Tonix Pharmaceuticals stock halted ahead of FDA approval news

Introduction & Market Context

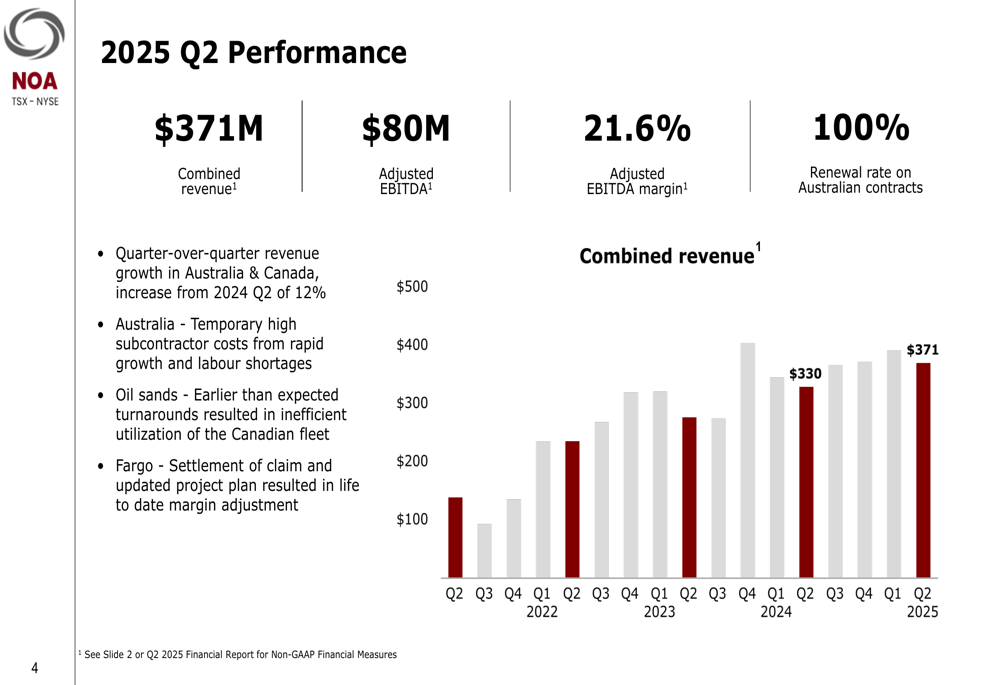

North American Energy Partners Inc (NYSE:NOA) released its Q2 2025 earnings presentation on August 14, 2025, revealing mixed results with strong revenue growth offset by declining profitability metrics. The company reported a 12% increase in combined revenue to $371 million compared to $330 million in Q2 2024, while simultaneously lowering its full-year guidance for adjusted EBITDA and EPS.

The stock had closed at $16.48 on August 13, up 1.76% ahead of the earnings release, with modest after-hours trading gains of 0.73%. This follows a pattern seen after Q1 results, when investors responded positively despite an EPS miss, suggesting continued confidence in the company’s long-term growth strategy despite near-term profitability challenges.

Quarterly Performance Highlights

North American Energy’s Q2 2025 results showed revenue growth in both its Australian and Canadian operations, with Australia continuing to lead company expansion with a 30% compound annual growth rate (CAGR).

As shown in the following chart of quarterly revenue performance:

Key financial metrics for Q2 2025 included:

