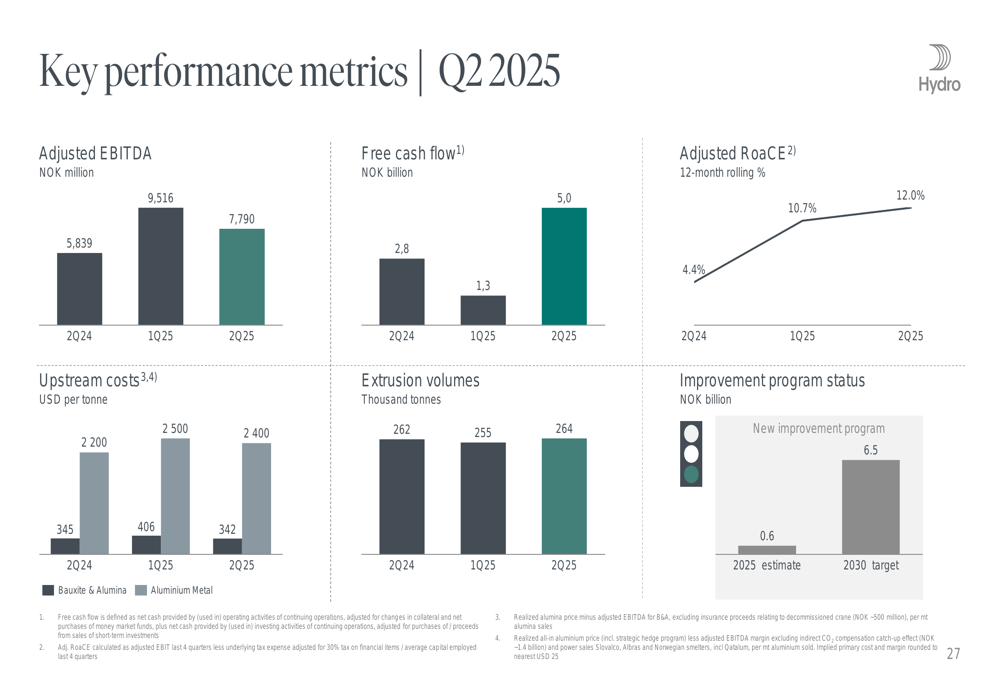

Norsk Hydro ASA (OTC:NHYDY) (OB:NHY) presented its second quarter 2025 results on July 22, highlighting a challenging period marked by market uncertainty and declining performance. The aluminum producer reported adjusted EBITDA of NOK 7.8 billion, down from NOK 9.5 billion in the previous quarter, as the company navigates an increasingly volatile global market environment.

President and CEO Eivind Kallevik emphasized the company’s focus on "performance and capital discipline" amid what the presentation described as "uncertain markets" influenced by geopolitical tensions including U.S. tariffs, the Russia-Ukraine conflict, and Middle East instability.

Quarterly Performance Highlights

Norsk Hydro’s Q2 2025 results showed mixed performance across key metrics. While the company maintained a free cash flow of NOK 5 billion and an adjusted return on average capital employed (RoaCE) of 12%, the quarter-over-quarter decline in adjusted EBITDA signals growing challenges.

As shown in the following chart detailing the company’s performance metrics:

