Tonix Pharmaceuticals stock halted ahead of FDA approval news

Introduction & Market Context

North American Construction Group (NYSE:NOA) released its first quarter 2025 earnings presentation on May 15, revealing mixed results that drove the stock down 14.72% in premarket trading to $14.31. While the company achieved 13.3% revenue growth, profitability metrics declined significantly year-over-year, with adjusted EPS falling 34.2% and net income dropping by half.

The company continues to execute its geographic diversification strategy, with Australian operations now generating 65% of earnings, up from previous quarters. However, weather challenges in both Australia and Canada impacted margins and equipment utilization during the quarter.

Quarterly Performance Highlights

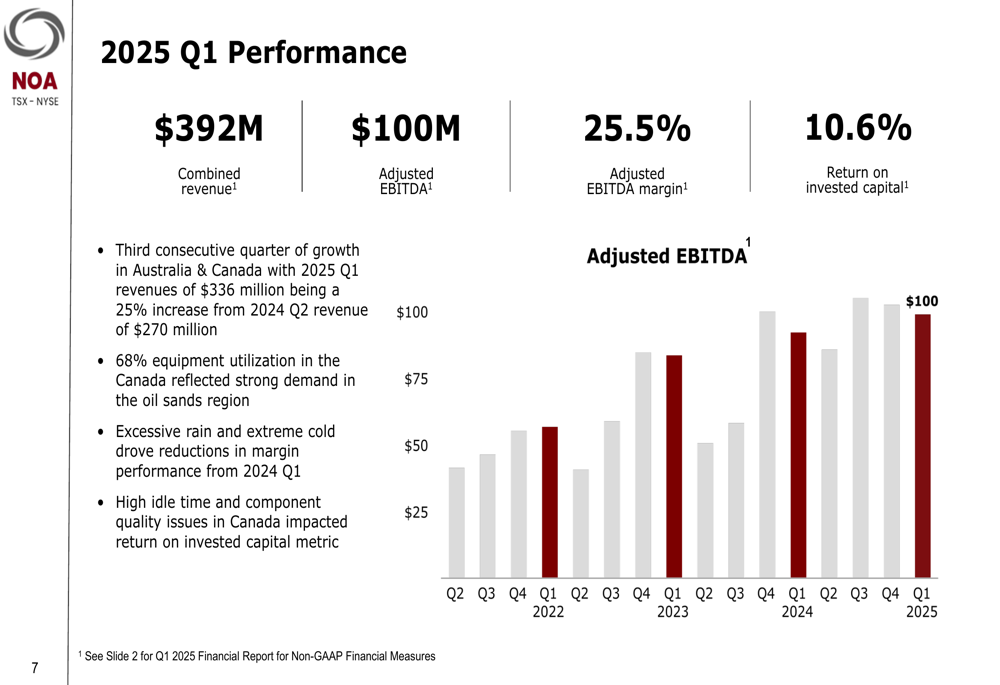

North American Construction Group reported Q1 2025 combined revenue of $392 million, up 13.3% from $346 million in Q1 2024. Despite this growth, adjusted EBITDA margin compressed to 25.5% from 28.2% in the prior year period, while adjusted EPS fell to $0.52 from $0.79.

As shown in the following chart of quarterly performance:

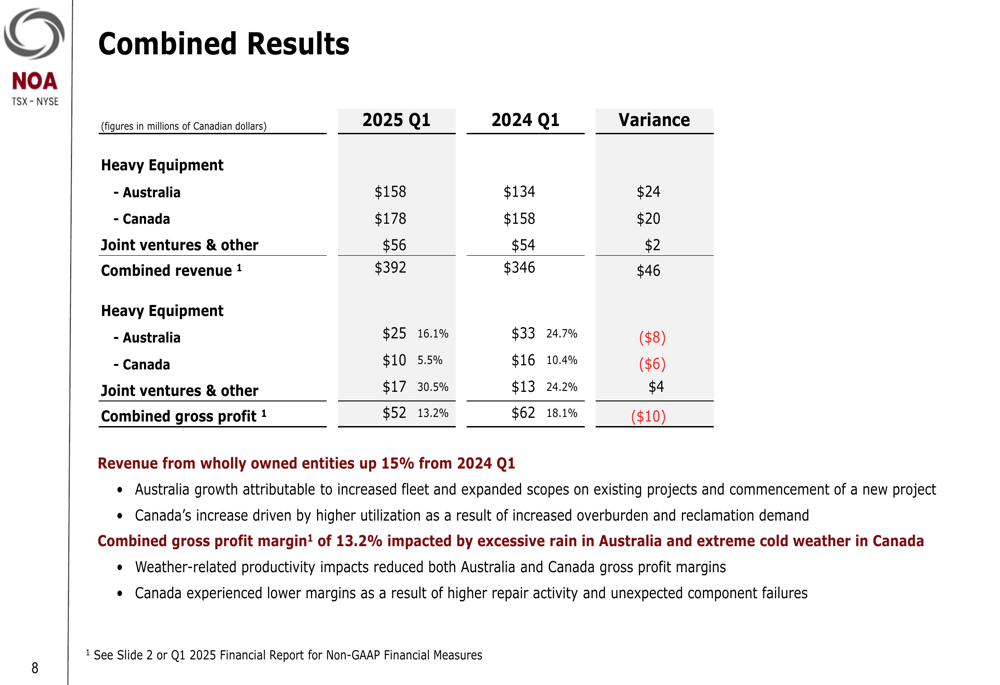

The company’s combined results breakdown reveals that Heavy Equipment operations in Australia generated $158 million in revenue with a gross profit of $25 million (16.1% margin), while Canadian operations contributed $178 million with a gross profit of $10 million (5.5% margin). Joint Ventures & Other added $56 million in revenue with $17 million in gross profit (30.5% margin).

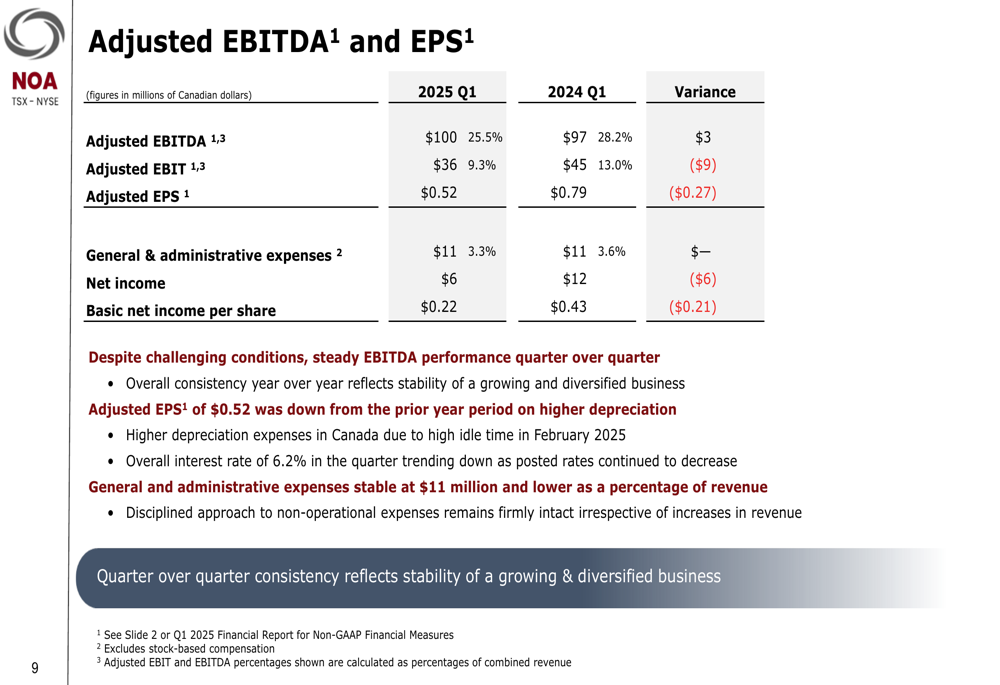

The decline in profitability metrics is further illustrated in the adjusted EBITDA and EPS comparison:

Management attributed the margin compression to excessive rainfall in Australia and cold weather in Canada, which negatively impacted equipment utilization and operational efficiency.