- Combined revenue of $371 million, up from $330 million in Q2 2024

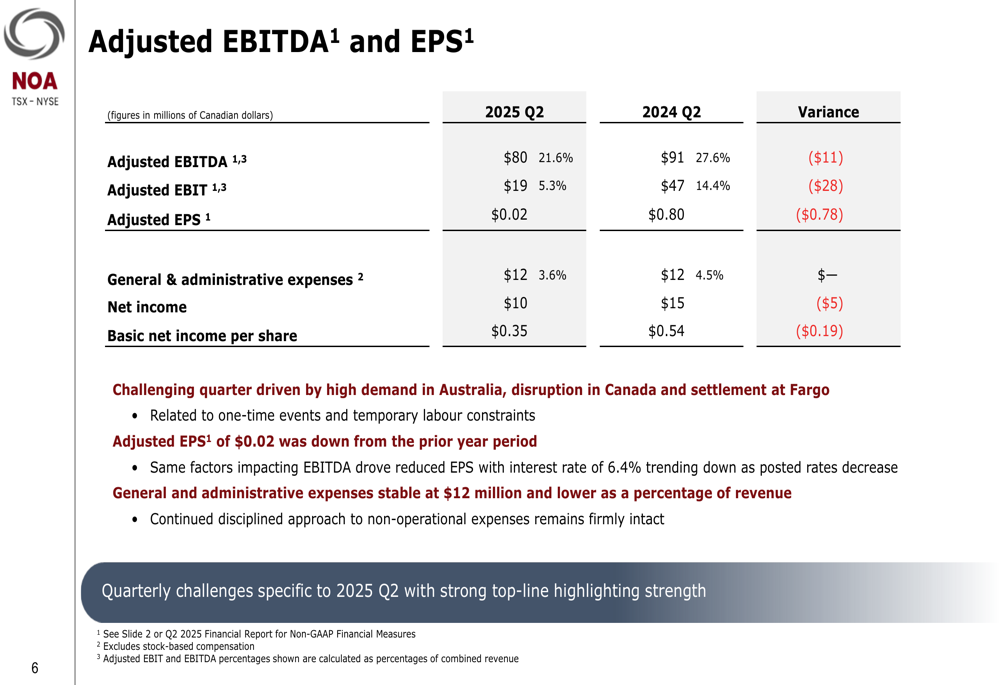

- Adjusted EBITDA of $80 million (21.6% margin), down from $91 million (27.6%) in Q2 2024

- Adjusted EPS of $0.02, significantly down from $0.80 in Q2 2024

- Cash provided by operating activities of $65 million, relatively flat compared to $66 million in Q2 2024

The company achieved several operational milestones during the quarter, including signing a $2.0 billion contract in Queensland, progressing the Fargo project past 70% completion, and renewing a mine management contract in Texas extending to 2028. Equipment utilization remained strong at 74%, approaching the company’s target range of 75-80%.

Detailed Financial Analysis

While revenue growth was robust, profitability metrics showed significant pressure. The adjusted EBITDA margin declined from 27.6% in Q2 2024 to 21.6% in Q2 2025, while adjusted EBIT fell from $47 million to $19 million. This profitability decline was attributed to labor constraints driven by high demand in Australia, stoppages at customer sites in Canada, and settlement costs related to the Fargo project.

The following table details the company’s adjusted EBITDA and EPS performance:

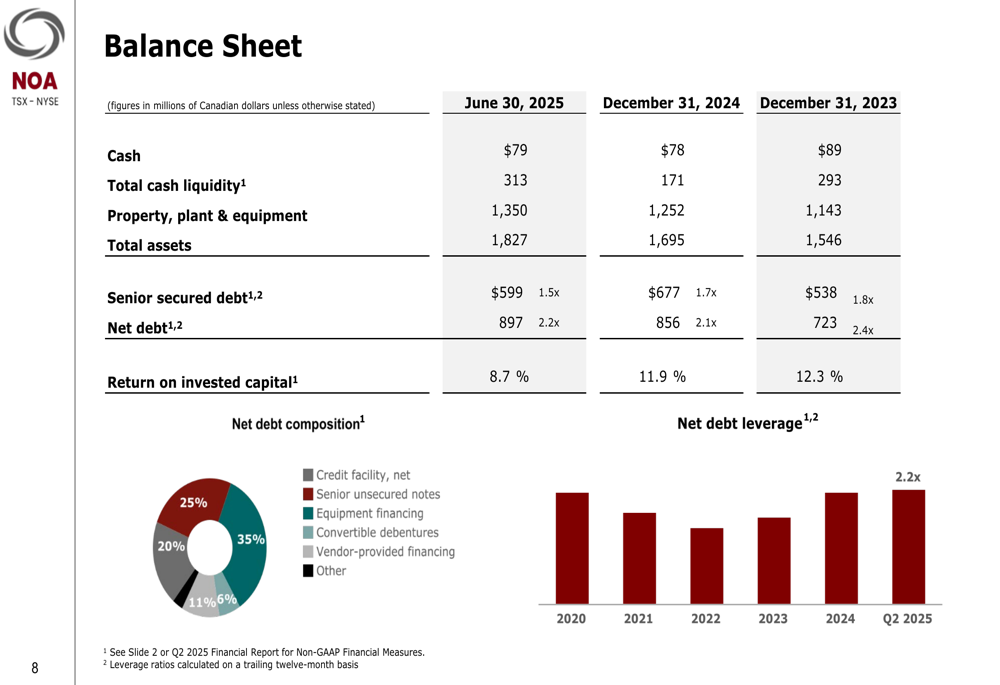

The balance sheet showed increasing leverage, with net debt rising to $897 million (2.2x leverage) as of June 30, 2025, compared to $856 million (2.1x) at the end of 2024. Return on invested capital declined to 8.7% from 11.9% in December 2024.

The company’s debt composition and leverage trends are illustrated below:

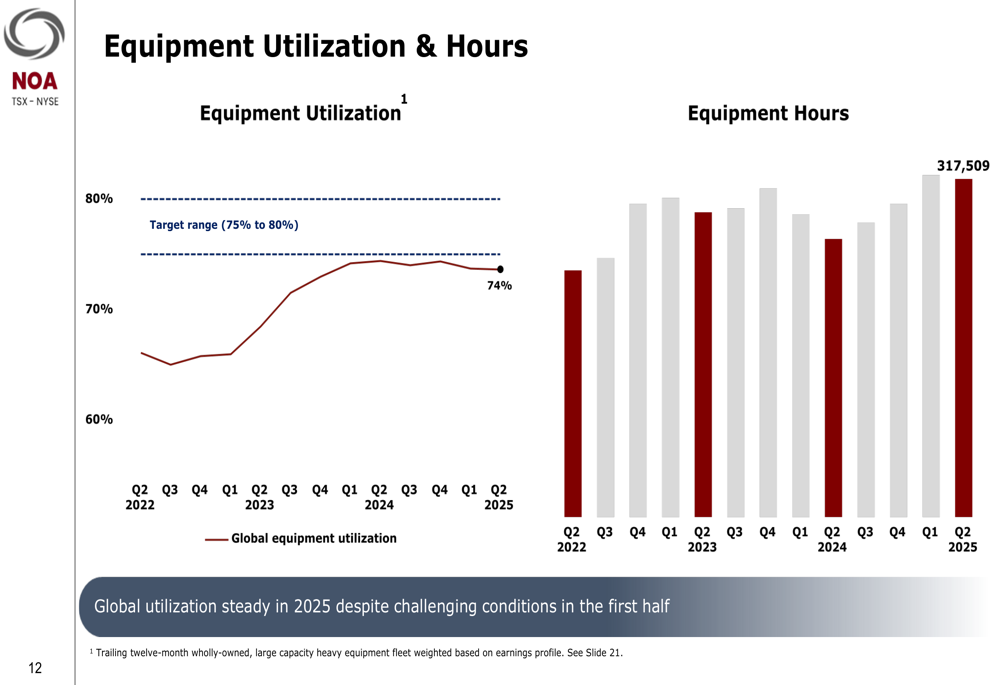

Equipment utilization remained a bright spot, with global utilization holding steady at 74% despite challenging conditions in the first half of 2025. Equipment hours continued to grow, reaching 317,509 in Q2 2025.