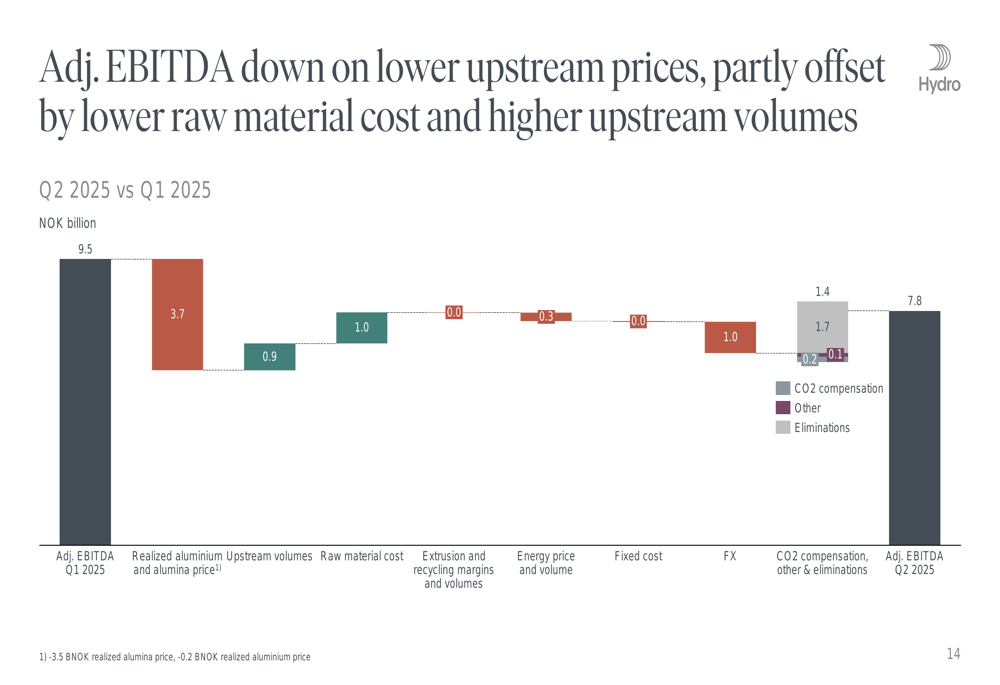

The decline in adjusted EBITDA from Q1 to Q2 2025 was primarily attributed to lower realized aluminum and alumina prices, which had a negative impact of NOK 3.7 billion. This was partially offset by increased upstream volumes (+NOK 0.9 billion), decreased raw material costs (+NOK 1.0 billion), and favorable currency effects (+NOK 1.4 billion).

The following waterfall chart illustrates these factors:

Safety remains a priority for Norsk Hydro, with the company reporting improvements in both Total (EPA:TTEF) Recordable Injuries (TRI) and High Risk Incidents (HRI) per million hours worked. The TRI rate per end-Q2 2025 stood at 1.96, below the average of 2.57 since Q2 2020, while the HRI rate was 0.61, compared to an average of 1.08 since Q2 2020.

Segment Performance Analysis

Norsk Hydro’s business segments showed varying performance in Q2 2025:

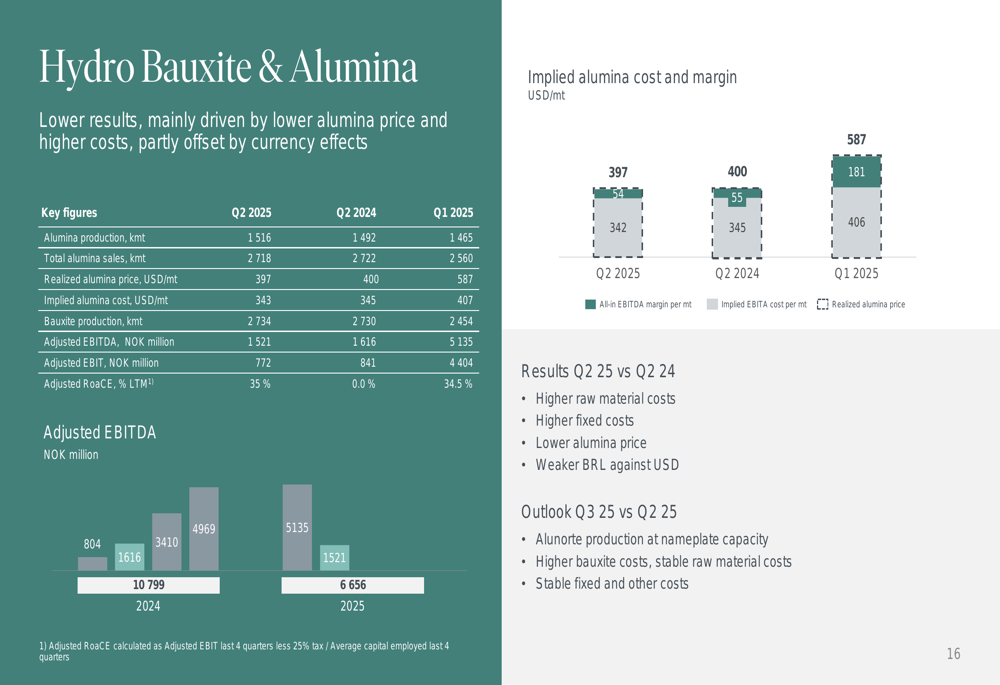

The Bauxite & Alumina (OTC:AWCMY) segment reported an adjusted EBITDA of NOK 1,521 million and an adjusted RoaCE of 35%. Alumina production reached 1,516 kmt, with a realized alumina price of USD 397/mt. The outlook for Q3 indicates Alunorte production at nameplate capacity but with higher bauxite costs.

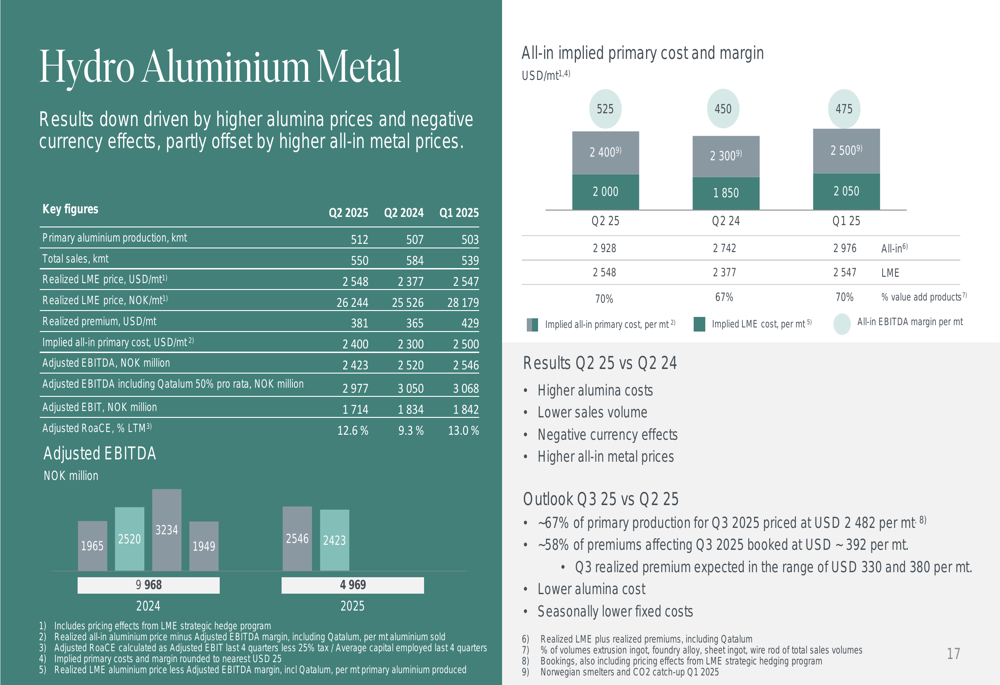

The Aluminium Metal segment posted an adjusted EBITDA of NOK 2,423 million and an adjusted RoaCE of 12.6%. Primary aluminum production was 512 kmt, with a realized LME price of USD 2,548/mt. Results were negatively impacted by higher alumina prices and currency effects, partially offset by higher all-in metal prices.