Operational Performance

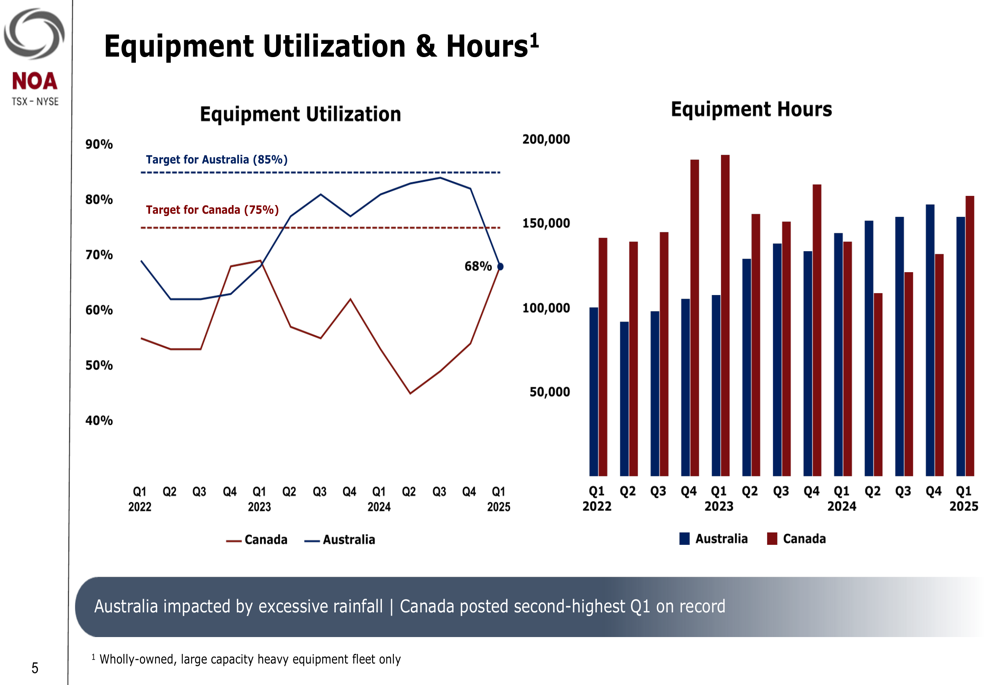

Equipment utilization in the Canadian oil sands region reached 68% in Q1 2025, below the company’s target of 75% but showing improvement with 70% utilization achieved in February. The company noted that Australia was impacted by excessive rainfall, while Canada posted its second-highest Q1 equipment hours on record.

The following chart illustrates equipment utilization and hours trends:

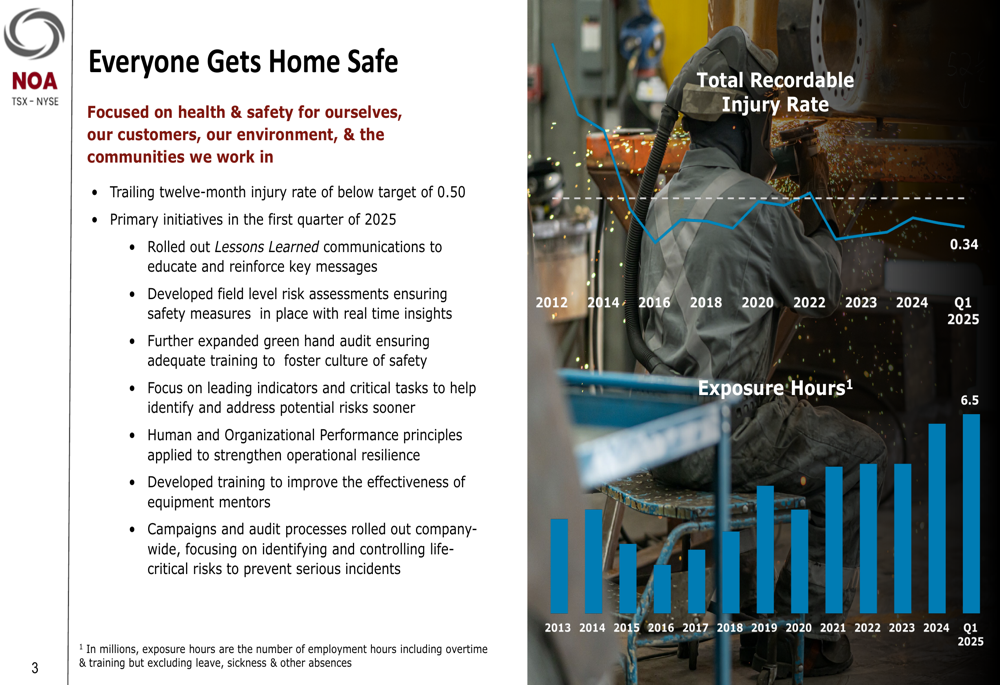

The company continues to prioritize safety, reporting a trailing twelve-month injury rate below its target of 0.50. Key safety initiatives in Q1 included expanding green hand audits, focusing on leading indicators, and implementing company-wide audit processes.

Balance Sheet and Cash Flow

Cash provided by operating activities improved significantly to $51 million in Q1 2025, compared to $19 million in Q1 2024, driven by strong EBITDA performance and improved working capital management. However, free cash flow remained negative at $(42) million due to front-loaded capital maintenance programs.

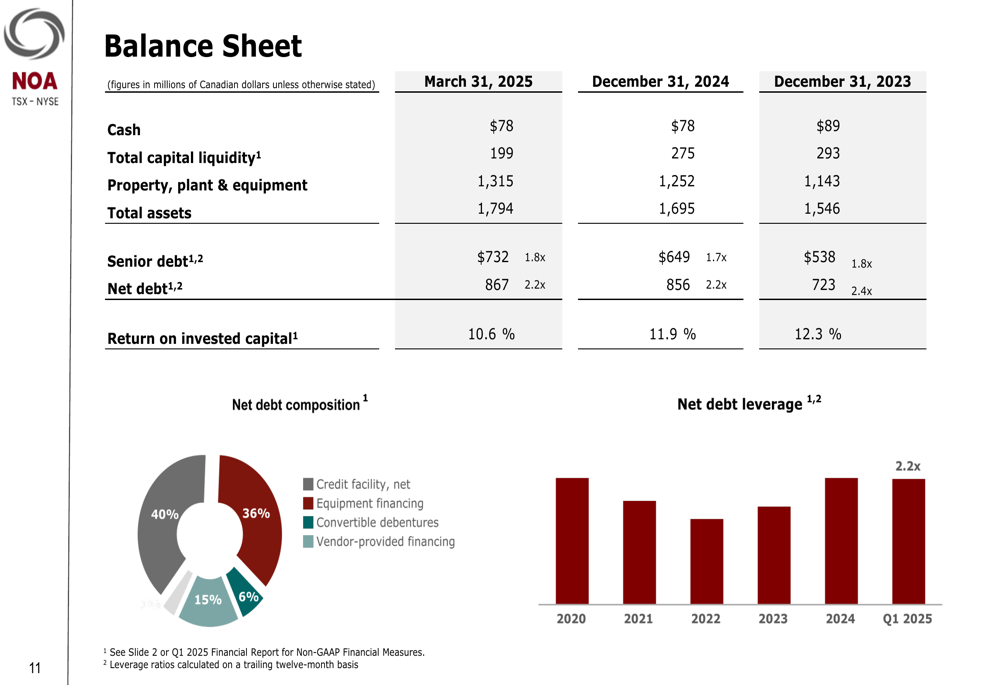

As of March 31, 2025, North American Construction Group reported total assets of $1,794 million, with property, plant, and equipment valued at $1,315 million. The company’s net debt stood at $867 million, representing a leverage ratio of 2.2x, while total capital liquidity was $199 million, down from $275 million at the end of 2024.