Strategic Initiatives

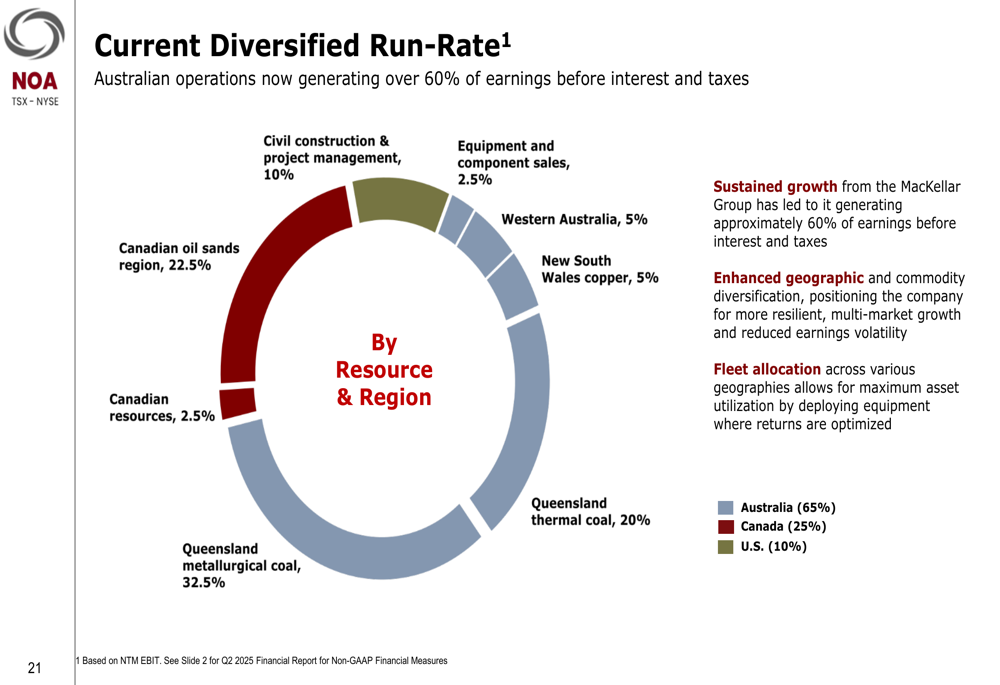

North American Energy continues to focus on growth in Australia, which now generates over 60% of the company’s earnings before interest and taxes. The company’s diversified revenue stream spans multiple resources and geographies, with Queensland metallurgical coal (32.5%), Canadian oil sands (22.5%), and Queensland thermal coal (20%) representing the largest segments.

The company’s revenue diversification is illustrated in the following breakdown:

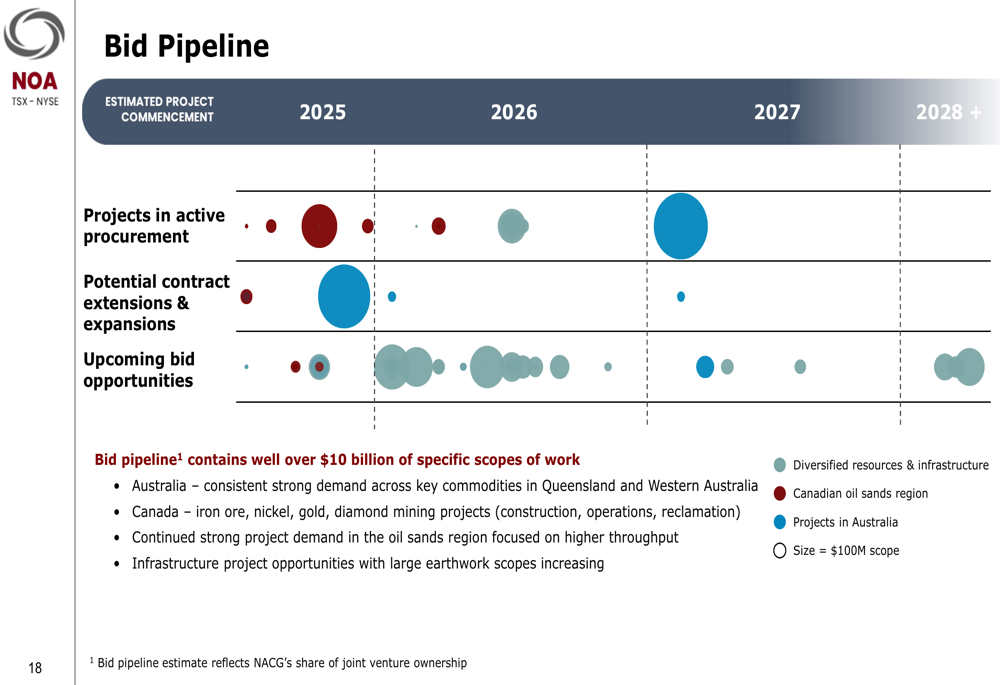

The company highlighted its robust bid pipeline worth over $10 billion, with particularly strong demand across key commodities in Queensland and Western Australia. This pipeline includes active procurement projects, potential contract extensions, and upcoming bid opportunities.