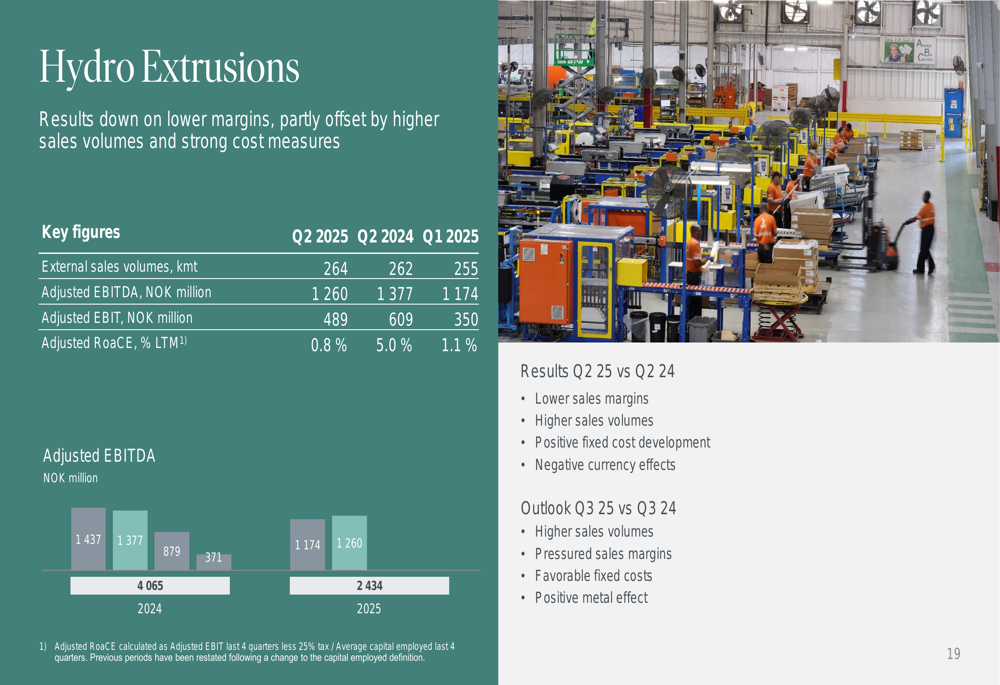

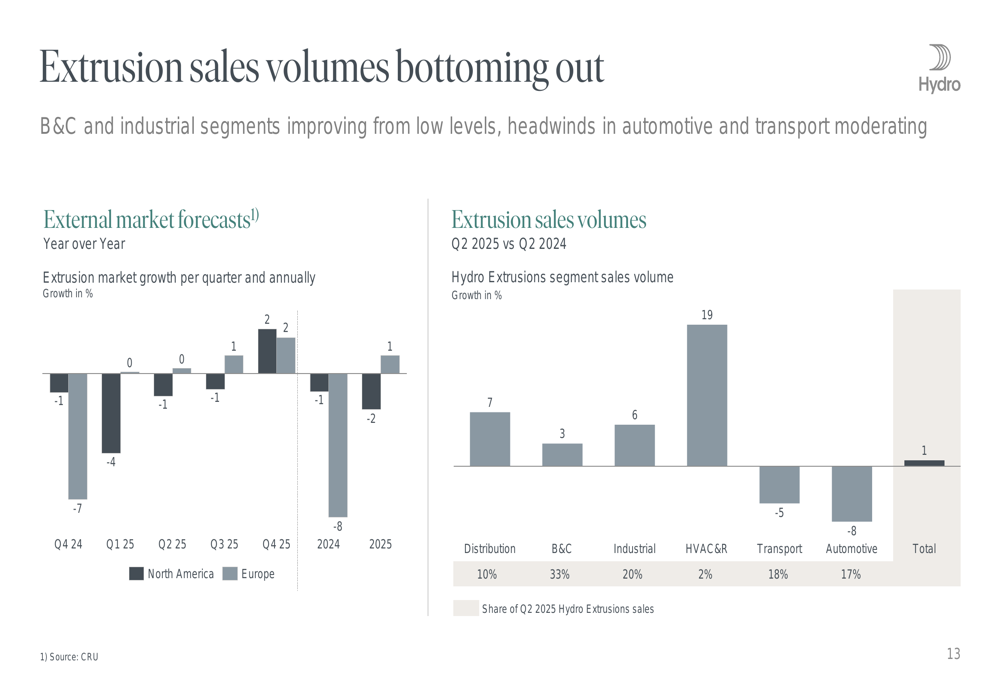

The Extrusions segment showed signs of stabilization with adjusted EBITDA of NOK 1,260 million, though RoaCE remained low at 0.8%. External sales volumes reached 264 kmt, with building and construction (B&C) and industrial segments improving, while automotive and transport headwinds are moderating.