The following slide provides key balance sheet highlights:

Geographic Diversification Strategy

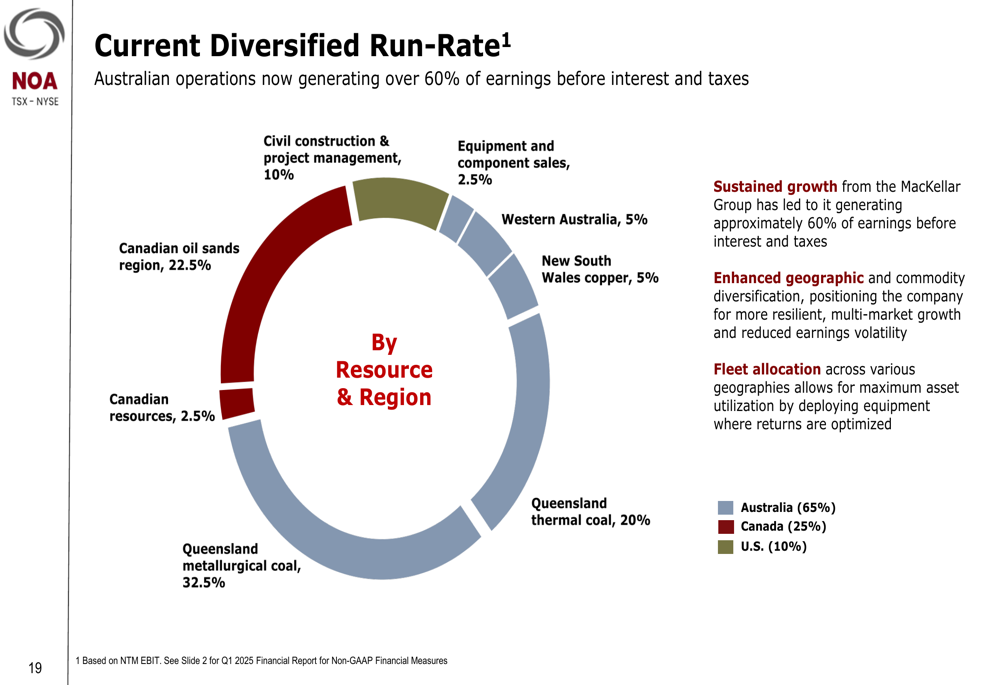

North American Construction Group continues to make significant progress on its geographic diversification strategy, with Australian operations now generating 65% of earnings before interest and taxes, compared to 25% from Canada and 10% from the U.S.

The company’s current diversified run-rate by geography and resource is illustrated below:

This diversification has been driven by the company’s expansion in Australia through its MacKellar Group subsidiary, which now serves metallurgical coal (32.5% of earnings), thermal coal (20%), copper (5%), and Western Australia operations (5%).