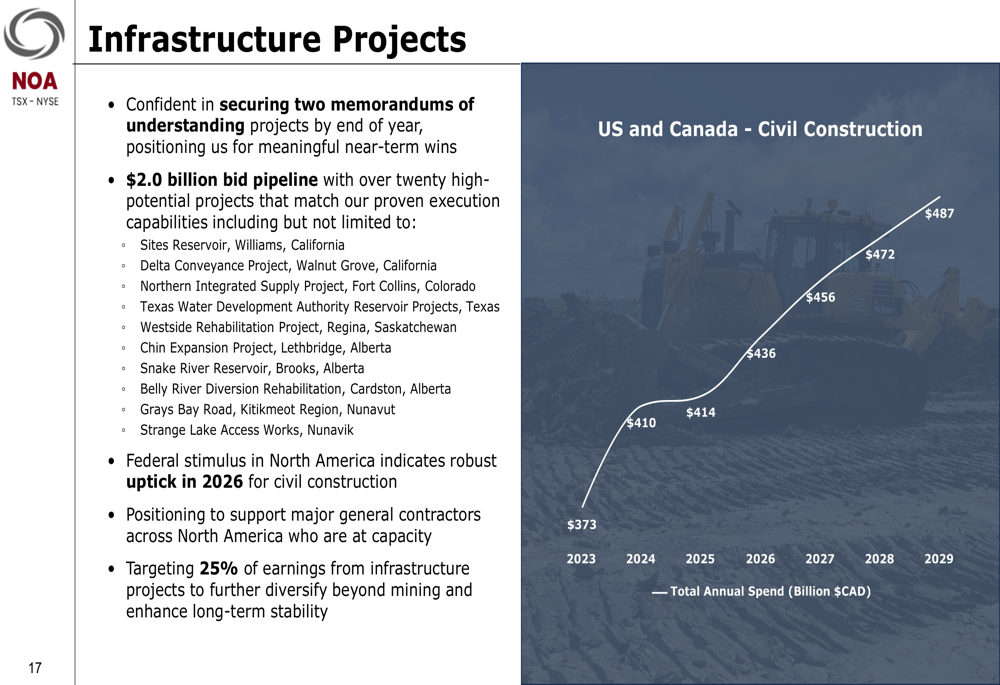

North American Energy is also pursuing growth in infrastructure projects, with a $2 billion bid pipeline. The company expects total annual infrastructure spending to grow steadily through 2029, presenting significant opportunities for expansion beyond its traditional mining services business.