The following chart shows extrusion sales volumes by segment, indicating a bottoming out of the market:

The Energy segment delivered an adjusted EBITDA of NOK 1,069 million with an adjusted RoaCE of 16.5%. Power production reached 2,136 GWh, with higher prices and volume contributing positively to results.

Strategic Initiatives and Cost-Cutting Measures

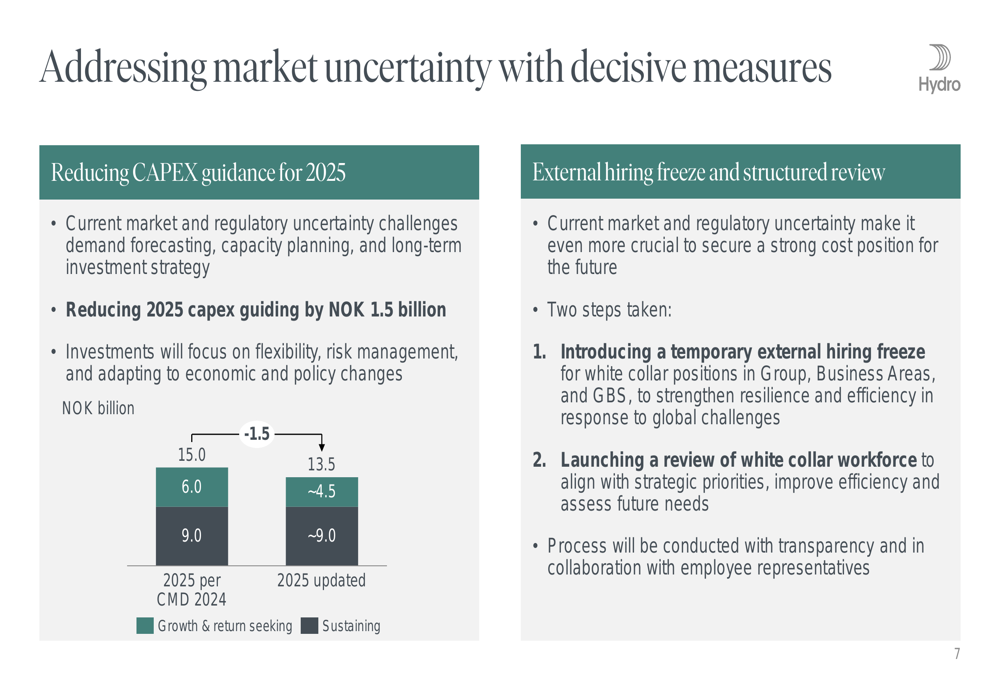

In response to market uncertainty, Norsk Hydro announced several cost-cutting measures, including a reduction in its 2025 capital expenditure target by NOK 1.5 billion, from NOK 15.0 billion to NOK 13.5 billion. The company is also implementing an external hiring freeze for white-collar positions and launching a structured review of its white-collar workforce.

The following chart illustrates the CAPEX reduction:

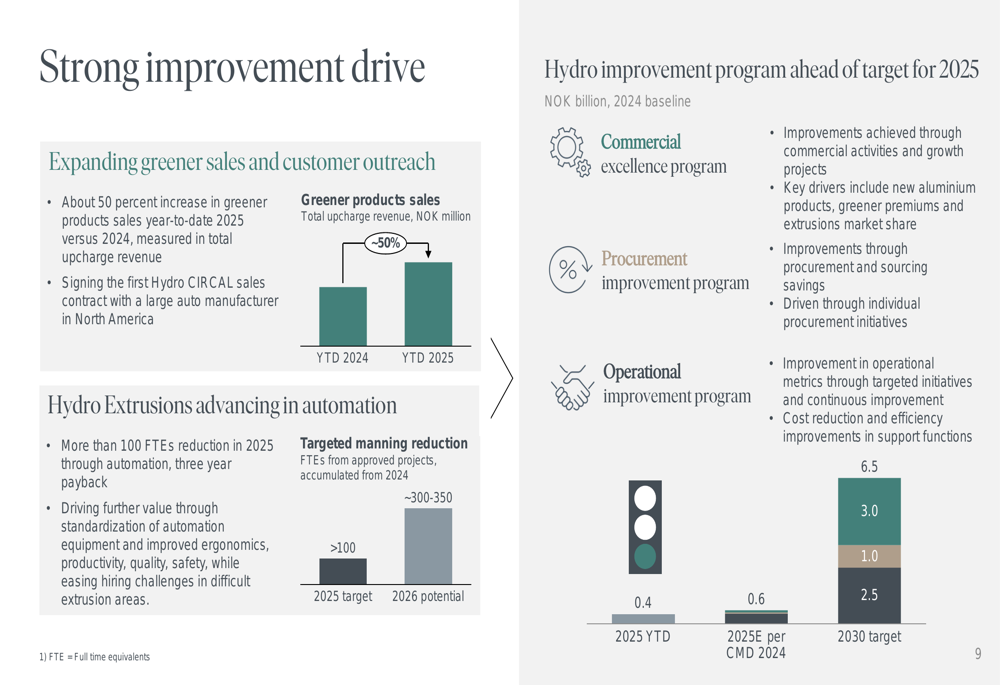

Despite these measures, Norsk Hydro continues to advance its strategic initiatives. The company reported approximately 50% increase in greener products sales year-to-date 2025 compared to 2024, and is targeting a manning reduction of 300-350 full-time equivalents (FTEs) from approved automation projects.

The Hydro improvement program has achieved NOK 0.4 billion year-to-date 2025, with a target of NOK 6.5 billion by 2030. This represents progress toward the 2025 estimate of NOK 0.6 billion announced at the Capital Markets Day 2024.

In its power sourcing strategy, Norsk Hydro terminated undelivered volumes from Swedish Cloud Snurran AB since November 2024 and reached an agreement for voluntary termination of a power purchase agreement in July 2025, entitling the company to up to EUR 90 million in compensation. The company also reported approximately NOK 400 million in impairments in Brazilian energy assets.

Forward-Looking Statements

Looking ahead, Norsk Hydro outlined several priorities for navigating the uncertain market environment:

1. Maintaining health and safety as the top priority

2. Preserving robustness while maneuvering uncertain markets

3. Delivering on recycling, extrusions, and renewable growth ambitions

4. Executing on decarbonization and technology roadmap

5. Seizing opportunities in greener aluminum at premium pricing

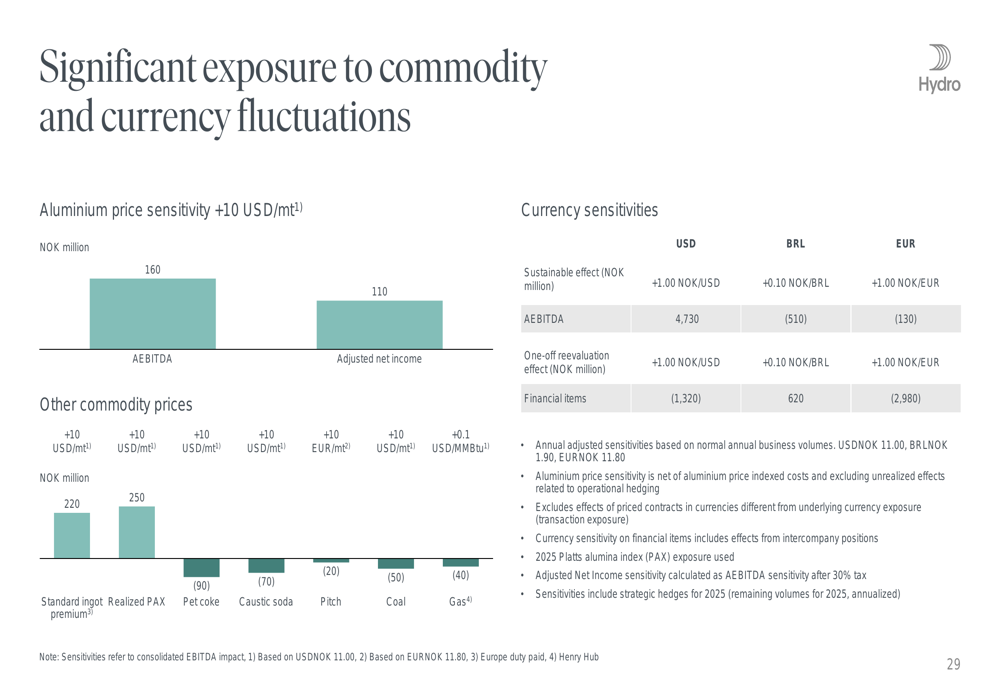

The company’s exposure to commodity and currency fluctuations remains significant, as illustrated in the following sensitivity analysis:

For Q3 2025, Norsk Hydro expects Alunorte production to remain at nameplate capacity with stable raw material costs. The company anticipates seasonally lower recycling volumes, lower results from sourcing and trading activities, and continued volatile trading and currency effects. In the Energy segment, lower production, net spot sales, and prices are expected compared to Q2 2025.

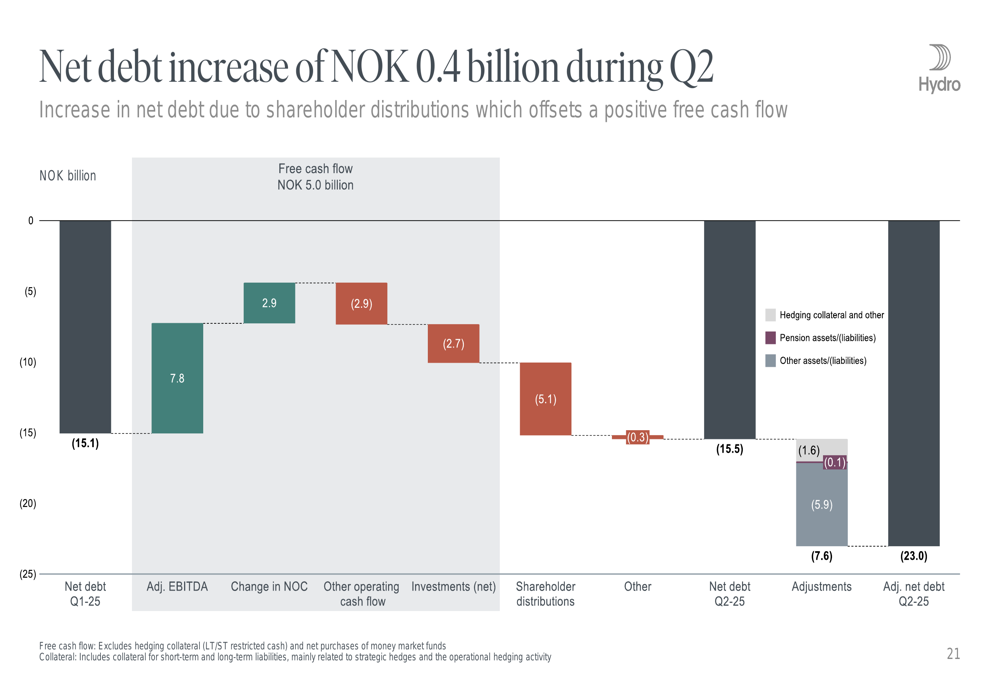

The company’s net debt increased by NOK 0.4 billion during Q2, as shareholder distributions offset positive free cash flow:

This more cautious outlook represents a shift from the robust performance reported in Q1 2025, when the company saw a 20% year-over-year increase in revenue to NOK 57 billion and strong adjusted net income of NOK 4 billion. The implementation of cost-cutting measures suggests Norsk Hydro is preparing for a more challenging market environment in the second half of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.