Market Opportunities and Future Outlook

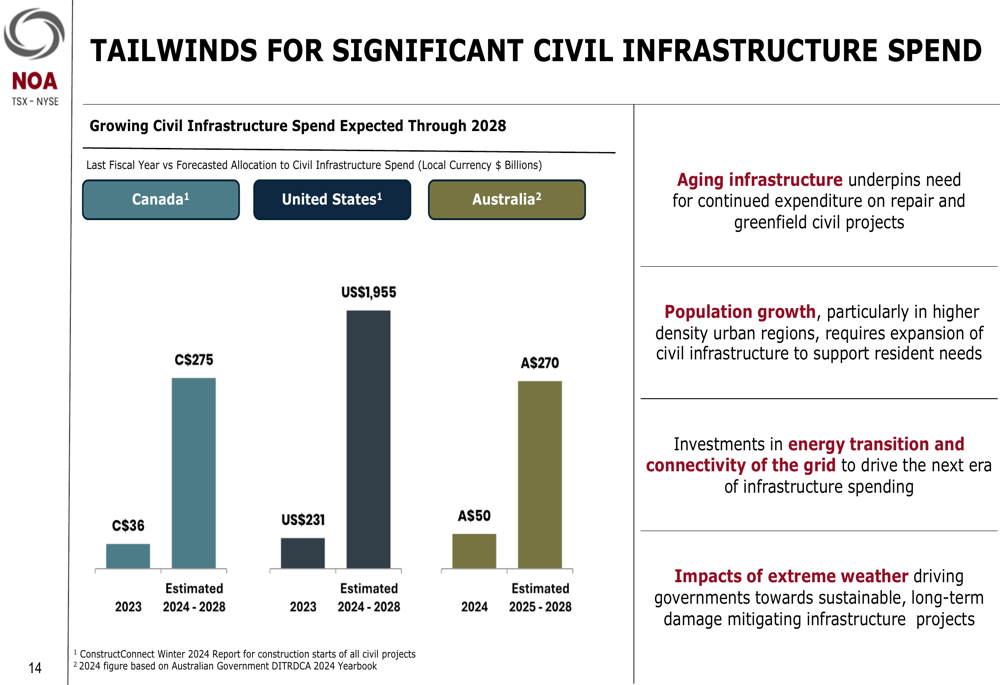

North American Construction Group highlighted significant tailwinds for civil infrastructure spending through 2028, with estimated expenditures of C$275 billion in Canada, $1,955 billion in the U.S., and A$270 billion in Australia. Key drivers include aging infrastructure, population growth, investments in energy transition, and impacts of extreme weather.

The following chart illustrates these infrastructure spending projections:

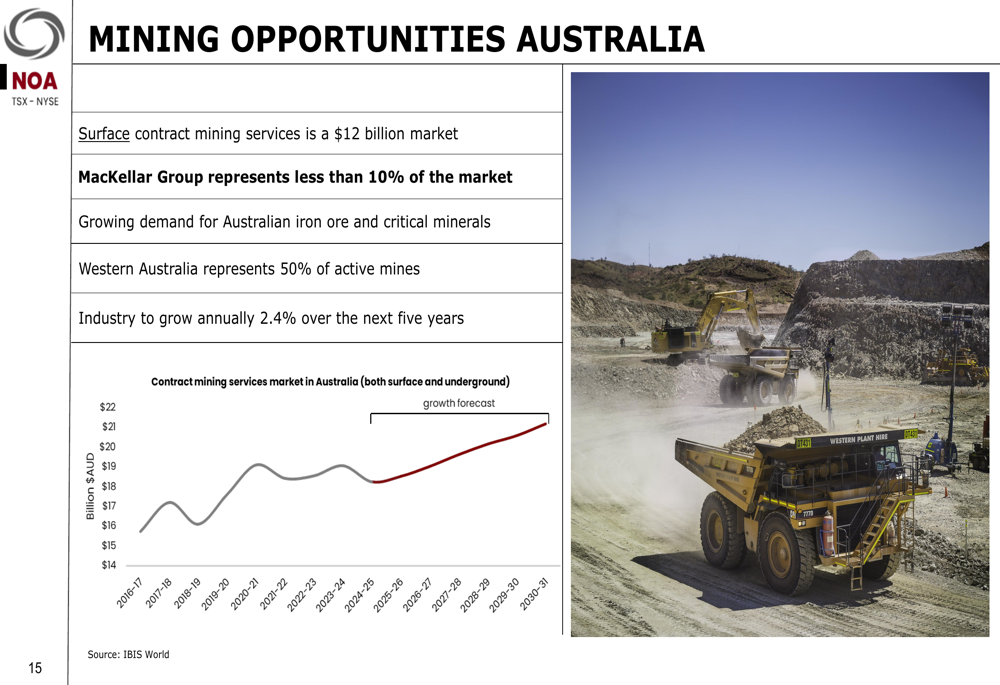

In Australia, the company sees substantial mining opportunities, noting that surface contract mining services represent a $12 billion market, with MacKellar Group currently holding less than 10% market share. The Australian mining market is expected to grow at 2.4% annually over the next five years.