Forward-Looking Statements

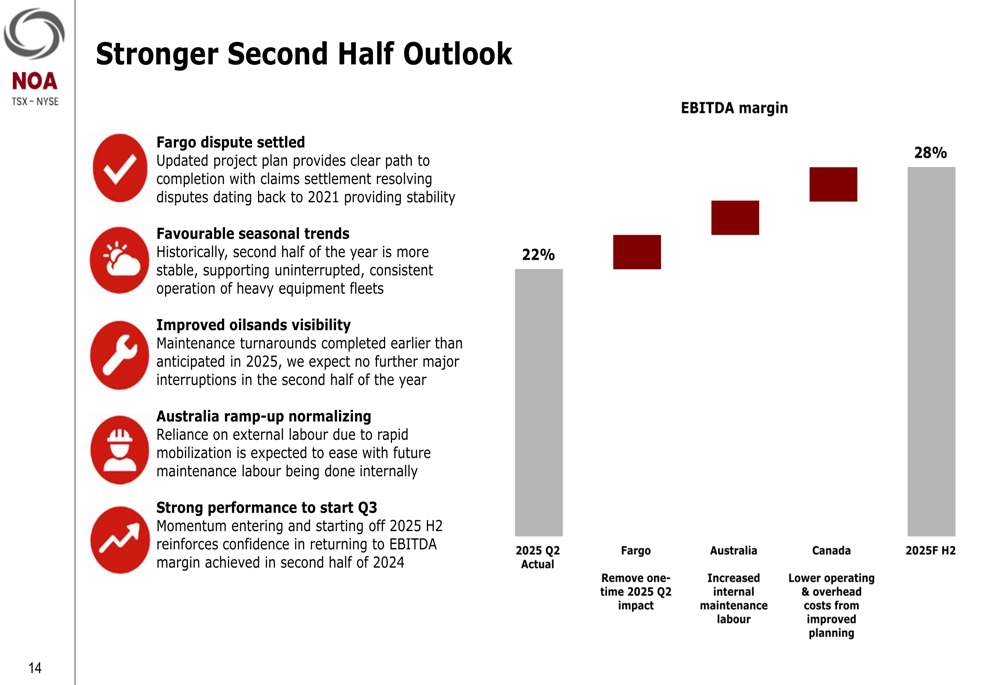

Despite challenges in the first half of 2025, North American Energy projects stronger performance in the second half of the year, with EBITDA margins expected to improve from 22% in Q2 to 28% in H2 2025. This improvement is anticipated due to several factors including normalized operations in Australia, improved labor availability, and the completion of turnarounds in Canada.

The expected EBITDA margin improvement is shown in the following chart:

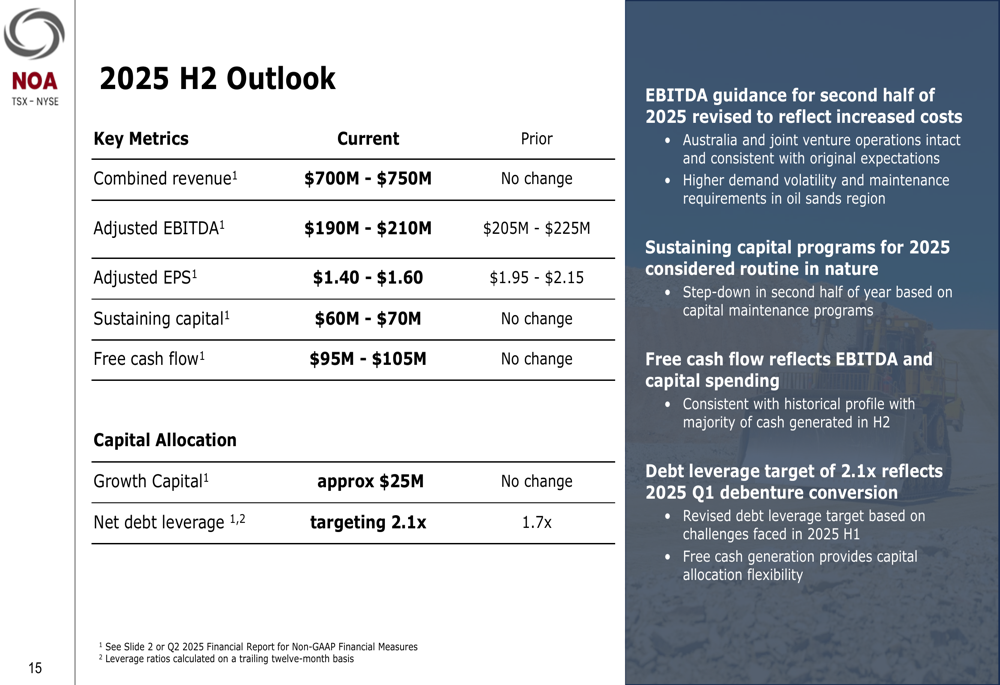

However, the company has revised its full-year guidance downward:

- Adjusted EBITDA: $190M - $210M (previously:$205M - $225M)

- Adjusted EPS: $1.40 - $1.60 (previously:$1.95 - $2.15)

- Net debt leverage: targeting 2.1x (previously:1.7x)

The company maintained its guidance for combined revenue ($700M - $750M), sustaining capital ($60M - $70M), free cash flow ($95M - $105M), and growth capital (approximately $25M).

This guidance revision follows a pattern seen in Q1 2025, when the company reported an EPS of $0.21 against a forecast of $0.83, suggesting ongoing challenges in translating revenue growth into bottom-line performance.

Despite these near-term profitability pressures, North American Energy remains focused on its long-term growth strategy, particularly in Australia where the contract mining services market is projected to grow steadily through 2030. The company’s strong contract renewal rate (100% in Australia) and substantial bid pipeline provide a foundation for future growth, though investors will be watching closely to see if management can deliver on its projected second-half improvement in profitability metrics.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.