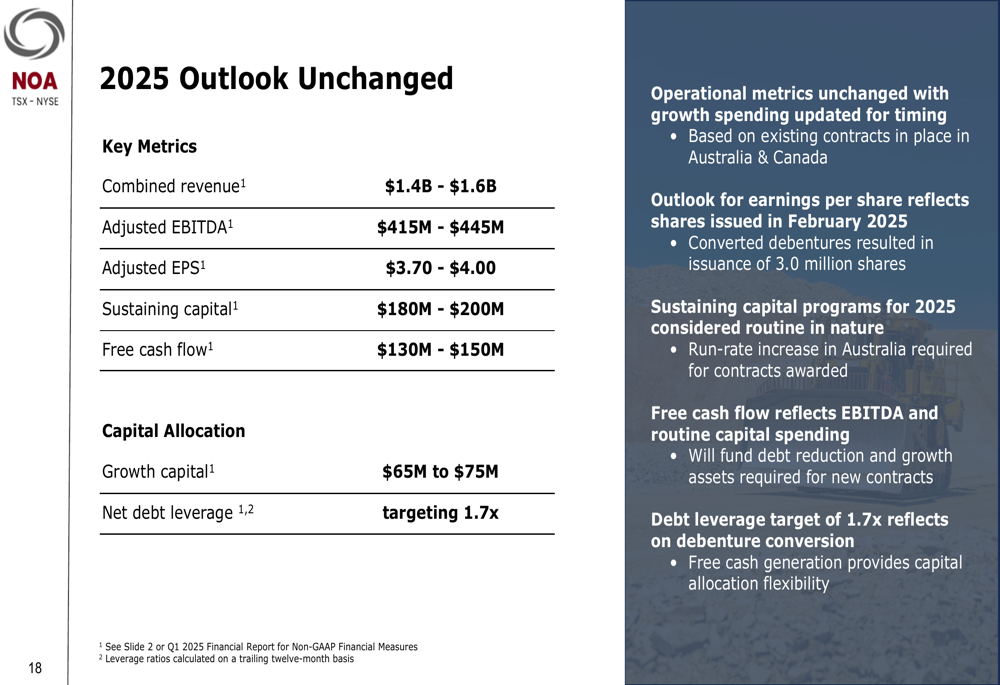

For 2025, North American Construction Group maintained its outlook, projecting combined revenue of $1.4-$1.6 billion, adjusted EBITDA of $415-$445 million, and adjusted EPS of $3.70-$4.00. The company expects to generate free cash flow of $130-$150 million and targets a net debt leverage ratio of 1.7x by year-end.

Strategic Initiatives

Looking ahead, North American Construction Group outlined six key priorities for 2025, including enhancing safety systems, increasing equipment utilization, geographic diversification outside of Queensland and Alberta, focusing on customer satisfaction, leveraging ERP systems to optimize business processes, and expanding maintenance and component rebuild services for third-party customers.

The company’s contractual backlog stands at $3.2 billion, down from $3.5 billion at year-end as $300 million was converted to revenue in Q1. Management expects the backlog to remain above $3.0 billion due to a strong bid pipeline exceeding $10 billion of specific scopes of work.

With its heavy equipment fleet of approximately 1,200 assets valued at ~$3.8 billion, North American Construction Group is well-positioned to capitalize on growth opportunities across its diversified geographic footprint, despite the profitability challenges experienced in Q1 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.